BEYOND THE NUMBERS

Why the Tax Preferences for Capital Gains Aren’t Sound Policy

Ahead of tomorrow’s joint House-Senate hearing on capital gains taxes, we’ve issued a major report on why policymakers should shrink the large tax advantages that capital gains enjoy. Here’s the opening:

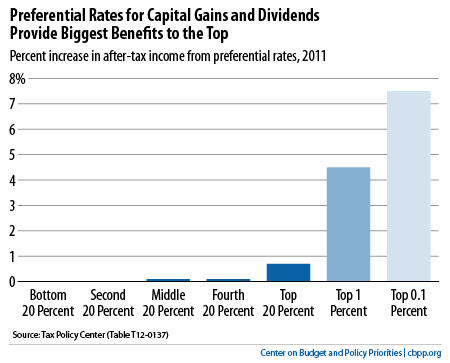

The large tax preferences that capital gains enjoy over “ordinary” income, such as salary and wages, add to budget deficits, widen income inequality, and do little if anything to promote economic growth. Recent bipartisan deficit commissions have called for eliminating or sharply reducing these tax preferences, as the landmark 1986 Tax Reform Act did. By doing so as part of a package that reduces deficits and reforms the tax code, policymakers could help put the nation’s fiscal house in order and make the tax code fairer and more efficient.

The tax code now strongly favors capital gains — increases in the value of assets, such as stocks and real estate — over ordinary income. Not only is the capital gains tax rate far below the top tax rate on ordinary income, but taxpayers can delay paying taxes until they realize their capital gains (usually when they sell assets). In many cases, taxpayers can avoid paying capital gains tax altogether; about half of all capital gains are never subject to capital gains tax, according to the Congressional Research Service (CRS).

Click here for the full report.

Related Posts: