Congress Needs to Boost Disability Insurance Share of Payroll Tax by 2016

Traditional Step Would Avert Trust Fund Depletion, Benefit Cuts

Policymakers need to replenish the Social Security Disability Insurance (DI) trust fund by late 2016, but that necessity comes as no surprise and poses no crisis. Although the DI trust fund is legally separate from the much larger Old-Age and Survivors Insurance (OASI) trust fund, both are integral parts of Social Security. Traditionally, lawmakers have divided the total payroll tax between OASI and DI according to the programs’ respective needs. Workers’ paychecks simply show a deduction for “Social Security tax,” and few know — or have reason to care — how that amount is apportioned.

When lawmakers last redirected some payroll tax revenue from OASI to DI in 1994, they expected that step to keep DI solvent until 2016 given anticipated economic and demographic trends. Despite fluctuations in the meantime, current projections still anticipate depletion of the trust fund in 2016 as forecast.

DI’s anticipated trust fund depletion does not indicate that the program is out of control or that it is “bankrupt;” if the trust fund were depleted and policymakers took no action, the program could still pay about 80 percent of benefits. But cutting benefits by one-fifth for an extremely vulnerable group of severely disabled Americans is unacceptable.

DI’s finances should ideally be addressed in the context of legislation to restore overall Social Security solvency. But even if policymakers make progress toward a well-rounded solvency package before late 2016, which seems unlikely, any changes in DI benefits or eligibility would surely phase in gradually and hence do little to fully replenish the DI fund by 2016. Consequently, policymakers would still need to reallocate payroll tax revenues between the two programs. There is nothing novel or controversial in such a step, and failing to take it would be irresponsible.

Payroll Tax Reallocation Is Nothing New

The current Social Security tax is 6.2 percent of wages up to $117,000 in 2014, paid by both employers and employees. Of this total, 5.3 percent of covered wages goes to the OASI trust fund, and 0.9 percent goes to the DI trust fund. This allocation reflects the decision of policymakers in 1994, when they last reallocated taxes between the programs.

Congress has reallocated payroll tax revenues many times in the past — and in both directions. This is a traditional and historically noncontroversial step.

- Using a narrow definition of “reallocation” — one in which the total payroll tax rate remained the same but the split between OASI and DI changed — there have been six such instances (in 1970, 1980, 1983, 1994, 1997, and 2000). Three of those changes shifted funds from OASI to DI, and three shifted funds from DI to OASI.

- Using a broader definition — one in which the total tax rate changed and the OASI and DI rates changed in opposite directions (one increasing and the other decreasing) — there were an additional five instances (in 1968, 1978, 1979, 1982, and 1984). Three of these shifted funds from OASI to DI, and two from DI to OASI.

These 11 reallocations were enacted in six separate laws.[1] (See Appendix Table 1.)

As then-Congressman Jake Pickle stated in 1980 during consideration of legislation to reallocate payroll taxes between Social Security’s two programs, “[T]he bill we bring today is a deliberate step both to [ensure] the stability of the trust funds and to provide the Congress the time it will need to make any further changes necessary….Reallocation, the mechanism used in [H.R.] 7670, has been the traditional way of redistributing the [Old-Age, Survivors, and Disability Insurance, or OASDI] tax rates when there have been changes in the law and in the experience of programs and in order to keep all the programs on a more or less even reserve ratio.”[2]

1983 Social Security Reforms Imposed a Financial Loss on DI That 1994 Reallocation Only Partially Offset

The last major reform of Social Security occurred in 1983. At the time, DI was in relatively strong financial shape, while OASI faced insolvency within a few months.[3] The Social Security Amendments of 1983, while addressing the OASI shortfall, slightly raised DI’s cost and cut DI’s share of the payroll tax. That financial harm was only partly mitigated by the tax-rate reallocations enacted in 1994.

The 1983 amendments had many provisions intended chiefly to address the OASI shortfall — such as covering new federal employees, delaying cost-of-living adjustments, imposing income tax on a portion of Social Security benefits, accelerating a scheduled payroll tax increase, and so forth — but one of the most important was raising the full retirement age (FRA). The FRA climbed from 65 to 66 between 2000 and 2005 and will rise again from 66 to 67 between 2017 and 2022.

This change to the FRA worsened the DI trust fund. Disabled workers are reclassified as retired workers when they reach the FRA (without any change in their monthly benefit). Raising the FRA delayed this switch from disability to retirement benefits from age 65 to age 66 and ultimately to 67 and therefore increased DI’s costs even while lowering Social Security costs overall.

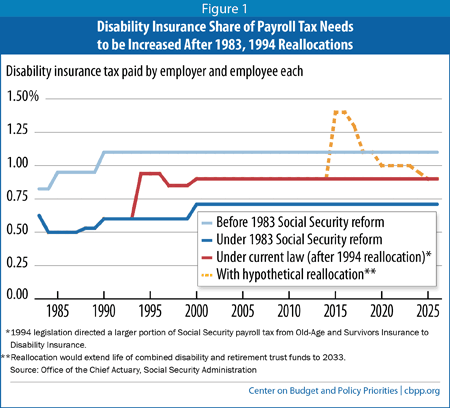

In addition, the 1983 amendments cut DI’s share of the payroll tax. Under the law in effect before the amendments, DI’s share of the payroll tax was 0.825 percent and was scheduled to rise to 1.1 percent by 1990. The 1983 law trimmed DI’s share to 0.5 percent in 1984 through 1987, with gradual increases in subsequent years, finally leveling off at 0.71 percent in 2000 and beyond. This reduction in the DI share allowed for a parallel increase in the OASI share to address its financial problems as the major reforms enacted in 1983 phased in.

