BEYOND THE NUMBERS

What to Look for in Monday’s Social Security Trustees’ Report

The trustees of the Social Security system — the Secretaries of the Treasury, Health and Human Services, and Labor, the Commissioner of Social Security, and two public trustees — will release their annual review of the program’s finances on Monday. Here are a few things to keep in mind in the meantime.

Although we have no inkling of what the report will say, we know that annual fluctuations in the trustees’ long-term estimates are normal. Social Security is subject to a variety of economic and demographic uncertainties, and the actuaries are constantly improving their methods.

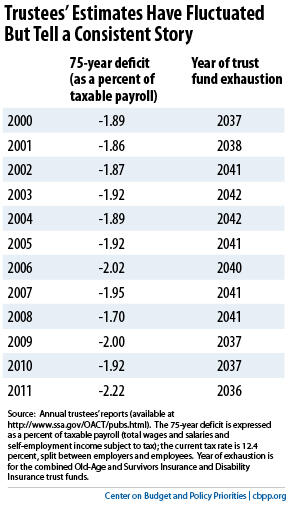

The estimated gap between Social Security’s tax revenues and its expenditures over the next 75 years has fluctuated within a narrow band of 1.70 to 2.22 percent of taxable payroll in the last decade’s reports (see table). (Taxable payroll is the total wages and self-employment income subject to Social Security taxes.)

The estimated year in which Social Security’s combined trust funds — the Old-Age and Survivors Insurance (OASI) trust fund and the Disability Insurance (DI) trust fund — will be exhausted has ranged in those reports between 2036 and 2042. It’s important to remember that, even after the combined trust funds are exhausted, Social Security could still pay about three-fourths of scheduled benefits using its payroll tax income.

The new report will note that the DI trust fund, which is legally separate from the much larger OASI trust fund, faces exhaustion sooner. (Last year, the trustees forecast that would happen in 2018; more recently, the Congressional Budget Office projected DI trust fund depletion in 2016.) But traditionally, Congress has reallocated payroll tax revenue between the OASI and DI funds as necessary to address such challenges. That’s why analysts usually focus on the outlook for the combined trust funds.

Policymakers shouldn’t address DI in isolation. Instead, they should aim at a balanced package of Social Security reforms that achieves overall long-term solvency while preserving and even strengthening the program’s vital role in protecting breadwinners and their families.

Check out our analysis of last year’s report and our other Social Security analyses here. Look for an update as soon as we have a chance to digest the new report.