Adopting a State-Based Health Insurance Marketplace Poses Risks and Challenges

States Should Do So Only With a Clear Plan to Increase Coverage

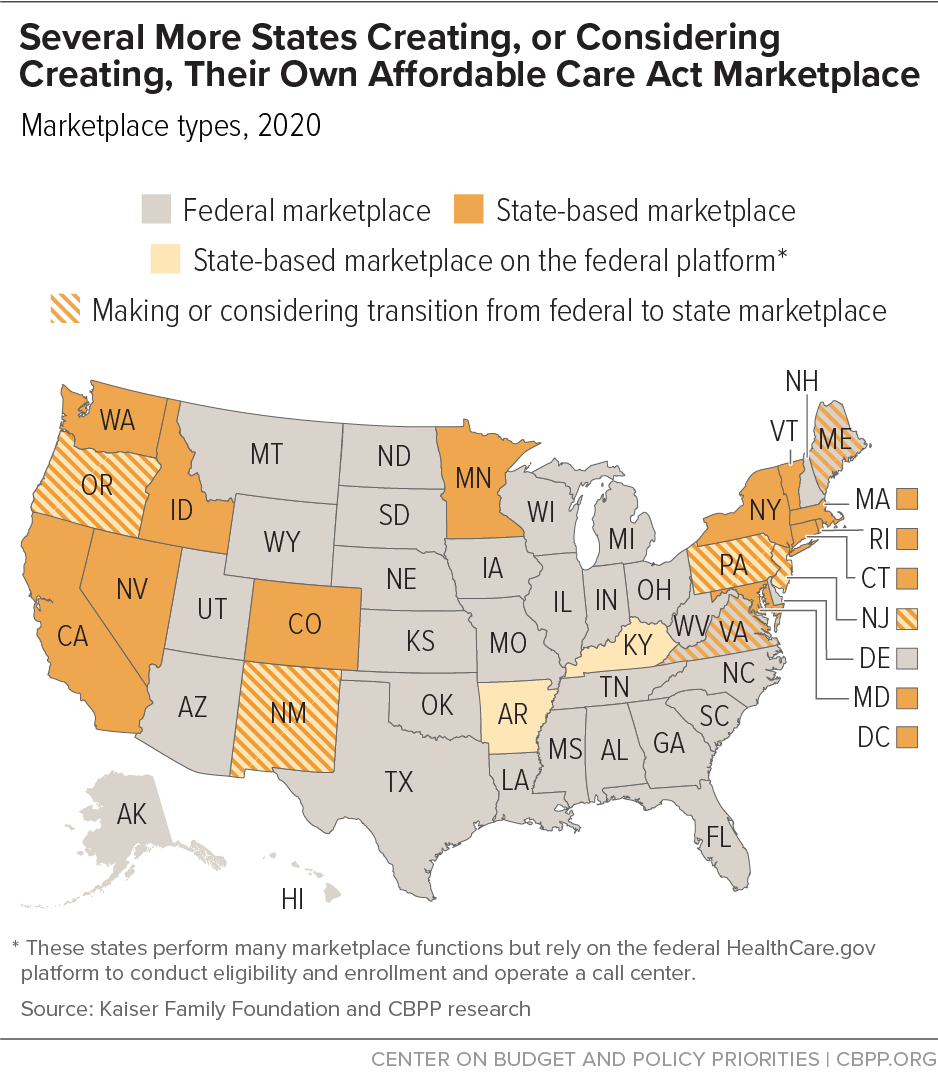

Several states are moving to launch their own health insurance marketplaces, citing hopes of saving money and gaining more control over marketplace functions that affect their residents. (See Figure 1.) But while establishing a state-based marketplace (SBM) presents important opportunities, it isn’t necessarily the right move for every state. States should weigh the decision carefully and pursue an SBM only as part of a well-developed plan to expand coverage. It is a means to an end, not an end unto itself.

"It is a means to an end, not an end unto itself."Policymakers in states that rely on the federal HealthCare.gov eligibility and enrollment platform or the full set of services provided by the Federally Facilitated Marketplace (FFM) understandably question the federal government’s commitment to running a well-functioning exchange. The Trump Administration supports repeal of the Affordable Care Act (ACA) and has cut funding for marketing and outreach of exchange plans, expanded the availability of skimpy non-marketplace plans, and used its regulatory authority to reduce marketplace financial assistance. Some state policymakers hope that establishing SBMs will protect their residents from at least some federal actions undermining the marketplaces. They also seek more control and authority over their marketplaces to improve operations, coordination across programs, and outreach and marketing.

States also hope they can reduce costs. User fees for states using the HealthCare.gov platform have risen in recent years (mainly because they are tied to premiums, which have risen), even as the cost of hiring vendors to provide exchange technology and related services has fallen as that market has matured. Some states believe they could operate a marketplace for considerably less than their consumers now pay in user fees.[1]

But transitioning to an SBM is no small task. It involves significant challenges and costs to states and risks to consumers. To do it successfully, states must procure services from one or more (possibly new) vendors; transfer data from the federal system; and ensure that their new marketplace can share information with Medicaid and the Children’s Health Insurance Program (CHIP), communicate with insurers, and maintain enrollment of existing marketplace consumers without a hitch. The technological challenges are likely familiar for state officials, who remember the technology failures when the ACA marketplace first launched (for HealthCare.gov and several SBMs). But states may be less aware of other complex functions that HealthCare.gov and the FFM now perform with reasonable success, such as conducting email outreach to consumers and addressing income-related data-matching issues that arise in the eligibility process. Even a state that avoids major technology failures could easily end up offering consumers a worse experience than they currently have, especially if it prioritizes keeping spending as low as possible.

