Critics Still Wrong on What’s Driving Deficits in Coming Years

Economic Downturn, Financial Rescues, and Bush-Era Policies Drive the Numbers

The data in this analysis has been updated, but this version has a detailed critique of a misleading report by the Heritage Foundation that places blame for the deficits on rapid growth in Social Security, Medicare, Medicaid, and interest costs, and dismisses the significance of weak revenues in general and the 2001 and 2003 tax cuts in particular.

To view the updated data see:

Economic Downturn and Bush Policies Continue to Drive Large Projected Deficits

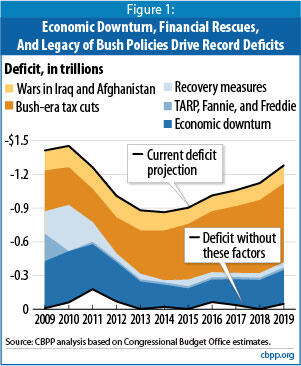

Some critics continue to assert that President George W. Bush’s policies bear little responsibility for the deficits the nation faces over the coming decade — that, instead, the new policies of President Barack Obama and the 111th Congress are to blame. Most recently, a Heritage Foundation paper downplayed the role of Bush-era policies (for more on that paper, see p. 4). Nevertheless, the fact remains: Together with the economic downturn, the Bush tax cuts and the wars in Afghanistan and Iraq explain virtually the entire deficit over the next ten years (see Figure 1).

The deficit for fiscal year 2009 was $1.4 trillion and, at nearly 10 percent of Gross Domestic Product (GDP), was the largest deficit relative to the size of the economy since the end of World War II. If current policies are continued without changes, deficits will likely approach those figures in 2010 and remain near $1 trillion a year for the next decade.

While President Obama inherited a dismal fiscal legacy, that does not diminish his responsibility to propose policies to address our fiscal imbalance and put the weight of his office behind them. Although policymakers should not tighten fiscal policy in the near term while the economy remains fragile, they and the nation at large must come to grips with the nation’s long-term deficit problem. But we should not mistake the causes of our predicament.

Recession Caused Sharp Deterioration in Budget Outlook

Whoever won the presidency in 2008 was going to face a grim fiscal situation, a fact already well known as the presidential campaign got underway. The Congressional Budget Office (CBO) presented a sobering outlook in its 2008 summer update,[1] and during the autumn, the news got relentlessly worse. Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that became embroiled in the housing meltdown, failed in early September; two big financial firms — AIG and Lehman Brothers — collapsed soon thereafter; and others teetered. In December 2008, the National Bureau of Economic Research confirmed that the nation was in recession and pegged the starting date as December 2007. By the time CBO issued its new projections on January 7, 2009 — two weeks before Inauguration Day — it had already put the 2009 deficit at well over $1 trillion.[2]

The recession battered the budget, driving down tax revenues and swelling outlays for unemployment insurance, food stamps, and other safety-net programs.[3] Using CBO’s August 2008 projections as a benchmark, we calculate that the changed economic outlook accounts for over $400 billion of the deficit each year in 2009 through 2011 and slightly smaller amounts in subsequent years. Those effects persist; even in 2018, the deterioration in the economy since the summer of 2008 will account for over $250 billion in added deficits, much of it in the form of additional debt-service costs.

Financial Rescues, Stimulus Add to Deficits in Near Term

The government put Fannie Mae and Freddie Mac into conservatorship in September 2008.[4] In October of that year, the Bush Administration and Congress enacted a rescue package to stabilize the financial system by creating the Troubled Assets Relief Program (TARP). Together, TARP and the GSEs accounted for $245 billion (including extra debt-service costs) of fiscal 2009’s record deficit. Their contribution then fades quickly (see Figure 1).

