Tax Holiday for Overseas Corporate Profits Would Increase Deficits, Fail to Boost the Economy, and Ultimately Shift More Investment and Jobs Overseas

Update, June 19, 2014: This paper has been updated.

Momentum is growing in Congress behind legislation to enact another “repatriation tax holiday” that allows multinational corporations to bring profits held overseas back to the United States and pay tax on them at a rate of only about 5 percent (rather than the normal tax rate on corporate profits). But the economic or fiscal case for doing so remains poor.

In recent days, several congressional Democrats have expressed support for some version of the legislation. [1] The momentum comes in the midst of a major lobbying campaign for it by a coalition of large and powerful U.S.-based multinational corporations.[2] Proponents argue that a second temporary repatriation holiday would boost domestic investment and jobs, which is the same pitch that proponents used to sell policymakers on a similar repatriation holiday in 2004 – and one with obvious resonance as the economy struggles to recover from recession and unemployment remains very high.

Nevertheless, the evidence shows that the first holiday failed to produce the promised results. Its primary effect was to provide a huge windfall to the shareholders of a small number of very large corporations.

Moreover, a new tax holiday would increase budget deficits by tens of billions of dollars over the coming decade. And unlike the 2004 repatriation holiday, which was sold as a “one-time-only” event, a second holiday would send a powerful message to corporations to shift investment and jobs overseas and hold the profits there — until yet another tax holiday is declared. Indeed, enactment of another such tax holiday would further embed the shifting of investment, jobs, and profits overseas as a major tax avoidance strategy for many U.S. multinational corporations.

- A tax holiday enacted in 2004 failed to produce the promised economic benefits. The evidence shows that firms mostly used the repatriated earnings not to invest in U.S. jobs or growth but for purposes that Congress sought to prohibit, such as repurchasing their own stock and paying bigger dividends to their shareholders. Moreover, many firms actually laid off large numbers of U.S. workers even as they reaped multi-billion-dollar benefits from the tax holiday and passed them on to shareholders.

- Repeating the tax holiday would increase incentives to shift income overseas. If Congress enacts a second tax holiday, rational corporate executives will conclude that more tax holidays are likely in the future. That will make corporations more inclined to shift income into tax havens and less likely to make investments in the United States. That’s why Congress, in enacting the 2004 tax holiday, explicitly warned that it should be a one-time-only event and should not be repeated.

- The claim that a tax holiday would increase domestic investment by freeing multinationals from cash restraints is extremely dubious. U.S. non-financial corporations currently have $1.9 trillion in cash and other liquid assets, the highest level as a share of total corporate assets since 1959. The ten companies lobbying hardest for a new tax holiday alone have at least $47 billion in cash and other liquid assets that could be used for domestic investments — without triggering additional tax liability.

- Some of the biggest beneficiaries of a tax holiday would be firms that have aggressively shifted income overseas. Companies in the technology and pharmaceutical industries have been particularly aggressive in shifting income abroad because they rely on intellectual property, which is relatively easy to shift to other countries as a tax avoidance strategy. Half of all repatriations from the 2004 tax holiday came from companies in these two sectors alone. The same corporations and sectors would stand to benefit disproportionately — and enormously — from a second tax holiday.

What Is a Dividend Repatriation Tax Holiday?

Although U.S.-based corporations with foreign subsidiaries are taxed on their worldwide profits, they generally pay no U.S. corporate taxes on their foreign income until it is “repatriated,” or sent back to the parent corporation from abroad. This effectively allows such firms to defer payment of the U.S. corporate income tax on their overseas profits indefinitely, even though they may obtain an immediate tax deduction for many expenses incurred in supporting the same overseas investments. This can produce a negative U.S. corporate income tax — that is, a net government subsidy — for overseas operations.

In addition to causing the federal government to lose tax revenue, this structure gives multinationals a significant incentive to shift economic activity — as well as their reported profits — overseas.

In 2004, as part of the American Jobs Creation Act (AJCA), Congress enacted a one-time “dividend repatriation tax holiday” that allowed firms to bring overseas profits back to the United States at a dramatically reduced tax rate. Normally, corporations pay the difference between the U.S. corporate rate of 35 percent and the rate at which overseas profits have been taxed by the foreign country. (To avoid double taxation, U.S. companies also receive a tax credit for all taxes they have paid to foreign countries.) The 2004 tax holiday allowed corporations to repatriate foreign-earned income at an effective rate of just 3.7 percent.[3]

As a result of the holiday, multinational corporations were able largely to avoid paying U.S. corporate income tax on foreign earnings they had accumulated and held overseas.

Proposals to repeat the 2004 holiday at the same extremely low tax rate, or at an even lower rate, are now emerging. One proposal, from Rep. Brian Bilbray of California, would essentially reduce the tax rate on repatriated earnings to zero.[4]

2004 Tax Holiday Failed to Generate Promised Economic Benefits

In calling for the 2004 tax holiday, lobbyists for large multinational corporations framed the proposal as an economic stimulus measure, contending that the repatriated profits would be invested in corporate expansions in the United States and thereby produce a large increase in capital spending, a boost to economic growth, and a large number of new jobs. The American Job Creation Act, which authorized the tax holiday, stated that its intention was to “encourage the investment of foreign earnings within the United States for productive business investments and job creation.” [5]

These promises were not borne out. As researchers at the National Bureau for Economic Research, the Congressional Research Service, the Treasury Department , and outside analysts have reported, there is no evidence the holiday had any of these positive effects. To the contrary, there is strong evidence that the repatriated earnings were used primarily to benefit corporate owners and shareholders, and that the restrictions Congress imposed on the use of the repatriated earnings to ensure they were invested in the United States were ineffective.

To qualify for the 2004 tax holiday, corporations had to draft and follow a “dividend reinvestment plan” that provided for the reinvestment of the repatriated cash in an approved use. Permitted investments included hiring and training U.S.-based workers, investing in infrastructure in the United States, research and development, and marketing in the United States. The legislation, followed by subsequent IRS guidance, sought to bar firms from spending earnings repatriated under the holiday on executive compensation, shareholder dividends, and stock buy-backs.

The tax holiday was successful at inducing large multinational corporations to repatriate their earnings at the lower rate: $362 billion in earnings were repatriated under the holiday, of which $312 billion qualified for the tax break, according to the IRS. [6] But studies have shown that firms overwhelmingly used these earnings not for productive new investments or jobs, but for the very purposes Congress had sought to prohibit:

- A comprehensive study published by the National Bureau of Economic Research (NBER) found that the repatriation holiday “did not increase domestic investment, employment, or [research and development].”[7] Multinationals that repatriated higher levels of earnings under the holiday did not increase their domestic investments (or any other approved uses of the funds) to a larger degree than multinationals that repatriated lower levels of earnings. Other studies yielded similar results. One found that “firms enjoying disproportionately larger gains under the act were no more likely to spend repatriated funds on growth-generating activities than other firms.” [8]

- A study by professors at the Wharton School of Business and the University of Oregon concluded that even though the 2004 law specifically prohibited the use of repatriated earnings for share repurchases, firms used a significant share of repatriated earnings for exactly that purpose. [9] They found that, “in spite of having plans to invest in approved activities, repatriating firms significantly increase[d] payments to shareholders, and that the amount of this increase is related to the amount of repatriation.” Similarly, the NBER study found that a dollar increase in repatriations “was associated with an increase of almost $1 in payouts to shareholders.” That is, most of the repatriated profits were paid out as windfalls to shareholders.

- After examining the various studies that have been conducted, the Congressional Research Service reported that the “studies generally conclude that the reduction in the tax rate on repatriated earnings…did not increase domestic investment or employment.” [10]

Analysts also specifically examined the behavior of corporations that were part of the 2003-2004 lobbying campaign, which explicitly promised that firms would use the funds to create jobs and scale up domestic investment. The NBER researchers found that even firms that had lobbied for the tax holiday failed to use the funds as they had said they would (and as the law technically required, but as explained below, in ways that were easily circumvented). Using membership in a lobbying coalition and campaign contribution activity to select the corporations to examine, the researchers found that “no matter which of the measures of lobbying is utilized, repatriations in response to the holiday by firms that lobbied for the [repatriation tax holiday] did not significantly increase investment in the United States.” [11]

The failure of the 2004 tax holiday to deliver the promised results should not have come as a surprise: economists and observers from across the political spectrum had predicted it would prove ineffective as economic stimulus.

- The Bush Administration opposed the tax holiday, citing analysis by the President's Council of Economic Advisers showing that it not only was unsound tax policy and unfair to the majority of U.S. companies but also “would not produce any substantial economic benefits.” [12]

- Similarly, before the holiday took place, a J. P. Morgan Chase survey found that most firms intended to use their repatriated funds for repurchasing stock or paying dividends.[13]

- And an Urban Institute-Brookings Institution Tax Policy Center brief explained that firms would be able to comply with the law’s stipulations without investing more in the United States than they otherwise would have: “Firms have substantial flexibility in how they finance new projects. By rearranging their financing sources, they will be able to meet the requirement of the law without changing their underlying investment decisions.”[14]