Moreover, it would be a waste to put significant work and resources toward a transition only to end up with an SBM that simply mirrors the FFM’s capabilities. If a state is going to operate an SBM, it should do so to improve exchange operations, simplify the eligibility and enrollment process for consumers, improve coordination between the SBM and Medicaid, or offer additional financial assistance. States that transition to an SBM should have a plan to phase in near-term and longer-term improvements that would make this project worthwhile.

States that have decided to move forward with SBM transitions should:

- Set targets for increased enrollment that span all state health coverage programs.

- Make sure the SBM is prepared to at least match the FFM’s user experience and identify improvements the SBM can make right away.

- Prioritize significant investments in marketing, outreach, and enrollment assistance.

- Commit to a “no wrong door” eligibility and enrollment system, in which people who apply for health coverage are easily enrolled in the appropriate program — whether that is an SBM plan, Medicaid, or another state program — and make immediate strides toward “no wrong door” when the SBM launches.

- Ensure that SBM spending will be sufficient to provide high-quality services to residents and achieve the state’s other goals for the transition.

- Protect consumers from subpar health plans and problematic web-broker and insurer marketing practices.

- Leverage the establishment of an SBM to advance broader policy changes, such as additional subsidies to make coverage more affordable.

States still considering whether to establish an SBM should first evaluate whether taking most of those steps would be feasible. If not, the transition likely would not be worth the upheaval, costs, and risks involved.

Background: Types of Marketplaces

Under the ACA, each state must either operate its own marketplace (sometimes called an exchange) or rely on the federal marketplace to handle exchange functions such as certifying health plans that meet ACA standards and determining eligibility for exchange plans and subsidies.

In most states, the federal government runs the marketplace. The federal platform called HealthCare.gov handles eligibility and enrollment functions and the call center for consumers, and the marketplace collects a user fee from the insurers offering plans through it. The fee is 3.0 percent of exchange plan premiums in 2020.

Thirteen states run their own SBMs, meaning they take charge of all required functions and have their own systems for conducting eligibility and enrollment, operating a call center, and conducting consumer outreach and plan certification. These states pay no user fees to the federal government.

Another six states have a hybrid between the two: SBMs on the federal platform, or SBM-FPs, which take charge of many marketplace functions but rely on the federal HealthCare.gov platform to conduct eligibility and enrollment and operate a call center. These states pay the federal government a user fee that is set at a lower rate (2.5 percent of marketplace plan premiums in 2020) compared to full FFMs.[2]

The rest of this paper presents seven recommendations for states that have decided to move forward with SBM transitions.

1. Set Targets for Improved Enrollment in Health Coverage

Setting enrollment targets can help keep the goal of expanding coverage front and center, preventing states from focusing too narrowly on cutting costs or minimizing disruption. Setting targets across programs can also help ensure that the state includes lower-income residents eligible for Medicaid or CHIP in the push for improved health coverage.

Issues to Consider: Enrollment Targets

- What is an achievable goal for health coverage gains that the state could set for its first year and for subsequent years of operating an SBM?

- What more ambitious goals for coverage or affordability could the state set for future years?

States should develop targets by analyzing data on their remaining uninsured populations. Across states, the majority of the remaining uninsured have incomes low enough to qualify for subsidized marketplace coverage or Medicaid. Data analysis should show that expanding coverage will require increasing both Medicaid and marketplace enrollment, which could boost support for program coordination.[3]

2. SBMs Should at Least Match FFM’s User Experience and Should Identify Areas for Immediate Improvements

As noted, health insurance marketplaces are required by law to perform certain functions, including certifying health plans offered through the marketplace; maintaining a website, toll-free hotline, and navigator program to assist consumers; determining eligibility for marketplace subsidies; and connecting people eligible for Medicaid and CHIP with those programs. A state preparing to operate an SBM must maintain a basic level of functioning in all these areas through the transition.

The FFM generally performs these functions well, though not perfectly. It has addressed its early technology problems and greatly improved its eligibility and enrollment process in key areas, such as by improving the process when applicants must submit documentation to resolve data-matching issues related to their eligibility. The FFM also has a highly effective, low-cost email outreach program that sends multiple targeted messages to consumers, prompting them to take action at key moments. States using the FFM have benefitted from these advances, and future SBMs will need to wrestle with how to maintain this level of performance without repeating past mistakes that either the FFM or other SBMs have made.

While policymakers in states transitioning to an SBM will naturally focus on making it function on time, on budget, and with minimal disruption for consumers and other stakeholders, states should also consider how they can use their increased authority and flexibility to make meaningful improvements right away. This can help demonstrate tangible benefits of the SBM and a build a case for additional policy changes or spending, if needed. It also may help a state meet its targets for increased enrollment.

One simple policy a state could adopt is an extended annual open enrollment period. Many existing SBMs provide more than the six weeks the FFM allows (November 1 through December 15). This allows more time to conduct outreach and get more people to enroll, while also giving a fledgling SBM more time to address any issues that might arise in its initial years. Extending the enrollment period into January, as many SBMs do, also holds the advantage of getting past the holiday season and the end of the year — a time when low-income people face especially high financial stress, according to research.[4]

Another immediate improvement would be to make it easier to enroll in coverage through special enrollment periods (SEPs), which allow people who experience certain life events, such as loss of other coverage or the birth of a child, to enroll in a marketplace plan outside the annual enrollment period. In recent years, the FFM has added restrictions to certain SEP-triggering events, such as a requirement to have prior coverage. It has also instituted verification procedures that require people accessing an SEP to submit documentation (such as a letter from their former insurer or employer) proving their eligibility for an SEP before they can get coverage. These additional requirements can present a barrier to people using SEPs, and data suggest SEP use via the FFM has dwindled. But SBMs do not have to adopt the same restrictions or verification requirements, and many existing SBMs have opted instead for a simpler, more accessible system.

