Six Tests for Corporate Tax Reform

Reform Should Help Shrink Long-Term Deficits, Reduce Biases and Preferences in the Tax Code, and Discourage Tax Sheltering

Congress may consider major changes to the corporate tax code this year. In light of the nation's significant economic and budgetary challenges, a well-designed corporate tax reform proposal should:

- Contribute to long-term deficit reduction. Corporate tax revenues are now at historical lows as a share of the economy, at a time when the nation faces deficits and debt that are expected to grow to unsustainable levels. Although the top statutory corporate tax rate is high, the average tax rate — that is, the share of profits that companies actually pay in taxes — is substantially lower because of the tax code's many preferences (deductions, credits and other write-offs that corporations can take to reduce their taxes). Moreover, when measured as a share of the economy, U.S. corporate tax receipts are actually low compared to other developed countries. All parts of the budget and the tax code, including corporate taxes, should contribute to deficit reduction. Well-designed corporate tax reform can improve economic efficiency and help on the deficit-reduction front at the same time.

- Reduce the tax code's bias toward overseas investments. U.S. multinationals pay much lower taxes on profits from their overseas investments than on profits from their domestic investments. That gives corporations a strong incentive to shift economic activity and income from the United States to other countries. Policymakers should address the features of the corporate tax code that allow so much business activity to escape taxation and that favor foreign investments over domestic ones.

- Improve economic efficiency by reducing special preferences. The corporate tax code taxes different kinds of corporate investments at very different rates. This "unlevel playing field" encourages businesses to choose among investments in substantial part based on their tax benefits, instead of making those decisions based entirely on investments' real economic value. Policymakers should level the playing field through corporate tax reform.

- Provide more neutral treatment of corporate and non-corporate businesses. Over time, various policy changes have made it easier for companies to enjoy the benefits of corporate status without being subject to the corporate income tax. Reform should reflect the guiding principle that firms engaging in similar activities and enjoying similar legal benefits should be taxed at similar rates.

- Reduce the tax code's bias towards debt financing. The current corporate tax code encourages corporations to finance their investments with debt (e.g., by issuing bonds) rather than equity (e.g., by selling stock). This encourages corporations to rely excessively on debt, which, as the recent financial crisis demonstrated, poses risks for both the firms and the broader economy. The tax code should be more even-handed in treating these two types of financing.

- Take specific steps to discourage tax sheltering. If policymakers lower the statutory corporate tax rate to well below the top individual tax rate, they should also establish safeguards to prevent high-income individuals from sheltering their income in corporations in order to pay taxes at a lower rate.

This report explains why these tests are an essential measuring stick for reform proposals.

1. Does the proposal contribute to long-term deficit reduction?

For a number of reasons, corporate tax reform is a solid candidate to make a contribution to fiscal improvement:

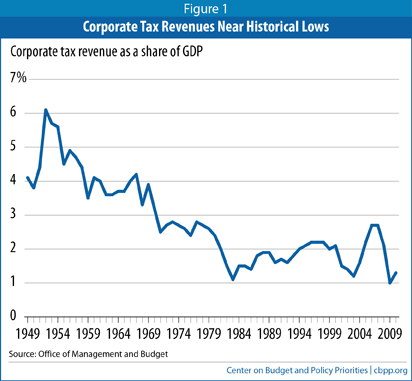

- During the 1950s, federal corporate tax revenue averaged 4.7 percent of the gross domestic product (GDP). But by the most recent decade (2000-2009), corporate taxes had fallen to just 1.9 percent of GDP (see Figure 1). As a result of this trend and other policy changes, the corporate tax now contributes considerably less to federal revenues than it once did: between 2000 and 2009, 10.7 percent of federal revenues were collected through the corporate tax, down from 29.8 percent of revenues in the 1950s.

