http://www.cbpp.org/3-25-99socsec.htm

Mr. Chairman and Members of the Subcommittee on Social Security:

I very much appreciate your invitation to testify on the subject of the overall budget framework and Social Security program's goals and criteria for assessing reform proposals. My name is Wendell Primus and I am Director of Income Security at the Center on Budget and Policy Priorities. The Center is a nonpartisan, nonprofit policy organization that conducts research and analysis on a wide range of issues affecting low- and moderate-income families. We are primarily funded by foundations and receive no federal funding.

The Overall Budgetary and Social Security Framework of Congressional Plans

My understanding of the overall budgetary and Social Security framework assumed under the House and Senate budget resolutions is as follows:

- Continuing to abide by the discretionary caps through 2002 and holding non-defense discretionary spending in most years after 2002 below the 2002 inflation-adjusted level (although modestly above a freeze level),

- Enacting substantial net tax cuts of $778 billion over 10 years, which would nearly equal the estimated size of the on-budget surplus over this period, and

- Using much of the Social Security surplus to establish individual account plans and employing a variant of the Feldstein approach.

I would like to comment briefly on the feasibility and economic ramifications of this framework, discuss criteria for how to judge Social Security reform and compare alternative Social Security plans under those criteria and conclude with a few thoughts on an alternative framework.

Understanding the Economic and Budgetary Implications of this Framework

What we have learned over the past several weeks about the Senate and House budget resolutions is cause for serious concern from a fiscal discipline point of view. If this framework were enacted, there is a large risk that the eventual outcome would be a return of large budget deficits, little reduction in the debt burden we would pass on to our children and grandchildren, severe reductions in non-defense discretionary spending, large tax cuts that grow in size over time, and significant new spending on the elderly. Policymakers are promising more than can be delivered within the available budgetary resources, especially once we get a few years past the end of the 10-year budget window in FY 2009 and the baby boom generation begins to retire in large numbers.

Unrealistic Discretionary Budget Cuts:

The budgets the Senate and House Budget Committees have approved would require radical shrinkage over time in some parts of the federal government. Not only would the budget plans maintain the stringent caps the 1997 budget agreement placed on discretionary (i.e., non-entitlement) spending for years through 2002 — which themselves would require sizeable reductions in discretionary spending in the next several years — but the budgets call for large additional reductions in non-defense discretionary programs in the years after that.

- The Senate and House budget resolutions include approximately $200 billion in additional reductions in discretionary programs between 2003 and 2009, on top of the reductions that would result from enforcing the caps through 2002 and holding discretionary spending in fiscal years 2003 through 2009 to the fiscal year 2002 cap level, adjusted for inflation. These additional reductions in discretionary programs provide room for larger tax cuts than could otherwise be accommodated.

- The cuts the House Budget resolution contains in non-defense discretionary programs are so large that by 2009, overall non-defense discretionary spending would be 29 percent below its FY 1999 level, adjusted for inflation.(1) These deep cuts would occur although non-defense discretionary spending already constitutes as small or smaller a share of the Gross Domestic Product than in any year since 1962. Discretionary cuts of this magnitude are unrealistic.

One fact that I find astonishing is if discretionary spending is allowed to grow just enough to preserve the same inflation-adjusted amount of resources available to discretionary programs as is available to these programs this year, not including the emergency spending in fiscal year 1999, discretionary spending would use up $824 billion — or 88 percent — of the non-Social Security surplus. In other words, all of the projected non-Social Security surplus is due to assumed reductions in discretionary programs.

The CBO baseline projections assume that policymakers will keep spending within the discretionary caps.(2) There is, however, little evidence to suggest that appropriations bills can pass Congress and be enacted that actually live within those limits. Look at the 1999 appropriations process. The caps were considerably less tight and yet substantial funding had to be designated as "emergency." In addition, the bill the Senate passed several weeks ago on military pay and pensions increases both discretionary spending and entitlement costs. According to CBO, the legislation increases discretionary spending by $40.8 billion over the next 10 years, with the costs rising each year. The costs reach $6.5 billion a year by 2009 and would continue to rise for a number of years after that. This requires Congress and the President to agree to make even deeper cuts in other discretionary programs (possibly including other defense programs). Including entitlements and revenues, the bill's total cost is $55 billion over 10 years.

The reality is that the discretionary caps will be increased. The only questions are when Congress will adjust the caps and by what amount.