Transitioning to an SBM is also an opportunity for a state to implement policies supporting continuous enrollment in coverage, which can help a state meet its enrollment goals and reduce administrative burdens. For states without continuous eligibility for children in Medicaid and CHIP, the shift to an SBM may be a reason to consider adopting it, in order to reduce instances when people “churn” on and off those programs. States can also seek Medicaid waivers to implement continuous eligibility for adults, as Montana and New York have done.[5] On the SBM side, states can consider allowing easier access to marketplace plans throughout the year — rather than only during open enrollment — for people with low or moderate incomes, as Massachusetts does for people up to 300 percent of the federal poverty level. This allows many people eligible for significant subsidies to enroll without having to prove they qualify for a SEP-triggering event. This policy, along with strong integration with Medicaid and other factors, has helped Massachusetts become the only state where exchange enrollment actually increases throughout the year, instead of declining as in all other states.[6]

SBMs can also make a number of operational improvements. For example, as they develop their technology platform and call center plan, they can ensure that call center staff have access to specific information about a person’s application and where it is in the process, any communications that have gone out from the SBM, and other pertinent details. An SBM would also benefit from setting up a special system to efficiently address particularly complex or urgent issues a consumer might bring to the call center. For example, an SBM could create a small team of highly trained staff with the knowledge, ability, and authority to take call referrals and resolve such issues.

In addition, SBMs can offer consumers more ways to get help than the FFM does. Partly due to Trump Administration cuts to navigator funding, the FFM offers little in-person help. SBMs can spend more on navigators and consumer assisters that offer people impartial, in-person help with applications and enrollment, as well as walk-in centers such as those in Massachusetts and California. SBMs can also make greater use of text messaging to inform or prompt action by consumers, and they can improve the services and information available to people with limited English proficiency. SBMs can also improve notices sent to consumers, ensuring that they provide information specific to the consumer’s situation and actionable content the recipient can understand.

A major area where SBMs can immediately improve compared to the FFM is coordination with Medicaid and CHIP, as explained below.

Issues to Consider: Match and Improve on the FFM User Experience

To provide at least a basic level of service to consumers, among other activities, SBMs will need to:

- Provide a user-friendly experience

- Provide robust customer service on the phone, through the website, and in person.

- Make the SBM website and application available on a mobile device.

- Ensure the identity-proofing system for accessing an online application and account protects consumer information without creating unnecessary barriers.a

- Provide accurate and understandable information on the website to help people apply, compare plans, and complete enrollment.

- Provide a call center with well trained, well paid, and adequately supervised staff who have access to software enabling them to provide callers with accurate information specific to their situation.

- Deliver high-quality service and accessible materials to people with limited English proficiency and people who have disabilities.

- Provide customized notices to consumers that detail the specific actions they must take to secure and maintain coverage and subsidies.

- Coordinate with Medicaid and CHIP

- Avoid bouncing people from one program to another by ensuring that information transfers from the SBM to these programs are smooth and that the SBM has accurate eligibility information about the other programs.

- Ensure that the SBM can receive and act on account transfers from Medicaid and CHIP when families apply through the Medicaid agency and are ineligible for Medicaid and CHIP, or when their income increases while on Medicaid or CHIP.

- Limit data-matching issues. Simplify the process for addressing data-matching issues.b This includes reducing how often such issues arise, making it as easy as possible for consumers to submit documentation when needed, and allowing them to submit written explanations when documentation is not available.

- Data migration. Ensure that the SBM has access to consumer data to help target outreach and enrollment efforts during the transition (when it will need to obtain these data from the FFM) and after the transition.

a Identity proofing requires applicants to answer personal and financial questions (including past addresses and details about credit cards and loans) to verify who they are. This information is matched against available electronic data. But it presents challenges for some people (such as those with limited credit histories) and often is not required. See Terri Shaw and Shelby Gonzales, “Remote Identity Proofing: Impacts on Access to Health Insurance,” Center on Budget and Policy Priorities and Social Interest Solutions, January 7, 2016.

b Eligibility for marketplace plans and subsidies depends on a number of factors, including income and citizenship or immigration status. The information that applicants provide about their eligibility is checked against electronic data sources, but when there is an inconsistency (which can occur for many reasons), people must submit additional documentation or risk losing coverage or subsidies. See Judith Solomon, “Limiting Data-Matching Issues Could Help Stabilize Federal Marketplace Coverage,” Center on Budget and Policy Priorities, February 16, 2016.

3. Invest in Marketing, Outreach, and Enrollment Assistance to Help Reach Coverage Goals

States that have invested significant resources in marketing and outreach, such as California, have found it has greatly increased take-up of health care coverage, which in turn improved the risk pool.[7] Marketing and outreach can help drive people, including the uninsured, to the SBM when they need coverage, especially during the annual open enrollment period. Effective outreach to renewing enrollees can help ensure they maintain coverage and update their eligibility information. Enrollment assistance, such as through impartial navigators and consumer assisters, can help people get through hurdles in the enrollment process. Navigators have proven especially effective in reaching low-income and uninsured populations and helping people with complex circumstances get and maintain coverage.

This category of SBM spending is relatively small, though advertising costs vary significantly depending on local media markets. A survey of SBMs found that advertising spending per uninsured resident in 2018 was about $3 in Massachusetts and Minnesota, $10 in Maryland, and $14 in California, New York, and Rhode Island. State navigator spending per uninsured person ranged from roughly $2 in California and Vermont to $27 in Maryland and Minnesota.[8]

A strong outreach program may not necessarily require a large amount of funding, especially compared to other line items in an SBM’s budget. Therefore, outreach would be a particularly unfortunate area for new SBMs to skimp on because small dollar investments can yield high returns.

