Senate Housing Legislation Highly Disappointing: Less Than One-Fourth of Cost of Senate Bill Goes for Provisions That Will Actually Help Address the Foreclosure Crisis

On April 10, the Senate passed legislation that its supporters say will help struggling families hold on to their homes and assist the communities hit hardest by the foreclosure crisis. Measures that would help achieve these goals, however, account for less than one-fourth of the bill’s cost. The remainder of the cost comes from an array of tax-cut provisions that either are unrelated to housing or are related but would do little or nothing to aid either homeowners at risk of foreclosure or hard-hit communities. Moreover, one of the bill’s provisions would actually worsen the problems that local governments face, and several other provisions could have adverse consequences, as well.

In addition, to avert a Republican filibuster, Senate negotiators omitted from the bill the one provision likely to be the most beneficial in averting foreclosures — a measure to provide a mechanism for large numbers of homeowners at risk of foreclosure to work out new mortgage arrangements with lenders. This measure was not passed over due to cost; its cost is lower than the amount the bill would spend on tax cuts that would do little or nothing to address the foreclosure crisis.[1]

The Senate also rejected an amendment to modify bankruptcy law so that judges would have the option of writing down the principal an individual owes on a mortgage on a primary home, as part of a bankruptcy proceeding. This provision, as well, could have a significant effect in preventing foreclosures and would do so without a cost to taxpayers.

In other words, the Senate bill is replete with costly, ineffective provisions, while measures that would be less costly and more efficacious were left out.

Tax Cuts in Package Would Largely Fail to Achieve Bill’s Avowed Goals

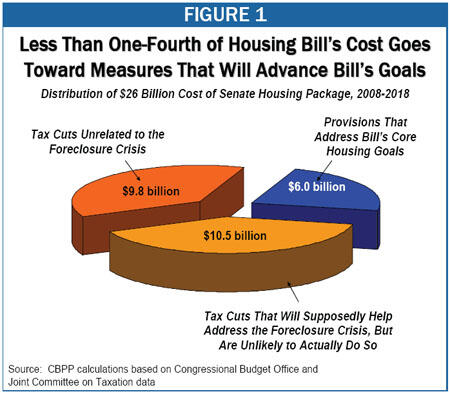

In introducing the tax components of the bill on the Senate floor, Finance Committee Chair Max Baucus declared, “simply put, we are here today to help families to keep their homes.”[2] Yet of the bill’s $22 billion in tax cuts (which constitute about 85 percent of the total cost of the bill), only $1.8 billion is devoted to provisions that would help to alleviate the foreclosure crisis. (These provisions are discussed in the box on page 6.) The remainder of the tax package is divided between provisions that are entirely unrelated to foreclosures and problems in the housing market ($9.8 billion, or 37 percent of the cost of the bill’s tax provisions are in this category[3]) and provisions that seemingly aim to address these problems but would, in fact, do little or nothing to help ($10.5 billion, or 40 percent of the bill’s tax package is in this category).[4]

Tax Provisions that Aim to Address the Problem But Would Do Little or Nothing to Help

In this section of the analysis, we focus on the tax provisions the Finance Committee has presented as addressing the housing-market crisis.

Net Operating Loss Carry-Back Provision

The Senate bill’s single largest provision deals with business net operating losses. A business experiences a “net operating loss” when its tax deductions exceed its income. Under current law, businesses may use their net operating losses to reduce their previous two years’ taxable income, in which case they receive refunds of taxes they paid in those years. Businesses also may use these losses to reduce their taxable income in any of the next 20 years.[5]

The Senate legislation would extend the “carryback” period from two years to four years for net operating losses incurred in 2008 or 2009, at a cost of $6.1 billion over the next decade (2008-2018). The tax benefits that businesses would receive upfront would be much larger than this — about $25 billion worth — but much of this forgone revenue would be recouped in subsequent years (since some of the losses that would be claimed as carrybacks in 2009 and 2010 would otherwise have been deducted as carryforwards in later years ).[6]

| Table 1: | |||

| Provision | Description | Cost (2008-2018) | Main Problems |

|---|---|---|---|

| Extension of net operating loss carryback period* | Allows businesses to use 2008 and 2009 business losses to obtain refunds of tax payments made for the four prior years (instead of refunds of tax payments for only the two prior years, as under current law) | $6.1 billion | Supposed to help the housing sector by boosting the homebuilding industry, but unlikely to change builders’ decisions about whether to invest, retain workers, or sell houses at “firesale” prices. Could even encourage “firesales,” by making it easier for sellers to take immediate tax write-offs for the resulting losses. Much of the tax benefit would go to firms that have no relation to housing. The tax break is unlikely to help the economy; in its recent report on economic stimulus options, CBO gave this proposal the lowest of its three ratings for cost-effectiveness as economic stimulus. |

| Credit for purchases of foreclosed homes | Provides a $7,000 nonrefundable tax credit, spread over two years, to taxpayers who purchase foreclosed homes (with no income limit on who may qualify for the credit.) | $1.6 billion | Unlikely to boost overall housing demand enough to benefit current homeowners by raising home values. Instead, most of the benefits would likely go to people who would purchase homes anyway, without the tax incentive. To the extent that the credit did boost demand for foreclosed homes, the beneficiaries would mostly be banks and other lenders who own foreclosed properties. Could have unintended adverse consequences, such as boosting prices for foreclosed homes at the expense of other homes or making banks and other lenders quicker to foreclose by increasing the demand for foreclosed homes. Not well-targeted to help communities hard hit by foreclosures. |

| Property tax deduction for non-itemizers | Creates a temporary $1,000 per-couple, $500 per-individual, tax deduction for property tax payments by filers who do not itemize their deductions | $1.5 billion | Benefits all homeowners who do not itemize and who have incomes high enough to benefit from a deduction, instead of targeting those most likely to need help. Because the assistance would be spread so thinly, the tax benefits would be too small — $150 for a couple in the 15 percent tax bracket — to have a meaningful effect in helping families avert foreclosures. Denies the deduction to taxpayers who live in jurisdictions that increase property tax rates. This would effectively prevent localities from raising property tax rates to help compensate for shrinking property tax revenues, which in turn could worsen localities’ fiscal problems and lead to sharp cuts in schools, police, and other services. The provision also would be virtually impossible for the IRS to administer. |

| * A smaller provision of the Senate legislation, added as an amendment during floor debate on the bill, would allow certain businesses to obtain refundsof Alternative Minimum Tax and research and development tax credits. The effects of this provision on the economy would likely be similar to the effects of the net operating loss provision. | |||

Supporters of the net operating loss provision claim it would help to address the housing crisis by boosting the homebuilding industry. According to a Finance Committee press release, “homebuilders and other housing sector businesses particularly need cash to prevent layoffs, to avoid selling land and houses at distressed prices, and simply to shore up their lagging bottom lines.” The press release also implies that the net operating loss provision would encourage homebuilders to make new investments.[7] These claims, however, do not withstand scrutiny.

Providing Businesses With More Cash Generally Will Not Change Their Business Decisions

Generally speaking, homebuilders (and other businesses) will retain workers if they believe that the value of what the workers can produce exceeds their wages. They will invest in new construction if they anticipate adequate demand for new houses. And they will avoid selling houses at “firesale” prices if they expect to be able to sell them at higher values in the not-too-distant future.

None of these calculations is influenced significantly by a tax break like the NOL provision, which provides businesses with more cash whether or not they avoid layoffs and firesales or increase investment. Simply put, a no-strings-attached cash infusion will not prevent businesses from making profit-maximizing choices about hiring, investment, and sales.

To be sure, the NOL provision could potentially affect the decisions of one group of businesses: companies that would like to retain workers, undertake new construction, or keep their newly-built homes off the market but are constrained by low cash flow and borrowing constraints. Given the current stare of the economy and the housing market, however, it is unlikely there are many homebuilders who believe it would be profitable to scale up production now and who would do so if only they had more cash on hand.