In the months following enactment of the tax holiday, press accounts indicated that many firms laid off workers even as they reaped large benefits from the tax holiday and passed them on to shareholders. The New York Times reported in 2004 that one of the most prominent proponents of the original holiday, Hewlett-Packard, “has announced a repatriation of $14.5 billion, layoffs of 14,500 workers, and stock buybacks of more than $4 billion for the first half of 2005 – about three times the size of its buybacks in the period a year earlier.” [15] Other companies that took advantage of the holiday but laid off American workers shortly thereafter included:

- Pfizer, which repatriated around $37 billion (the largest amount of any firm) shortly before eliminating around 10,000 American jobs and closing U.S. factories in 2005;[16]

- Ford Motor Company, which repatriated around $850 million under the holiday and then laid off more than 30,000 U.S. workers in 2005 and 2006; [17]

- Merck, which repatriated $15.9 billion and announced layoffs of 7,000 workers in 2005;

- Honeywell International, which repatriated $2.7 billion and laid off 2,000 workers in 2005 and 2006.

These lay-offs cannot be attributed to a weak economy. They came at a time when the U.S. economy was growing significantly and adding jobs. As the Treasury Department has noted, many of the largest beneficiaries of the tax holiday cut jobs in 2006 despite overall economy-wide job growth — and used the repatriated funds instead to repurchase stock and pay dividends.[18]

This evidence shows how even carefully constructed conditions written into the law to limit how firms may use repatriated profits are unlikely to have much effect on how the funds are spent. Economists often describe money as being “fungible,” meaning that dollars are interchangeable so there is rarely a practical way to enforce restrictions on how funds may be used. Despite clear and strict limitations on how firms were supposed to use repatriated cash, the profits they brought home under the ACJA were used to pay for already budgeted expenses, which in turn enabled corporations to free up other money for restricted activities including stock buybacks and distributions to shareholders.

In sum, there is no evidence that the holiday led either to increased hiring or to an increase in the investments as Congress had sought. The evidence suggests that the tax holiday conferred windfall gains on a small number of large multinational corporations — many of which were simultaneously eliminating thousands of U.S. jobs — and on the corporations’ shareholders.

That the tax holiday failed the first time is a compelling reason not to repeat this experiment. As explained below, however, it is far from the only reason not to march down this path again.

A Second Repatriation Holiday Would Be An Even Larger Policy Mistake

Currently, firms that shift income to foreign tax havens generally understand that, while they will be able to defer tax as long as they leave their profits abroad, they will generally have to pay U.S. corporate income taxes when the profits are repatriated. This knowledge acts as a restraint (albeit a weak one) on decisions to shift investments overseas primarily for tax reasons. If Congress enacts another tax holiday, however, rational corporate executives will almost certainly conclude that more tax holidays are likely in the future and will adjust investment and tax decisions accordingly. Corporations will move more investment and jobs overseas and book more profits overseas, and then keep the profits there while they wait for another tax holiday in which the vast bulk of these profits will be exempt from tax.

In other words, the expectation of future tax holidays will make firms more inclined to shift income into tax havens and less likely to reinvest earnings in the United States — precisely the opposite of what the measure is promoted by lobbyists as accomplishing. Temporary holidays on repatriated earnings create an incentive for firms to increase the very sort of tax avoidance schemes that have helped produce the current large accumulation of undistributed foreign earnings. As tax experts Lee Sheppard and Martin Sullivan have observed, “repatriation tax holidays have the effect of encouraging the very behaviors they were intended to reverse.”[19]

As Sullivan also put it, “Another repatriation holiday would remove the only significant restraint on them [U.S. multinational corporations] to move profits abroad. The dam would be broken.”[20]

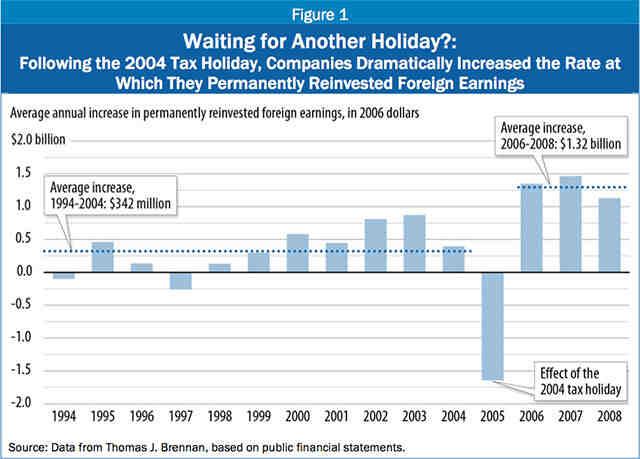

Indeed, a recent study by Northwestern University law professor Thomas J. Brennan strongly suggests that firms, anticipating a second holiday, have already aggressively shifted profits overseas. Analyzing the public records of a large group of U.S. multinationals that together accounted for 79 percent of the repatriations that occurred under the 2004 holiday, Brennan found that “since the holiday window, there has been a dramatic increase in the rate at which firms add to their stockpile of foreign earnings kept overseas.”[21] In each of the three years following the 2004 tax holiday, these companies increased the amounts of new “permanently reinvested” foreign earnings by three times as much, on average, as they had in the each of the ten years before the holiday (see Figure 1). [22]