This is an area where states should be able to outperform the FFM, which has sharply cut back on investments in marketing and navigators. On the other hand, states cannot assume they will outperform the FFM, especially in email outreach, one of the highest-return approaches.[9] The FFM appears to have continued a robust email outreach program under the Trump Administration, and it benefits from a large email list, compiled since 2014, that includes existing consumers, past consumers, and others who have expressed interest in HealthCare.gov.

States should have a plan to obtain lists and coordinate outreach with the Centers for Medicare & Medicaid Services (CMS) during the transition. Even with such a plan, the consumer-level information available to states from the FFM may be limited, and states should recognize this as one challenge of the transition. States should aim to develop their own lists over time and to work with advocates, service and health providers, navigators, insurance brokers, and others within the state to disseminate information to potential consumers from the beginning.

Issues to Consider: Marketing and Outreach

- Is the state prioritizing investments in marketing, outreach, and consumer assistance?

- Is the state developing an effective, evidence-based outreach strategy, including both advertising and targeted email outreach?

- How will the state ensure it has a robust navigator program to reach low-income and uninsured populations, help people with complex circumstances, and provide unbiased help?

- As the state transitions away from HealthCare.gov, what data might be available to target outreach, marketing, and enrollment assistance to consumers?

4. Commit to a “No Wrong Door” Eligibility and Enrollment System

An especially critical area for SBMs to focus on is providing the “no wrong door” eligibility process that the ACA envisions, in which people submit one application and then can easily enroll in the health program for which they are eligible: an exchange plan, Medicaid, or CHIP. The “no wrong door” concept applies to all health insurance marketplaces, meaning they must provide at least minimal coordination across programs. But when a state administers both the marketplace and Medicaid, it can do far better than the FFM in this area.

One way to achieve “no wrong door” is to integrate the SBM’s eligibility process with that of other health programs, including Medicaid, as most first-generation SBMs did. This has clear advantages. Integrated eligibility systems are far better at providing a “no wrong door” experience than the FFM, which usually transmits information to state Medicaid agencies about applicants who appear likely eligible for Medicaid. Such transfers can be complex and require applicants to provide additional or duplicative information. An integrated system also provides a more streamlined process for enrollees, for example by allowing them to move more seamlessly from one program to another if their eligibility changes and by simplifying the eligibility and enrollment process when families have members who qualify for different programs.

But in general, most states launching the next generation of SBMs are not planning to integrate their eligibility systems with Medicaid and CHIP, at least not right away, as they are operating with smaller budgets and tighter timelines. Nevertheless, a state should ensure it provides a smooth, streamlined enrollment process for families. Surpassing the capabilities of the FFM in this area is a must-do for any state considering an SBM.

Low-income people experience income volatility that can affect their eligibility for health coverage and cause them to “churn” frequently between programs. States can use the greater flexibility and authority that comes with operating an SBM to protect residents from coverage gaps and losses.

At a minimum, in planning for an SBM, a state not integrating with Medicaid should work with the state Medicaid agency to establish close coordination between programs. One policy that could make great strides toward “no wrong door” would be to allow the SBM to make a final determination of eligibility for Medicaid and CHIP. If a state instead continues to transfer cases to the Medicaid agency for a determination, it should avoid making people provide additional, unnecessary information. For example it can ensure that electronic files the SBM transfers include details such as eligibility factors that the SBM has already verified and verification documents that applicants have submitted.

State health programs must ensure that their eligibility rules are aligned and that different programs’ notices are coordinated in the language they use and their directives to applicants, especially for notices informing individuals that they have been denied or terminated in one program but are likely eligible for another. States must contemplate how to ensure that families with members who qualify for different health programs (such as children in CHIP and parents in the SBM) can enroll in a streamlined manner and, if they have problems, file a single eligibility appeal. States should ensure the SBM call center workers are sufficiently trained in Medicaid and CHIP and should establish “warm hand-offs” so that when callers must be transferred to another call center or agency, they are sent directly to someone who can help them. In general, the state should provide a system that appears seamless across programs, even if it does not fully integrate its SBM with Medicaid and CHIP.

5. Ensure SBM Spending Will Be Sufficient to Provide Robust Services to Consumers

Although reducing costs is one reason states cite for switching to an SBM, savings are not guaranteed and, in any case, are not a sufficient reason to undertake an SBM transition. Prioritizing cost savings as a goal of an SBM transition could lead states to miss opportunities for progress toward other objectives. It could also constrain the SBM’s budget in ways that limit its ability to successfully serve state residents.

Clearly, SBMs forming now can operate at a lower cost than those formed prior to 2014. The new SBMs can lease exchange platforms already developed by private vendors, which is less costly than building their own technology infrastructures.[10] These vendors offer core exchange functions (the technology platform plus customer service features, including the call center) at a lower cost than the amount of user fees that a state’s insurers pay to use the FFM. States thus see an opportunity to continue collecting the same amount of user fees while using some of those revenues for other purposes.

But what does it cost to operate a strong exchange? There is no clear or uniform answer. As a starting point, it is useful to look at what several longstanding exchanges, including the FFM, spend per enrollee each year, as well as what several of the new SBMs plan to spend. An examination of the budget documents for several “first-generation” SBMs, as well as the FFM, shows that it costs roughly $240 to $360 per marketplace enrollee per year to run these exchanges. (See the Appendix.) While comparing different exchanges’ spending on an apples-to-apples basis is impossible due to differences in the policy decisions they have made, the populations they serve, and the functions they perform, this range provides a useful frame for examining the budgets and policy decisions of the second generation of SBMs.

The newer SBMs are, indeed, planning to spend less: in the range of $100 or $200 per enrollee, though the figure varies by state.[11] Nevada, which just transitioned to a full state-based marketplace for the 2020 plan year, expects to spend about $13 million per year (about $172 per exchange enrollee) once it reaches a steady state, compared to about $19 million per year if the state continued paying user fees to federal government as an SBM on the federal platform. [12] (See textbox, “Nevada’s Transition to an SBM.”)

