BEYOND THE NUMBERS

President’s Budget Plan Would, Indeed, Stabilize the Debt

We’ve noted that the budget plan President Obama released on Monday would produce a substantial accomplishment: stabilizing the federal debt as a share of the economy in the second half of this decade. We were surprised, therefore, to see Maya MacGuineas of the Committee for a Responsible Federal Budget quoted in the Washington Post (a quote that Thomas L. Friedman cited in his New York Times column) as stating that “They don’t even stabilize the debt.”

Her claim seems to hinge on the fact that under one set of assumptions, there is a tiny uptick in the debt-to-GDP ratio between 2019 to 2021. Yet those same assumptions show that the ratio would be the same in 2021 as in 2017 — and much lower in both years than in 2013. It is hard to see how a fair observer could conclude that the debt would not be stabilized.

Every major budget commission of recent years has concluded that arresting the rise in the debt as a share of the economy, and then keeping it stable, is the core fiscal policy goal for the decade ahead. The Office of Management and Budget (OMB) estimates that under the President’s plan, debt would hit 76.9 percent of GDP in 2013 but then decline to 73 percent of GDP in 2021. In the second half of the decade — 2017 through 2021 — the debt-to-GDP ratio would be stable, declining slightly from 74.8 percent of GDP to 74.2 percent, 73.8 percent, 73.4 percent, and 73.0 percent.

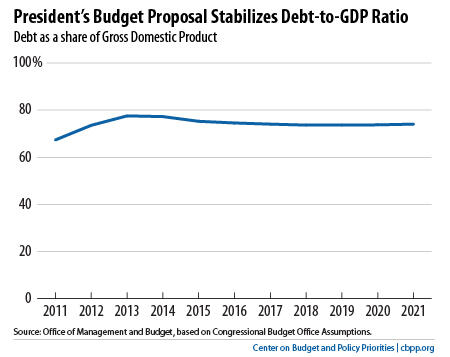

OMB also provided estimates of the debt-to-GDP ratio under its plan using Congressional Budget Office assumptions, and the results are similar. Under CBO assumptions, the debt-to-GDP ratio would hit 77.5 percent of GDP in 2013 and then decline to 74 percent in 2021. From 2017 through 2021 the ratio would essentially be flat: 74.0 percent, 73.6 percent, 73.6 percent, 73.7 percent, and 74.0 percent (see chart).

To be sure, without further policy changes — particularly changes that will slow the growth in health care costs throughout the U.S. health care system — the debt-to-GDP ratio would start to grow again in years and decades after 2021, and further action would be needed. But stabilizing the debt-to-GDP ratio through the end of this decade would be a very large accomplishment. And under either the OMB or CBO assumptions, it seems clear that the President’s plan would meet that goal, effectively stabilizing the debt-to-GDP ratio in 2017 through 2021.

To understand Ms. MacGuineas’ claim that the plan would not stabilize the debt, we looked at the analysis of the plan issued by the Committee for a Responsible Federal Budget, which she heads. It ignores the estimates under OMB assumptions and says, “Measured against CBO assumptions, the President’s submission would nearly, but not quite, stabilize the debt as a share of the economy.” It bases this claim on the fact that these estimates show the debt ticking up estimates show debt rising from 73.6 percent of GDP in 2019 to 74.0 percent in 2021.

For starters, one wouldn’t know from MacGuineas’ highly critical quote that her own organization has concluded that the President’s plan “would nearly, but not quite, stabilize the debt.”

More important, it is a stretch to suggest that the very slight increase in the debt-to-GDP ratio from 2019 to 2021 under CBO’s assumptions signifies in any meaningful sense that the President’s plan wouldn’t stabilize the debt through 2021. Anyone who has ever done multi-year budget projections knows that changes of a few tenths of a percentage point in the debt-to-GDP ratio projected from 2017 through 2021 are not meaningful — the range of uncertainty in budget projections five to ten years out vastly exceeds these small variations.

In any case, no economist would say that a slight reduction in the debt-to-GDP ratio one year followed by a slight increase of the same magnitude over the next couple of years represents an unsustainable budget.

Getting the debt-to-GDP ratio down to 74 percent in 2017 and having it fluctuate slightly between 73.6 percent and 74.0 percent over the second half of the decade (as would occur under the CBO assumptions) clearly qualifies as stabilizing the debt. And under the OMB assumptions, the debt continues to edge down as a share of GDP over this period.

There are aspects of the President’s plan that budget analysts can reasonably criticize. But it isn’t reasonable to use tiny variations in the debt projections for the 2019-2021 period to attack the plan for not stabilizing the debt, especially when the five-year path from 2017- 2021 is essentially flat.

Doing so may make a great soundbite, but it doesn’t constitute sound fiscal analysis.