The study found evidence that corporate tax sheltering, rather than changes in actual economic activity, is largely responsible for this trend. “[T]he increased amount of overseas investment appears to be driven in part by an increased tendency of firms to classify foreign earnings as permanently reinvested overseas”, the study reported. It concluded that the tax holiday appears to have been “a net failure” even in terms of achieving the elementary objective of returning foreign earnings to the United States. [23]

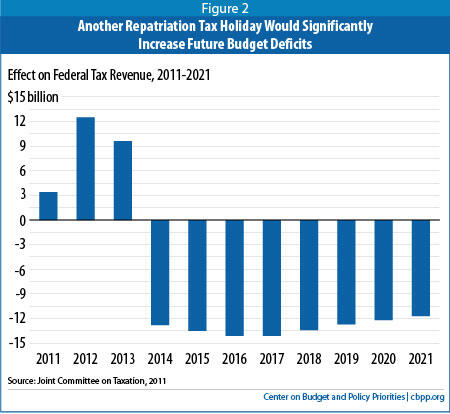

Such changes in corporate behavior in the aftermath of a tax holiday not only reduce domestic investment below what it otherwise would have been; they also increase budget deficits. Although lobbyists claim that a second repatriation holiday would “help reduce the deficit,” and could be achieved at “no cost to taxpayers,” any short-term revenue gains would be more than offset by long-term losses, producing a net increase in deficits and the national debt.[24]

Analyzing the fiscal effects of the 2004 tax holiday, the Joint Congressional Committee on Taxation (JCT) anticipated the changes in corporate behavior that various studies have since confirmed: JCT predicted that “at least some taxpayers would change their future behavior to anticipate a second [repatriation tax holiday], by investing more offshore than they would have done had a one-time tax holiday not been enacted, and keeping the resulting earnings offshore indefinitely.”[25] The JCT projected that the 2004 tax holiday would increase revenues by $2.8 billion in the first year but then decrease revenues each subsequent year by an average of $0.7 billion, for a net loss of $3.3 billion over ten years.[26]

Given the difficult fiscal challenges the nation faces, enlarging the deficit by enacting another tax holiday for overseas corporate profits would place even more pressure on the rest of the budget — from Medicare to scientific research, education, and infrastructure — and on the tax code itself, where it ultimately could lead to other tax increases to help offset these revenue losses.

It was largely because of the risk that a holiday would lead corporations to expect similar holidays in the future and thereby increase incentives for firms to shift investment overseas, with a resulting increase in the deficit, that Congress emphasized that the 2004 measure should be a one-time-only tax break. The conference report on the legislation creating the tax holiday stated: “The conferees emphasize that this is a temporary economic stimulus measure, and that there is no intent to make this measure permanent, or to ‘extend’ or enact it again in the future.” [28] Were Congress to break that promise and, just seven years later, allow corporations to repatriate accumulated foreign earnings again at an extraordinarily low rate, it would undermine the integrity and fairness of the corporate tax code and hasten the trend toward more aggressive corporate use of overseas tax shelters.

Claim that New Tax Holiday Is Needed to Address Firms’ Cash Shortage Is Extremely Dubious

Lobbyists pushing a new tax holiday have argued that large multinationals are currently cash-constrained and that they would make significant, job-creating investments in the United States if only they had access to their foreign earnings. This claim is extremely dubious.

According to the Federal Reserve, U.S. non-financial corporations now have $1.9 trillion in liquid assets, the highest level as a share of total corporate assets since 1959. Lobbyists argue that this number is misleading because a significant share of these assets is tied up overseas. Evidence suggests, however, that the largest multinational corporations — the ones that stand to gain most from a tax holiday — are not significantly constrained with respect to their cash position.