Tax Cuts Should Wait Until Social Security and Medicare Programs Have Been Strengthened

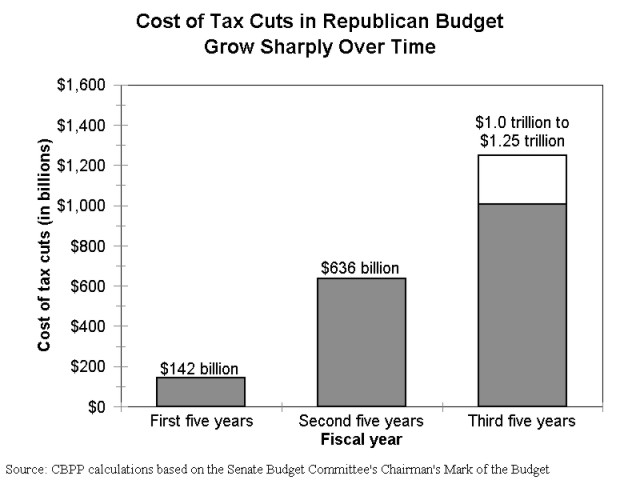

The proposed House and Senate budget resolutions include tax cuts designed to absorb most of the on-budget (non-Social Security) surplus for the next ten years. To follow the path of the anticipated surplus, the tax cuts start relatively small and grow substantially over time. The proposed resolutions include tax cuts costing $142 billion over the first five years, with the cost rising to $636 billion in the second five-year period.

In fact, by 2007 the annual cost of the proposed tax cuts exceeds the amount of the on-budget surplus the Congressional Budget Office estimates will be available.(3) The additional tax reduction is "paid for" by further reductions in non-defense discretionary spending, beyond those that result from adhering in years after 2002 to the cap for FY 2002, adjusted only for inflation.

Looking beyond 2009, the problem becomes still greater. Three factors suggest these tax cuts will become unaffordable after 2009 and would almost certainly bring back deficits in the non-Social Security budget.

- CBO baseline projections indicate that the non-Social Security surplus stops growing and begins to shrink during the five years after 2009.(4) Once the surplus stops mounting and begins to contract, there will be a smaller non-Social Security surplus each year to support a tax cut.

- But the cost of the tax cut is likely to continue growing substantially after 2009. The size of the tax cut in the Senate resolution grows from $32 billion in 2003 to $177 billion in 2009, an annual average increase in cost of more than $24 billion a year. Between 2008 and 2009, the cost grows by $26.5 billion.(5) If this incremental growth were to continue in the years beyond 2009, the cost of the tax cut would rise from $636 billion in 2005-2009 to $1.25 trillion in the five years from 2010 to 2014.

- Even if growth in the tax cut could be held down to the rate of growth in GDP in years following 2009 — which is unlikely because it would require reductions in tax relief at that time— the cost of the tax cut in the five years from 2010 to 2014 would still exceed $1 trillion. (See Figure 1.)

- With the size of the non-Social Security surpluses beginning to decline and the cost of the tax cut continuing to grow, the only way to avoid a re-emergence of on-budget deficits would be to make cuts in programs on top of those that would made by 2009. Such cuts, which could entail eliminating a sizable share of what remained in non-defense discretionary spending, are not likely to be achievable. As a result, the tax cuts in the House and Senate budget resolutions would likely result in a return of deficits in the non-Social Security budget.

The projected surpluses present policymakers with a once-in-a-generation choice. You can spend those surpluses by cutting taxes or raising government spending and thus boosting current consumption. Or you can save those surpluses by paying down the debt held by the public, by strengthening Social Security and Medicare, and raising national saving, investment and long-term economic growth.

Tax Cuts Should Wait Because of the Economic Uncertainty Surrounding These Budget Projections

Furthermore, if Congress and the President pass legislation this year that is projected to result in balance or modest surpluses in the non-Social Security budget but the economy subsequently weakens and grows more slowly than CBO has forecast, the non-Social Security budget will likely slide back into deficit during the next ten years. The resulting deficits could be substantial. CBO estimates that a downturn of the size of the recession of the early 1990s, which was not a severe recession as recessions go, would increase the budget deficit (or reduce surpluses) by approximately $85 billion a year just after the recession hits bottom.

