Myths and Realities About the Alternative Minimum Tax

The Alternative Minimum Tax was created in 1969 to ensure that the highest-income households could not exploit loopholes, exclusions, and deductions to avoid paying any federal income tax. The AMT acts as a stop-gap tax system, with taxpayers owing their regular income tax or AMT liability, whichever is higher.

Because the AMT parameters were never indexed for inflation, and because the 2001 and 2003 tax cuts substantially lowered taxpayers’ liability under the regular income tax without changing the structure of the AMT, the tax will affect a rapidly increasing number of taxpayers in future years in the unlikely event that no changes are made. As a result, there is considerable anxiety surrounding the AMT, and some in Congress are eager to do away with it altogether. Repealing the AMT, however, would cost at least $800 billion over the next decade (2008-2017), and as much as $1.5 trillion, depending on whether the 2001 and 2003 tax cuts are extended (according to estimates by the Urban Institute-Brookings Institution Tax Policy Center). Repeal of the AMT would cost more than repeal of the estate tax.

Public discussion of issues surrounding the AMT suffers from several misconceptions, which seem to be widespread among policymakers and many media outlets.

Myth 1: The AMT is (or is rapidly becoming) a “middle-class” tax.

“What started out as a misguided attempt to tax the ‘rich’ has become a significant added tax burden on millions of middle-income Americans.” — Senator Jon Kyl, May 23, 2005

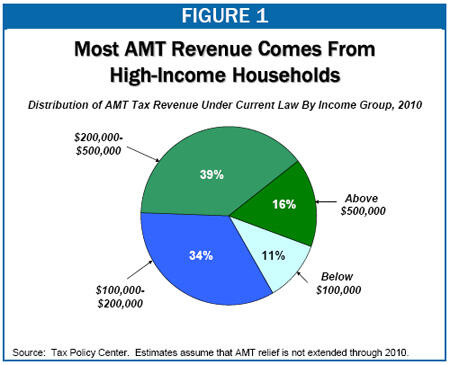

Reality: The bulk of AMT revenue continues to come from high-income households.

The Urban Institute-Brookings Institution Tax Policy Center estimates that, under current law (that is, in the unlikely event that Congress takes no action to restrict the AMT’s reach and the AMT grows to affect tens of millions of additional taxpayers), more than half of AMT revenue in 2010 still will come from households with incomes over $200,000 (the highest income 4 percent of all households). About 90 percent of AMT revenue will come from households with incomes above $100,000 (the highest-income 16 percent of all households). (See Figure 1.)

It’s true that, over time, an increasing percentage of AMT taxpayers will be middle- and upper-middle income households. But these households will pay considerably less in AMT taxes, on average, than higher income households. In 2010, households with incomes between $50,000 and $100,000 that are on the AMT will pay an average of about $1,000 in AMT taxes, according to the Tax Policy Center estimates, if no AMT relief is provided and the AMT is allowed to swell. AMT taxpayers with incomes between $100,000 and $200,000 will pay an average of about $2,500, while AMT taxpayers with incomes above $200,000 will pay an average of more than $11,000. For this reason, households with incomes below $200,000 will comprise a majority of AMT taxpayers but will be the source of less than half of all AMT revenue.

Knowing who pays the AMT is necessary to understanding who would benefit from repealing it. Because households with annual incomes above $200,000 are the source of more than half of all AMT revenue, more than half of the benefits of repeal would go to these high-income households.

Furthermore, even assuming Congress does not repeal the AMT, it will almost certainly act to prevent the tax from affecting growing numbers of middle-income households. To date, Congress has provided relief from the AMT in the form of temporary increases in the AMT exemption. If this relief is extended, nearly all AMT revenue in 2010 will come from households with incomes above $200,000. Thus, nearly all of the benefits of going beyond the current AMT “patch” and repealing the AMT would go to these very high-income households.

Myth 2: The growth in the AMT was unanticipated and accidental, and so the cost of repeal should not have to be offset.