In February 2009, the new Obama Administration and Congress enacted a major package — the American Recovery and Reinvestment Act (ARRA) — to arrest the economy’s plunge. Mainstream economists overwhelmingly argued that, to combat the recession, the federal government should loosen its purse strings temporarily to spur demand, with a mix of assistance to the unemployed, aid to strapped state and local governments, tax cuts, spending on infrastructure, and other measures. By design, this package added to the deficit. Since then, policymakers have enacted several smaller measures to spur recovery and aid the unemployed. By our reckoning, the combination of ARRA and these other measures account for $1.1 trillion in deficits over the 2009-2019 period (including the associated debt service). Their effects are highly concentrated in 2009 through 2011 and fade thereafter, delivering a boost to the economy during its most vulnerable period.[5]

Bush Tax Cuts, War Costs Do Lasting Harm to Budget Outlook

Some commentators blame recent legislation — the stimulus bill and the financial rescues — for today’s record deficits. Yet those costs pale next to other policies enacted since 2001 that have swollen the deficit. Those other policies may be less conspicuous now, because many were enacted years ago and they have long since been absorbed into CBO’s and other organizations’ budget projections.

Just two policies dating from the Bush Administration — tax cuts and the wars in Iraq and Afghanistan — accounted for over $500 billion of the deficit in 2009 and will account for almost $7 trillion in deficits in 2009 through 2019, including the associated debt-service costs. [6] (The prescription drug benefit enacted in 2003 accounts for further substantial increases in deficits and debt, which we are unable to quantify due to data limitations.) These impacts easily dwarf the stimulus and financial rescues. Furthermore, unlike those temporary costs, these inherited policies (especially the tax cuts and the drug benefit) do not fade away as the economy recovers (see Figure 1).

Without the economic downturn and the fiscal policies of the previous Administration, the budget would be roughly in balance over the next decade. That would have put the nation on a much sounder footing to address the demographic challenges and the cost pressures in health care that darken the long-run fiscal outlook.[7]

The Effect of President Obama’s Budget

The key question is: where do we go from here? President Obama’s 2011 budget proposes to reduce anticipated deficits over the next ten years, chiefly by letting the Bush tax cuts for high-income taxpayers expire on schedule, closing certain tax loopholes and reforming the international tax system, keeping estate taxes at their 2009 parameters, enacting health care reform, and freezing (in aggregate) most appropriations for non-security domestic programs for the next three years. The President also supports another round of temporary recovery measures that would boost the deficit in 2010 through 2012, a proposal that is appropriate in size and well targeted.[8] Center on Budget and Policy Priorities’ analyses have found that in aggregate, the President’s proposals would reduce deficits over the 2011-2020 period by an estimated $1.3 trillion.[9]

Like most fiscal analysts, we believe that the Administration and Congress will need to take considerably larger steps. The President himself acknowledges that his proposals do not fully put the budget on a sustainable footing and has established a bipartisan fiscal commission to recommend more substantial deficit reductions. First and foremost, policymakers will need to restrain the growth of health care costs. The health reform legislation begins that process. It takes important initial steps to restructure the health care payment and delivery systems and to move away from paying providers for more visits or procedures and toward rewarding effective, high-value health care. As we learn more about how to slow health care cost growth without endangering health care quality, strong additional measures will be essential. But restraining health care cost growth will not itself be sufficient to address the long-term fiscal problem. Other actions also will be needed, including steps to raise additional revenue and make changes in other programs.

Heritage Foundation’s Analysis is Misleading

A recent Heritage Foundation report claims that tax cuts and other policies initiated during the Bush administration are not a significant factor behind the deficits we face in the coming decade.[10] Heritage places blame for the deficits squarely on rapid growth in Social Security, Medicare, Medicaid, and interest costs, and dismisses the significance of weak revenues in general and the 2001 and 2003 tax cuts in particular. But Heritage’s analysis is both misguided and seriously misleading.

