House-Passed Housing Tax Package Improves Significantly on Senate Version: But Addressing the Foreclosure Crisis Will Require Other Measures

On April 10, the Senate passed a bill comprised largely of housing-related tax cuts. [1] Six weeks later, the House passed its own housing legislation including its own package of housing-related tax measures.

Some of the provisions in House-passed housing tax package have merit, and the House-passed tax package represents a significant improvement over the Senate’s version. Unlike the Senate bill, the House package is revenue-neutral, and it omits both an ineffectual special-interest tax break and a seriously misguided provision that would limit the ability of local governments to raise revenue. The House package also includes a set of worthwhile reforms to the Low-Income Housing Tax Credit, as well as a provision (also included in the Senate bill) that would allow states to issue additional tax-exempt housing bonds and use the proceeds to refinance subprime mortgages to help some families remain in their homes. (For a detailed comparison of the House-passed and Senate tax packages, see the appendix table.)

Still, the tax package in the House-passed housing bill would, as a whole, do little to address the foreclosure crisis. Far more important in this respect are several non-tax measures now before Congress. These include provisions in the House-passed housing legislation and approved by the Senate Banking Committee that would facilitate restructuring of mortgages and thus help families struggling to keep their homes, as well as measures passed by both the House and the Senate to help communities especially hard hit by foreclosures.

Major Components of the House-passed Package

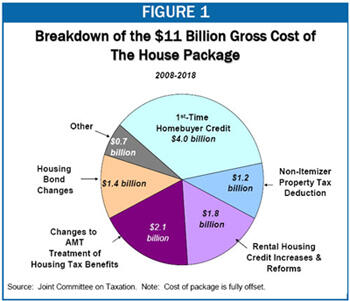

Figure 1 shows the breakdown of the cost of the House-passed tax package. The single largest provision is a tax credit that provides a $7,500 interest-free loan to first-time homebuyers who purchase homes within the next year. The combined cost of this provision and another tax break for homeowners — a non-itemizer property tax deduction that was also included in the Senate legislation — is $5 billion, or about 46 percent of the package’s total gross cost. As explained below, these two provisions are not a good use of scarce resources, which would be better spent on measures targeted to addressing the foreclosure crisis.

The next major elements of the House-passed package are a set of reforms to the Low-Income Housing Tax Credit (LIHTC), a temporary expansion of that credit, changes to rental housing bond rules, and a set of changes in the treatment of housing tax incentives (including the LIHTC) under the Alternative Minimum Tax (AMT). These provisions, which account for more than one-third of the package’s cost, should enhance the effectiveness of the LIHTC and tax-exempt housing bonds at promoting the construction and rehabilitation of affordable rental housing. The final major provision in the package, which accounts for another 12 percent of its cost, increases temporarily the value of tax-exempt housing bonds that states and localities can issue and allows the proceeds from these bonds to be used to refinance loans for families in danger of losing their homes due to adjustable rate sub-prime mortgages.[1] This provision (also included in the Senate tax package) would provide state and local governments with the means to help some low-income homeowners remain in their homes.

The cost of the package is fully offset by two revenue-raising provisions: a measure that requires securities’ brokers to report additional information to taxpayers and the Internal Revenue Service (IRS) and a measure that would delay an already-enacted corporate tax cut for one year. All of these provisions are discussed in more detail below.

End Notes

[1] The House-passed bill also includes various smaller provisions, such as changes to the rules governing Real Estate Investment Trusts (REITs); these other provisions together cost about $725 million over ten years.

Más de los autores

Areas of Expertise

Areas of Expertise