“It’s ridiculous to rely on revenue that was never supposed to be collected in the first place. Another trap is raising taxes to ‘pay’ for AMT repeal. It’s unfair to raise taxes to repeal something with serious unintended consequences like the AMT.” — Senator Charles Grassley, January 4, 2007

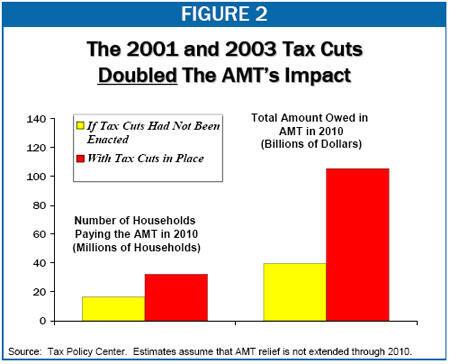

Reality: Lawmakers put off reform of the AMT so as to use the AMT to mask (and defer) the true costs of the 2001 and 2003 tax cuts. More than half of the current AMT problem is due to the effects of the 2001 and 2003 tax cuts, which pushed millions more taxpayers onto the AMT and more than doubled the amount of tax owed under the AMT in the absence of AMT relief.

The Tax Policy Center estimates that, if the 2001 and 2003 tax cuts had not been enacted, 16 million taxpayers would pay a total of about $43 billion in AMT in 2010, in the absence of AMT relief (see Figure 2). With the 2001 and 2003 tax cuts in place, a total of 32 million taxpayers will pay a total of more than $100 billion in AMT in 2010, if AMT relief is not provided.[1]

These effects should come as no surprise to supporters of the 2001 and 2003 tax cuts, who used the AMT to mask the true cost of those tax cuts. In the spring of 2001, when Congressional leaders were formulating their large tax-cut package, they faced a major obstacle. The Congressional Budget Resolution allowed for tax-cut legislation costing up to $1.35 trillion over ten years. The combined cost of all tax cuts on the Administration and the Congressional leadership’s agenda, however, was far higher than that. Former Representative Bill Thomas, then Chairman of the House Ways and Means Committee, described the “problem” as a need to get “a pound and a half of sugar into a one-pound bag.”[2]

The Congressional leadership accomplished this goal by employing three major gimmicks, all designed to conceal the true long-run cost of their tax package. First, they phased in some of their tax cuts (for example, repeal of the estate tax) over time so that the full costs of these provisions did not show up until the end of the ten-year budget window. Second, they sunsetted all of the tax cuts at the end of 2010, significantly reducing their cost in fiscal year 2011 (the last year of the budget window)[3]. Finally, they used the AMT to dramatically reduce the tax cuts’ official cost.

As explained above, taxpayers owe the Alternative Minimum Tax whenever their tax liability as calculated under the AMT is higher than their tax liability as calculated under the regular income tax. Therefore, substantially reducing households’ tax liability under the regular income tax without changing what they owe under the AMT inevitably increases the number of households that owe the AMT, as well as the amount of revenue the AMT collects. Essentially, if large tax cuts and changes in the AMT are not enacted together, the AMT will take back some (or all) of the tax cuts that households receive under the regular income tax, as households will end up paying tax based on their tax liabilities under the AMT rather than under regular income tax law.[4]

This point is well understood by tax experts, and it was brought to the attention of members of Congress in the spring of 2001, when the Joint Committee on Taxation provided lawmakers with estimates of how the tax cuts then under consideration would impact the AMT. These estimates showed that the new tax cuts would double the number of AMT taxpayers by 2010.[5]

Policymakers could have chosen to act on the information the Joint Tax Committee provided, reforming the AMT so that it did not affect rapidly increasing numbers of households and so that households would receive the full value of whatever new tax cuts were enacted. But, because the Congressional Budget Resolution set a limit for the total cost of the 2001 tax cut, providing a meaningful AMT fix would have required scaling back other tax cuts under consideration (such as the large reductions in the top marginal income-tax rates).

Instead, Congress chose to enact a vastly cheaper ($14 billion) three-year AMT “patch” (a temporary increase in the exemption level) in order to maximize the size of the other tax cuts. The patch was enough to make sure that the number of AMT taxpayers did not immediately explode and that most people received the full value of their 2001 tax cuts — but only through 2004.

Had Congress then actually allowed the AMT patch to expire at the end of 2004, the AMT would have taken back a substantial fraction of the 2001 tax cuts in subsequent years. The official cost estimates for the 2001 tax cuts assumed that this would occur, and so they omitted the cost of the portion of the tax cuts that would be taken back by the AMT. As a result, the tax cuts appeared much cheaper than they otherwise would have.

In reality, however, Congress did not allow the AMT patch to expire, but extended it through the end of 2006 (at a cost of about $80 billion). The Congressional Budget Office now estimates that continuing the policy of “patching” the AMT would have an annual cost of about $70 billion by 2010. More than sixty percent of that cost simply represents the deferred cost of the enacted 2001 and 2003 tax cuts.

Myth 3: The only way to protect middle-class households from the AMT is to repeal it.

“[The AMT] is a monster that really cannot be improved. It cannot be made to work right. It is time to draw the curtain on this monster.” — Senate Finance Committee Chair Max Baucus, January 4, 2007

Reality: The AMT can be reformed — and in a revenue-neutral manner — so as to fully protect middle-class households from the tax.

As noted above, repealing the AMT would cost about $800 billion between 2008 and 2017, if all of the 2001 and 2003 tax cuts were allowed to expire, and $1.5 trillion, if all of these tax cuts were extended (according to estimates by the Tax Policy Center). Over the long run, the revenue losses from AMT repeal dwarf even the cost of estate-tax repeal, another very expensive tax cut that many in Congress have rejected as unaffordable.[6]

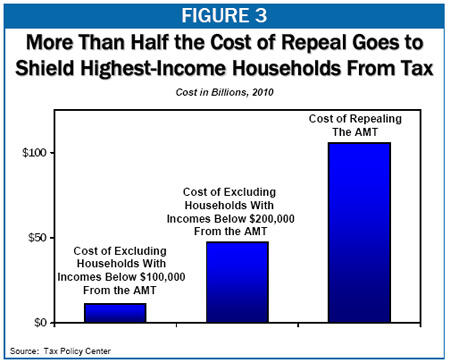

Fortunately, various tax experts have suggested reform alternatives that would protect all or nearly all middle- and upper-middle class households from paying the AMT, while preserving the revenue from the tax. More than half of the cost of repealing the AMT would, as described above, go for tax cuts for households with incomes above $200,000 (see Figure 3). Thus, a fix that better targets relief toward middle-income households would be considerably less expensive than repeal, and its costs could be offset through any number of possible measures.

For example, one approach to AMT reform would be to extend the current AMT “patch” (the temporary higher AMT exemption level that expired at the end of 2006) and index it for inflation. This reform would be better targeted than repeal toward middle-income taxpayers, although at least a fourth of the cost over the next few years still would go to provide tax cuts for households with incomes above $200,000.

Another option would be to simply exempt all households with incomes below a given level (e.g. $200,000) from the AMT. Under such an approach, by definition, no household with income below the chosen level would pay the AMT, and the benefits would be targeted to those with incomes below that level.

Either of these approaches would be substantially less costly than repeal, though still expensive. CBO estimates that continuing the current patch through 2017 would cost $569 billion between 2008 and 2017 if the 2001 and 2003 tax cuts are allowed to expire and more than $1 trillion if these tax cuts are extended. The cost of an AMT exclusion for households with incomes below a certain level could be less (depending on the income level chosen), but would still be quite high.

Paying for AMT Reform

The House of Representatives recently voted to reinstate the “Pay-As-You-Go” (PAYGO) budgeting rule, and Democratic leaders have promised that the Senate will follow suit. Under PAYGO, the cost of legislation that increases entitlement spending or reduces revenues must be paid for. Hence, PAYGO would require that the cost of any AMT fix be offset (unless the PAYGO rules were waived).

