Ways And Means Social Security Bill Could Include Costly, Poorly Targeted Retirement Tax Proposals

House Ways and Means Chairman Thomas has suggested that new tax cuts to promote retirement savings should be considered as part of Social Security reform. Expanding retirement saving — especially among low-income families, many of whom have little or no savings — is an important goal, and steps like making contributions to 401(k)s more automatic could produce important progress. To avoid worsening the nation’s fiscal outlook, however, any such changes must be paid for, both over the first decade and over the long term.

Unfortunately, a growing number of proposals are vying for the committee’s consideration that would carry significant long-term costs while providing the bulk of their retirement benefits to high-income individuals, the group least in need of new tax incentives to save adequately for retirement.

Some Unsound Proposals That May Be Considered

- Eliminating the income limits on Roth IRAs, currently $160,000 for married filers and $110,000 for single filers. The Administration’s proposal to establish Retirement Savings Accounts would eliminate these income limits.

- Raising the contribution limits for IRAs and 401(k)s, which under current law will rise to $5,000 per worker for IRAs and $15,000 per worker for 401(k)s over the next few years. (Limits are higher for those aged 50 and over.) Further increases beyond those set in current law have been proposed.

- Creating new retirement tax breaks linked to health costs. Various proposals with influential backers, such as Merrill Lynch or Fidelity, would allow people to make substantial tax-deductible contributions to investment accounts, receive earnings on the accounts that are entirely sheltered from taxation, and then withdraw funds tax-free in retirement as long as the amounts withdrawn do not exceed the retiree’s out-of-pocket health care costs in that year. These accounts would violate the long-standing principle that retirement accounts can feature tax-deductible contributions or tax-free withdrawals, but not both.

Problems with These Proposals

These proposals ultimately would worsen the nation’s already serious long-term deficit problems. Several of these proposals would prove very costly over time. Over the next 75 years, the Retirement Savings Account proposal alone would cost an amount equal to roughly 10 percent of the Social Security shortfall during that period, the Brookings-Urban Institute Tax Policy Center has estimated.

Generally, the bulk of the revenue losses caused by these proposals would not occur until people retire and withdraw funds tax-free that otherwise would be taxed. As a result, the cost of these proposals is “backloaded,” meaning it is relatively small in the first decade but would grow sharply in succeeding decades. These backloaded costs would mount at the same time that the baby boomers are retiring in large numbers and the nation faces deficits of unprecedented magnitude.

Also, many retirement-related tax breaks would worsen states’ long-term revenue outlook because most states tie their definition of taxable income to the federal definition.

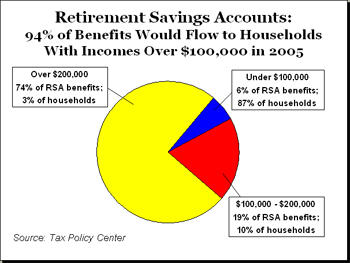

The proposals would provide the most help to those who least need it, and little help to the middle class. The Retirement Savings Account proposal, for example, would benefit only those people who earn more than the current income limits on Roth IRAs. The Tax Policy Center has found that if this proposal were in effect in 2005, some 74 percent of its tax benefits would go to the three percent of households with incomes over $200,000, and 94 percent of the benefits would go to households with incomes over $100,000.

Similarly, raising the IRA and 401(k) contribution limits would benefit only the small fraction of people who can afford to contribute the current maximum amounts allowed to these accounts. People who cannot set aside the maximum amounts currently allowed would not be affected by measures to raise the maximums still higher.

Studies have found that only about 5 percent of people eligible for IRAs, and only about 5 percent of 401(k) participants, contribute the maximum amount now. These are the only people who would benefit from raising the contribution limits. This group consists almost entirely of high earners: according to CBO, only 1 percent of 401(k) participants who earn less than $40,000 contributed the maximum amount in 1997, but 40 percent of those earning over $160,000 did.

As for the proposed health-related retirement accounts, the value of the tax deductions they would provide would depend on the accountholder’s tax bracket. Most low- and middle-income families are in the zero, 10 percent, or 15 percent tax bracket during their working years and owe little or no taxes in old age. (Roughly two-thirds of all elderly persons owe no income tax or are in the 10 percent or 15 percent bracket.) Thus, the upfront deductions and tax-free withdrawals that these accounts offer would be worth relatively little to low- and middle-income families. High-income households in the top tax brackets, in contrast, could use the accounts as lucrative new tax shelters into which they could shift substantial sums from taxable investment accounts.

The proposals could weaken employer-sponsored pensions. Changing income or contribution limits on IRAs could weaken pension coverage by enabling small business owners and executives to set aside significant amounts of tax-advantaged savings for their own retirement without having to provide pension coverage for their workers.

Currently, business owners who want to put away more than $8,000 a year in tax-advantaged retirement savings for themselves and a spouse must offer a retirement plan that covers their workers as well as themselves. If the IRA contribution limits are raised significantly, owners would be able to put away substantially larger amounts without having to offer an employer plan. Pension and retirement analysts have widely warned this could cause some employers (particularly small business owners) to scale back or cancel their plans, and that more new small business owners would be likely to decide not to offer a pension in the first place.

The proposals would do little to spur new saving. High-income households, which would gain the most from these possible changes, are much more likely than other households already to save adequately for retirement. (Today, the 10 percent of households with the highest incomes hold more than half of the total assets in 401(k)s and IRAs.) Research indicates that high-income households would primarily respond to new tax breaks such as these by shifting existing savings from taxable to non-taxable accounts, not by increasing the total amount they save.

In fact, new retirement-related tax breaks would likely reduce the nation’s overall level of saving if they are not “paid for” on an ongoing basis. National saving is the sum of private saving and either public saving (government surpluses) or public dissaving (government deficits, which soak up private savings). If new tax breaks increase deficits by an amount that exceeds the amount of new private saving they generate, their net effect would be to reduce national saving.

This outcome would be especially likely if the new tax breaks, like those discussed here, are aimed primarily at high-income people, since a relatively small share of the additional funds these individuals would place in tax-advantaged accounts would represent new saving.

The proposals could more than compensate high-income families for the large cuts in traditional Social Security benefits that the President’s plan would impose on them, while doing relatively little to compensate middle-income families for the benefit cuts they would experience. Chairman Thomas and Social Security Subcommittee Chairman Jim McCrery have said that including new retirement-related tax cuts in Social Security legislation would enable them to compensate middle- and upper-income workers for the larger reductions in Social Security benefits these workers would face under proposals like the President’s. But the retirement-related tax cuts outlined here would primarily benefit those at the top of the income spectrum, while offering relatively few benefits to middle-income workers.

Consider, for example, a family earning average wages ($37,000) that retires in 2055. Under the President’s Social Security proposal, it would face an annual reduction of $4,522 (in today’s dollars) in Social Security benefits. Such a family would gain nothing from eliminating the IRA income limit or raising the IRA (or 401(k)) contribution limits, because it is already eligible for an IRA and, like most families, does not make enough to contribute the maximum amount currently allowed.

For a family earning $400,000, in contrast, such changes in IRA rules would produce handsome benefits. Eliminating the IRA income limit would make the family eligible for an IRA, into which it could put $5,000 annually. By the time the family retired, it would have an additional $250,000 just as a result of being eligible for the IRA tax breaks. (If the IRA contribution limit were raised as well, the family would be able to deposit more than $5,000 in its IRA each year and would receive more than $250,000 in tax-cut benefits in retirement from the IRA.) That $250,000 would be enough to buy a $17,000 annuity, which would more than make up for the family’s $13,085 annual reduction in traditional Social Security benefits under the President’s plan.

* * *

As noted, there are a range of proposals that could help low- and middle-income families save more for retirement, and some of these are also apparently being considered by Chairman Thomas. But policymakers should resist attempts to couple those sensible reforms with the types of costly and misguided proposals outlined here.

End Notes

[1] For a more thorough discussion of these issues, see Joel Friedman and Robert Greenstein, Boosting Income and Contribution Limits for Pension Savings Would Swell Deficits, Do Little for Middle-Class Families, Center on Budget and Policy Priorities, May 18, 2005.

Más de los autores