más allá de los números

Obscure Provision Tilts Senate Tax Bill Even More to Corporations

Under an obscure “trigger” provision, the Senate Finance Committee tax bill tilts its tax cuts even more to the nation’s wealthiest corporations at the expense of hard-working families: if federal revenues hit certain levels after nine years, businesses would get another $79 billion in tax cuts in 2027. That’s before a single dollar would go to protecting low- and moderate-income households from the tax increases they face under the bill.

As we’ve explained, even without this provision the bill clearly prioritizes corporate tax cuts over low- and middle-income people: it makes its deep corporate tax cuts permanent, including a much lower tax rate for multinationals’ foreign profits, but lets all its individual income tax cut provisions expire at the end of 2025. And to pay for those permanent corporate tax cuts, it would raise taxes on middle-class households and those with even lower incomes and would cause 13 million more people to go uninsured.

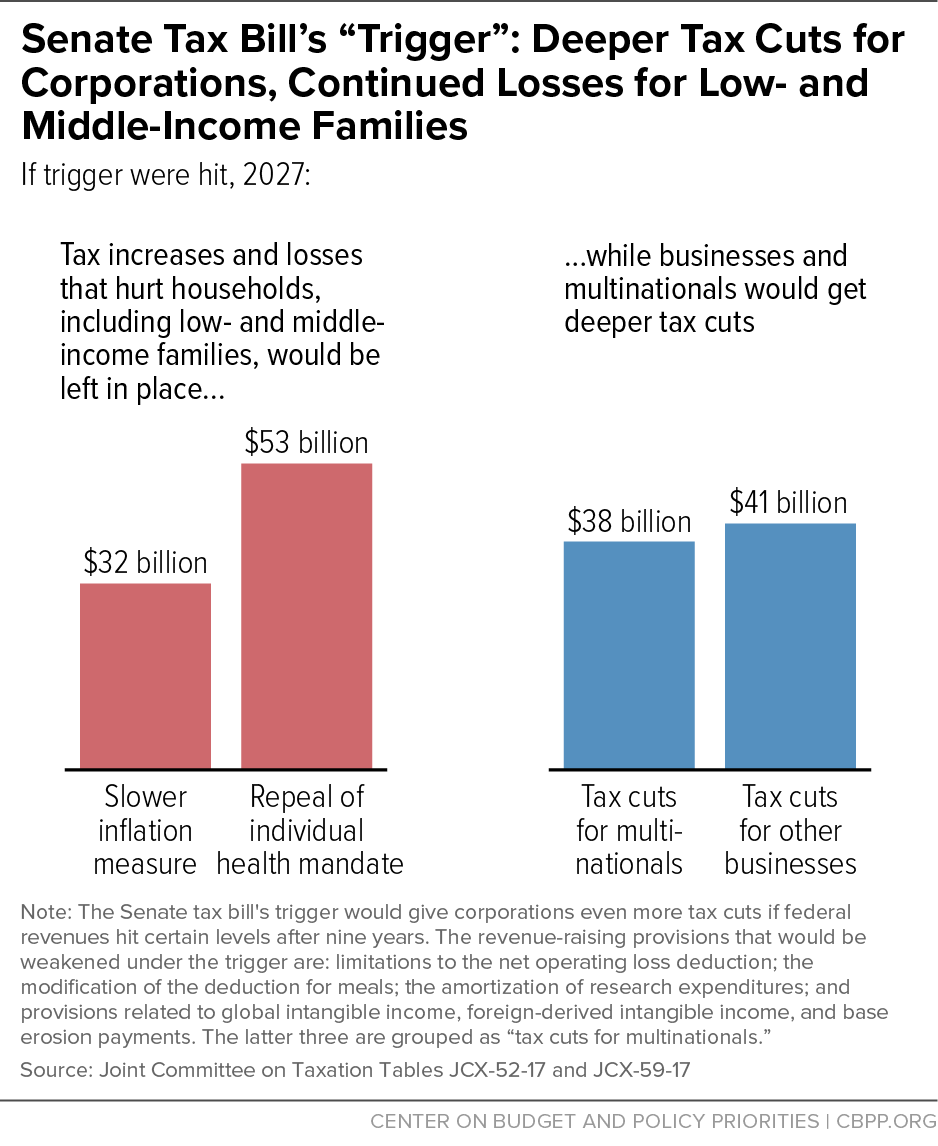

Under the trigger, if revenues meet specified levels after nine years, certain revenue raisers in the bill will automatically expire — retroactively for 2026 and then going forward. That would give businesses even larger tax cuts than they’d already receive under the bill: $45 billion more for 2026 and $79 billion more for 2027. Although Republicans argue that their trigger is fiscally responsible, the fact remains that it can only make things worse, relative to the Joint Committee on Taxation estimate that the bill already adds about $1.4 trillion to deficits over ten years. The bill, by the way, includes no provision to trigger tax increases in case revenues fall short of specified targets.

Of the trigger’s additional corporate tax cuts, $18 billion of them for 2026 and $38 billion for 2027 would go to multinationals by rolling back the bill’s already weak provisions to prevent them from shifting more profits offshore. The bill provides a huge, permanent incentive for corporations to shift profits and even investments offshore by setting a far lower effective tax rate on their foreign, as opposed to domestic, profits. It tries to contain the tax avoidance and offshoring of profits and investment that this lower tax rate would generate by (among other things) setting a minimum tax on certain foreign profits from intellectual property and other intangibles. But that minimum tax, of 12.5 percent, is well below the bill’s 20 percent statutory rate on domestic profits. And while the bill schedules the rate to rise to a somewhat more adequate 16 percent after 2025, it would stay at 12.5 percent if the trigger is activated.

Another way of viewing this is that lawmakers are signaling to multinationals that many of the scheduled revenue-raising provisions that those companies will face in the bill are gimmicks to limit the bill’s apparent cost, but that lawmakers hope won’t take effect.

Meanwhile, all individual taxpayers who would face tax increases from another permanent feature of this bill — a slower inflation measure (the chained Consumer Price Index) for adjusting tax brackets and certain tax provisions each year to account for inflation — would get no such automatic protection from those tax increases. Nor would the millions of households that would face higher premiums and other harm due to the repeal of the Affordable Care Act’s individual mandate that most people get health coverage or pay a penalty.

The $79 billion in added tax cuts that corporations would get in 2027 from the trigger is nearly as much as low- and middle-income families would lose that year due to the bill’s tax increases and repeal of the mandate. And the $38 billion of additional corporate tax cuts from rolling back provisions designed to stop multinational tax avoidance would more than cover the bill’s tax increases through the slower measure of inflation. (See chart.)

The trigger has many other problems as well, as New York University Professor David Kamin explains. For example, as a budget process measure, it should not be permitted in a “reconciliation” bill that can pass the Senate with a majority vote (rather than the 60 votes that most legislation requires). And, even if it were permitted, it might well make the bill add to deficits beyond the first decade, violating another of the Senate’s rules for reconciliation. But the trigger’s biggest problem is that it simply reinforces the bill’s basic architecture: prioritizing tax cuts for corporations above all else.