State officials in New Jersey, where insurers owed $50 million in user fees to the FFM in 2019, have said they can use the same amount to serve their residents better than the FFM has done and plan to shift to an SBM for 2021.[13] Spending $50 million a year to operate an SBM would translate to about $217 per enrollee, but the state plans to spend far less (about $15 million in 2021) on its contracts for a technology platform and a consumer assistance center during its first year as a full SBM. State law requires the total user fees collected for the SBM to be held in a revolving trust that can be used only for start-up costs, exchange operations, outreach, enrollment, and “other means of supporting the exchange.” [14]

In Pennsylvania, which plans to launch a full SBM in 2021, officials have said it will cost as little as $30 million a year to operate — far less than the $98 million the state’s individual-market insurers are expected to pay toward the user fee in 2020.[15] Pennsylvania plans to continue collecting the user fee at the same level but is proposing to use between $42 million and $66 million in 2021 to establish and fund a reinsurance program that will reduce unsubsidized premium costs beginning in 2021.[16] Assuming about $100 million in total user fee collections, this leaves about $34 million to $58 million to fund the state’s exchange, or about $101 to $172 per exchange enrollee in the first year.

It remains to be seen whether the lower spending of the new SBMs will be sufficient to deliver high-quality services to consumers or to make meaningful improvements compared to the FFM. Compared to the first-generation SBMs, the new SBMs often take on a narrower set of IT changes and functions, instead focusing on basic functions akin to what the FFM has achieved.

Nevada’s Transition to an SBM

Nevada’s Silver State Exchange is the first “second-generation” exchange to be up and running as a full SBM, having just completed its first open enrollment period in December 2019. The state’s experience so far demonstrates that this transition is a significant undertaking and can present unexpected challenges.

Heather Korbulic, executive director of the exchange, said the launch was successful in several respects. The SBM met its timeline and budget targets, and the call center worked well, answering a large volume of calls before and during the enrollment period and addressing 90 percent of issues in one call.

Technical issues arose with the eligibility and enrollment process but were diagnosed and resolved quickly, she said. For example, early on, nearly all consumers were flagged for what is normally an uncommon data-matching issue: when the SBM sent their information electronically to the federal data services hub (a mechanism for state and federal agencies to exchange information for administering the ACA), the system found they may have other health coverage and asked them to upload documents to resolve the matter. The SBM contractor GetInsured identified the problem as faulty computer logic at the state exchange. Fixing the coding and cleaning up the data resolved the problem, and the affected consumers received accurate determinations.

Another surprise Korbulic cited was that a significant number of people (about 21,000) were found ineligible for Medicaid and transferred to the exchange. Some were newly applying to Medicaid during open enrollment; others were former Medicaid beneficiaries who had been found ineligible through Medicaid’s regular redetermination process. Nevada opted to replicate the FFM’s process for dealing with people who appear to be Medicaid eligible — namely, to transmit their case to the state Medicaid agency to complete the determination. While this reduced the complexity of the SBM transition, it can be a more fragmented process than having eligibility and enrollment processes that are integrated with Medicaid and other health programs so that people who apply at the exchange and are Medicaid eligible can be directly enrolled.

One benefit of Nevada now running its own exchange is that it has the information needed to conduct outreach to people found ineligible for Medicaid and encourage them to finish an application at the exchange within the 60-day deadline that applies to them. “We are aggressively pursuing them to let them know they are potentially eligible . . . and that will hopefully lead to an increase in our enrollment,” Korbulic said. The exchange lacked email addresses for most people who started their application with Medicaid, and she had just approved spending $8,000 on a mailer to tell them they need to come to the exchange to finish the process.

Overall, the Silver State Exchange saw plan selections dip by about 7 percent by the end of open enrollment, hitting 77,410 compared to 83,449 the prior year. Nationally, enrollment was flat. It’s unclear why enrollment fell in Nevada. (It also fell the year prior to the transition.) Korbulic suggested other potential factors, including that more people may have opted for a short-term health plan or health sharing ministry instead of health insurance that meets ACA standards. She plans to collect more data that can be used to improve the exchange’s enrollment and retention over time.

On the other hand, the new SBMs are still taking on major responsibilities, including some — such as customer service centers — where there is some uncertainty around costs. Vendor proposals to Nevada (as reviewed in a report to Oregon’s marketplace) provided staffing estimates that varied by several hundred percent and suggested training that ranged from four to 12 weeks for new staff.[17] And relying on vendors might not always be the most efficient option. Idaho’s exchange, for example, has found running its own call center to be cheaper and provide better customer service than contracting it out, though the state relies on the vendor GetInsured to provide its technology platform.

Issues to Consider: Budget and Spending

- Does the proposed budget (overall and for specific functions) provide enough resources to fulfill the required functions and meet the SBM’s enrollment goals?

- How do the state’s projected costs compare to other states and the FFM?

- Is the state’s user fee expected to cover all exchange costs? Might other funding sources be available, such as a state appropriation or allocated Medicaid funds?

- How will the state deal with any unanticipated expenses or delays?

- Can the vendors the state has chosen deliver high-quality services for consumers?

- Is the state planning for enough in-house capacity and staffing, and are some functions best performed in-house?

In addition to investing sufficient resources to provide high-quality services from the start, states will need to ensure that sufficient funds are available to make additional improvements in the future and to deal with any unexpected costs. For example, federal policy changes can raise costs for an SBM, and a state may lack the economies of scale to absorb the costs. Recent rule changes for health reimbursement arrangements are one example, as is a set of requirements for SBMs to conduct data checks of enrollee eligibility twice per year. [18]

6. Protect Consumers from Subpar Health Plans and Problematic Web-Broker Practices

In recent years, the federal government has put consumers at risk by expanding the availability of subpar health coverage and expanding alternative “direct enrollment” pathways for insurers and brokers without adequate protections.