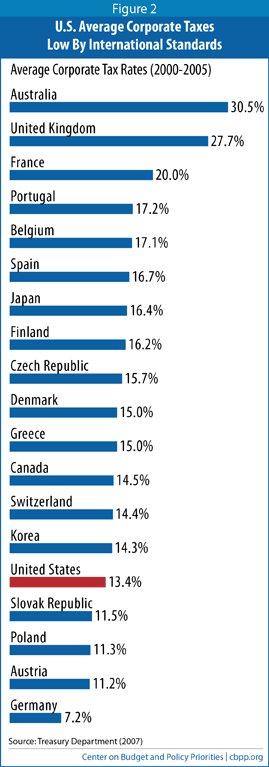

- In recent decades, and especially since the start of the 1980s, corporate profits have increased as a share of GDP — but corporate tax revenues have not followed suit. The non-partisan Congressional Research Service (CRS) recently summarized the upshot of this trend: "Despite concerns expressed about the size of the corporate tax rate, current corporate taxes are extremely low by historical standards, whether measured as a share of output [i.e., GDP] or based on the effective tax rate on income."[1]Between 2000 and 2005, the share of corporate operating surplus[2] that U.S. corporations pay in taxes — a proxy for the average tax rate — was the second lowest among the studied G7 leading industrialized nations and nearly 3 percentage points below the average of member nations in the Organisation for Economic Co-operation and Development (OECD), according to a 2007 Treasury Department report (see Figure 2, next page).[3] As that report summarized, "The contrast between [the United States'] high statutory corporate income tax rate and low average corporate tax rate implies a relatively narrow corporate tax base, due to accelerated depreciation allowances, corporate tax preferences, and tax-planning incentives created by [the] high statutory rate."Imagen

- The U.S. corporate tax code includes a host of special provisions that significantly reduce the taxes that most corporations owe. In addition to being economically inefficient, these provisions are expensive: in its 2007 report, the Treasury Department estimated the revenue loss from corporate tax preferences at more than $1.2 trillion over ten years.

- Largely because of these preferences, the corporate tax base is very narrow. This reduces economic efficiency by creating an unlevel playing field for different forms of investment, which encourages firms to invest in areas that would not have merited such investments in the absence of the tax breaks. In fact, there is a strong case for tax policy changes that raise revenue and reduce the deficit even as they lower the statutory tax rate, increase economic efficiency, and boost competitiveness.

The case for designing corporate tax reform that reduces long-term deficits grows even stronger when one considers the opportunity costs. As the incipient debate over how deeply to cut funding for domestic discretionary programs has already made clear, adequate investments that are important to the economy's future — in scientific research, education, and infrastructure — are likely to be at significant risk. The failure of corporate tax reform to contribute to deficit reduction would increase this risk.

Moreover, corporations have a large stake in sustainable fiscal policy. In addition to benefiting from the types of public investments that the current fiscal situation puts at risk, corporations are affected by borrowing costs. Persistent large budget deficits are likely to put upward pressure on underlying interest rates, which would in turn raise the cost of capital for businesses and other borrowers.[4]

Corporate tax reform that reduces the statutory rate and broadens the base on a revenue-neutral basis could still benefit the economy by reducing the economic distortions created by the current tax system.[5] But given the nation's major fiscal challenges, revenue-neutral corporate tax reform would represent a missed opportunity. Policymakers are just starting to wrestle seriously with long-term deficits. Taking a major revenue source off the table for deficit reduction at the outset would be ill-advised.

Also ill-advised are proposals that pair one-time or temporary revenue-raisers (like a one-time tax on repatriated foreign earnings) with permanent revenue-losers (like rate reductions), whose true costs become clear only over the long run.[6] Given that our fiscal challenges are fundamentally long-term in nature, it would be irresponsible to adopt a package of reforms that might be deficit-neutral over the ten-year budget window but increases borrowing in subsequent years. Corporate tax reform should adhere to the following principle: changes that raise revenue on only a temporary basis should not be used to pay for changes that permanently increase the deficit.

2. Does the proposal reduce the tax code's bias toward overseas investments?

International tax regimes span the spectrum between "residence" (or "worldwide") and "territorial." A residence tax system taxes a company on its global income, regardless of where that income was generated; a territorial system taxes only the domestic share of a multinational company's income.

The current U.S. corporate income tax, while often characterized as a worldwide system, is actually a hybrid. It does tax U.S.-based corporations on a worldwide basis, while providing a credit for foreign taxes paid in order to avoid double taxation. In a major nod in the territorial direction, however, foreign profits are not taxed until they are repatriated. In practice, corporations often "defer" repatriating their foreign profits indefinitely, with the result that those profits are never subjected to U.S. taxes — even though corporations may obtain an immediate U.S. tax deduction for expenses they incur in supporting the same overseas investments. As tax expert Edward Kleinbard has observed, "the residual tax the United States collects on repatriated income is surprisingly small."[7]

