Chained CPI Proposal Would Cut Social Security Retirement Benefits by About 2 Percent, on Average

The President’s new budget proposes to use the chained Consumer Price Index (CPI) for computing cost-of-living adjustments in Social Security and certain other federal benefits, as well as for indexing key parameters of the tax code.[1] The effect of this proposal on Social Security retirement benefits would vary by a person’s age and benefit level and would differ for current and future beneficiaries, but most future beneficiaries would experience a benefit reduction averaging about 2 percent over the course of their retirement. For most current beneficiaries and for low-income beneficiaries, the average reduction would be smaller.

- Future beneficiaries receiving an average benefit would experience a benefit reduction averaging 1 percent to 2 percent over the course of their retirement. The benefit reduction would average 1.1 percent if they draw benefits through age 71, 1.8 percent if they draw benefits through age 81 (which is more common), and 1.6 percent if they draw benefits through age 91.

- For future beneficiaries receiving smaller-than-average benefits, the reduction would be smaller, likely in the 0.5 percent to 1.5 percent range — except for beneficiaries poor enough to qualify also for Supplemental Security Income (SSI), who would be held harmless.

- For future beneficiaries receiving higher-than-average benefits, the reduction would be larger, averaging 2 percent or slightly more.

Current beneficiaries would suffer smaller losses than future beneficiaries at any given age. Current beneficiaries now 69 or older receiving an average benefit would receive lower benefits than under current law for the first ten years, but generally would receive higher benefits than under current law in years after that. After 15 years, the cumulative change in benefits for the average current beneficiary would be near zero. Current beneficiaries receiving smaller-than-average benefits would come out ahead if they lived more than ten or 15 years.

Proposal Includes Protections for Low-Income and Older Beneficiaries

The proposal includes features to mitigate its effects on low-income beneficiaries and older beneficiaries. It also exempts means-tested programs, notably SSI for very poor seniors and people with disabilities.[2]

Specifically, Social Security recipients would receive a special benefit increase — equal to 5 percent of the average retiree benefit, or about $750 a year — that phases in gradually between ages 76 and 85 (as well as a second 5 percent increase between ages 95 and 104). Disabled beneficiaries would receive the 5 percent increase after they had been on the rolls for 15 years — it would phase in between their 15th and 24th years of benefit receipt — and another such increase between their 34th and 43rd years, if they live that long.

The special benefit increase (or “bump”) would provide more help to seniors and people with disabilities who receive smaller-than-average Social Security benefits. All eligible retirees and disability beneficiaries would receive the same basic dollar increase, so those with smaller benefits would receive a larger percentage increase.

In addition, since the proposal calls for the chained CPI to take effect in 2015 and the 5-percent benefit adjustment to begin to take effect in 2020 (and to be phased in through 2029), people who are 69 or older today would begin to receive the 5-percent benefit increase after being subject to the chained CPI for only five years.

As noted, the proposal exempts SSI and other means-tested programs. Since Social Security benefit increases result in offsetting SSI benefit reductions and vice versa, each dollar in Social Security benefits that SSI recipients lose (or gain) from the switch to the chained CPI would be offset by a dollar increase (or reduction) in their SSI benefits. They would essentially be held harmless.

Impact Varies by Age and Benefit Level

Table 1 shows how the proposal would affect three illustrative future retirees: a low-wage retiree with benefits at the 20th percentile (that is, whose benefits exceed those of the bottom 20 percent of beneficiaries), a retiree who receives the average benefit, and a high-wage retiree who has always earned the maximum amount subject to the Social Security payroll tax, representing the top 2 percent of retirees.

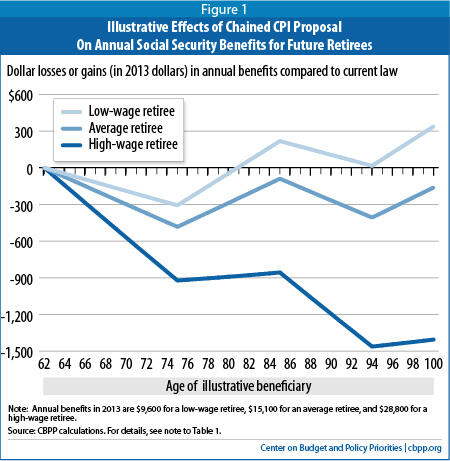

Then, between ages 76 and 85, the special 5-percent benefit increase would counteract the effect of the chained CPI. By age 85, the low-wage retiree’s benefit would be 2.3 percent higher than under current law; the average retiree’s benefit would be 0.6 percent lower than under current law, and the high-wage retiree’s benefit would be 3.0 percent lower. In the year the retirees reach 85, those impacts translate into a dollar gain of about $220 for the low-wage retiree and a dollar loss of about $90 and $860 for the medium- and high-wage retiree, respectively. (See Figure 1.)

From ages 86 to 94, the benefit reduction would grow again (or the benefit increase would shrink) for all three illustrative retirees. Retirees who lived to age 95 would begin to receive another special benefit increase at that point.

The average annual reduction in benefits for future retirees from ages 62 through 81 would range from 1.5 percent for the low-wage worker to 2.1 percent for the high-wage worker. Twenty years is roughly the life expectancy of a typical 62-year old.[4] Over ages 62 through 91, the average annual reduction would range from 0.5 percent to 2.5 percent, although only about one-fifth of retirees live that long.

