Trump Budget Continues Multi-Year Assault on IRS Funding Despite Mnuchin’s Call for More Resources

The Internal Revenue Service (IRS) budget has been cut by 18 percent since 2010, after adjusting for inflation, and the agency has lost roughly 13,000 employees — around 14 percent of its workforce. These cuts have harmed customer service, frustrated honest taxpayers, and undermined critical enforcement efforts to combat tax avoidance and growing identity theft. Treasury Secretary Steven Mnuchin, whose department includes the IRS, appears to understand that these cuts are misguided, stating at his confirmation hearing:

I am concerned about the staffing of the IRS. It is an important part of fixing the tax gap and I am very concerned about the lack of first-rate technology at the IRS, the issue of making sure that we protect the American public’s privacy when they give information to the IRS, cybersecurity around that, and also customer service for the many hard-working Americans that are paying taxes.[1]

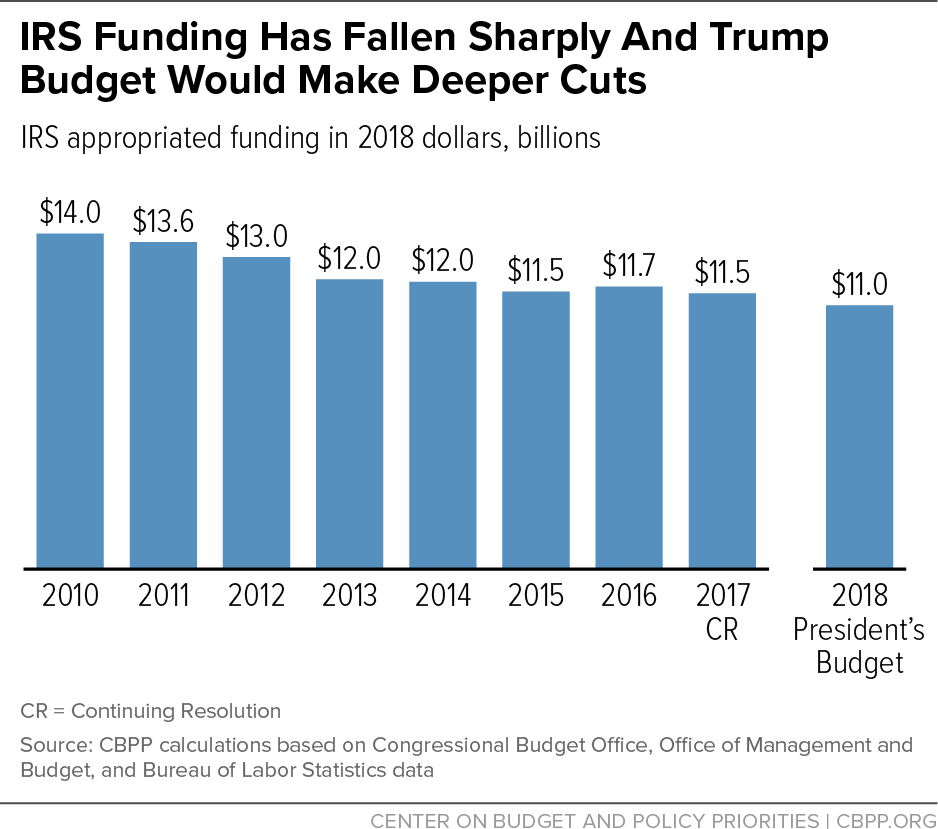

The IRS needs additional resources to address the issues that Mnuchin outlined; providing those resources would both improve taxpayer services and increase revenues by improving tax compliance. Despite this, the Administration’s 2018 budget proposal cuts IRS funding by an additional $239 million,[2] bringing the total decline since 2010 (after adjusting for inflation) to 21 percent. [3] (See Figure 1.)