It is conceivable that a cash infusion could increase the willingness of some homebuilders to hold on to newly-built homes, since some businesses may be selling those assets to avoid bankruptcy. But the NOL provision also could make firesales more attractive — since it would make it easier for businesses to take immediate tax write-offs for the resulting losses.[8]

Furthermore, even if the NOL provision could somehow accomplish the goals the Finance Committee press release sets for the legislation, it is not clear that all of these goals are desirable. Additional housing construction now would only add to the glut in the housing market, further depressing home values and likely prolonging the crisis as a consequence. In addition, “shor[ing] up lagging bottom lines” for businesses that are not doing well in the market place is not generally considered a federal responsibility.

Most of the Benefits From the NOL Provision Would Accrue to Businesses Outside the Housing Sector, and the Measure Would Provide Little Boost to the Overall Economy

Many businesses experience net operating losses even during an economic expansion, with some of them exhausting the standard two-year NOL carryback period. During an economic downturn, the number of businesses that suffer losses in excess of what they can apply against their prior two years’ taxable income rises.

IRS data show that, during the last economic downturn, firms in the manufacturing, information, and finance and insurance sectors made the biggest use of net operating loss deductions.[9] Together, these three sectors claimed more than half of all NOL deductions in 2002. These data indicate that the claim that the NOL provision is a subsidy targeted to the homebuilding industry is incorrect.

That might not be a problem if the NOL provision were likely to boost the overall economy by providing effective economic stimulus. But in its January 2008 report on stimulus options, the Congressional Budget Office gave the NOL proposal its lowest cost effectiveness rating for stimulus (out of three possible ratings). CBO noted that NOL provision would likely do little to stimulate near-term investment.[10]

This is because the points noted above with respect to the homebuilding industry — that the NOL provision would likely have little effect on hiring and investment decisions — also apply to businesses generally. As a Goldman Sachs analysis explained, “companies don’t spend money just because it’s there to spend. To justify outlays for new projects, the expected returns have to exceed the cost, and that usually requires growth in demand strong enough to put pressure on existing resources.”[11]

In other words, in the absence of adequate consumer demand, provisions like the Senate NOL provision simply benefit companies’ bottom lines without doing much to boost investment, jobs, or the overall economy. To increase business production and investment during an economic downturn, policymakers generally must take measures to boost consumer demand rather than simply to increase business cash flow.

Tax Credit for Purchases of Foreclosed Homes

Under the Senate bill, people purchasing foreclosed homes who intend to occupy those homes as their primary residences could claim a tax credit worth $7,000, spread over two years. The theory appears to be that the tax credit would increase the demand for foreclosed homes, which would help struggling homeowners by raising the prices of their properties and thereby facilitating refinancing. Supporters also argue that this tax credit would help neighborhoods suffering from an epidemic of foreclosures, by making it more likely that foreclosed homes would be sold to new owner-occupants.[12]

Provisions in the Senate Bill that Respond to the Foreclosure Crisis

The bill does include some provisions to address mounting foreclosures and their consequences.

Helping current homeowners avoid foreclosures. The bill contains the following provisions that should be helpful in this regard:

- Lower-cost loans to refinance current mortgages. The bill would give states and localities a one-time increase of $10 billion in tax-exempt housing bond authority and would allow these bonds to be used to assist with refinancings of adjustable-rate, subprime mortgages that were issued between 2002 and 2007. (Currently, this bond authority can be used only to help finance new mortgages for first-time homebuyers with low and moderate incomes and for multi-family rental housing.) Proponents have estimated that the $10 billion increase in bond authority, which would come at a cost of $1.8 billion to the Treasury, could fund mortgages for 80,000 households. These mortgages would have lower interest rates than conventional loans, making them more affordable for lower-income borrowers.

- Housing counseling. The bill would provide an addition $180 million for housing counseling to aid homeowners at risk of foreclosure.

- Help for active-duty service-members. The bill would strengthen protections against foreclosure on the homes of active-duty service-members.

Assistance for hard-hit communities. The bill would provide $3.9 billion in supplemental Community Development Block Grant (CDBG) funds that states, localities, or other entities could use to purchase and redevelop foreclosed or abandoned properties for resale or rental.* At least 25 percent of these funds would have to be used for properties that would house families with incomes at or below 50 percent of the area median income. (Nationally, 50 percent of median income equals $30,750 for a family of four in 2008.) The remaining funds would have to be used for housing for families with incomes at or below 120 percent of area median income (nationally, $73,800 for a family of four).

These funds would be distributed on the basis of actual foreclosures and the prevalence of subprime loans and mortgage defaults and delinquencies. Lenders would benefit from the purchase of foreclosed properties they owned, but not excessively so, as the properties would be purchased at a discount from their current value.

Improvements in future mortgage lending. The bill includes a number of provisions to reform FHA lending. Most notably, it would permanently increase the mortgage amount that the FHA can provide or insure from 95 percent of the median home price in an area to 110 percent of the median price (with certain limitations). These changes would provide a foundation for the expanded role that Senator Chris Dodd and Representative Barney Frank are seeking to have the FHA play in refinancing troubled mortgages (see pages 10-11). The Senate bill also makes changes to the Truth in Lending Act to help borrowers better understand loan terms and better choose loans that they can afford.

* In areas without sufficient demand for housing, state or localities could demolish blighted structures and hold the land for future redevelopment.

Unfortunately, this strategy, as well, is unlikely to provide meaningful help to current homeowners. The Congressional Budget Office estimates that 2.8 million foreclosure proceedings will be initiated in the next four years, with about 1.1 million of these homeowners ultimately losing their homes through foreclosure.[13] To address the glut in the housing market, the tax credit would have to generate an increase in demand for foreclosed homes that is both swift and massive — on a scale far beyond what is plausible.[14]

Moreover, the tax credit could do harm. While a $7,000 credit is unlikely to be large enough to induce many people not otherwise planning to purchase a home to enter the market, it could sway some households’ decisions about which home to buy. If the credit induced homebuyers to purchase foreclosed homes instead of other homes, it would pump up demand and prices for foreclosed homes at the expense of other homes. To the extent this occurred, it would help banks and other lenders who owned foreclosed properties, at the expense of other homeowners, many of whom have already been hurt by declining home values.

Some analysts have noted that the proposed tax credit could even encourage foreclosures.[15] If the credit made it easier for banks and other lenders to sell foreclosed homes quickly, they might be more eager to foreclose on properties and less willing to renegotiate mortgage terms. In recent testimony before the Senate Banking Committee, former Treasury Secretary Larry Summers criticized the tax credit on these grounds. Summers emphasized the credit’s potential adverse effects and the fact that the benefits of the credit would flow to lenders rather than homeowners, explaining that “Providing tax credits conditioned on initiation of the foreclosure process is likely to have perverse effects — foreclosures may be encouraged, and the benefits will flow to financial institutions that have foreclosed on homes rather than to families in need.”[16]

Credit Poorly Targeted for Helping Communities

The proposed tax credit for purchases of foreclosed homes also would be an inefficient way to aid neighborhoods plagued by large numbers of foreclosures. The tax credit would not be targeted to such neighborhoods. Since demand almost certainly is stronger for foreclosed homes in areas with few foreclosures than in areas with many, most of the benefits of the tax credit would likely go to people who purchase homes that are not in areas with a high concentration of foreclosures. (The added funds that the Senate bill would provide for the Community Development Block Grant, by contrast, would be much better targeted on hard-hit-areas; see the box on page 8.)

The Non-Itemizer Property Tax Deduction

The Senate bill also includes a new property tax deduction for non-itemizers (that is for taxpayers who claim the standard deduction rather than itemizing their deductions). Homeowners who are struggling to keep their homes must pay property taxes (like all homeowners), and those who do not itemize would receive some assistance from this provision, provided their incomes are high enough for them to benefit from a tax deduction.