According to their most recent financial statements, the ten companies that are leading the lobbying on this issue [29] together have at least $47 billion (and likely much more) in cash and liquid assets that could be used for domestic investments, without triggering additional tax liability.[30] As Joel Slemrod, one of the nation’s leading tax economists, has observed, “The fact that they have these cash hoards suggests that investment is not being constrained by lack of cash.” Even Allen Sinai, chief global economist of Decision Economics and author of two earlier studies that corporations have cited in the past in support of a tax holiday, acknowledges that credit is not a significant restraint on corporations: “The case for [another repatriation tax holiday] now is not as strong because companies are so cash rich.”[31]

Various explanations have been offered for corporations’ large current cash holdings, but surveys indicate that the primary reasons firms are not investing more are lack of demand and uncertainty about the health of the economy.[32] During an economic downturn, the primary problem that firms usually face is a shortage of demand for their products, not a shortage of cash. In part for this reason, firms benefiting from another tax holiday are likely to retain most of the repatriated earnings (and the accompanying tax windfall) or pass them on to shareholders and business owners rather than invest them.[33]

The Congressional Research Service recently concluded that even if some firms are cash-constrained and might invest more if more cash were available, this constraint would likely apply primarily to small firms, which stand to benefit far less from a tax holiday. [34] Tax economist Martin Sullivan agrees: “A handful of America’s largest multinationals account for the bulk of unrepatriated accumulated foreign earnings. … They are not credit-constrained. Repatriation would provide cash flow to large multinationals — precisely the sector of the economy that does not need cash to finance investment.” [35]

Moreover, some of the companies currently citing cash shortages as an argument for another tax holiday have recently sent tens of billions of dollars back to shareholders through large stock repurchases and dividend payments. Consider the case of Cisco Systems. During the 2004 tax holiday, Cisco repatriated $1.2 billion at the temporary low corporate tax rate. Since then, the company has increased by $24.8 billion the amount of profits that are permanently reinvested overseas. In the Wall Street Journal last October, Cisco CEO John Chambers pushed for another tax holiday, contending that corporations’ current cash balances are irrelevant: “Large cash balances remain on U.S. corporate books because U.S. companies can’t spend their foreign-held cash in the U.S. without incurring a prohibitive tax liability.”[36] But in September 2010, just one month before he penned his op-ed implying that current cash reserves are largely inaccessible to companies, Chambers announced to investors that Cisco would issue the first dividend in the company’s history. The decision was described by Cisco’s Chief Financial Officer Frank Calderoni as “part of our continued commitment to return cash to shareholders.” Moreover, at a meeting with analysts in San Jose, California, Chambers himself said that the exact size of the dividend paymentwould depend in part on whether Congress would enact another tax holiday on repatriated profits. [37] In addition, two months later, Cisco’s board announced it was adding as much as $10 billion to a stock repurchase program on top of a previously-announced $72 billion.[38]

Nor is this trend limited to Cisco. Other companies that have joined the coalition lobbying for the tax holiday even as they use large cash reserves to buy back stock or increase dividends include:

- Pfizer, which announced a new $5 billion share repurchase program on February 1, 2011[39];

- Microsoft, which announced a 23 percent increase in its quarterly dividend on September 21, 2010 [40];

- Adobe Systems, which announced a plan to repurchase $1.6 billion in stock on June 22, 2010[41];

- Qualcomm, which announced a $3 billion stock repurchase program on March 1, 2010 as well as a 12 percent increase in its quarterly dividend on March 1, 2010[42]; and

- CA, Inc., which announced on May 15, 2010 that its board had authorized a $0.5 billion new stock repurchase program. [43]

In summary, an influx of additional cash is unlikely to change the investment decisions of companies that are not cash-constrained. As the NBER researchers reported, “In the absence of financial constraints, well-governed firms would choose optimal levels of investment and employment before the tax holiday, so they would not increase expenditures on capital and labor when the holiday occurred.” [44]

Biggest Beneficiaries Would Include Firms That Have Aggressively Shifted Income Overseas to Avoid U.S. Taxes

One reason many companies now find themselves with so much of their cash located overseas is that they have deliberately manipulated their finances to make it appear as though a large portion of their profits originate in low-tax countries where they remain outside the reach of the U.S. corporate income tax. Multinational corporations that artificially shift profits to low-tax countries often do so through the transfer of difficult-to-price intangible property or the strategic location of expenses. [45]

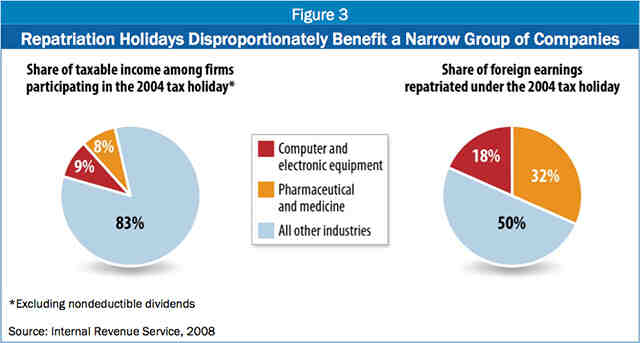

Former IRS Commissioner Mark Everson highlighted this growing trend in 2006 testimony. “Tax issues associated with the transfer of intangibles outside the United States,” Everson warned, “have been a high risk compliance concern for us and have seen a significant increase in recent years. Taxpayers, especially in the high technology and pharmaceutical industries, are shifting profits offshore.” [46] For this reason, the firms that have done the most to avoid U.S. corporate taxes stand to benefit disproportionately from another repatriation holiday, just as they did from the 2004 tax holiday.