An under-resourced IRS would be poorly positioned to enforce the new statutes and regulations that would accompany a tax overhaul.Failing to adequately fund the IRS would be particularly ill-timed, as President Trump and congressional Republicans intend to propose a broad revamp of the tax code that could create new opportunities for tax avoidance — and an even greater need for IRS resources to ensure compliance. In particular, GOP tax plans call for preferential treatment of pass-through business income that would invite massive tax avoidance by wealthy taxpayers, costing hundreds of billions of dollars over the next decade, according to the Tax Policy Center (TPC).[4] An under-resourced IRS would be poorly positioned to enforce the new statutes and regulations that would accompany a tax overhaul. The combination of increased avoidance opportunities and weakened IRS enforcement capacity would further reduce revenues and undermine the integrity of the tax system.

The IRS performs a basic and essential function of government: collecting the revenue to fund our military and key domestic investments, including public safety, education, and health research, and programs that provide needed support to retirees, seniors, people with disabilities, and low-income households. An underfunded IRS poses a threat not only to IRS’s effectiveness, but to the public’s trust that the tax laws will be enforced fairly. Policymakers should provide the resources the IRS needs to do its job effectively.

IRS Funding Has Been Cut Deeply

The IRS has been targeted for sharp funding cuts since 2010. Its current budget of $11.2 billion is 18 percent below the 2010 level, after adjusting for inflation.[5] As most IRS funding goes to staffing, the cuts have forced the IRS to dramatically reduce its workforce; the agency lost roughly 13,000 employees — around 14 percent of its workforce — between 2010 and 2016.[6]

These damaging cuts have weakened the agency’s ability to perform its core functions of collecting taxes and enforcing the nation’s tax laws. As seven former IRS commissioners from both Republican and Democratic administrations have written: “Over the last fifty years, none of us has ever witnessed anything like what has happened to the IRS appropriations over the last five years and the impact these appropriations reductions are having on our tax system.”[7]

Cuts in staff and other resources have affected taxpayer services, cybersecurity, and enforcement.[8] Taxpayer services have remained at subpar levels across this period, despite an improvement in 2016 after Congress modestly boosted taxpayer services funding. Even with this improvement, only 53 percent of calls from taxpayers were answered in fiscal year 2016 (down from 74 percent in 2010) and callers waited almost 18 minutes on average for an answer (up from 11 minutes in 2010).[9] Funding cuts have also caused the IRS to delay much-needed upgrades to its information technology systems, compromising the security of taxpayer data and weakening its ability to identify and assist victims of identity theft. As IRS Commissioner John Koskinen stated, “We’re falling behind in upgrading hardware infrastructure and software. This compromises the stability and reliability of our information systems, and leaves us open to more system failures and potential security breaches.”[10]

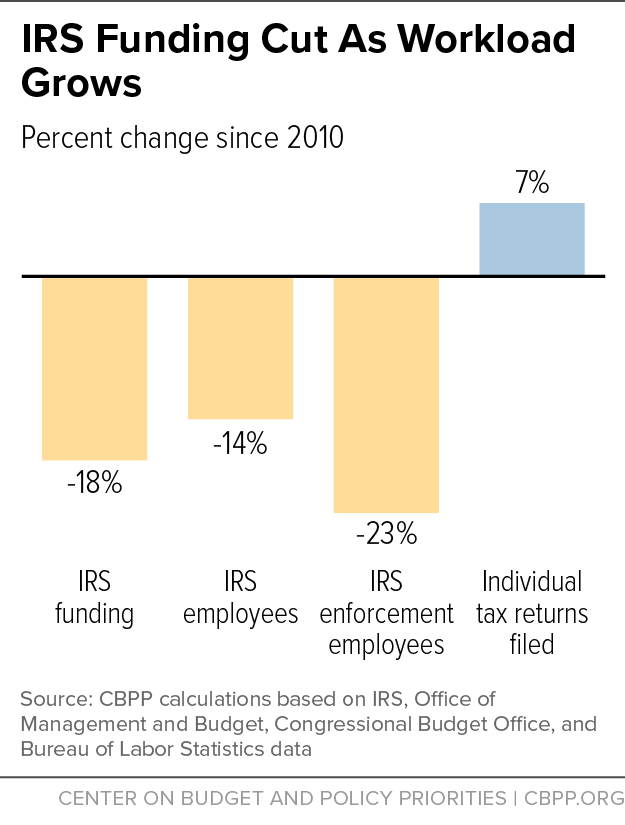

These cuts have occurred even as IRS responsibilities have grown. (See Figure 2.) The IRS processed 10 million (7 percent) more individual returns in 2016 than in 2010.[11] It also has dedicated increased resources to adapt to continually evolving cybersecurity threats, as its systems are under increasingly sophisticated attack from hackers attempting to steal taxpayer information and fraudsters filing returns using stolen identities. In 2016 alone, IRS systems identified 969,000 fraudulent tax returns, preventing more than $6.5 billion in fraudulent refunds from being released.[12] Tax legislation enacted in recent years also requires significant IRS resources to administer. For example, the Foreign Account Tax Compliance Act requires the IRS to collect and analyze new data from financial institutions across more than 100 countries to reduce illegal tax evasion.

In short, funding cuts to date have significantly the weakened the agency’s ability to fulfill its duties, and additional cuts would only compound these issues. As National Taxpayer Advocate Nina Olson stated in her most recent report to Congress: “Simply put, the IRS cannot function well in the 21st century with the budget it has today,” and “It cannot become a 21st century tax administration without adequate support from Congress.”[13]

Enforcement Serves Vital Function But Has Been Hit Especially Hard

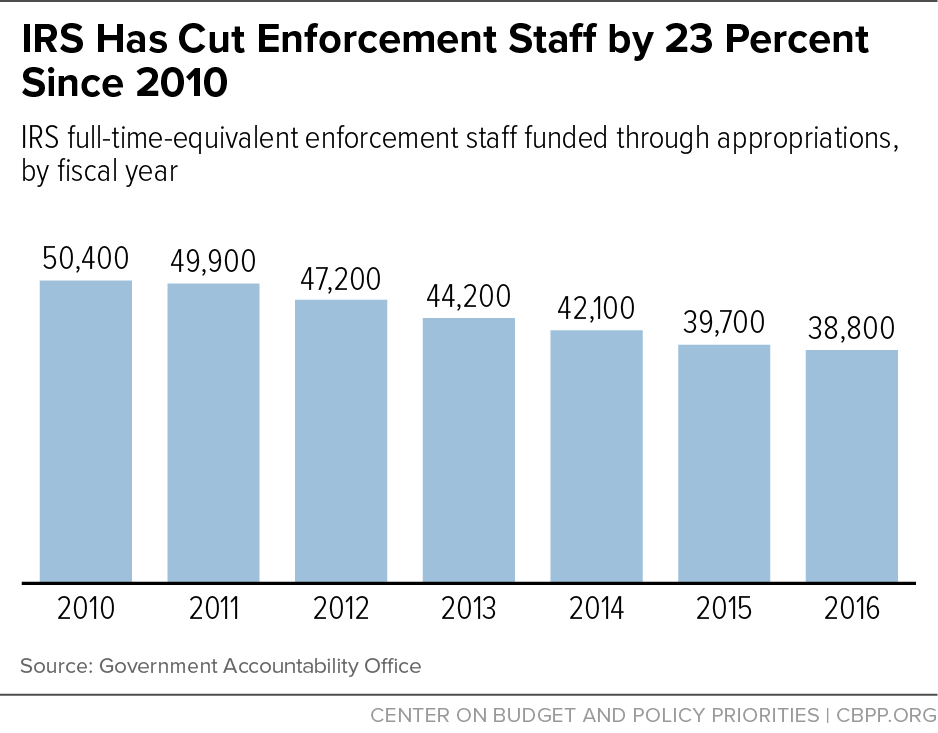

IRS enforcement activities maintain the integrity of the nation’s tax system. The IRS collects more than 90 percent of federal revenues, largely through taxpayers’ voluntary compliance, but enforcement activities such as audits play a critical role by and ensuring that taxpayers pay the taxes they owe.[14] Unfortunately, IRS enforcement funding has been hit disproportionately hard by funding and staffing reductions since 2010. In 2016, enforcement funding was 20 percent below its 2010 level in inflation-adjusted terms. As a result, enforcement alone has lost more than 11,000 employees — almost a quarter of its staff — since 2010.[15] (See Figure 3.)