This deferral feature, combined with other provisions that reduce the effective tax rate on foreign investments, often allows U.S. multinationals to pay significantly lower taxes on profits from their overseas investments than on profits from their domestic investments. The average combined tax rate, including both U.S. and foreign taxes, on large (i.e., assets over $10 million) corporations' total foreign-source income was 16.1 percent in 2004, two-thirds of the 25 percent tax rate on their domestic income, according to a 2008 Government Accountability Office (GAO) study. (The average U.S. effective tax rate on foreign-source income was around 4 percent.)[8] Such a large differential between tax rates on domestic and foreign income provides strong incentives for firms to shift both actual investments and reported profits from the United States (and other countries with comparable tax rates) to low-tax countries.[9]

This tilt in the tax code in favor of foreign investments has important revenue implications: the deferral provision will cost the Treasury $212.8 billion over the 2012-2016 period, according to the Office of Management and Budget, making it one of the single largest tax expenditures in the corporate tax code. Moreover, because corporations often finance foreign investments through domestic debt and then deduct the interest payments on that debt during the calculation of their U.S. tax bill, these investments erode the effective tax rate even on domestic profits. [10] As policymakers begin work on base-broadening tax reforms, they should remember that the result of leaving the deferral feature and other international tax expenditures untouched — let alone expanding them, as some have proposed — would be higher tax rates on domestic investments than would otherwise need to be the case.

Representatives of U.S. multinationals are likely to note that most developed countries operate under a territorial tax regime, and to argue that this puts them at a competitive disadvantage.[11] But in reality, few countries have the sort of free-rein territorial system that the lobbyists of those multinationals often promote — one that would do little or nothing to prevent companies from evading domestic taxes by shifting income to foreign jurisdictions.

Moreover, in considering this complex issue, policymakers should recognize that the interests of U.S. multinationals may differ from those of domestic U.S. firms, which in turn may differ from those of American workers. A CRS analysis calls attention to this point: "Economic theory acknowledges that a home-country [tax] exemption for foreign income may well maximize the competitiveness of the home country's multinationals. Again, however, economics indicates that a broader perspective produces different results." Specifically, "if a country is capital-rich, as is the United States, the capital exporting country's economic welfare is maximized when tax policy to some extent discourages overseas investment" relative to domestic investment.[12]

As the Tax Policy Center has highlighted, our tax code currently provides exactly the opposite incentives: "[Deferral] and other incentives also encourage firms to locate physical assets, production, and jobs in [foreign] countries."[13] Similarly, Kleinbard has noted that the current tax structure encourages domestic multinationals to shift real investments — not just accounting profits — overseas.[14] It is important that policymakers also consider the perspective of American workers, given that in recent decades, due to a confluence of factors, real wages of production workers have stagnated. [15]

Intel's former CEO, Andy Grove, recently wrote that while U.S. entrepreneurs continue to develop new products and technologies, the subsequent "scaling up" process by which companies build the capacity and hire the workers to mass-produce these innovations now occurs primarily in foreign countries rather than in the United States.[16] He asked: "[W]hat kind of a society are we going to have if it consists of highly paid people doing high-value-added work — and masses of unemployed?" Grove argued that public policy — including tax policy — should seek to address this problem.

Accordingly, policymakers should reevaluate elements of the corporate tax code that not only reduce tax revenues by allowing so much foreign business activity to escape taxation but also favor overseas investments over domestic investments.

3. Does the proposal improve economic efficiency by reducing special preferences?

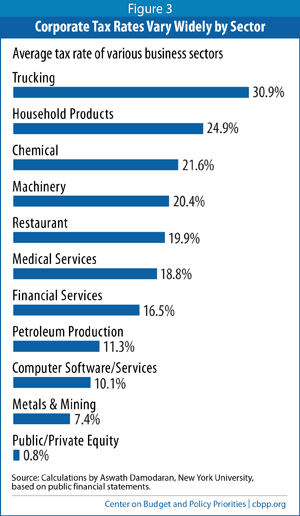

For example, the Congressional Budget Office has estimated that the effective marginal corporate-level tax rate [17] ranges from 29 percent on computer equipment to a negative 2.2 percent on petroleum and natural-gas structures.[18] Such enormous disparity creates economic distortions and inefficiency, since it encourages businesses to choose among investments based on their after-tax return, which may differ greatly from their real economic value. These distortions contribute heavily to dramatic variations in effective tax rates across industries (see Figure 3).

