BEYOND THE NUMBERS

OECD: Tax and Spending Policy Can Push Against Rising Inequality

A number of reports on the recent income inequality study by the Organisation for Economic Co-operation and Development (OECD) have highlighted the finding that the United States ranks fourth in inequality among OECD countries. This ranking uses the “Gini” index of the distribution of “market income” — that is, income before counting the effect of taxes and government transfer programs such as Social Security.

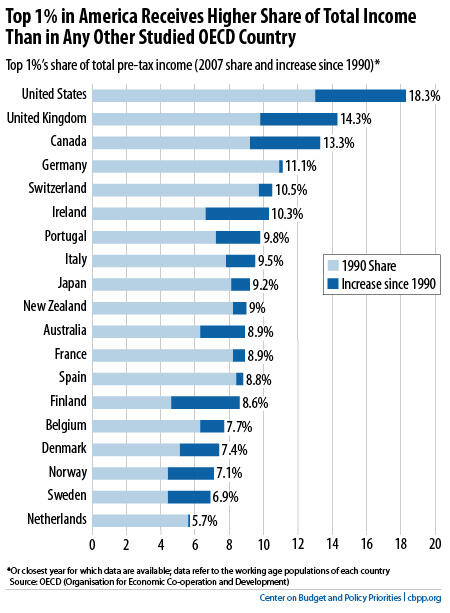

Equally important is the OECD’s finding that in 2007, the share of total market income going to the top 1 percent of households was higher in the United States than in the other 18 OECD countries for which such data are available (see chart). (In the United States, the top 1 percent had incomes above $360,000 in 2007; their average income was $989,000.) Also, the percentage-point increase in the top 1 percent’s share of total market income between 1990 and 2007 was larger in the United States (5.3 percentage points) than in any other country examined.

Moreover, even within the top 1 percent of earners, the very top have enjoyed particularly large income gains: the OECD notes that “the scale of the rise in the share of the top 0.1% in the United States stands out as being substantially larger than the rise in the corresponding share in other countries.” The top 0.1 percent received 8.2 percent of total income in 2007, up 3.3 percentage points from 1990. (In 2007, the top 0.1 percent of U.S. income earners earned more than $1.5 million and had average incomes of $3.9 million.)

Nor, for the United States and most of the other countries the OECD examined, do these data include income from capital gains and dividends. If you include these income sources, the top 1 percent of U.S. income earners received 23.5 percent of the nation’s income in 2007, up 9.2 percentage points from 1990, and the top 0.1 percent received 12.3 percent, up 6.5 percentage points from 1990.

These findings are particularly important because the OECD suggests that, given the sustained rise in income concentration at the very top, countries should consider increasing the average amount of taxes high-income earners pay, too. In the United States, average tax rates of high-income earners have been trending downwards.

The OECD sets out some options for raising average tax rates of high-income taxpayers, including options that we’ve previously discussed, such as reducing the preferential treatment of capital gains income, taxing “carried interest” as ordinary income, and reducing the value of tax expenditures for high-income taxpayers.

These and other options are well worth considering in light of growing income inequality (which, as the OECD report states, creates social, political, and economic challenges), as well as the need for revenues to help reduce deficits.