Although a total of 843 companies participated in the 2004 tax holiday, the bulk of the benefit went to companies in the sectors identified by Everson as having made the most aggressive use of tax avoidance schemes. IRS data show that half of all qualifying repatriations under the 2004 tax holiday came from large pharmaceutical and technology corporations (see Figure 3)[47]; one large pharmaceutical company, Pfizer, alone accounted for over 10 percent of total repatriations.[48]

Lee Sheppard and Martin Sullivan have observed that “The principal effect of another repatriation holiday would be to reward multinationals for shifting income out of the United States to low-tax jurisdictions.”[49] Even setting this fact aside, there is no compelling reason to think that large, profitable pharmaceutical and technology companies have a particularly pressing need for credit that smaller firms and firms in other industries do not have, or that they deserve a lucrative tax break that would flow overwhelmingly to them.

Indeed, one of the factors that the Bush Administration cited in opposing the 2004 tax holiday was “concerns regarding the fairness” of the holiday to “U.S. companies that do not have foreign operations and have already paid their full and fair share of tax.” As the Bush Administration predicted, firms that made investments in the United States and paid their taxes received no benefit from the original tax holiday, while companies that had done the most to avoid paying U.S. taxes received the largest tax benefits. In this vein, Michael Mundaca, the Treasury’s current Assistant Secretary for Tax Policy, recently warned, “To pay for giving this large tax cut once again to a small group of U.S. companies without increasing the deficit, we would have to raise taxes on other U.S. businesses.”[50]

Conclusion

Providing large multinational corporations with a large tax cut via a repatriation tax holiday is not likely to generate the promised investments or jobs in the United States. Policymakers should be extremely skeptical of the claim that, despite the evidence that the 2004 tax holiday failed to boost investment or jobs significantly, the results would somehow be different the second time around. Corporations already have considerable cash reserves on hand to invest domestically if they so choose. And repeating the tax holiday would provide large benefits to many of the corporations that have acted most aggressively to shift income overseas and avoid U.S. taxes, and would encourage these and other firms to shift even more income overseas in anticipation of future tax holidays.

Policymakers also should reject fanciful claims that such a tax holiday would not increase the deficit. It is understandable why lobbyists are making these claims — it is difficult to explain why policymakers should enlarge the deficit in order to hand massive windfalls to large powerful multinational corporations at the same time that they are talking of a need to cut everything from Social Security benefits to education and investments in research and infrastructure on the grounds that deficits are too large.

If policymakers are concerned that companies now incur a tax liability when they bring foreign-earned income back to the United States, they could consider ending or limiting the feature of the tax code that created this disincentive in the first place: the ability to indefinitely defer payment of U.S. corporate income taxes on overseas profits. Such a step, by reducing the tax distortions between foreign-held and repatriated earnings, would have the same practical effect as the tax holiday while raising — rather than losing — significant new tax revenue helping to preserve the corporate tax, and eliminating a major incentive for firms to shift jobs and profits overseas.

End Notes

[1] At a Third Way event last week, Reps. Jared Polis (CO) and Loretta Sanchez (D-CA) as well as Sen. Kay Hagan (D-NC) expressed support for the idea, while another group, NDN, hosted a working lunch on the idea earlier this month. See Tim Fernholz, “Democrats Warming to Tax Repatriation,” NJ Daily AM, Tuesday, June 21, 2011.

[2] David Kocieniewski, “Companies Push for Tax Break on Foreign Cash,” New York Times, June 19, 2011.

[3] Section 965 to the Internal Revenue Code, which established the 2004 tax holiday, allowed multinational corporations to deduct (that is, to pay no taxes on) 85 percent of qualifying dividends received from their controlled foreign corporations (CFCs). If companies paid the top corporate tax rate of 35 percent on the remaining 15 percent of their repatriated profits, the effective tax rate would have been 5.25 percent [0.15*0.35=0.0525]. But about 30 percent of even that reduced tax liability was eliminated by foreign tax credits. As a result, the effective rate was actually closer to 3.7 percent [0.15*0.35*0.7=0.03675]. See Edward D. Kleinbard and Patrick Driessen, “A Revenue Estimate Case Study: The Repatriation Holiday Revisited,” Tax Notes Special Report, September 22, 2008.