More Worthwhile Uses for the Funds that the Senate Bill Spends on Unhelpful Tax Cuts

In general, expenditure programs are likely to be more effective than tax cuts in addressing the foreclosure crisis, in part because such programs can better target assistance to families and communities that need it. The Senate bill’s dubious tax cuts would consume funds that could otherwise be used for much more targeted responses to the housing crisis, including the following:

- A proposal by Senator Chris Dodd and Rep. Barney Frank to have the Federal Housing Administration guarantee the restructuring of mortgages on certain properties that are at risk of foreclosure. This measure, which would provide a mechanism for large numbers of at-risk homeowners to work out new mortgage arrangements with lenders, would likely do more than any other to help families remain in their homes. (This proposal is discussed in more detail on page 10-11 of this analysis.) The Congressional Budget Office has estimated that the version of this proposal approved by the House Financial Services Commit

Yet this provision is poorly designed and poorly targeted. Millions of homeowners who own their homes outright, as well as millions of others who are not struggling with their mortgage payments, would benefit. Because the tax benefits would be spread so widely, they would be exceedingly small. The Senate bill’s deduction of $1,000 per couple ($500 per individual) which would cost $1.5 billion for one year but would provide a benefit worth only $100 to a couple in the 10 percent tax bracket and only $150 to a couple in the 15 percent tax bracket. (It would be worth $50 and $75, respectively, to singles in these brackets.) These amounts are too trivial to make a difference in protecting families facing foreclosure.

The idea of a non-itemizer property tax deduction appears to have arisen during a period when housing values were appreciating rapidly and property taxes were perceived to be a major burden on moderate-income homeowners. In today’s housing market, however, where property values are falling rather than rapidly rising, this issue is less important and the deduction makes little sense.

Low- and Moderate-Income Seniors Would Not Benefit From a Property Tax Deduction

Much of the concern around property taxes typically centers on seniors, for whom these taxes are sometimes thought to constitute a burden. Yet low- and moderate-income seniors would receive little or no benefit from the Senate’s property tax deduction for non-itemizers. They generally owe no income tax and hence could not use the deduction. (Social Security benefits are not taxable for low- and moderate-income beneficiaries, so seniors generally owe federal income tax only if they have substantial non-Social Security income.) Estimates from the Urban-Brookings Tax Policy Center indicate that 61 percent of elderly households would not benefit from any new federal tax deduction, because they have no federal income tax liability.[17]

Senate Provision Would Worsen Problems Facing Local Governments

The Senate bill also contains a related provision that would deny the new property tax deduction to residents of any locality that raised its property tax rate between April 2, 2008 and January 1, 2009. This provision would effectively prevent localities from raising property tax rates to help compensate for shrinking property tax revenues caused by falling home values. As a result, the Senate bill could force many hard-pressed localities to cut police, firefighting, schools, and other basic public services.

This provision would represent an inappropriate federal intrusion into local taxing authority. It also would intensify pressure on state governments to help make up the lost local revenue, despite the fact that many states are facing serious budget problems of their own. States — unlike the federal government — must balance their budgets, even during recessions.

In dealing with the current economic problems, a first principle for Congress should be to “do no harm.” Due to its effects on local governments, this provision fails that minimal test.[18]

This provision also would place unprecedented demands on the IRS and likely would be impossible for the IRS to administer. At least 40,000 towns, counties, and school districts levy property taxes, and in many cases, their boundaries do not correspond to other boundary measures such as zip codes. It would take a Herculean effort for the IRS to try to determine which tax filers live in areas that make them eligible for the tax deduction and which filers do not.

Tax Cut Provisions Entirely Unrelated to the Housing Crisis

The previous section of this analysis examined the $10.5 billion in tax cuts contained in the Senate bill that are supposed to be related to the foreclosure crisis but would actually provide little help in averting foreclosures (and in some cases, would likely have adverse effects). Another $9.8 billion in tax cuts in the Senate bill do not even purport to be related to housing or foreclosures.