Tax reform that moves toward a more even-handed treatment of different kinds of investments would improve economic efficiency. Policymakers may still want to favor certain activities, such as research and development, that produce benefits beyond those that the individual firm will realize itself — but such exceptions to tax neutrality should stem from deliberative and informed policy decisions.

4. Does the proposal reflect careful consideration of the boundary between corporate and non-corporate taxation?

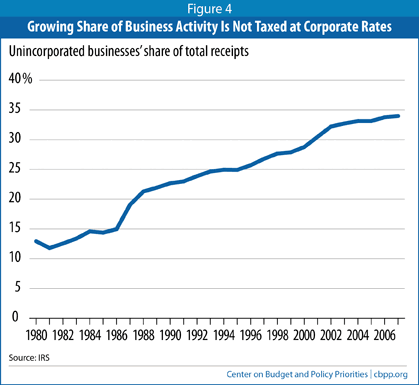

The share of business activity that is subject to corporate taxes has declined significantly in recent decades, largely because of policy changes that have made it easier for firms to obtain the benefits of corporate status while avoiding corporate-level taxes.

Although businesses operating through C-corporations are subject to corporate taxes, the capital income of some other types of businesses is "passed through" to the business owners. These owners benefit from the same tax deductions and credits as do corporations, but are taxed only at the individual level.

While the relative benefits of pass-through versus corporate taxation depend on a number of factors, [19] businesses whose investors face the top two marginal tax rates are generally better off from a tax perspective operating as a pass-through.[20] In other words, the current tax code creates strong incentives for companies to organize as pass-through entities, allowing their investors to avoid corporate-level taxes entirely.

Over the past half century, and particularly during the 1980s and 1990s, states and the federal government significantly expanded the legal benefits of pass-through entities. These changes have made it easier for businesses to operate through such legal structures as S corporations, partnerships, limited liability companies, and sole proprietorships — while also benefiting from limited liability and other provisions that formerly were available only to corporations.

This trend toward non-incorporation is a significant contributor to the erosion of the corporate income tax base. As a recent CRS study explained: "While a large fraction of the decline in corporate tax revenues is associated with [changes] in rates and depreciation, other causes may be more liberal rules that allow firms to obtain benefits of corporate status (such as limited liability) while still being taxed as unincorporated businesses and tax evasion, particularly through international tax shelters."[22]

The reality is that under current policy, two businesses of equal size, engaged in like activities, and enjoying similar legal benefits can be taxed at dramatically different rates. Accordingly, President George W. Bush's Advisory Panel on Federal Tax Reform proposed restricting availability of pass-through taxation, such as by taxing all large businesses — including those currently taxed as pass-through entities — through the corporate income tax.[23] Similarly, the President's Economic Recovery Advisory Board (PERAB) highlighted this concern, and suggested that corporate tax reform might adopt the goal of providing "tax neutrality with respect to organizational form." [24] Reform efforts should reflect the guiding principle that, just as similar investments should be subject to similar tax treatment, so should firms engaging in similar activities and enjoying similar benefits be taxed at similar rates. [25]

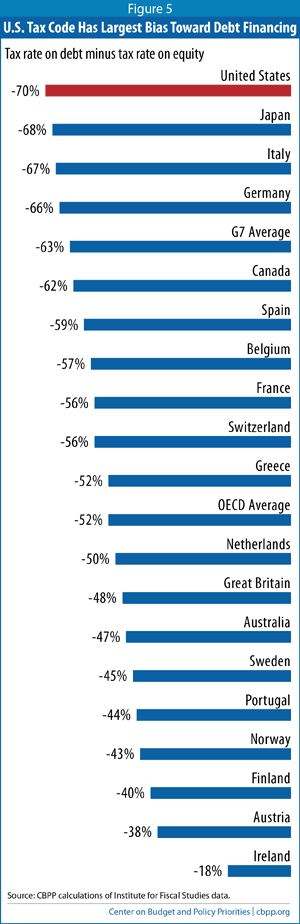

5. Does the proposal reduce the tax code's bias towards debt financing?

The corporate income tax code encourages corporations to finance their investments with debt rather than equity. Indeed, the tax code provides a large subsidy — a negative tax rate of 46 percent — for corporate financing of equipment investments with debt. When a corporation issues debt to finance the purchase of an investment asset, it can deduct both the depreciation of the asset and the interest it pays on the debt. In contrast, firms that finance investment with equity can claim the depreciation deduction but not the value of the dividends they pay to their investors.

The 2007 Treasury report also noted that "excessive reliance on debt financing imposes costs on investors because of the associated increased risk of financial distress and bankruptcy." It imposes costs on taxpayers and the overall economy as well, as the recent financial crisis demonstrates. Leverage ratios of the major financial firms rose sharply in the years leading up to the crisis, leaving very thin equity cushions when the financial crisis hit. The excess leverage went beyond the financial services sector, with significant economic consequences. As the Treasury report warned, "Excessive reliance on debt financing increases the rigidity of the corporate capital structure and subjects investors to larger costs associated with bankruptcy and financial distress."

In a similar vein, a 2009 International Monetary Fund report concluded that large biases toward debt financing in corporate tax codes are "hard to justify given the potential impact on financial stability" and that "one lesson of the [recent financial] crisis may be that the benefits from mitigating [these biases] are far greater than previously thought."[26] Reducing the bias toward debt financing thus is an important test for corporate tax reform proposals.

6. Does the proposal take specific steps to discourage tax sheltering?

While lowering the statutory rate and broadening the base would make the corporate tax code more economically efficient, those steps come with a potential risk that policymakers should mitigate as much as possible — cutting the statutory rate below the top individual tax rate could give high-income individuals the opportunity to avoid taxes by sheltering their income within a corporation. PERAB highlighted this risk in its report on tax reform, noting that a significant reduction in the corporate rate "could encourage both the shifting of income from the individual income tax base to the corporate tax base and the sheltering of income in corporations."[27]

The top corporate tax rate of 35 percent is currently equal to the top rate on individuals. Were policymakers to lower the corporate rate significantly, some high-income individuals could reduce their tax burden by "retaining" a portion of their earnings in a corporation rather than receiving the earnings as ordinary income that is taxed at the top individual tax rate. These retained earnings could initially accumulate in a corporation and subsequently be distributed to owners through dividends or realized as capital gains, both of which are currently taxed at 15 percent.

To some extent, current law restricts the ability of corporations to accumulate these retained earnings. For example, companies pay a tax on retained earnings that exceed what is considered a reasonable level. Nevertheless, because a significant corporate rate cut would increase the incentive to shelter, PERAB concluded that policymakers may need to provide "additional safeguards."

The Congressional Research Service offered a possible way to reduce the incentive to shelter, noting that the scope of sheltering "would be limited if dividends and capital gains were taxed at higher rates."[28] Policymakers should explore this option, along with other steps to strengthen existing restrictions or enact additional safeguards.

End Notes

[1] Jane G. Gravelle and Thomas L. Hungerford, "Corporate Tax Reform: Issues for Congress," Congressional Research Service, updated April 6, 2010.

[2] Operating surplus is an accounting concept used in the OECD national accounts statistics to represent the portion of a firm's production-derived income that is not distributed to workers. While actual corporate capital income is the ideal metric for this sort of international comparison, no such measure exists in a form that can be compared across countries and time. For this reason the Treasury study, following a number of other researchers, uses corporate operating surplus as a proxy measurement of corporate capital profits.

[3] U.S. Department of the Treasury, "Treasury Conference on Business Taxation and Global Competitiveness: Background Paper," July 23, 2007, http://www.treasury.gov/press-center/press-releases/Documents/07230%20r.pdf . Note: the Treasury study did not report the average tax rate for Italy, a member of the G7.

[4] See Congressional Budget Office, "The Long-Term Budget Outlook," June 2010, http://www.cbo.gov/ftpdocs/115xx/doc11579/06-30-LTBO.pdf.

[5] See: Aviva Aron-Dine, "Well-Designed, Fiscally Responsible Corporate Tax Reform Could Benefit the Economy," Center on Budget and Policy Priorities, June 4, 2008, https://www.cbpp.org/sites/default/files/atoms/files/6-4-08tax.pdf.

[6] Tax expert John Buckley has noted that a similar dynamic characterized the individual income tax rate reductions in the 1986 tax overhaul. Because those permanent rate cuts were financed in large part with temporary timing changes, they proved unsustainable, and Congress later partially reversed them. Comments at "Tax Analysts Roundtable Discussion on: Taxes and Small Business," January 20, 2012.

[7] Edward D. Kleinbard, "Stateless Income's Challenge to Tax Policy," Tax Notes Special Report, September 5, 2011.