[4] The zero percent rate would be available to all funds repatriated pursuant to a “qualified domestic reinvestment plan.” Amounts used for other purposes would be taxed at an effective rate of about 5.25 percent (less after foreign tax credits are taken into account). As this paper explains, restrictions on the allowable uses of repatriated earnings are practically impossible to enforce. For this reason, it is unlikely that this distinction drawn in the Bibray bill (H.R.1036) would have much practical relevance, and the overwhelming majority of funds would consequently qualify for the zero percent rate.

[5] H.R. 1162: “Invest in America Act of 2003.”

[6] Melissa Redmiles, “The One-Time Received Dividend Deduction,” IRS Statistics of Income Bulletin, Spring 2008, http://www.irs.gov/pub/irs-soi/08codivdeductbul.pdf.

[7] Dhammika Dharmapala, Kristin J. Foley, and C. Fritz Forbes, “Watch What I Do, Not What I Say: The Unintended Consequences of the Homeland Investment Act,” NBER Working Paper, June 2009.

[8] Clemons and Kinney, “An Analysis of the Tax Holiday for Repatriation Under the Jobs Act,” Tax Analysts Special Report, October 20, 2008.

[9] Jennifer Blouin and Linda Krull, “Bringing It Home: A Study of the Incentives Surrounding the Repatriation of Foreign Earnings Under the American Jobs Creation Act of 2004,” Journal of Accounting Research, September 2009.

[10] Donald J. Marples and Jane G. Gravelle, “Tax Cuts on Repatriation Earnings as Economic Stimulus: An Economic Analysis,” Congressional Research Service, January 30, 2009.

[11] Dharmapala, Foley, and Forbes, 2009.

[12] “Letter to the Honorable Charles E. Grassley,” October 4, 2004.

[13] Roy Clemons and Michael R. Kinney, “An Analysis of the Tax Holiday for Repatriation Under the Jobs Act,” Tax Analysts Special Report, October 20, 2008.

[14] Kimberly A. Clausing, “The American Jobs Creation Act of 2004: Creating Jobs for Accountants and Lawyers,” Urban-Brookings Tax Policy Center, December 2004, http://www.taxpolicycenter.org/UploadedPDF/311122 _AmericanJobsAct.pdf .

[15] New York Times , “Postcards from a Tax Holiday,” November 12, 2005.

[16] Nadal, 2008.

[17] Lisa M. Nadal, “News Analysis: Repatriation Gluttony — Was it Worth It?” Tax Analysts, 2008.

[18] Michael Mundaca, “Just the Facts: The Costs of a Repatriation Tax Holiday,” Treasury Notes, March 23, 2011 http://www.treasury.gov/connect/blog/Pages/Just-the-Facts-The-Costs-of-a-Repatriation-Tax-Holiday.aspx .

[19] Lee A. Sheppard and Martin A. Sullivan, “Multinationals Accumulate to Repatriate,” Tax Notes, January 19, 2009.

[20] See Mike Zapler, “Economists: Tax holiday not a jobs machine, Politico, March 11, 2011. In a similar vein, Sullivan also has noted that “Subjecting foreign profits to full U.S. tax on repatriation put[s] a speed limit on profit shifting. Without it, we are on the Autobahn.” Martin A. Sullivan, “Repatriation Holiday Would Destroy American Jobs,” Tax Notes, November 15, 2010.

[21] Thomas J. Brennan, “What Happens After a Holiday?: Long-Term Effects of the Repatriation Provision of the AJCA,” Northwestern Journal of Law and Social Policy, Spring 2010.

[22] Tax experts Lee Sheppard and Martin Sullivan drew a similar conclusion when they analyzed the financial statements of firms that participated in the 2004 holiday. They calculated a measure of how much profit multinationals keep offshore with the intention of maximizing tax advantages; between 2003 and 2007, the annual increase in this measure doubled, from $60 billion to $122 billion. See Lee A. Sheppard and Martin A. Sullivan, “Multinationals Accumulate to Repatriate,” Tax Notes, January 19, 2009.

[23] Brennan, 2010.

[24] The website of the lobbying coalition claims, “This money will help strengthen our economic recovery, create jobs, and help reduce the deficit – at no cost to taxpayers.” WinAmerica: Investing Here at Home, accessed March 28, 2011, http://www.winamericacampaign.org/issues/background/.

[25] Kleinbard and Driessen, 2008.

[26] Kleinbard and Driessen, 2008.

[27] Joint Committee on Taxation, “Letter to Hon. Lloyd Doggett,” April 15, 2011.