Figure 1

CBO cautions that its surplus forecasts could be off by even larger amounts if revenues grow more slowly than forecast. Analysts do not fully understand why revenues have grown more rapidly than projected in recent years, and they do not know the extent to which the factors that have caused this unexpected revenue growth are temporary or permanent. Revenue growth in future years could be significantly lower or higher than CBO currently projects. If it is significantly lower (and legislation using most of the non-Social Security surpluses currently projected has been enacted), deficits in the non-Social Security budget are likely to return.

A drop in the stock market also would result in lower-than-expected revenue collections, since less capital gains tax would be collected. That, too, could push the non-Social Security budget back into deficit.

CBO this year devoted a full chapter of its annual report on the budget and the economy to the uncertainty of its budget projections. CBO warned that "considerable uncertainty" surrounds its budget estimates "because the U.S. economy and the federal budget are highly complex and are affected by many economic and technical factors that are difficult to predict. Consequently, actual budget outcomes almost certainly will differ from the baseline projections..." (6) CBO reported that if its estimate of the surplus for 2004 proves to be off by the average amount that CBO projections made five years in advance have proven wrong over the past decade, the surplus forecast for 2004 could be too high or too low by $300 billion.

A much more prudent course would be to wait several years before enacting any substantial tax cuts to see if on-budget surpluses of the magnitude now projected actually appear, to determine if our unusually long-lasting economic recovery continues to last (the probability is high that a recession will occur sometime between now and 2009), and to determine the levels of a realistic set of discretionary caps needed to enact the 13 appropriations bills.

Feldstein type Plans Increase Spending on the Elderly, Undermine Social Security as We Know Itand Are Not Adequately Financed

The Social Security plans now emerging in Republican leadership circles appear to envision using the bulk of the Social Security surpluses to fund individual accounts. The Social Security proposal that I understand Chairman Shaw to be developing, as well as the plan Senator Phil Gramm has crafted, would establish individual accounts apparently without reducing Social Security benefits. Such plans require large amounts of additional funding for a number of decades. Under the proposed budget resolutions, these new funds could not come from the non-Social Security surplus, since the vast majority of that surplus would be used for tax cuts. This leaves only one source for funding these accounts — the Social Security surpluses. However, after about 2012, the Social Security surplus is projected to stop growing each year and start to decline, while the cost of funding these individual accounts would continue to increase. As a result, sometime in the five-year period from 2010 to 2014, the cost of individual accounts equal to two percent of Social Security wages would exceed the entirety of the Social Security surpluses. At that time, this plan would require new taxes, even deeper cuts in the rest of government or deficit spending. Individual accounts are essentially a large new entitlement program.

At a time when we have not fully funded the promises we have made to the elderly under the current Social Security program, and when we face large financing gaps in Medicare and unmet needs in other areas, the Feldstein plan would make new promises to the elderly and direct substantial new resources to retirement pensions without increasing government revenues to defray these added costs. The plan poses as a "free lunch" entailing no pain or tough choices. In reality, the plan would be likely to put programs funded through general revenues at a substantial disadvantage and to sacrifice the needs of younger generations to increase benefits directed to the elderly, especially the more affluent elderly.

The plan also would weaken the progressive nature of the current benefit structure, widening the nation's already-large income disparities. In addition, it would establish a hybrid private account/Social Security benefit structure not likely to be politically sustainable over time. The plan would set in motion a dynamic that could lead eventually to the dismantling of much or all of Social Security as we know it today.

Summary of Economic and Budgetary Implications of Congressional Budget Resolutions

The emerging Republican budget and Social Security proposals risk exacerbating the serious fiscal problems the nation faces when the baby-boom generation retires. Since the tax cuts would use up the on-budget surplus while most of the Social Security surplus was used for individual accounts, there would be little debt reduction. As a result, these proposals would squander a historic opportunity to reduce sharply or eliminate the debt held by the public, and future generations would be burdened with obligations to continue making large interest payments on the debt far into the next century. Even if deficit spending is avoided during the next 10 years, the likelihood is high that in the next five-year budget window, our public debt would again increase.

- On-budget surpluses would head back to deficits because currently projected on-budget surpluses stop growing after 2012 while the tax cuts would continue to mount.

- Off-budget surpluses head back to large deficits at approximately the same time because the cost of individual accounts would exceed the Social Security surpluses.

- Aggravating these problems, interest payments would still be around $200 billion a year because there would have been little debt reduction over the previous ten years.

CBO already projects fiscal difficulty when the boomers retire, with deficits returning sometime between 2020 and 2030 and climbing to record levels. Moreover, those projections assume that all the surpluses are used solely for debt reduction. Under the tax cut and individual account proposals just discussed, deficits would return much sooner and climb much higher.