Subpar plans include so-called short-term health plans, which a Trump Administration rule allows to last up to one year or longer. These plans are exempt from ACA standards and consumer protections, meaning that they can medically underwrite applicants, exclude pre-existing conditions from coverage, and do not include all the ACA’s essential health benefits. Subpar plans also include association health plans. A Trump Administration rule (currently blocked by the courts) allows these plans to offer coverage to individuals and small businesses that is exempt from many ACA standards.

All states have the authority to block or limit subpar plans, and it’s especially important that states transitioning to an SBM use the opportunity to assert their authority over their markets and protect consumers. Tightening the rules for health coverage markets outside the marketplace would enable any policy advances the state makes to reach more people, while also ensuring that SBM outreach and marketing efforts don’t have to compete with misleading and distracting marketing by the sellers of subpar plans. As a state seeks to boost enrollment in health coverage, it must avoid losing people to subpar plans that will leave them with high costs if they get sick.

Most SBM states have already banned or sharply limited short-term plans, as have some states moving toward or considering operating an SBM, such as New Mexico, New Jersey, and Oregon. But Pennsylvania has not yet done so, and protections in Nevada, Maine, and Virginia fall short of banning these plans or undoing the Trump Administration’s expansion.[19]

States opting to run their own exchanges should also prevent direct enrollment from detracting from the SBM project, whether by barring it altogether or by ensuring this process is subject to far stronger consumer protections than is the case in FFM states. Under direct enrollment (DE) and the recently expanded enhanced direct enrollment (EDE), the FFM lets insurers and web-brokers use their own websites to help consumers enroll in marketplace plans and marketplace subsidies with little to no interaction with the marketplace.[20] Some direct enrollment entities have a track record of steering consumers to subpar plans, failing to connect people with Medicaid and CHIP, and undermining competition among insurers based on price and quality by failing to show consumers all marketplace plans or comparative information.[21]

Issues to Consider: Consumer Protection

- Has the state implemented a ban or three-month limit on short-term health plans?

- Are there other non-compliant plans or health products that are popular in the state (such as health care sharing ministries, association health plans, or indemnity plans) that pose risks to consumers?

- How will the state make the SBM — rather than insurer and broker websites — the “go-to source” for individual health coverage?

Notably, California and several other SBMs do not allow DE or EDE. In the second generation of SBMs, one potential risk is that some states may consider creating alternative enrollment pathways to hold down call center and website volume (and potentially costs) at the SBM or in response to pressure from insurers that want the option to enroll people through websites that do not display their competitors’ plans.

States that decide to allow some form of direct enrollment via private entities would need to establish strong protections and comprehensive standards to avoid the problems with the FFM’s direct enrollment system. For example, a state could avoid allowing insurer websites to conduct DE or EDE, which is the most detrimental to competition, while also ensuring web-brokers can participate only if they present all information for all plans the SBM makes available and meet other standards. States that allow direct enrollment should also consider how they can ensure that web-brokers operate in a manner consistent with the “no wrong door” requirements when their customers appear eligible for Medicaid or other programs.

7. Use the Shift to an SBM to Achieve Broader Policy Changes

A state’s decision to set up its own marketplace creates an opportunity for more significant policy changes. In particular, operating an SBM makes it easier for a state to provide state-funded subsidies to supplement those the federal government already provides to help people afford marketplace plans. States that rely on the FFM have no way to seamlessly integrate state-funded subsidies with federal premium tax credits. If a state is willing to invest in a supplemental state tax credit, this is a good reason to make the transition to an SBM.

Several states with SBMs have moved or are considering moving in this direction:

- Massachusetts has long provided sizable subsidies to people with incomes up to 300 percent of the federal poverty level. For example, people with incomes below 150 percent of poverty are guaranteed a $0 premium plan option with low out-of-pocket costs, compared to premiums of $48 to $63 per month for benchmark coverage in other states.[22]

- Vermont provides supplemental premium and cost-sharing assistance to people with incomes between up to 300 percent of poverty.[23]

- California provides state subsidies, beginning in 2020, for people with incomes between 400 and 600 percent of poverty (who have incomes too high to qualify for the federal subsidies) and supplemental subsidies for people with incomes between 200 and 400 percent of poverty.[24]

- Maryland’s exchange is studying boosting subsidies for younger people, with the goals of reducing uninsurance among this group and improving the risk profile of its individual market.[25]

There is strong evidence that increasing subsidies boosts marketplace enrollment and reduces uninsured rates.[26] For example, a careful study of Massachusetts’ additional subsidies finds that cutting premiums by about $40 per month increases take-up of individual market coverage among eligible people by 14 to 24 percentage points, with larger effects at lower income levels.[27] Add-on subsidies for people who already qualify for federal premium tax credits can be especially cost effective for states: if the state subsidies lead more uninsured people to enroll, the federal government will cover most of the cost (through the premium tax credits), while the state pays only for the incremental subsidies.

An SBM transition can also create an opportunity for a state to consider other coverage policies not directly related to the SBM. For example, a number of states with SBMs have established individual mandate penalties to replace the federal mandate penalty, which was repealed beginning in 2019. Research shows that individual mandates boost coverage and strengthen the individual market risk pool,[28] and a new study shows they create opportunities for highly effective outreach to uninsured consumers.[29] At this time, New Jersey is the only state undertaking or considering an SBM transition that has adopted an individual mandate.

As noted, shifting to an SBM is a significant undertaking. States should not take this decision lightly and should focus on the bigger goal: increasing affordability and reducing uninsured rates among their residents.

