BEYOND THE NUMBERS

Cost of Proposed Corporate Tax Holiday Soars

As I explained recently, corporations have launched a massive lobbying campaign for another temporary tax holiday for overseas profits they bring back to this country. Part of their pitch has been that it would effectively be a “free lunch” for taxpayers. Today, the cost of that supposedly “free” lunch went way, way up.

Before Congress enacted the first such holiday in 2004, the Joint Committee on Taxation (JCT) estimated it would cost $3 billion over ten years. When some lawmakers proposed a second holiday in 2009, the cost estimate shot up to $29 billion as JCT saw how much more profits corporations were shifting overseas.

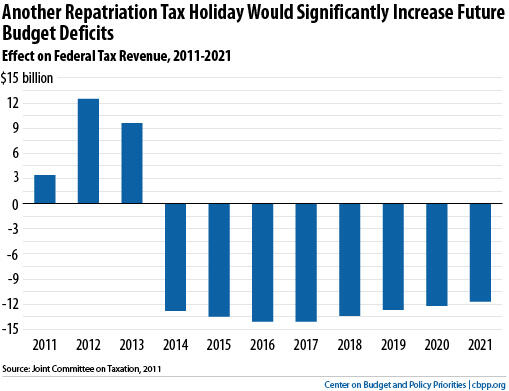

JCT today estimated the cost of a new holiday at $79 billion over ten years. Revenues would go up slightly in the first few years as corporations took advantage of the holiday to “repatriate” foreign earnings at a much lower tax rate, but large revenue losses in later years would more than wipe out those gains as corporations aggressively shift more jobs and income overseas in anticipation of another temporary holiday (see graph).

The Joint Tax analysis also bolsters the central arguments against another holiday:

- The tax holiday enacted in 2004 failed to produce the promised economic benefits. The evidence shows that firms mostly used the repatriated earnings not to invest in U.S. jobs or growth but for purposes that Congress sought to prohibit, such as repurchasing their own stock and paying bigger dividends to their shareholders. JCT studied the research carefully and concluded: “the research has shown little macroeconomic benefit from the original enactment.”

- A second holiday would be even worse than the first because it would entice even more overseas investments: If Congress enacts a second tax holiday, rational corporate executives will conclude that more tax holidays are likely in the future. That will make corporations more inclined to shift income into tax havens and less likely to make investments in the United States. As JCT has stated, a tax holiday “encourages investments and/or earnings to be located overseas.” That’s why Congress, in enacting the 2004 tax holiday, explicitly warned that it should be a one-time-only event and should not be repeated.