Secretary Mnuchin highlighted the need for additional enforcement resources during his confirmation hearing, noting “I am concerned about the staffing of the IRS. That is an important part of the fixing the tax gap” and that “[if] we add people, we make money.”[16] Indeed, the IRS estimates that the net tax gap — the amount of taxes owed but uncollected even after enforcement activities — is roughly $400 billion annually.[17] Treasury estimates that every additional $1 invested in enforcement can produce $6 in additional revenue, and the additional, indirect savings from deterring tax evasion are more than three times that.[18] By cutting enforcement “the government is losing billions of dollars to achieve budget savings of a few hundred million dollars,” according to Commissioner Koskinen.[19]

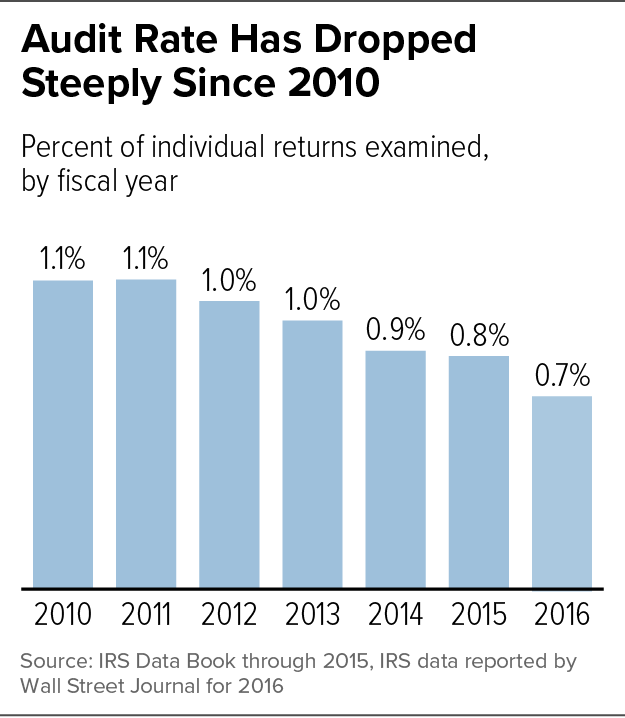

The decline in enforcement has reduced the IRS’s ability to go after tax cheats. The IRS audited just 1 of every 140 individual returns in 2016, down from 1 of 90 returns in 2010.[20] (See Figure 4.) Among high-income taxpayers, whom the IRS has designated as an enforcement priority due to their more complex finances and greater risk of noncompliance, audit rates have also fallen steeply.[21] The audit rate for returns with incomes over $1 million fell from its recent peak of 12.5 percent in 2011 to 5.8 percent in 2016.[22]

The enforcement cuts have also put pressure on the IRS’s Criminal Investigations (CI) division, which plays a crucial role in enforcement by investigating potentially criminal tax code violations including identity theft, tax evasion, money laundering, and terrorist financing. In a recent press conference, CI division Chief Richard Weber noted that CI “is down hundreds and hundreds of special agents,” even though “there are certainly enough cases for us to work, if we had the resources.”[23] As a result, its capacity to investigate and prosecute criminal activity has been limited significantly, and the CI unit initiated 28 percent fewer investigations in 2016 than it did in 2010.[24]

Adequate IRS Resources Especially Important If Major Tax Changes Enacted

Fundamental changes to the tax system are high on Republicans’ legislative agenda. Their proposals are expected to be similar to plans put forward last year by House Republicans and President Trump during the campaign, which would dramatically alter the individual and business tax systems.[25] A revamped tax code would have major implications for IRS resources. IRS staff would need to become familiar with the new tax system in order to interpret and enforce tax laws and counsel taxpayers. Changes to information technology systems would likely be needed to reflect new policies. And tax legislation often requires the IRS to lead extensive rulemaking processes to develop and finalize new regulations. Each of these responsibilities could strain IRS resources in any funding environment, let alone one in which IRS funding is being cut.