[8] Government Accountability Office, "U.S. Multinational Corporations: Effective Tax Rates Are Correlated with Where Income Is Reported," August 2008, http://www.gao.gov/new.items/d08950.pdf.

[9] Multinational corporations are often able to shift reported profits to low-tax countries through complex transactions (typically involving the transfer of intangible property or the strategic location of expenses) that reduce the effective tax rates on these investments.

[10] See Kleinbard, 2011, page 1035.

[11] If a U.S. multinational and a company from a country with a territorial system compete in a third country, the foreign firm will face no home-country tax, while the U.S. firm will in theory face U.S. tax on its profits, albeit on a deferred basis.

[12] As the CRS report explains, while the welfare of multinational corporations is maximized under a territorial-type system, and capital-rich countries are best off under a system that tilts the scales in favor of domestic investment, global welfare is maximized where firms' international investment decisions are not affected by differential tax burdens — i.e., a worldwide system that taxes foreign and domestic profits equally. Congressional Research Service, "Taxes and International Competitiveness," May 19, 2006.

[13] Tax Policy Center, "The Tax Policy Briefing Book: A Citizens' Guide for the 2008 Election, and Beyond," http://www.taxpolicycenter.org/briefing-book/TPC_briefingbook_full.pdf .

[14] See Kleinbard, 2011, pages 1034-1035.

[15] Current Employment Statistics Survey, "Average Weekly Earnings of Production and Nonsupervisory Employees," http://www.bls.gov/webapps/legacy/cesbtab8.htm.

[16] Andy Grove, "How America Can Create Jobs," Bloomberg Businessweek, July 1, 2010, http://www.businessweek.com/magazine/content/10_28/b4186048358596.htm .

[17] The effective marginal tax rate is the percentage of investment returns that is paid in taxes on a "marginal" investment. A marginal investment is one that earns returns just high enough to make it worthwhile. The effective marginal tax rate is often the best measure of how the corporate tax affects incentives to invest, whereas average tax rates, computed as the ratio of corporate taxes to corporate capital income, is generally the better representation of the overall corporate tax burden. See: Treasury Department, 2007.

[18] Congressional Budget Office, "Background Paper: Computing Effective Tax Rates on Capital Income," December 2006. Note: The effective tax rates included in CBO's published analysis incorporate both corporate and personal taxes on investment income. Effective tax rates reflecting only the corporate income tax are drawn from CBO's back-up spreadsheet, available at http://cbo.gov/doc.cfm?index=7698.

[19] The primary factors are the marginal personal and corporate tax rates faced by investors, the tax rates for dividends and long-term capital gains, and the length of time the investments are expected to be held (since investors in C-corporations benefit from the ability to defer those individual-level taxes until the gains on those investments are realized).

[20] This is true under both current tax rates and a number of proposed changes to maximum individual, corporate, and long-term capital gains tax rates. See Gary Guenther, "Distribution of Small Business Ownership and Income by Individual Tax Rates and Selected Policy Issues," Congressional Research Service, February 26, 2010.

[21] Alfons J. Weichenrieder, "Survey on the Taxation of Small and Medium-Sized Enterprises," OECD Centre for Entrepreneurship, SMEs & Local Development, revised September 2007, http://www.oecd.org/dataoecd/52/25/39597756.pdf.

[22] Gravelle and Hungerford, 2010.

[23] The President's Advisory Panel on Federal Tax Reform, "Simple, Fair, & Pro-Growth: Proposals to Fix America's Tax System," November 1, 2005, http://govinfo.library.unt.edu/taxreformpanel/.

[24] The President's Economic Recovery Advisory Board, "The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation," August 2010, http://www.whitehouse.gov/sites/default/files/microsites/PERAB_Tax_Reform_Report.pdf .

[25] To be sure, lowering the statutory corporate tax rate would reduce somewhat the incentive to avoid the corporate rate through non-incorporation. It is unlikely, however, that this would be sufficient to stem the flow of new businesses and new investments into the unincorporated sector.

[26] International Monetary Fund, "Debt Bias and Other Distortions: Crisis-Related Issues in Tax Policy," June 12, 2009, www.imf.org/external/np/pp/eng/2009/061209.pdf.

[27] The President's Economic Recovery Advisory Board, "The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation," August 2010, http://www.whitehouse.gov/sites/default/files/microsites/PERAB_Tax_Reform_Report.pdf .

[28] Gravelle and Hungerford, 2010.

Más de los autores

Areas of Expertise