The bulk of these unrelated tax cuts — $8.3 billion of them — consist of measures to extend various tax incentives for renewable energy. These provisions appear to have been added to the housing bill as a way to circumvent the Pay-As-You-Go budget rules that require such measures to be paid for. The Senate waived the PAYGO rules for the housing bill as a whole, on the grounds that it is important to act rapidly to address the foreclosure crisis and that including offsets in the bill would delay its enactment. Whatever the merits of that decision, it should not be abused to justify waiving PAYGO so that the Senate can extend unrelated tax cuts without paying for them. The tax provisions in question may well warrant extension, but if so, they warrant being paid for.

Bill Disappointing for What It Omits

The Senate housing bill does not include a proposal Senator Chris Dodd has developed and the House Financial Services Committee has adopted, under which the Federal Housing Administration would facilitate the restructuring of mortgages on homes at risk of foreclosure. Such a measure would provide a mechanism for large numbers of homeowners at risk of foreclosure to work out new mortgage arrangements.[19] Its absence from the Senate bill is a major omission; many experts believe it could substantially reduce the number of foreclosures and enable many homeowners in danger of defaulting on their mortgages to remain in their homes. Noted economist and former Federal Reserve vice-chairman Alan Blinder has written that such a measure “… [while] not a panacea, offers a smart approach to a knotty set of problems — an approach that should breathe some life into the housing market, the mortgage market, and the related securities markets.”[20]

Bankruptcy Provisions

During floor debate on the housing bill, the Senate rejected an amendment to modify bankruptcy laws to allow judges to write down the principal amount owed on a mortgage. This decision was unfortunate. Allowing judges in bankruptcy proceedings to write down the principal would be beneficial, as it would help bring about mortgage restructurings in which the interests of both parties have a chance to be weighed. In addition, for homes that have more than one mortgage lien, as many do, it may be difficult to make a workable arrangement among the necessary parties without the type of forum that a bankruptcy proceeding provides. The prospect of bankruptcy proceedings in which a judge could write down a mortgage also could have another beneficial effect — it could increase incentives for lenders to enter into restructuring agreements before that stage is reached.[21]

A number of leading mainstream economists, including Larry Summers, have advised that such a provision would be helpful in averting widespread foreclosures.[22] Critics of such a change in bankruptcy rules argue that it would increase the number of bankruptcy filings and lead to tighter restrictions on lending in the future. Summers has counseled, however, that while some lenders might increase the risk premium on future mortgages (to reflect the very modest increased possibility that they could incur losses as a result of bankruptcy proceedings), such concerns are substantially outweighed by the beneficial effects a bankruptcy provision would have in ameliorating the looming foreclosure crisis.

Congress Needs to Do Better

Since the Senate passed its housing bill, the House of Representatives has approved two bills to address the foreclosure problem. The first bill, H.R. 3221, combines Rep. Frank’s version of the proposal to have the FHA guarantee new mortgages for struggling homeowners with several other measures, including a housing tax package passed by the House Ways and Means Committee a few weeks ago. The Ways and Means bill represents a significant improvement over the Senate version, although it devotes several billion dollars to tax provisions that would not constitute an effective use of scarce resources.[23] The second bill (H.R. 5818) would provide $15 billion in grant and loan assistance to states and communities hit hard by foreclosures.[24]

As Congress moves forward on legislation to address the mortgage crisis, it should drop ineffectual tax provisions included in either the Senate bill or the House bill, include the important housing-related provisions that the Senate bill omits, and retain funding to stabilize communities hard hit by foreclosures and provisions to help renters. In addition, as Congress continues to refine its response to the foreclosure crisis, it should include measures to ameliorate the harm to innocent renters who lose their homes to foreclosure through no fault of their own.

End Notes

[1] The cost of a similar proposal that House Financial Services Committee Chair Barney Frank has crafted is $1.7 billion, according to the Congressional Budget Office, or $2.7 billion assuming that funds for administration and counseling are appropriated. CBO Cost Estimate for H.R. 5830, May 2, 2008.

[2] “Floor Statement of Senator Max Baucus Regarding Housing Tax Provisions,” April 3, 2008.

[3] This category includes the extensions of renewable energy tax incentives, the changes to rules governing Real Estate Investment Trusts (REITs), and the small provisions targeted to the Katrina-affected region and the areas affected by the March 2008 tornados.

[4] This category includes the net operating loss provision, the provision allowing businesses to receive refunds of Alternative Minimum Tax and research and development tax credits, a credit for purchases of foreclosed homes, and a non-itemizer property tax deduction.

[5] Loss “carrybacks” have a higher value than “carryforwards” because they are paid out immediately, instead of years in the future. In addition, companies cannot be certain they will have the opportunity to use all of their loss carryforwards.

[6] A smaller provision in the Senate bill also would allow corporations, under certain circumstances, to obtain refunds of certain business tax credits. The effects of this provision on the economy would likely be similar to the effects of the net operating loss provision. This provision would cost $1.4 billion over ten years.

[7] “Tax Relief for American Homebuilders: Baucus-Grassley Business Tax Provision Saves Jobs, Helps Struggling Companies Survive,” Committee on Finance News Release.

[8] See Citizens for Tax Justice, “The Senate’s Foreclosure Prevention Act Unfairly Rewards Big Business Over Middle-Class Americans,” April 7, 2008.

[9] These IRS data are limited to C corporations.

[10] Congressional Budget Office, “Options for Responding to Short-Term Economic Weakness,” January 2008.

[11] GS Weekly, September 21, 2007.

[12] “Tax Relief for American Homebuyers: $7,000 Credit for Purchase of Foreclosed Homes Will Aid Responsible Buyers, Raise Property Values,” Committee on Finance News Release.

[13] CBO Cost Estimate for H.R. 5830, May 2, 2008.

[14] The Joint Committee on Taxation estimates that the cost of the $7,000 credit which would be in effect for one year, is $1.6 billion. This suggests that the Joint Tax Committee expects 200,000-250,000 people to claim the credit. Even if all of these people were buyers who entered the housing market because of the credit, the boost to housing demand would still represent a modest fraction of the projected number of foreclosures. In reality, most of these individuals would probably be people who would have purchased homes anyway, meaning that the true boost to demand for housing would be much smaller.

[15] See for example, The Washington Post, “A Pro-Foreclosure Bill,” April 7, 2008.

[16] Lawrence H. Summers, “The Current Economic Situation,” Testimony Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, April 10, 2008.

[17] See Tax Policy Center Table T08-0012.

[18] For more discussion of this provision, see “Statement by Iris Lav, Deputy Director, on Provision in Bipartisan Senate Housing Package Affecting Local Property Taxes,” Center on Budget and Policy Priorities, April 3, 2008.

[19] These proposals would encourage mutually beneficial mortgage restructurings by having the Federal Housing Administration (FHA) guarantee new mortgages issued to struggling homeowners. Essentially, lenders could agree to allow homeowners to pay off existing mortgages at below face value (reflecting the reality of diminished home values) or to issue new mortgages to homeowners in amounts they could better afford to pay. The FHA would guarantee the new mortgages.

[20] Alan S. Blinder, “How to Cast a Mortgage Lifeline,” New York Times, March 30, 2008.

[21] Because the FHA refinancing proposal that Rep. Frank and Senator Dodd have proposed would be voluntary, the incentives that a bankruptcy provision would provide also could enhance the effectiveness of that initiative. The bankruptcy measure would thus complement the FHA proposal.

[22] See Lawrence H. Summers, “The Current Economic Situation,” Testimony Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, April 10, 2008, and Douglas W. Elmendorf, “Policies for Tackling the Mortgage Mess,” Testimony Before the U.S. Senate Committee on Banking, Housing, and Urban Affairs, April 10, 2008.

[23] For further discussion, see Aviva Aron-Dine, Barbara Sard, and Will Fischer, “Ways and Means Committee Housing Tax Package Improves Significantly on Senate Version: But Addressing the Foreclosure Crisis Will Require Other Measures,” Center on Budget and Policy Priorities, April 11, 2008.

[24] See “Statement by Barbara Sard, Director of Housing Policy, on House Action on Foreclosure Legislation,” Center on Budget and Policy Priorities, May 7, 2008.

Más de los autores

Areas of Expertise

Areas of Expertise