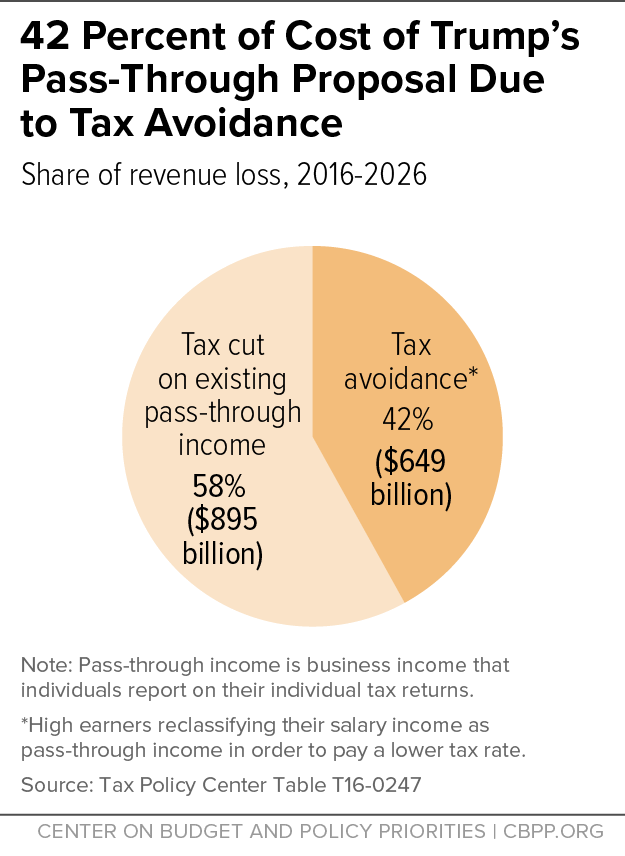

Moreover, several proposals that Republicans are considering would create new tax avoidance opportunities, making an adequately resourced IRS even more essential. For example, both the House GOP and Trump tax plans include a special, lower tax rate on pass-through business income — that is, income that “passes through” to business owners and is taxed at the owners’ individual tax rates rather than at the corporate income tax rate. This provision, which would primarily benefit very high-wealth individuals who receive the bulk of pass-through income, would also spur large-scale tax avoidance by expanding the incentive for high-income professionals to classify their wage and salary income as business income to receive the lower tax rate.[26] Indeed, TPC concluded that under the Trump pass-through proposal, such tax avoidance maneuvers by high-income households would account for more than 40 percent of the provision’s $1.5 trillion ten-year cost.[27] (See Figure 5.)

IRS rulemaking and enforcement would be crucial to averting even more abuse. For instance, the House GOP plan asserts that its lower pass-through rate would only apply to “active” pass-through income, requiring owners and investors to meet rules about how involved they are in managing the business. But the line between “active” and “passive” business income is difficult to determine, and the House GOP plan does not describe how it would prevent abuse. Thus, it could fall on the IRS to craft rules distinguishing between them and to prevent abuse through enforcement.

Other changes to the tax system could also create new opportunities for tax avoidance. The House GOP tax plan would change the corporate income tax to a “destination-based” cash flow tax, the first of its kind in the world.[28] Switching to the new system would create a number of complex tax administration issues, both predictable — such as how to tax intellectual property and financial services firms — and unforeseen.[29] In addition, both the Trump and House GOP plans would eliminate the estate tax on inherited wealth.[30] Depending on the details, eliminating the estate tax could facilitate tax avoidance across generations and undermine aspects of the income tax system.

Conclusion

The Trump Administration’s proposed funding cuts to the already under-resourced IRS should be cause for concern. Such cuts have the potential to undermine the integrity of the tax system, particularly following years of cuts that have compromised enforcement and other crucial IRS functions. The potential for major changes to the tax system this year makes it even more important for policymakers to give the IRS sufficient resources to fulfill its mission.

