Actual U.S. Corporate Tax Rates Are in Line with Comparable Countries

The tax framework that the Trump Administration and congressional Republican leaders announced on September 27 would dramatically lower the top corporate tax rate, from 35 percent to 20 percent. President Trump has argued that the U.S. rate is among the world’s highest and makes U.S. companies “uncompetitive.” These comparisons are misleading. Rather than focusing on the top statutory rate, they should focus on what companies actually pay. And they should focus on large, high-income countries, which companies likely view as similar to the United States as potential places to locate and invest in for non-tax reasons. After accounting for tax breaks and loopholes, U.S. corporate rates are well below the 35 percent top statutory rate and are in line with corporate rates in similar countries. The Treasury Office of Tax Analysis estimates:[1]

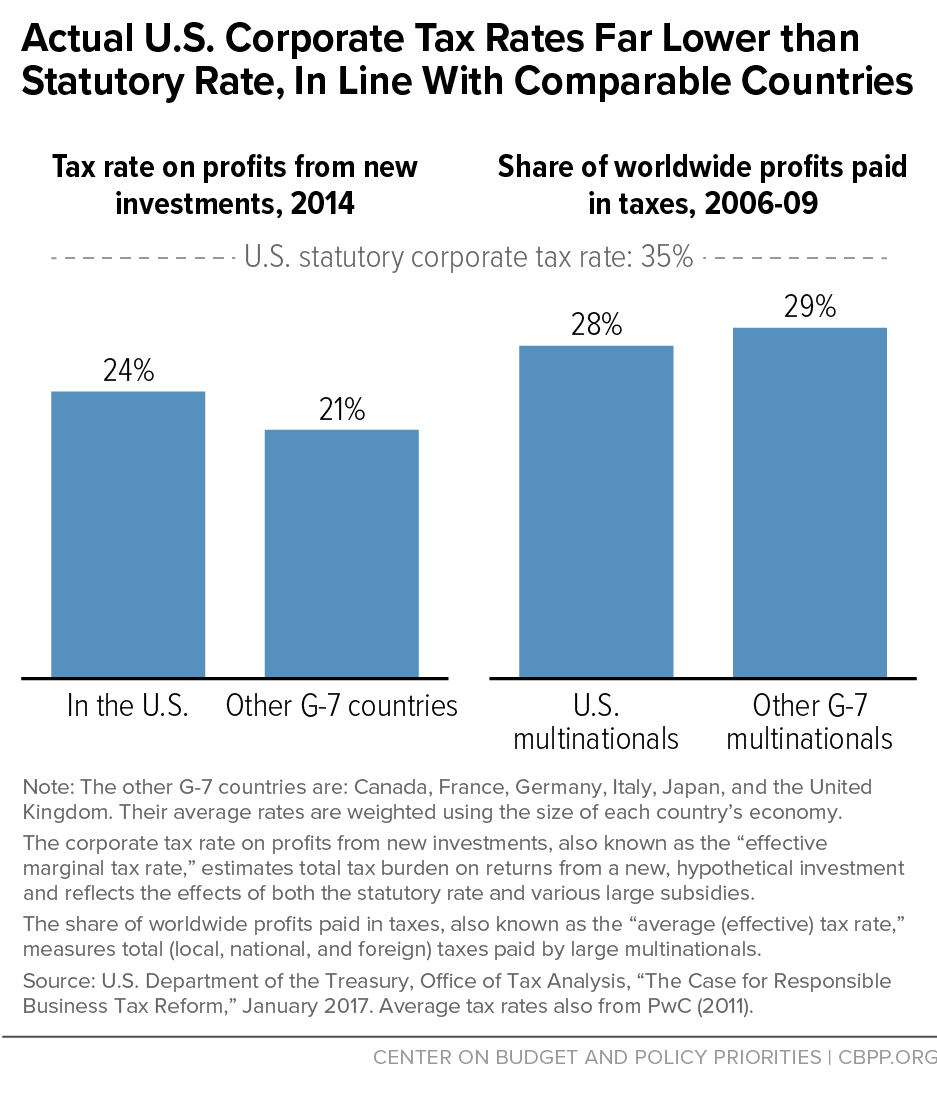

- The average corporate tax rate on profits from new investments made in the U.S. is 24 percent; the average corporate rate on profits from new investments made by companies in other “Group of Seven” (G-7) industrialized, democratic countries, weighted by the size of their economies, is 21 percent. This measure of tax rates is useful when considering how corporate taxes affect companies’ decisions about where to make new investments.