Appendix: Estimating Spending by Selected Marketplaces

While it is impossible to compare different exchanges’ costs on a truly apples-to-apples basis, examining the budgets of longstanding exchanges — both state-run and the FFM — that serve millions of people can provide a sense of what it costs to operate one. As discussed in this paper, the new SBMs plan to operate at a lower cost than several existing SBMs, in the range of $100 to $200 per marketplace enrollee per year in several cases. For four “first-generation” SBMs that we examined, as well as FFM states, it costs about $240 to $360 per marketplace enrollee per year to operate. We arrived at these ranges using the following sources:

- For effectuated exchange enrollment (that is, the number of individuals who had an active policy in February 2019 and who paid their premium) in each state, we used “Early 2019 Effectuated Enrollment Snapshot,” Centers for Medicare & Medicaid Services, https://www.cms.gov/sites/default/files/2019-08/08-12-2019%20TABLE%20Early-2019-2018-Average-Effectuated-Enrollment.pdf. For effectuated enrollment solely in the FFM, we excluded states with full SBMs but included SBMs on the federal platform.

- For spending in the FFM states, we used the fiscal year 2018 actual spending on health insurance exchanges as reported in CMS budget documents. See “Justification of Estimates for Appropriations Committees, Centers for Medicare & Medicaid Services, Department of Health & Human Services, Fiscal Year 2020, pp. 178-183 and 212, https://www.cms.gov/About-CMS/Agency-Information/PerformanceBudget/FY2020-CJ-Final.pdf.

- For spending by California’s exchange, we used the fiscal year 2018-2019 budget for Covered California, June 15, 2018, p. 26, https://hbex.coveredca.com/financial-reports/PDFs/CoveredCA_2018-19_Budget-6-15-18.pdf.

- For spending by Massachusetts’ exchange, we used the Health Connector Administrative Finance Update, slide presentation at the July 12, 2018 board of directors meeting, p. 8, https://betterhealthconnector.com/wp-content/uploads/board_meetings/2018/07-12-18/Health-Connector-Administrative-Finance-Update-VOTE-071218.pdf.

- For spending by Minnesota’s exchange, we used the MNsure Three Year Plan, Fiscal Years 2019-2020-2021, prepared for the July 17, 2019 board meeting, https://www.mnsure.org/assets/Bd-2019-07-17-DRAFT-FY20-budget_tcm34-393218.pdf.

- For spending by Washington’s exchange, we used the Washington Health Benefit Exchange’s financial report for the August 23, 2018 board meeting, p. 4, https://www.wahbexchange.org/wp-content/uploads/2018/08/HBE_EB_180823_Finance-Update.pdf.

States differ in how much they invest in functions such as marketing and outreach to hard-to-reach populations and in how much they support small business enrollment. States also have different funding sources for their operations — an important parameter for what its exchange might have available to spend. Most exchanges charge user fees or assessments that are calculated as a percentage of the premiums that insurers charge, though states have made different decisions about which insurers pay the fees. Some state exchanges receive state appropriations, and those that handle enrollment for other programs (such as Minnesota and Washington) can receive Medicaid cost-allocation funding for the relevant exchange functions that support those enrollees.

End Notes

[1] Sabrina Corlette et al., “States Seek Greater Control, Cost-Savings by Converting to State-based Marketplaces,” Urban Institute, October 10, 2019, https://www.rwjf.org/en/library/research/2019/10/states-seek-greater-control-cost-savings-by-converting-to-state-based-marketplaces.html?cid=xem_partners_unpd_ini:moni%2011_dte:20191010.

[2] Kaiser Family Foundation, “State Health Insurance Marketplace Types, 2020,” https://www.kff.org/health-reform/state-indicator/state-health-insurance-marketplace-types/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Marketplace%20Type%22,%22sort%22:%22asc%22%7D.

[3] “Fact Sheets: Who are the Remaining Uninsured?” Center on Budget and Policy Priorities, March 21, 2019, https://www.cbpp.org/research/health/fact-sheets-who-are-the-remaining-uninsured; Aviva Aron-Dine, “Making Health Insurance More Affordable for Middle-Income Individual Market Consumers, CBPP, March 21, 2019. https://www.cbpp.org/research/health/making-health-insurance-more-affordable-for-middle-income-individual-market.

[4] Katherine Swartz and John Graves, “Shifting the Open Enrollment Period for ACA Marketplaces Could Increase Enrollment and Improve Plan Choices,” Health Affairs, July 2014, http://www.healthaffairs.org/doi/10.1377/hlthaff.2014.0007#.

[5] Continuous eligibility in Medicaid provides a full year of coverage regardless of changes in a family’s income. See Judith Solomon, “Medicaid: Compliance with Eligibility Requirements,” Center on Budget and Policy Priorities, testimony before the Senate Finance Subcommittee on Health Care, October 30, 2019, https://www.cbpp.org/health/medicaid-compliance-with-eligibility-requirements.

[6] Sarah Lueck, “Proposed Change to ACA Enrollment Policies Would Boost Insured Rate, Improve Continuity of Coverage,” Center on Budget and Policy Priorities, June 5, 2019, https://www.cbpp.org/research/health/proposed-change-to-aca-enrollment-policies-would-boost-insured-rate-improve.

[7] Peter V. Lee et al., “Marketing Matters: Lessons from California to Promote Stability and Lower Costs in National and State Individual Insurance Markets,” Covered California, September 2017, https://hbex.coveredca.com/data-research/library/CoveredCA_Marketing_Matters_9-17.pdf.

[8] Sabrina Corlette and Rachel Schwab, “States Lean In as the Federal Government Cuts Back on Navigator and Advertising Funding for the ACA’s Sixth Open Enrollment,” Commonwealth Fund, October 26, 2018, https://www.commonwealthfund.org/blog/2018/states-lean-federal-government-cuts-back-navigator-and-advertising-funding.

