BEYOND THE NUMBERS

Countdown Day 5: Top Ten Facts About Social Security

Today’s the final day of our countdown of the top ten facts about Social Security in honor of its 75th anniversary this weekend. We released a report today summarizing all ten. Here are our posts on the other eight: Day 1, Day 2, Day 3, and Day 4.

The last two:

Social Security benefits are modest. Social Security benefits are much more modest than many people realize. In June 2010, the average Social Security retirement benefit was $1,170 a month, or about $14,000 a year. (The average disabled worker and aged widow received slightly less.) When the program’s full retirement age was 65, Social Security checks (after deducting the premium for Medicare’s Supplementary Medical Insurance) replaced about 39 percent of an average worker’s pre-retirement wages — significantly less than similar programs in most other Western countries. And that percentage will gradually fall because of the projected rise in Medicare premiums (as health care costs continue to outpace general inflation) and the further increase in Social Security’s full retirement age — which is now 66 and will climb to 67 over the 2017-2022 period.

Social Security can pay full benefits through 2037 without any changes, and relatively modest changes would place it on a sound financial footing for 75 years and beyond. Social Security’s costs will grow in coming years as members of the large Baby Boom generation (born between 1946 and 1964) move into their retirement years. Since the mid-1980s, however, Social Security has collected more in taxes each year than it pays out in benefits and has amassed a trust fund of $2.6 trillion. The trust fund will enable Social Security to keep paying full benefits through 2037 without any changes in the program, according to Social Security’s trustees (see our report on this), even though it will start paying out more in benefits than it receives in annual tax revenue before then.

After 2037, the trust fund will be exhausted if no changes are made. After that, Social Security will be able to pay three-fourths of its scheduled benefits using its annual tax revenue. Alarmists who claim that Social Security won’t be around when today’s young workers retire either misunderstand or misrepresent the projections. A mix of tax increases and modest benefit reductions — carefully crafted to shield the neediest recipients and give ample notice to all participants — could put the program on a sound financial footing indefinitely.

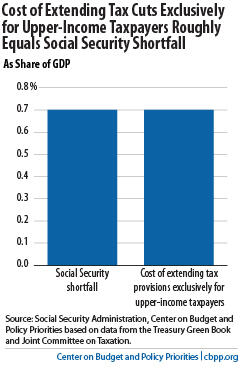

The long-term gap between Social Security’s projected income and promised benefits is estimated at 0.7 percent of gross domestic product (GDP) over the next 75 years (and 1.4 percent of GDP in 2084). By coincidence, that roughly matches the revenue loss over the next 75 years from extending the Bush tax cuts for people making over $250,000. Members of Congress cannot simultaneously claim that the tax cuts for the richest 2 percent of Americans are affordable while the Social Security shortfall constitutes a dire fiscal threat.