The Tax Policy Center recently published a menu of options for paying for AMT changes.[7] Some of these options would raise revenue by directly reforming the AMT. For instance, one possible offset would involve eliminating the reduced rates for capital gains and dividend income under the AMT. Currently, capital gains and dividends are taxed at lower rates than other income under the AMT, as they are under the regular income tax. Simply applying the same AMT tax rates that are levied on wage and salary income (rates that are well below the top tax rates under the regular income tax) to capital gains and dividends would raise considerable revenue, which could be used to pay for removing middle-income households from the AMT. Taxing capital gains and dividends at the same rates as other income under the AMT would also retarget the AMT toward high-income households, as these households receive far more of their income in the form of capital gains and dividends than do low- or middle-income households. (Currently, the very highest income households, those with incomes over $1 million, are less likely to owe AMT than are households with incomes between $200,000 and $1 million.)

In addition, this reform likely would make the AMT more effective in combating tax shelters, its original purpose. Many tax shelters involve reclassifying income as capital gains to take advantage of the lower capital gains tax rate. If capital gains income were taxed at the same rates as ordinary income under the AMT, the AMT would take back some of the benefits of these tax shelters and thus serve its purpose as a “stop-gap” for the regular income tax.[8]

Another option is to pay for AMT reform with a modest increase in the regular income tax rates levied on the highest-income taxpayers. Such an increase would raise taxes only on those who have benefited the most from the income-tax cuts enacted in recent years.

Given the range of available options and the grave long-term budget problems the nation faces, it would be fiscally irresponsible to provide a costly windfall to high-income taxpayers in the form of AMT repeal. Rather, if policymakers wish to address the AMT issue, they should enact an AMT reform plan that effectively targets relief to middle-class taxpayers and fully pays for the change in a progressive manner.

End Notes

[1] Even with AMT relief in place, the tax cuts significantly increase the number of households affected by the AMT. In 2012, the Tax Policy Center estimates that about 6 million households will owe the AMT if AMT relief is continued and the 2001 and 2003 tax cuts are extended. In contrast, fewer than 3 million households will owe the AMT if AMT relief is continued but the 2001 and 2003 tax cuts are allowed to expire.

[2] Representative William Thomas, “News Conference with Representative Bill Thomas, Chairman of the House Ways and Means Committee,” Federal News Service Transcript, March 15, 2001.

[3] For the 2001 tax-cut legislation to qualify as a reconciliation bill — which is not subject to filibuster in the Senate and thus can be passed with 51 votes instead of 60 votes — the tax cuts had to expire before the end of 2011. (Senate rules prohibit provisions in reconciliation bills that would increase the deficit outside of the budget window, which in 2001 was 2001-2011.) The sponsors of the legislation chose to sunset the tax cuts in 2010 rather than 2011 in order to squeeze more tax breaks into the bill and still stay within the budget resolution limit.

[4] Consider the following hypothetical example. Suppose a household initially owes $15,000 under the regular income tax and that this household receives a $5,000 tax cut (under the regular income tax), after which it owes only $10,000. Suppose that this household’s liability under the AMT is $13,000. Then, without the tax cut, the household would not owe AMT, since its regular income tax liability ($15,000) would be higher than its AMT liability ($13,000). With the tax cut reducing its regular income tax liability, the household’s AMT liability exceeds its regular income tax liability ($10,000) by $3,000. As a result, the household owes $3,000 in AMT; the AMT effectively takes back $3,000 of its $5,000 tax cut.

[5] Joint Committee on Taxation, “Estimated Revenue Effects of a Chairman’s Mark of the ‘Restoring Earnings to Lift Individuals and Empower Families (Relief) Act of 2001,’” JCX-41-01, May 11, 2001, page 8.

[6] See Aviva Aron-Dine, “Revenue Losses From Repeal of the Alternative Minimum Tax Are Staggering,” Center on Budget and Policy Priorities, revised February 1, 2007.

[7]Leonard E. Burman, William G. Gale, Gregory Leiserson, and Jeffrey Rohaly, “Options to Fix the AMT,” Tax Policy Center, January 19, 2007, http://www.taxpolicycenter.org/UploadedPDF/411408_fix_AMT.pdf.

[8] This option is discussed in the Tax Policy Center study, and has also been analyzed and advocated by Citizens for Tax Justice. See “A Progressive Solution to the AMT Problem,” Citizens for Tax Justice, December 2006, http://www.ctj.org/pdf/amtsolution.pdf.

Más de los autores