Table 2 shows how the proposal would affect three illustrative current retirees who are now 69 years old and will turn 71 in 2015, when the proposal takes effect. As the table indicates, the losses for current retirees receiving average or below-average benefits would generally peak at 1.2 percent, while current retirees who receive lower benefits and live into their 80s would generally experience a small increase in benefits.

Impact Would Be Smaller Than Raising the Retirement Age

By way of comparison, a one-year increase in Social Security’s “full retirement age” — now 66 and scheduled to rise to 67 — is equivalent to a roughly 7 percent across-the-board cut in benefits,regardless of whether a worker files for Social Security before, upon, or after reaching the full retirement age.[5] Many people mistakenly assume that an individual who works to age 67 or 70 would not incur any benefit reduction if the full retirement age were raised. In fact, the benefit reductions for all retirees that would result from an increase in the retirement age would be substantially larger than the benefit reductions under the chained CPI proposal.

| Table 1 Illustrative Effects of Chained CPI Proposal On Social Security Retirement Benefits for Future Retirees | |||

| Low-Wage Retiree | Average Retiree | High-Wage Retiree | |

| Age | Change in annual benefit | ||

| 62 | 0 | 0 | 0 |

| 63 | -0.3% | -0.3% | -0.3% |

| 64 | -0.5% | -0.5% | -0.5% |

| 65 | -0.7% | -0.7% | -0.7% |

| 70 | -2.0% | -2.0% | -2.0% |

| 75 | -3.2% | -3.2% | -3.2% |

| 80 | -0.5% | -1.9% | -3.1% |

| 85 | 2.3% | -0.6% | -3.0% |

| 90 | 1.1% | -1.8% | -4.1% |

| 95 | 0.7% | -2.4% | -5.0% |

| 100 | 3.5% | -1.1% | -4.9% |

| Age | Change in average benefit | ||

| 62-71 | -1.1% | -1.1% | -1.1% |

| 62-81 | -1.5% | -1.8% | -2.1% |

| 62-91 | -0.5% | -1.6% | -2.5% |

| Note: Annual benefits in 2013 are $9,600 for a low-wage retiree, $15,100 for an average retiree, and $28,800 for a high-wage retiree. These figures are based on the distribution of benefits in December 2012, available at http://www.ssa.gov/OACT/ProgData/benefits/ra_mbc201212.html. | |||

| Table 2 Illustrative Effects of Chained CPI Proposal on Social Security Retirement Benefits For Current Retirees, Age 71 in 2015 | |||

| Low-Wage Retiree | Average Retiree | High-Wage Retiree | |

| Age | Change in annual benefit | ||

| 71 | -0.3% | -0.3% | -0.3% |

| 72 | -0.5% | -0.5% | -0.5% |

| 73 | -0.7% | -0.7% | -0.7% |

| 74 | -1.0% | -1.0% | -1.0% |

| 75 | -1.2% | -1.2% | -1.2% |

| 76 | -0.7% | -1.0% | -1.2% |

| 77 | -0.2% | -0.7% | -1.2% |

| 78 | 0.4% | -0.5% | -1.2% |

| 79 | 0.9% | -0.2% | -1.2% |

| 80 | 1.5% | 0.0% | -1.2% |

| 85 | 4.2% | 1.3% | -1.1% |

| 90 | 3.0% | 0.1% | -2.3% |

| 95 | 2.6% | -0.6% | -3.2% |

| Age | Change in average benefit | ||

| 71-75 | -0.7% | -0.7% | -0.7% |

| 71-80 | -0.2% | -0.6% | -1.0% |

| 71-85 | 0.9% | -0.1% | -1.0% |

| 71-90 | 1.5% | 0.0% | -1.2% |

| Note: Annual benefits in 2013 are $9,600 for a low-wage retiree, $15,100 for an average retiree, and $28,800 for a high-wage retiree. | |||

End Notes

[1] Robert Greenstein, Commentary: The Debate Over the Chained CPI, Center on Budget and Policy Priorities, April 9, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=3950.

[2] Office of Management and Budget, Chained CPI Protections, April 10, 2013, http://www.whitehouse.gov/omb/budget/factsheet/chained-cpi-protections.

[3] Jeffrey Kling, Using the Chained CPI to Index Social Security, Other Federal Programs, and the Tax Code for Inflation, Testimony before the Subcommittee on Social Security, Committee on Ways and Means, April 18, 2013, http://www.cbo.gov/sites/default/files/cbofiles/attachments/44083_ChainedCPI.pdf. The Office of the Chief Actuary at the Social Security Administration assumes a slightly larger gap, 0.3 percentage points a year, as does an analysis of the chained CPI proposal by the National Women’s Law Center. Joan Entmacher, Katherine Gallagher Robbins, and Abby Lane, “Obama Plan Fails to Adequately Protect Long-Term Social Security Beneficiaries from Chained CPI,” April 2013, http://www.nwlc.org/sites/default/files/pdfs/chainedcpipresidentobamabumpup.pdf.

[4] Social Security Administration, Annual Statistical Supplement to the Social Security Bulletin, 2012, Table 4.C6, http://www.ssa.gov/policy/docs/statcomps/supplement/2012/4c.html#table4.c6.

[5] Kathy Ruffing and Paul N. Van de Water, Social Security Benefits Are Modest, Center on Budget and Policy Priorities, January 11, 2011, https://www.cbpp.org/cms/index.cfm?fa=view&id=3368#textBox.

Más de los autores

Areas of Expertise