- Heritage ignores the fact that rapidly-rising interest costs — one of its “culprits” behind rising outlays — result in significant part from the tax cuts and other fiscal policies of the Bush era . The tax cuts and the wars in Iraq and Afghanistan accounted for over $2.6 trillion of our national debt by the end of 2008 and, if continued, will add another $7 trillion in debt by 2019. In that year alone, about $450 billion of our interest bill will stem from those two policies. It is disingenuous to tar interest as a “fast-growing” spending program while ignoring which policies — including tax cuts — account for that fact.

Heritage admits that it understates the cost of the tax cuts by omitting their impact on rising net interest costs. “On the other hand,” Heritage asserts, “the original CBO scores of tax cuts have been underestimates because they excluded all supply-side feedback effects and overestimated the GDP between 2008 and 2011, which made all revenue and tax cut projections appear larger.” That convenient justification, however, misses the boat. We know that the tax cuts led to higher borrowing and larger debt-service costs. We do not know that they led to extra economic activity (or that they would have a positive effect on economic activity if made permanent). In fact, analyses of so-called “dynamic scoring” of tax cuts have found that: 1) such estimates generally come close to the standard estimates;[11] 2) stimulative effects may appear strong in the short run but tend to dissipate over longer horizons; and 3) most importantly, as both CBO and the Joint Committee on Taxation have concluded, large tax cuts financed by borrowing can harm the economy over the long term rather than help it. [12] In short, there is no reason to ignore the enormous debt overhang that the Bush tax cuts caused and plenty of reason to be skeptical of their economic benefits. Including the interest costs, the Bush-era tax cuts account for over $700 billion — or nearly 55 percent — of the deficit projected for 2019 under current policies. - Heritage ignores the fact that the share of deficits accounted for by the Bush-era tax cuts will grow in future years as the impact of the economic downturn on deficits diminishes . Because the economic downturn and efforts to combat it have such a large effect on the deficit in 2010, the share of the deficit accounted for by the tax cuts seems relatively modest; we estimate that the tax cuts account for about one quarter of the 2010 deficit. But as the effects of the downturn recede, the tax cuts will account for a much larger share. In 2019, the tax cuts, if continued, will account for nearly three-fifths of the deficit. And, despite the growing impact of rising health care costs and the continued aging of the population after 2019, the tax cuts will continue to have a major impact on the deficit. The Center has estimated that not extending the tax cuts — or fully paying for the cost of extending them — would reduce the projected budget shortfall through 2050 by two-fifths. [13]

- In constructing its baseline, Heritage partly assumes its own conclusion. The baseline projections developed by Heritage generally resemble CBPP’s, with one crucial difference. Heritage assumes that regular discretionary spending (other than war costs and stimulus funds) will grow at the same rate as the GDP over the next 10 years. In contrast, we assume that such appropriations will grow somewhat more slowly in the 10-year budget window because they will grow with inflation; this is the standard, widely accepted baseline assumption. Heritage’s decision to scrap normal baseline practices and assume higher levels of discretionary spending boosts such spending by more than a full percentage point of GDP by the end of the ten-year period and adds to interest costs as well. Heritage then uses this increased spending it assumes to buttress its claim that it is excessive spending growth that causes the deficit. In theory, policymakers might choose to increase discretionary spending to keep pace with GDP, but that is highly unlikely in these straitened times. And that is not how the Budget Enforcement Act, CBO, and the Office of Management and Budget define “current policy” when they make their baseline budget projections for the coming decade. [14]

- It was not a sudden spurt of growth in Social Security, Medicare, and Medicaid that turned projected budget surpluses into deficits . CBO and many budget analysts have long pointed out that the “big three” entitlement programs will swell in future decades as a result of an aging population and steady growth in per-capita health-care costs.[15] Indeed, CBO had already projected that this would eventually occur when, in 2001, it projected significant budget surpluses through 2011 and years beyond . [16] Since the growth in these large programs was anticipated (other than the growth due to enactment of the Medicare prescription drug benefit), it is not what turned projected surpluses to deficits.

Moreover, although CBO was projecting years of surpluses as the Bush Administration took office in 2001, it nevertheless warned that the nation’s long-term fiscal health was worrisome. The Bush Administration and Congress nevertheless opted to ignore these warnings and to cut taxes deeply, establish a Medicare drug benefit without covering its costs, and fight two wars on borrowed money.

Technical Note

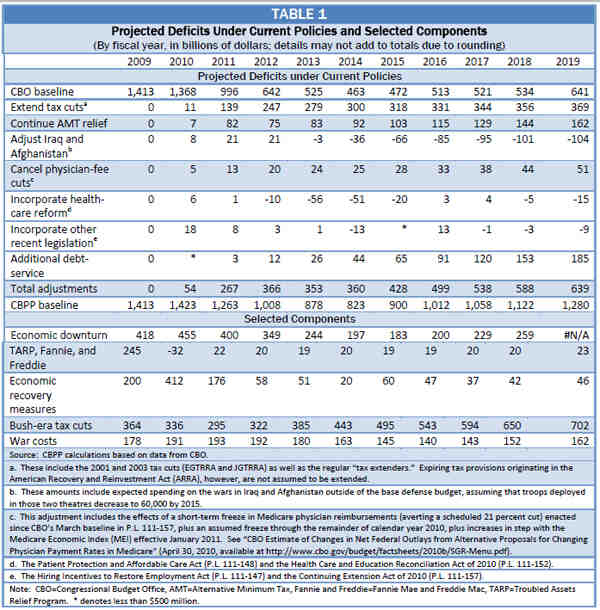

Baseline projections depict the likely path of the federal budget if current policies remain unchanged. We base our estimates on CBO’s latest ten-year projections, published in March 2010, with several adjustments to reflect what will happen if we continue current tax and spending policies.

Specifically, our baseline includes the budgetary effects of continuing the 2001 and 2003 tax cuts that are scheduled to expire after 2010, renewing certain other so-called “tax extenders” such as the research and development tax credit, and continuing relief from the Alternative Minimum Tax (AMT). Our baseline also assumes the effects of continuing to defer scheduled cuts in payments for Medicare providers, as has routinely occurred in recent years, and instead providing doctors with a payment increase based on the Medicare Economic Index. We also account for a gradual phase-down of operations in Iraq and Afghanistan. In all cases we based our adjustments on estimates published by CBO.

We calculated major components of the deficits as follows:

- Economic downturn — This category includes all changes in the deficit that CBO labeled “economic” in the five reports — in January, March, and August 2009 and January and March 2010[17] — that it has issued since September 2008, which total $1 trillion over the 2009-2018 period. It also includes the bulk of revenue changes that CBO classified as “technical.” In the revenue area, so-called technical changes essentially refer to trends in collections that CBO’s analysts cannot tie directly to published macroeconomic data. In fact, those data become available with a lag and are subject to major revision; weak revenues are often a tipoff that the economy is worse than the official statistics suggest. Furthermore, some key determinants of revenues — such as capital gains on stock-market transactions — are tied to the economy, but those influences are not captured by the standard macroeconomic indicators. Because the economic-versus-technical distinction is so arbitrary for revenues, we have ascribed most of CBO’s large, downward “technical” reestimates to the economic downturn. We add the associated debt-service costs. The technical reestimates to revenues and the associated debt-service costs add $1.5 trillion and $0.4 trillion, respectively, to this category over the 2009-2018 period.

Combined, the factors that we ascribe to the economic downturn account for nearly $3 trillion in extra deficits in 2009 through 2018. [18] - TARP, Fannie, and Freddie — The Treasury spent $243 billion for these entities in 2009 ($151 billion for TARP and $91 billion for Fannie Mae and Freddie Mac, net of dividends received). Projections for 2010 through 2019 come from CBO’s January 2010 baseline. We computed the extra debt-service costs, which total $111 billion over the 2009-2019 period. (By 2014, virtually the entire cost shown in Table 1 represents debt-service costs.)

- Recovery measures — When ARRA was passed, it bore a “headline” cost of $787 billion as officially estimated by CBO. [19] In January 2010, CBO revised that figure to $862 billion, chiefly to reflect higher costs than initially expected for ARRA’s provisions governing unemployment insurance and the Supplemental Nutrition Assistance Program (commonly known as food stamps) — primarily as a result of economic conditions — and for Build America Bonds.[20] We removed the portion of ARRA costs ascribed to indexing the AMT for another year.[21] Annual AMT “patches” have been a fixture since 2001, and ARRA just happened to provide the vehicle. The AMT provision accounted for $70 billion of ARRA’s $862 billion cost, leaving $792 billion. CBPP then added the cost of several smaller, discrete recovery measures that have been enacted in late 2009 and early 2010, totaling $84 billion in 2010 (but just $38 billion over the 2010-2019 period).[22] We then added the associated debt-service costs, which amount to $317 billion over the 2009-2019 period.

- Bush-era tax cuts — Through 2011, the estimated impacts come from adding up past estimates of various changes in tax laws — chiefly the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA), the Jobs and Growth Tax Relief Reconciliation Act of 2003 (JGTRRA), the 2008 stimulus package, and a series of annual AMT patches — enacted since 2001. Those estimates were based on the economic and technical assumptions used when CBO and the Joint Committee on Taxation (JCT) originally “scored” the legislation, but the numbers would not change materially using up-to-date assumptions. Most of the Bush tax cuts are scheduled to expire after December 2010 (partway through fiscal 2011). We added the cost of extending them, along with continuing AMT relief, from estimates prepared by CBO and JCT.[23] (We did not assume extension of the temporary tax provisions enacted in ARRA.) Together, the tax cuts account for $1.7 trillion in extra deficits in 2001 through 2008, and $3.4 trillion over the 2009-2019 period. Finally, we added the extra debt-service costs caused by the Bush-era tax cuts, amounting to more than $200 billion through 2008 and another $1.7 trillion over the 2009-2019 period — over $330 billion in 2019 alone.

- War costs — Spending for operations in Iraq and Afghanistan and related activities cost $610 billion through fiscal 2008, according to CBO ($575 billion for the Department of Defense and $35 billion for international affairs), and another $160 billion in 2009. [24] We based estimates of costs in 2010 through 2019 on CBO’s projections, adjusted for a phase-down to 60,000 troops; those costs come to $1 trillion.[25] We add the associated debt-service costs, which came to $64 billion through 2008 and will total another $684 billion over the 2009-2019 period ($119 billion in 2019 alone).

What About the Medicare Prescription Drug Benefit?

One of the major domestic initiatives of the Bush Administration was enactment of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (known informally as the Medicare Modernization Act, or MMA). The MMA created a new prescription-drug benefit in Medicare, known as Medicare Part D. This legislation was only partly paid for, and it added significantly to the deficit that President Obama inherited. Why is it absent from this analysis?

The Congressional Budget Office initially estimated that the MMA would add to the deficit by $395 billion over its first decade, spanning the years between 2004 and 2013. (Medicare’s chief actuary pegged the net cost significantly higher — at $534 billion over that period.) CBO’s estimate consisted of $552 billion in net spending — new benefits, partially offset by premiums and by receipts from the states — for the new Medicare drug benefit itself, minus $157 billion in savings in Medicaid and other federal programs. Although that “headline” estimate spanned ten years, costs were negligible in the first two years, because the new benefit took effect in January 2006.

Part D outlays are coming in somewhat lower than CBO and the Medicare actuary expected, but it is not possible to update the original price tag for the entire MMA. CBO now expects the net cost of Medicare Part D over that initial 2004-2013 period to be about $385 billion (as compared to the original $552 billion figure), excluding any effects from the newly-enacted health reform legislation. But, it is not possible to tell whether the savings in Medicaid and other programs have deviated from CBO’s original estimate of $157 billion. While Part D is a new, identifiable account in the federal budget, those other effects represent relatively small changes in large, ongoing programs.