End Notes

[1] C-SPAN, “Treasury Secretary Confirmation Hearing,” January 19, 2017, https://www.c-span.org/video/?421858-1/treasury-secretary-nominee-steven-mnuchin-testifies-confirmation-hearing.

[2] Office of Management and Budget, “America First: A Budget Blueprint to Make America Great Again,” March 16, 2017, https://www.whitehouse.gov/sites/whitehouse.gov/files/omb/budget/fy2018/2018_blueprint.pdf.

[3] These additional cuts are part of a $54 billion proposed reduction in overall funding for non-defense discretionary programs, which is already set to decline to record lows under current law. See David Reich and Chloe Cho, “Will Congress Ease the Continuing Pressure on Non-Defense Discretionary Programs or Worsen It?” Center on Budget and Policy Priorities, March 13, 2017, https://www.cbpp.org/research/federal-budget/will-congress-ease-the-continuing-pressure-on-non-defense-discretionary.

[4] Chuck Marr et al., “Will New Trump Tax Plan Include Pass-Through Tax Break for Wealthiest?,” Center on Budget and Policy Priorities, February 27, 2017, https://www.cbpp.org/research/federal-tax/will-new-trump-tax-plan-include-pass-through-tax-break-for-wealthiest.

[5] In fiscal year 2016, IRS funding was $11.2 billion, 16 percent below its 2010 level after adjusting for inflation. The IRS is currently funded through April 28, 2017 with a continuing resolution that extends its 2016 funding level into 2017 with a small across-the-board cut. If that funding level were continued through the entirety of 2017, IRS funding would be 18 percent below its 2010 level after adjusting for inflation.

[6] Government Accountability Office, “Internal Revenue Service: Observations on IRS’s Operations, Planning, and Resources,” February 27, 2015, http://www.gao.gov/assets/670/668769.pdf, p. 35; Government Accountability Office, “Internal Revenue Service: Preliminary Observations on the Fiscal Year 2017 Budget Request and 2016 Filing Season Performance,” March 8, 2016, http://www.gao.gov/assets/680/675668.pdf, p. 9.

[7] Former IRS Commissioners Mortimer M. Caplan, Sheldon S. Cohen, Lawrence B. Gibbs, Fred T. Goldberg, Jr., Shirley D. Peterson, Margaret M. Richardson, and Charles O. Rossotti, “Letter to the Honorable Thad Cochran, the Honorable Barbara A. Mikulski, the Honorable Harold Rogers, and the Honorable Nita M. Lowey: IRS Appropriations for Fiscal Year 2016,” November 9, 2015, http://taxprof.typepad.com/files/former-irs-commissioners-letter-on-agency-budget.pdf.

[8] For further details on the impact of IRS funding cuts, see Chuck Marr and Cecile Murray, “IRS Funding Cuts Compromise Service and Weaken Enforcement,” Center on Budget and Policy Priorities, updated April 4, 2016, https://www.cbpp.org/research/federal-tax/irs-funding-cuts-compromise-taxpayer-service-and-weaken-enforcement.

[9] Government Accountability Office, “2015 Tax Filing Season: Deteriorating Taxpayer Service Underscores Need for a Comprehensive Strategy and Process Efficiencies,” December 16, 2015, https://www.gao.gov/products/GAO-16-151 and National Taxpayer Advocate, “Annual Report to Congress 2016: Executive Summary,” Internal Revenue Service, 2017, https://taxpayeradvocate.irs.gov/2016AnnualReport.

[10] John Koskinen, “Koskinen Discusses Challenges Facing IRS, Tax Industry,” Tax Notes, October 31, 2014.

[11] Internal Revenue Service, “2017 and Prior Year Filing Season Statistics,” https://www.irs.gov/uac/2017-and-prior-year-filing-season-statistics.