Overall, according to the 1983 Trustees Report, the 1983 amendments reduced Social Security’s long-run deficit by 2.09 percent of taxable payroll — consisting of a 2.89 percent improvement in OASI and a 0.80 percent deterioration in DI.[4]

The drafters of the 1983 amendments did not deliberately underfund DI. They used the best information available to them at the time. If DI’s tax rate had been 1.1 percent for the last two decades, as it would have been without the 1983 amendments, we would not face the need to replenish the fund today.

After the 1994 reallocations, the trustees estimated that the DI fund would become depleted in 2016, OASI in 2031, and the combined funds in 2030. In the 2014 report, the trustees put those dates at 2016, 2034, and 2033.[7] Thus, despite the fluctuations over the past two decades, the projections made at the time of the last reallocation in 1994 have proven to be remarkably accurate, reinforcing the view that the DI shortfall is not a surprise or a reflection of a program that has somehow grown “out of control” in recent years. Indeed, most of the increase in DI spending is the result of demographic and other factors that are well understood.[8]

Reallocation Would Postpone DI Trust Fund Depletion to 2033

Under the assumptions of the 2014 Trustees Report, the actuaries estimate that raising DI’s share (currently 0.9 percentage point) of the 6.2 percent payroll tax by 0.5 percentage points in 2015 and 2016, 0.4 percentage points in 2017, and declining amounts through 2024 would equalize the actuarial status of the two trust funds — putting them both on track to become depleted in 2033 (instead of 2016 for DI and 2034 for OASI).[9] (See Figure 1.)

Since the disability and retirement programs are closely linked, it would be best to replenish the DI trust fund as part of a package that restores solvency to the Social Security program as a whole — that is, that extends the solvency of both trust funds well beyond 2033. That prospect seems highly unlikely to occur, however, between now and 2016.

In the absence of any changes, DI’s share of the payroll tax will be sufficient to cover only about 80 percent of the cost of current benefits starting in late 2016, according to the trustees. Without corrective action, DI benefits would thus have to be cut by about 20 percent across the board. Since benefits are modest (about $1,150 a month, on average) and beneficiaries have low incomes — one-fifth of DI beneficiaries live below the poverty level, and half have total family incomes below $30,000 a year[10] — Congress must not allow that to happen.

To prevent that, policymakers need to reallocate payroll tax revenues, modestly increasing DI’s share. Some reallocation will clearly be required, even if policymakers can agree on a comprehensive solvency plan for Social Security, because any cuts in DI benefits would doubtless be phased in over time and are likely to be relatively modest. Thus reallocation, a step that policymakers have taken many times in the past, will be an essential part of any solution to address DI’s financial problems in 2016.

End Notes

[1] For a full history of the relevant legislation, see the Social Security Administration’s collection at http://ssa.gov/history/legislativehistory.html, also summarized in Geoffrey Kollmann, Social Security: Summary of Major Changes in the Cash Benefits Program, May 18, 2000, http://www.socialsecurity.gov/history/reports/crsleghist2.html.

[2] Quoted in Geoffrey Kollmann and Carmen Solomon-Fears, Major Decisions in the House and Senate on Social Security: 1935-2000, Congressional Research Service Report RL30920, March 26, 2001, http://www.socialsecurity.gov/history/reports/crsleghist3.html.

[3] Kathy A. Ruffing, “Social Security: It’s Not 1983,” Center on Budget and Policy Priorities, Off the Charts blog, April 24, 2012, http://www.offthechartsblog.org/social-security-its-not-1983/.

[4] See Table 33 on page 4 in the 1983 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, http://www.ssa.gov/history/reports/trust/1983/1983c.pdf.

[5] Kathy A. Ruffing, Social Security Disability Insurance Is Vital to Workers With Severe Impairments, Center on Budget and Policy Priorities, August 9, 2012, https://www.cbpp.org/sites/default/files/atoms/files/8-9-12ss.pdf.

[6] For a comparison of scheduled tax rates and allocations before and after the 1983 Amendments, see Table A in John A. Svahn and Mary Ross, “Social Security Amendments of 1983: Legislative History and Summary of Provisions,” Social Security Bulletin, July 1983, http://www.ssa.gov/policy/docs/ssb/v46n7/v46n7p3.pdf. For the revised allocations after the 1994 act, see the 1995 Trustees Report, op. cit.

[7] See the 1995 and 2013 Trustees Reports, at http://www.ssa.gov/history/reports/trust/1995/triif.html and http://www.ssa.gov/OACT/TR/2013/tr2013.pdf, respectively.

[8] Kathy Ruffing, How Much of the Growth in Disability Insurance Stems from Demographic Changes? Center on Budget and Policy Priorities, January 27, 2014, https://www.cbpp.org/cms/index.cfm?fa=view&id=4080.

[9] Social Security Administration, Office of the Chief Actuary, “Potential Reallocation of the Payroll Tax Rate Between the Disability Insurance (DI) Program and the Old-Age and Survivors Insurance (OASI) Program – INFORMATION,” July 28, 2014, http://www.ssa.gov/OACT/solvency/NA_20140728.pdf.

[10] Average benefit from http://www.ssa.gov/OACT/ProgData/icp.html. Poverty rates and median family income from Michelle Stegman Bailey and Jeffrey Hemmeter, Characteristics of Noninstitutionalized DI and SSI Program Participants, 2010 Update, Social Security Administration, Office of Research, Evaluation, and Statistics, Note 2014-02, February 2014, http://www.ssa.gov/policy/docs/rsnotes/rsn2014-02.pdf. (CBPP multiplied the four-month income shown in SSA’s Table 3 by three to obtain an annual equivalent.)

Más de los autores

Areas of Expertise