In short, we did not include the costs of the prescription-drug program in this analysis because we could not estimate those net costs with the same confidence that we could estimate costs, based on CBO analyses, for other Bush-era policies — namely, the tax cuts and the wars in Iraq and Afghanistan. Over the 2009-2019 period that is this paper’s focus, CBO now expects net outlays for Part D to total approximately $880 billion (almost $130 billion in 2019 alone), but some fraction of that will be offset by savings in Medicaid and other programs that we are not able to estimate. Nevertheless, it is clear that, as noted above, enactment of the prescription-drug program added materially to the deficit that the current administration inherited.

Conspicuously missing from this list is the Medicare prescription-drug program that Congress enacted in 2003. That new program has also added significantly to deficits through 2019, but data limitations leave us unable to quantify its net budgetary effects (see the box above).

End Notes

[1] Congressional Budget Office, The Economic and Budget Outlook: An Update (September 2008). As CBO itself acknowledged, its baseline employed some arguably unrealistic assumptions about the expiration of the Bush tax cuts and other policies; several other organizations pegged future deficits much higher than CBO’s official estimates. See, for example, the Concord Coalition, “Setting Expectations: Why Baselines Matter in the Presidential Campaign and for the Fiscal Future” (September 11, 2008); Cato Institute, “$1 Trillion Budget Deficit by 2017?” (September 11, 2008).

[2] Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2009 to 2019 (January 2009).

[3] At the same time, the recession pushed down inflation and interest rates, which generated some offsetting savings.

[4] That occurred on September 7, 2008 — too late for inclusion in the CBO report issued just two days later.

[5] CBO estimates that ARRA boosted the number of people employed in the United States by 1.2 million to 2.8 million in the first quarter of 2010 (more, if measured on a full-time-equivalent basis) and that real (inflation-adjusted) GDP was 1.7 percent to 4.2 percent higher than it would have been if ARRA had not been enacted. Under CBO’s latest projections, ARRA’s impact on real GDP and employment will peak in the middle of 2010. Congressional Budget Office, Estimated Impact of the American Recovery and Reinvestment Act on Employment and Economic Output from January 2010 Through March 2010, May 2010, pp. 1-2.

[6] As explained in the technical note at the end of the paper, this analysis assumes that expiring tax cuts will be extended and new funding will be provided for the wars in Iraq and Afghanistan.

[7] See Kathy Ruffing, Kris Cox, and James Horney, “The Right Target: Stabilize the Federal Debt,” Center on Budget and Policy Priorities, January 12, 2010.

[8] Kris Cox, “President’s Budget Requests $266 Billion to Support Economic Recovery,” Center on Budget and Policy Priorities, February 5, 2010.

[9] Kathy A. Ruffing and James R. Horney, “Obama Budget Reduces Deficit by $1.3 Trillion Over Next Decade Compared to Current Policies,” Center on Budget and Policy Priorities, April 5, 2010. The Congress subsequently enacted several major proposals — including health-care reform and changes in higher-education programs — that constitute part of that $1.3 trillion in estimated savings.

[10] Brian M. Riedl, “The Three Biggest Myths About Tax Cuts and the Budget Deficit” (Heritage Foundation, June 21, 2010).

[11] Even the Bush Treasury Department estimated that, if the cost of extending the 2001 and 2003 tax cuts were paid for, the tax cuts would generate only enough economic growth to offset less than 10 percent of their long-term costs. And, of course, the 2001 and 2003 tax cuts were not paid for. See, U.S. Department of Treasury, “A Dynamic Analysis of Permanent Extension of the President’s Tax Relief,” July 25, 2006.