In addition, these budget proposals would require cuts of stunning depth in non-defense discretionary programs. Due to the magnitude of these cuts, some programs that constitute public investments and hold promise of improving productivity — and hence economic growth — could face the knife, as could many programs to aid the most vulnerable members of society. Of course, cuts of such magnitude might not be made given their political difficulty. But then the overall fiscal picture becomes even grimmer, given the costs of the tax cuts and the individual accounts.

The course these proposals chart is a troubling one. It constitutes a high-risk undertaking that is not consistent with building a sounder fiscal structure in preparation for the budgetary storms that lie ahead. It also would be likely to lead over time to some radical changes in the role and functions of the federal government.

Key Criteria by Which Social Security Reform Proposals Should be Judged

In their book Countdown to Reform, Henry Aaron and Robert Reischauer discuss four criteria for assessing Social Security reform. I think these four criteria provide a sound basis for such assessments. I also would add a fifth criterion — restoring and maintaining program solvency in a fiscally disciplined manner.

Boosting National Savings and Economic Growth — the Congressional plans fall short here. The on-budget surpluses would be devoted to tax cuts that will primarily increase current consumption. Devoting a portion of the on-budget surpluses to the Medicare trust fund and using those funds to reduce the publicly held debt, as well as devoting a portion of the surplus to Universal Savings Accounts that are saved rather than consumed, would increase national savings more than using these surpluses for tax cuts. If Congress in its wisdom rejects placing more monies in Medicare or the Universal Savings Accounts, it would be better to place these surpluses in the Social Security trust fund and use them for debt repayment than to use them for tax cuts.

Adequate Benefits that are Equitably Distributed and Represent a Fair Return —Individual account plans generally result in a less progressive distribution of benefits than Social Security does. For example, Aaron and Reischauer's analysis of the Feldstein plan finds it would boost government-funded retirement income several times as much for more-affluent workers than for low and moderately-paid workers.

One frequently hears the argument that diverting resources to individual accounts helps everyone, because such accounts yield much higher rates of return than Social Security. This is not correct. A recent Center paper by Peter Orszag summarizes and puts into layman's terms a recent and important set of papers by economists John Geanakopolos, Olivia Mitchell and Stephen Zeldes. The major finding of the papers by these three economists is that it is advance funding that increases rates of return, not individual accounts. Advance funding will raise rates of return whether it is provided through individual accounts or through Social Security.

The provision of funding that exceeds what is needed to pay current benefits, often termed "partial advance funding" when referring to Social Security, raises the rate of return on contributions because such funding can be invested at the market rate of interest; by definition, none of it is needed to pay current benefits. Since the market rate of return is higher than the rate of return on existing Social Security contributions, and since each dollar of additional funding can earn the market rate of return, additional funding secures a higher rate of return than existing contributions do. This higher rate of return can be captured by channeling the additional funding through either the trust fund or individual accounts.

A corollary of this point is that creating individual accounts out of existing Social Security payroll tax contributions, without any additional advance funding, does not raise the rate of return. If individual accounts are created out of existing funding, the benefits that current workers and retirees have accrued under Social Security must still be paid. That drives the overall rate of return back toward its current level under Social Security. It is the additional funding, not the individual accounts themselves, that is crucial to producing the higher rate of return.

As Geanakopolos, Mitchell, and Zeldes show, the statement that individual accounts yield much higher rates than Social Security is incorrect. Such a statement is based on an invalid rate-of-return comparison. That Geanakopolos, Mitchell, and Zeldes are correct is borne out by the work of the Social Security actuaries in analyzing the three very different plans advanced by Members of the 1994-1996 Advisory Council on Social Security. The three plans adopted very different approaches to individual accounts from no individual accounts (under the Maintain Benefits plan) to relatively large individual accounts (under the Personal Security Accounts plan). But despite the sharply different treatment of individual accounts in the three proposals, their estimated rates of return are very similar. Consider, for example, an average two-earner couple born in 1997. According to projections made by the Social Security actuaries and published in the Advisory Council report, the real rate of return for such a couple would be:

- Between 2.2 and 2.7 percent per year under the Maintain Benefits plan, depending on the share of the Social Security Trust Fund invested in equities;

- 2.2 percent per year under the Individual Accounts plan; and

- 2.6 percent per year under the Personal Security Accounts plan.