[9] Jonathan Cohn, “Trump Administration Says Obamacare Ads Don’t Work, But Federal Study Says They Do,” Huffington Post, September 20, 2017, https://www.huffpost.com/entry/obamacare-ads-trump-health-human-services_n_59c1dc7de4b0186c2206bdd3.

[10] “Summary analysis of Nevada and New Mexico marketplace technology platform RFIs,” Oregon Department of Consumer and Business Services memorandum from Victor Garcia to the Marketplace Advisory Committee, January 7, 2019.

[11] Effectuated enrollment data by state (representing the number of people who had an active policy) was used to calculate per enrollee spending. See “Early 2019 Effectuated Enrollment Snapshot,” Centers for Medicare & Medicaid Services, https://www.cms.gov/sites/default/files/2019-08/08-12-2019%20TABLE%20Early-2019-2018-Average-Effectuated-Enrollment.pdf.

[12] Fiscal and Operational Report, Silver State Health Insurance Exchange, June 30, 2019, p. 24, https://d1q4hslcl8rmbx.cloudfront.net/assets/uploads/2019/06/07B-FO_Report_06-30-2019.pdf.

[13] Ryan Hutchins, “New Jersey proposed state-based exchange,” Politico, March 22, 2019, https://www.politico.com/states/new-jersey/story/2019/03/22/new-jersey-proposes-state-based-obamacare-exchange-929807.

[14] “NJ Department of Banking and Insurance Announces Selection of GetInsured to Develop, Operate Technology Platform & MAXIMUS to Operate Consumer Assistance Center for State-Based Health Insurance Exchange,” News Release, January 6, 2020, https://www.state.nj.us/dobi/pressreleases/pr200106.html.

[15] Sarah Gantz, “Pennsylvania to shift from healthcare.gov to state-based insurance exchange,” Philadelphia Inquirer, July 2, 2019, https://www.inquirer.com/health/consumer/pa-state-based-exchange-health-insurance-obamacare-20190702.html.

[16] Commonwealth of Pennsylvania Comprehensive Description: State Innovation Waiver Application, Pennsylvania Insurance Department, November 2019, https://www.insurance.pa.gov/Coverage/Documents/State%20Based%20Exchange/1332/PA%201332%20Waiver%20Application%20Summary%20for%20Public%20Comment%20(2).pdf.

[17] “Summary analysis of Nevada and New Mexico marketplace technology platform RFIs,” op cit.

[18] Corlette et al., op. cit.

[19] We define “ban or sharp restriction” as a time limit of three months, a prohibition on the plans, or other standards that cause the plans to not be sold in a state. Sarah Lueck, “States Protecting Residents against Skimpy Short-Term Plans,” Center on Budget and Policy Priorities, July 24, 2019, https://www.cbpp.org/blog/states-protecting-residents-against-skimpy-short-term-health-plans.

[20] Under direct enrollment, consumers select plans on web-broker or insurer websites and are routed to HealthCare.gov to apply and get an official eligibility determination; under enhanced direct enrollment, consumers stay on the web-broker or insurer’s site during the entire process with eligibility determined by HealthCare.gov behind the scenes.

[21] Tara Straw, “Direct Enrollment in Marketplace Coverage Lacks protections for Consumers, Exposes Them to Harm,” Center on Budget and Policy Priorities, March 15, 2019, https://www.cbpp.org/research/health/direct-enrollment-in-marketplace-coverage-lacks-protections-for-consumers-exposes.

[22] Aviva Aron-Dine and Matt Broaddus, “Improving Subsidies for Low- and Moderate-Income Consumers Is Key to Increasing Coverage,” Center on Budget and Policy Priorities, March 21, 2019, https://www.cbpp.org/research/health/improving-aca-subsidies-for-low-and-moderate-income-consumers-is-key-to-increasing.

[23] Vermont Household Health Insurance Survey, Vermont Department of Health, 2018 Report, https://www.healthvermont.gov/sites/default/files/documents/pdf/VHHIS_Report_2018.pdf and “2020 Eligibility Thresholds,” Vermont Health Connect, https://info.healthconnect.vermont.gov/thresholds2020.

[24] “Projected Impacts of State Laws Affecting Health Care Consumers and Covered California in 2020,” Covered California, https://www.coveredca.com/news/pdfs/State_Subsidy_and_Mandate_Fact_Sheet.pdf.

[25] John-Pierre Cardenas, “2020 State Reinsurance Program Parameters & Plans,” Maryland Health Benefit Exchange Board Policy Presentation, September 9, 2019, https://www.marylandhbe.com/wp-content/uploads/2019/09/September-Board-Policy-Presentation-1.1.pdf.

[26] Aviva Aron-Dine and Matt Broaddus, “Improving ACA Subsidies for Low- and Moderate-Income Consumers Is Key to Increasing Coverage,” Center on Budget and Policy Priorities, March 21, 2019, https://www.cbpp.org/research/health/improving-aca-subsidies-for-low-and-moderate-income-consumers-is-key-to-increasing.

[27] Amy Finkelstein, Nathaniel Hendren, and Mark Shepard, “Subsidizing Health Insurance for Low-Income Adults: Evidence from Massachusetts,” American Economic Review, Vol. 109, No. 4, 2019, https://economics.mit.edu/files/15852.

[28] Matthew Fiedler, “How did the ACA’s individual mandate affect insurance coverage? Evidence from coverage decisions by higher income people,” Brookings Schaeffer Initiative for Health Policy, May 31, 2018, https://www.brookings.edu/research/how-did-the-acas-individual-mandate-affect-insurance-coverage-evidence-from-coverage-decisions-by-higher-income-people/.

[29] Jacob Goldin, Ithai Z. Lurie, and Janet McCubbin, “Health Insurance and Mortality: Experimental Evidence from Taxpayer Outreach,” NBER Working Paper No. 26533, December 2019, https://www.nber.org/papers/w26533.

Más de los autores