[12] Jason Furman, “A Short Guide to Dynamic Scoring” (Center on Budget and Policy Priorities, August 24, 2006); “Evidence Shows That Tax Cuts Lose Revenue” (Center on Budget and Policy Priorities, July 21, 2008).

[13] Ruffing, Cox, and Horney, “The Right Target.”

[14] The Budget Enforcement Act stipulates that the baseline projections should assume that discretionary spending grows at the rate of inflation. CBO, the Office of Management and Budget, and CBPP all follow these rules in their 10-year current-policy baseline projections. In projections of discretionary spending beyond the 10-year window, CBPP also takes into account population growth in order to reflect the long-term increase in demand for services that will result from slow, but steady, increases in the size of the population. CBO and some other analysts do assume in their long-term projections that discretionary spending will grow at the same rate as the economy after 2019, but as Alan Auerbach and William Gale explain in their analysis of the long-term fiscal problem, this choice reflects an assumption about future policy choices, not the cost of continuing current policies. (Auerbach and Gale note that “our forecast assumes that a richer society will want to spend more on discretionary spending, going beyond the current services provided by government.”) Alan J. Auerbach and William G. Gale, “Déjà vu All Over Again: On the Dismal Prospects for the Federal Budget,” Urban-Brookings Tax Policy Center, April 2010, p. 7.

[15] CBPP did so most recently in “The Right Target” (January 12, 2010).

[16] Congressional Budget Office, The Long-Term Budget Outlook (October 2000); The Budget and Economic Outlook: Fiscal Years 2002-2011 (January 2001).

[17] Congressional Budget Office, The Economic and Budget Outlook (January 2009),A Preliminary Analysis of the President’s Budget and an Update of CBO’s Budget and Economic Outlook (March 2009),The Budget and Economic Outlook: An Update (August 2009); The Economic and Budget Outlook (January 2010); and An Analysis of the President’s Budgetary Proposals for Fiscal Year 2011 (March 2010).

[18] Estimates are not available for 2019 because CBO’s August 2008 projections ended in 2018. For Figure 1, CBPP arbitrarily assumed that this category amounted to $300 billion in 2019 — a continuation of the previous few years’ pattern.

[19] See Congressional Budget Office, cost estimate for H.R. 1, American Recovery and Reinvestment Act of 2009 (February 13, 2009, online at www.cbo.gov) and Joint Committee on Taxation, “Estimated Budget Effects Of The Revenue Provisions Contained In The Conference Agreement For H.R. 1, The ‘American Recovery And Reinvestment Tax Act Of 2009’” (February 12, 2009, online at www.jct.gov).

[20] See Appendix A, “The American Recovery and Reinvestment Act of 2009” in CBO January 2010.

[21] That one-year fix — made necessary by the interaction of the AMT and the 2001 and 2003 tax cuts — is instead combined with the “Bush-era tax cuts,” below.

[22] Specifically, these reflect measures enacted in fall 2009 (Public Laws 111-92 and 111-118) to extend the homebuyers’ credit, allow businesses to carry back certain operating losses, extend and expand the tax credit for continuation of health insurance coverage for workers who lose their jobs, and lengthen the duration of emergency unemployment compensation They also reflect further extensions of aid to the unemployed and to businesses that hire them enacted in early 2010 (Public Laws 111-144, 111-147, and 111-157). Several of those measures included temporary provisions to avert reductions in fees paid to physicians by Medicare; we have removed those costs from the calculation of the effects of recovery measures, because we view them as an expression of current policy rather than new policies.

[23] CBO January 2010, “The Budgetary Effects of Selected Policy Alternatives Not Included in CBO’s Baseline” (Table 1-5) and unpublished backup from CBO.

[24] CBO January 2010, “Funding for Operations in Iraq and Afghanistan and Other Related Activities” (Box 1-1).

[25] CBO January 2010, Table 1-5.

Más de los autores

Areas of Expertise