In summary, the simple argument that individual accounts necessarily provide higher rates of return than Social Security is not valid. This argument rests on computations that either mistakenly count the cost of Social Security benefits that must be paid to current retirees as costs only under Social Security and not under a system of individual accounts or inappropriately compare the return on additional funding for individual accounts to the return on existing contributions to Social Security (or commit both errors).

Analytically sound comparisons also should reflect risk and administrative costs. Individuals generally dislike risk; a much riskier asset with a slightly higher rate of return is not necessarily preferable to a much safer asset with a slightly lower rate of return. Administrative costs are also important; all else being equal, higher administrative costs reduce the net rate of return an individual receives. When these factors are taken into account, the supposed advantage of individual accounts in providing higher rates of return diminishes further and may even be reversed, given the higher administrative costs associated with individual accounts than with Social Security.

Protection Against Risk

On one level, the Feldstein plan does provide ample protection against risk because it guarantees all participants a benefit as large as the Social Security benefits promised under current law. However, the plan is likely to undermine political support for the Social Security program as we know it today. Because people would seem to be paying substantial payroll taxes to Social Security and getting little back from it, Social Security would likely appear to much of the middle class and more affluent segments of the population to be a bad deal. It would seem to provide them a very poor rate of return compared to what there private accounts were paying. These disparate rates of return would partly reflect the fact that the Social Security trusts funds would bear all of the burden of financing the benefits of workers who had already retired or worked for many years before the individual accounts were established. The trust funds also would bear all of the burden of providing more adequate benefits to low-income retirees, low-earning spouses and divorced women, and covering widows, the disabled and the children of disabled and deceased workers. Although not obvious to many workers, a sizeable portion of the Social Security payroll tax is essentially an insurance premium for the disability and life insurance protection that Social Security provides. The private accounts, by contrast, would bear none of these burdens, which would enable them to appear a better deal to the average worker.

Also a clawback or a tax or an integration factor (whatever it is called) of 75 percent to 90 percent is politically unsustainable. It is unlikely that you can give the American people accounts which they manage and which public officials say are theirs and then take almost all of the accounts back when they retire. Lowering the "clawback" percentage, however would require deeper cuts in Social Security benefits, increased transfers from the rest of government to Social Security, or deficit-financing. Finally, as discussed earlier, a Feldstein-type plan poses substantial risks for the rest of government and for fiscal integrity.

Administrative Efficiency

The Feldstein plan would be complex and costly to administer. How costly would depend upon details of the plan. A recent study of the administrative costs of privately managed individual accounts in the United Kingdom shows that more than 40 percent of the their value is consumed by administrative fees and annuitization and other costs, a figure that is significantly higher than has been acknowledged thus far in the debate in the United States. What this experience in the U.K. vividly illustrates is that if individual accounts are created in the United States, a decentralized, privately managed approach (as distinguished a Thrift Saving Plan-type approach) could carry a variety of dangers.

Restoring and Maintaining Program Solvency in a Fiscally Disciplined Manner

A key question in assessing reform is whether 75-year solvency has been restored and whether it is maintained. The President's plan receives high marks for its emphasis on reducing the public debt.

Lowering interest burdens is one of the best things we can do for younger generations. It increases our ability to meet our Social Security promises. The interest savings alone from this proposal (as a percentage of GDP) would more than offset the increase in Social Security costs that will occur under current law over the first half of the next century. The Administration's plan also envisions that the half of the shortfall not closed by general-fund transfers be closed, in whole or in large part, through more traditional methods. The President has called for the specific changes to be identified and agreed upon through bipartisan negotiations. To reinforce this strategy, the Administration wants to "Save Social Security First"; it proposes that the increased discretionary spending and the USA accounts contained in its budget proposal not be created until Social Security solvency is restored.

In my opinion, both plans — the Administration's (insofar as specifics have been provided) and the Feldstein type approach — fall short on the fiscal discipline test. Under the Administration's approach, the massive infusion of general funds, if not tied to structural reforms in Social Security, might encourage policy-makers to avoid the needed structural reforms in Social Security (i.e. reductions in benefits and increases in revenues). Indeed, the crediting the Administration has proposed coupled with a higher level of trust fund investments in equities than the Administration has proposed could make the Social Security program solvent over 75 years without any structural changes. In my view, the transfers the Administration proposes need to be conditioned upon making the structural changes to close the full 75-year financing gap.