[28] H. Rept. 108-55, p. 65.

[29] BusinessWeek identified those ten companies as Adobe Systems, Apple, CA Technologies, Cisco, Duke Energy, Google, Microsoft, Oracle, Pfizer, and Qualcomm. Peter Coy and Jesse Drucker, “Tax Holiday for $1 Trillion May Lure Profits Without Spurring U.S. Growth,” March 17, 2011.

[30] We calculated this $47 billion figure from the public financial statements of the ten companies, by subtracting all unremitted foreign earnings from the total of cash and cash equivalents plus liquid investments for each company. This calculation likely understates these corporations’ domestic cash position because, in subtracting all “unremitted foreign earnings,” we necessarily subtracted too much. Some portion of those earnings (the firms’ financial statements do not specify what portion) are not in cash because they have been invested abroad in factories or other illiquid assets. This portion of unremitted foreign earnings thus is not included in the total of cash, cash equivalents, and liquid investments for each company, and thus should not have been subtracted from that total. Because we had no alternative but to subtract all unremitted foreign earnings, the $47 billion figure that our calculations produce is too low.

[31] Quoted in Mike Zapler, “Economists: Tax holiday not a jobs machine,” March 11, 2011 http://www.politico.com/news/stories/0311/51070.html.

[32] See for example Robert Sadowski, “A Cash Buildup and Business Investment,” Federal Reserve Bank of Cleveland: Economic Trends, January 10, 2011, http://www.clevelandfed.org/research/trends/2011/0111/01regact.cfm .

[33] Policymakers should also keep in mind that the tax-cut legislation enacted in December includes a very generous incentive for all businesses to make investments in the United States. The law allows for 100 percent immediate expensing in 2011 (that is, for an immediate deduction of all investments in new plants and equipment). This is purposefully designed as a tax incentive for new investment. In contrast, a tax repatriation holiday is a tax cut on profits generated by investments that have already been made.

[34] Jane G. Gravelle, “Tax Cuts and Economic Stimulus: How Effective Are the Alternatives?” Congressional Research Service, December 5, 2008, p. 5.

[35] Martin A. Sullivan, “Repatriation Holiday Would Destroy American Jobs,” Tax Notes, November 15, 2010.

[36] John Chambers and Safra Catz, “The Overseas Profits Elephant in the Room,” Wall Street Journal, October 20, 2010, http://online.wsj.com/article/SB10001424052748704469004575533880328930598.html .

[37] “Cisco Press Conference with CEO Chambers,” Tech Trader Daily, September 14, 2010.

[38] Meanwhile, Cisco has cuts its effective tax rate in half since the late 1990s, largely because of aggressive profit shifting to low-tax countries. As Martin Sullivan observes, “U.S. tax rules on deferral may have trapped Cisco’s cash overseas. But it is Cisco’s opportune use of lax U.S. transfer pricing rules that puts it there.” Martin A Sullivan, “Cisco CEO Seeks Relief for Profits Shifted Overseas,” Tax Notes, November 29, 2010.

[39] Business Wire, “Pfizer Announces New $5 Billion Share Repurchase Program,” February 01, 2011.

[40] Microsoft News Center, “Microsoft Announces 23 Percent Increase in Quarterly Dividend,” September 21, 2010.

[41] Adobe Systems Incorporated, “Adobe Reports Record Revenue: Company Announces Plan to Repurchase $1.6 Billion of Stock,” June 22, 2010.

[42] “Qualcomm Increases Quarterly Dividend by 12% and Announces New $3.0 Billion Stock Repurchase Program,” Qualcomm Incorporated Press Release, March 01, 2010.

[43] “CA's Board of Directors Approves $500 Million Common Stock Repurchase Program,” CA, Inc., Press Release, May 13, 2010.

[44] Dhammika Dharmapala, Kristin J. Foley, and C. Fritz Forbes, “Watch What I Do, Not What I Say: The Unintended Consequences of the Homeland Investment Act,” NBER Working Paper, June 2009.

[45] For an example of how this sort of tax planning works, see Jesse Drucker, “Google 2.4% Rate Shows How $60 Billion Lost to Tax Loopholes,” Bloomberg News, October 21, 2010.

[46] Written Testimony of Commissioner of Internal Revenue Mark Everson before the Senate Committee on Finance, June 13, 2006 http://www.irs.gov/newsroom/article/0,,id=158644,00.html.

[47] Redmiles, 2008.

[48] Nadal, 2008.

[49] Lee A. Sheppard and Martin A. Sullivan, “Repatriation Aid for the Financial Crisis?,” Tax Notes, January 5, 2008.

[50] Mundaca, 2011.

Más de los autores

Areas of Expertise