- The share of worldwide profits that U.S. multinational corporations pay in U.S. and foreign income taxes is about 28 percent; the average for companies headquartered in other G-7 countries, weighted by the size of their economies, is 29 percent. This measure of tax rates that a multinational might face on its income from all countries is useful for considering how corporate taxes might affect where multinationals choose to reside for tax purposes. (See chart.)

The Statutory Rate Isn’t an Appropriate Comparison

Comparisons of corporate tax rates should focus on the measures that reflect what companies actually pay, not the top statutory rate. Proponents of slashing the corporate tax rate often note the U.S. statutory tax rate is the highest among developed countries. But many U.S. companies use an array of targeted tax breaks and loopholes to significantly lower the taxes they pay. These include tax subsidies for certain types of investments (such as in research and development) and for particular industries (such as oil and gas).

The Joint Committee on Taxation estimates that in 2016, while the corporate income tax raised $300 billion in revenues, targeted subsidies delivered to companies through the corporate tax code cost about $270 billion. As a result of these subsidies and other tax avoidance measures, many large U.S. companies pay very low rates. For example, Pfizer paid a rate of about 7.5 percent on its $12 billion in worldwide pre-tax income in 2014. Studies generally also find that U.S. companies’ tax rates vary widely by industry and type of investment.

Comparisons Should Be Made With Similar Countries

Comparisons of corporate tax rates should focus on large, high-income countries, and should take into account the size of the countries’ economies when calculating international averages:

- Large, high-income countries such as the G-7 are likely to be most similar to the United States in terms of their public infrastructure, the workforce’s education and skills, and political structure and stability. These factors are what make these countries attractive places for companies to locate in and invest, regardless of their tax rates. By contrast, a developing country with an economic output per person that’s a fraction of the size of the United States and with much lower public investments is not a fair comparison.

- As the non-partisan Congressional Research Service (CRS) explains, “If tax rates are not weighted, then a small economy, such as Iceland, can have the same effect on the average of international rates as a large economy, such as Germany or Japan,” and, “Because small countries tend to have lower rates than large ones, comparing rates using simple averages across countries exaggerates the differential between the United States and tax burdens elsewhere in the world.”

- The CRS examined studies that compare U.S. tax rates with those of other countries — including those commonly cited as showing that even actual U.S. corporate tax rates are high by international standards. The CRS found that most of the difference between the actual U.S. corporate rate and the international average disappears when using appropriate countries and weights. A Treasury study (discussed above) came to a similar conclusion.

Corporate Rate Cuts a Poor Way to Grow the Economy

The erroneous international comparisons of corporate tax rates are often coupled with arguments that cutting the U.S. corporate tax rate would help create jobs and growth. In fact:

- The case for slashing corporate tax rates is thin: U.S. companies are posting near-record profits, and little suggests that corporate taxes — or poor corporate profitability — are a major constraint for the U.S. economy.

- Most of the benefit of corporate rate cuts flows to high-income investors rather than “trickling down” to workers in the form of higher wages, and the cuts are costly: Reducing the corporate tax rate to 15 percent, as President Trump has proposed, would cost more than $2 trillion over ten years. Such a tax cut could hurt the majority of Americans if it permanently increased deficits (which can slow economic growth in the long run, according to the Congressional Budget Office) or its high cost is paid for with large cuts to investments that help working families.[2]

- Rather than slashing the corporate tax rate, true corporate tax reform that addressed inefficient corporate tax breaks, loopholes, and the tilt of the tax code towards debt and foreign profits would be more likely to foster growth. Such reform could help investments flow to where they are most productive. It could also raise revenues to reduce deficits and invest in national priorities like education and infrastructure, benefitting the economy and most Americans.

End Notes

[1] This paper primarily relies on Treasury Office of Tax Analysis (OTA) estimates in “The Case for Responsible Business Tax Reform,” January 2017, http://bit.ly/2p1Jkff, unless otherwise noted. Effective tax rate for Pfizer was estimated by Americans for Tax Fairness using the company’s Securities and Exchange Commission filings. For further discussion and comparison of estimates, see Laura Power, “The Devil is in the Details: A Comparison of the Corporate Average Effective Tax Rate Calculations Used by Government Agencies,” Office of Tax Analysis Working Paper 105, January 2016, http://bit.ly/2zdyohF and Jane G. Gravelle, “International Corporate Tax Rate Comparisons and Policy Implications,” CRS, January 6, 2014, http://bit.ly/2lRe15u.

[2] See CBPP, “Corporate Tax Cuts Mainly Benefit Shareholders and CEOs, Not Workers,” August 21, 2017, http://bit.ly/2erA9SP; CBPP, “Corporate Rate Cuts Are a Poor Way to Help the Economy and Most Workers — and Could Hurt Them,” updated June 9, 2017, http://bit.ly/2vXgX5V.