However, the Feldstein type plans fails the fiscal discipline test to a much greater extent. Promises to the elderly would be increased and there would be massive infusions of general revenues. There are no structural reforms and revenues are not explicitly increased. As I have argued earlier, this will cause severe fiscal pressures down the road. In addition, as a result of the combination of a Feldstein-type plan and the proposed tax cut the publicly held debt would not be reduced very much and therefore the interest burden on our younger generations would remain high. Finally, while it is assumed that a portion will be invested in equities, the manner in which this is done (compared to investment of the trust fund in equities) is likely to be costly and inefficient, especially if the individual accounts are privately managed.

A Brief Description of a Fiscally Disciplined Alternative Framework

Let me briefly describe an alternative framework:

- Recognize reality and adjust the discretionary caps for fiscal year 2000 upward so that the 13 appropriation bills can be enacted.

- Transfer to Social Security or Medicare some portion of any remaining on-budget surpluses, which would result in further reductions in the publicly held debt.

- Delay enactment of any substantial tax cuts or substantial new spending for the out-years until the Medicare and Social Security programs have been strengthened and there is a better sense of how much of the on-budget surplus safely can be used for tax reductions.

- In addition to any transfers from the on-budget surplus, further transfer to the Social Security trust fund are appropriate to the extent that Congress is unwilling to grant the authority to invest up to 50 percent of the Social Security reserves in equities (a smaller percentage than state and local pension funds invest in equities) under the management of an independent board. To the extent that such authority is not granted, general revenue transfers to compensate the trust fund for this lost income are appropriate. This policy (or better yet the actual investment of 50 percent of the trust fund in equities) would close slightly more than 50 percent of the 75-year financing gap. (This proposal is described in more detail in testimony I provided earlier this year to the Senate Special Committee on Aging.)

- Close the remainder of the solvency gap by other structural changes in the Social Security program.

- Reduce the publicly held debt to zero by walling off the Social Security surpluses in a manner that precludes their being used for new tax reductions or spending increases. These surpluses should be used solely for Social Security solvency and debt repayment . A properly designed lock-box (that automatically adjusts for changing budget estimates due to economic and technical changes in estimates) employing a revised pay-as-you-go rule would be the most appropriate mechanism for accomplishing this. This pay-as-you-go rule should be enforced with a both a sequester and a 60-vote point of order. The bill announced yesterday by this Chairman is a significant improvement to the lock-box mechanisms being discussed on the Senate side. We would, however, suggest allowing a majority rather than a super-majority vote to waive the points of order that the bill establishes during recessions and wars.

In conclusion, Mr. Chairman, you consistently argued during the welfare debate that the states were doing the right thing and the federal government should take its cue from what the states were doing. I believe, Mr. Chairman, that in this Social Security debate, the federal government should adopt two policies from the states. One is that 50 to 60 percent of state pension funds are invested collectively in equities. Second, if states have learned how to set aside their pension funds and not spend or give them away in tax cuts, the federal government should be able to do that as well.

End Notes:

1. The FY 1999 level used here as a point of reference excludes emergency spending. If emergency spending were included, the dimensions of the discretionary cuts in the budget resolution would seem deeper.

2. More precisely, the CBO projections assume that discretionary spending will fit within the caps for as long as they are in place. After 2002, when the caps are no longer in place, the projections assume that discretionary spending will grow with inflation.

3. These figures are based on CBO's "capped baseline," which assumes that discretionary spending will increase with inflation after the current caps expire in 2002. This is the standard baseline that CBO and OMB use to estimate the extent to which the budget will be in deficit or surplus.

4. The CBO baseline goes through 2009.The CBO capped baseline was extended to 2014 for purposes of this analysis by applying the growth rates in the CBO long-term forecast. The projections show that annual surpluses in the non-Social Security budget begin to decline after 2012. Policy changes could shift by one or a few years the specific year in which these surpluses begin to shrink, but such shrinkage is virtually certain to occur some time shortly after the baby boom generation begins to retire.

5. In the Senate budget resolution, the size of the tax cut grows by an average of $24.2 billion a year between 2003 and 2009, while in House version the average annual growth is $24.6 billion. In the House version, the cost grows from $30.7 billion in 2003 to $178 billion in 2009, and growth between 2008 and 2009 is $24.8 billion.

6. Congressional Budget Office, The Economic and Budget Outlook: Fiscal years 2000-2009, January 1999, p. 81.