[12] John Koskinen, “Koskinen Discusses Challenges Facing IRS,” Tax Notes, July 12, 2016 and John Darlymple, “Written Testimony of John M. Darlymple, Deputy Commissioner for Services and Enforcement, Internal Revenue Service, Before the House Oversight and Government Reform Committee, Subcommittee on Government Operations and Subcommittee on Health Care, Benefits, and Administrative Rules, On IRS Taxpayer Service,” March 8, 2017, https://oversight.house.gov/wp-content/uploads/2017/03/Dalrymple_IRS_Testimony.pdf.

[13] National Taxpayer Advocate.

[14] Internal Revenue Service, “Budget-In-Brief FY 2017,” https://www.irs.gov/PUP/newsroom/IRS%20FY%202017%20BIB.pdf.

[15] Government Accountability Office, February 7, 2015; Government Accountability Office, March 8, 2016.

[16] C-SPAN.

[17] Tax Policy Center, “What is the Tax Gap?,” http://www.taxpolicycenter.org/briefing-book/what-tax-gap.

[18] “The Budget of the United States Government, Fiscal Year 2017,” Department of the Treasury, p. 1051, https://obamawhitehouse.archives.gov/sites/default/files/omb/budget/fy2017/assets/tre.pdf.

[19] John Koskinen, “Koskinen Discusses Challenges Facing IRS, Tax Industry,” Tax Notes, October 31, 2014.

[20] Richard Rubin, “IRS Audits of Individuals Drop for Fifth Straight Year,” Wall Street Journal, February 22, 2017, https://www.wsj.com/articles/irs-audits-of-individuals-drop-for-5th-straight-year-1487794717 and Internal Revenue Service, “2010 Data Book,” https://www.irs.gov/pub/irs-soi/10databk.pdf.

[21] IRS defines high-income returns as those with total positive income (TPI) over $200,000. Among returns with TPI over $1 million that it audited in 2014, IRS identified over $2,000 in additional tax liability per audit hour. Among the highest-income returns audited — those with TPI over $5 million — IRS identified more than $4,500 in additional liability per audit hour. Treasury Inspector General for Tax Administration, “Improvements Are Needed in Resource Allocation and Management Controls for Audits of High-Income Taxpayers,” September 18, 2015, https://www.treasury.gov/tigta/auditreports/2015reports/201530078fr.pdf.

[22] Rubin.

[23] Luca Gattoni-Celli, “IRS CI Chief Hopes Mnuchin Will Help Fill Workforce Gaps,” Tax Notes, February 28, 2017.

[24] Internal Revenue Service, “Enforcement Statistics,” https://www.irs.gov/uac/enforcement-statistics-criminal-investigation-ci-enforcement-strategy.

[25] The House Republican plan would also restructure the IRS, but that part of the proposal is not included in this analysis.

[26] As TPC’s analysis of the Trump tax plan noted, “Establishing a top rate on pass-through business income that is 10 percentage points below the top rate on wages would create a very strong incentive for wage earners to become independent contractors, who would be taxed at the preferential pass-through business rates. Congress could impose strict rules in an attempt to limit such changes in worker status, but the boundary is quite difficult to enforce under current law and would be even harder to police if the Trump proposal were enacted.” James R. Nunns et al., “Analysis of Donald Trump’s Tax Plan,” Tax Policy Center, December 22, 2015, http://www.taxpolicycenter.org/publications/analysis-donald-trumps-tax-plan/full.

[27] Marr et al.

[28] Many countries have destination-based value-added tax systems that use a “credit-invoice” system, but the House GOP plan would implement the border adjustment by altering the corporate income/profits calculation in the corporate income tax, which is unprecedented.

[29] As TPC Director Mark Mazur stated, “when you do a tax change this large you have to be very, very concerned about unintended consequences and opening up different dimensions of behavior and tax planning that may not be an issue in the current system.” Jonathan Curry, “Conversations: Mark Mazur,” Tax Notes, February 9, 2017.

[30] Chye-Ching Huang and Chloe Cho, “Ten Facts You Should Know About the Federal Estate Tax,” Center on Budget and Policy Priorities, September 8, 2016, https://www.cbpp.org/research/federal-tax/ten-facts-you-should-know-about-the-federal-estate-tax.