más allá de los números

By Expanding Wealth Taxes, States Can Expand Opportunity

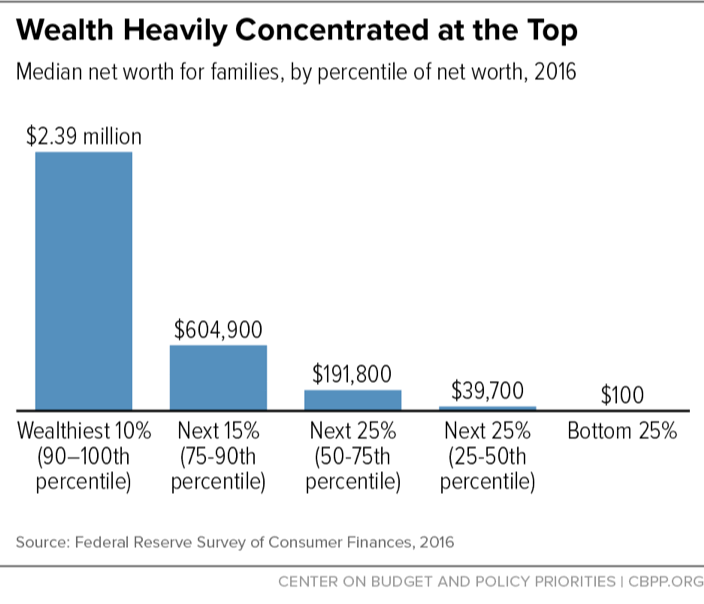

The nation’s wealth is concentrated in the hands of a few (see graphic), and state tax systems have contributed to that concentration as wealthy individuals and corporations used their power to shape state tax policies to benefit themselves. But better state tax policies could help build a more broadly shared prosperity.

The top 1 percent of households own roughly 40 percent of the wealth, while the bottom 90 percent own just 21 percent. This top-heavy structure reduces opportunity for millions of families — particularly Blacks, Latinos, and other families of color, who face great barriers to building wealth due to the legacy of historical racism and the ongoing damage from racial bias and discrimination.

State and local governments depend mainly on income, sales, and property taxes. Low- and middle-income taxpayers pay a larger share of their income in sales and property taxes than wealthier taxpayers. The opposite is generally true for state income taxes, but state taxes in total are “upside-down” in the vast majority of states, meaning they ask the most of taxpayers who can least afford it.

As states seek to improve their tax systems, they should pay special attention to taxing the assets of the very wealthy — such as stocks and bonds, real estate, and personal possessions like boats, jewelry, cars, and artwork. Loopholes and special tax benefits shield many of these assets from federal, state, and local taxes. For example:

- The federal estate tax now reaches just a few extremely wealthy estates — fewer than 1 in 1,000. And state estate taxes are increasingly rare.

- Homes are the one form of wealth that’s routinely taxed, but residential property taxes fall more heavily on low- and moderate-income households because they are typically set at a flat rate and because property owners who rent out apartments can pass on their property taxes to renters. What’s more, the assessment caps and other property tax limits that some localities have adopted often benefit wealthy homeowners disproportionately.

- Intangible property like stocks and bonds, which comprise a large share of the assets of the wealthy, isn’t taxed until the owner sells it. And the capital gains generated by its rise in value are taxed at lower rates than wages and salaries.

Eliminating these tax advantages would shift some of the responsibility for funding critical public services and investments like schools, roads, and health care from low- and moderate-income taxpayers to those best able to pay.

Reducing today’s extreme concentration of wealth is also critical to expanding equality of opportunity. Families with substantial savings and other wealth can give their children much better educational opportunities, a safety net to enable them to take risks on job opportunities that may not pay off, and loans to help them buy homes in better neighborhoods that will, in turn, give their children a head start.

Moreover, while fairness would dictate taxing income from inheritances at higher rates than income from work — since heirs don’t have to give up leisure time or work more to receive that income — inheritances are generally taxed at a much lower rate or not at all. One reason is the so-called “stepped-up basis” rule, under which people who inherit assets such as stocks, bonds, or real estate pay no taxes on any appreciation of their value that occurred before they inherited them.

Closing these holes in the tax system — such as by eliminating stepped-up basis, increasing property tax rates for high-end houses, or strengthening state estate taxes — would raise revenues for investments that help the state as a whole, such as education and health care. The added revenue could also support income supplements like state Earned Income Tax Credits to help families struggling to make ends meet as well as offset some of the concentration of wealth.

For more information on ways states can tax wealth see these CBPP issue briefs: