Federal Spending Target of 21 Percent of GDP Not Appropriate Benchmark for Deficit-Reduction Efforts

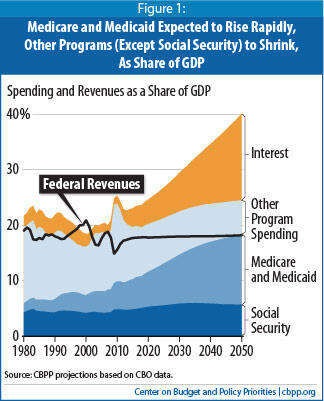

The average level of federal spending over the years since 1970 — about 21 percent of gross domestic product (GDP) — does not provide a reasonable benchmark for the level of spending that will be necessary or appropriate in the future. The Heritage Foundation has proposed that, in developing its recommendations, the President’s Commission on Fiscal Responsibility and Reform “should target the historical levels of taxes . . . and spending.” [1] Erskine Bowles, co-chair of the commission, has suggested that spending and revenues be balanced at no more than 21 percent of GDP.[2] Such recommendations, however, fail to take account of fundamental changes in society and government — the aging of the population, substantial increases in health care costs, and new federal responsibilities in areas such as homeland security, education, and prescription drug coverage for seniors. These factors make the expenditure levels of several decades ago inapplicable today.

A careful analysis of these factors indicates that it will not be possible to maintain federal expenditures at their average level for decades back to 1970 without making draconian cuts in Social Security, Medicare, and an array of other vital federal activities.

Over the 40 years from 1970 through 2009, revenues averaged a little over 18 percent of GDP, and expenditures averaged nearly 21 percent of GDP. Those averages reflected a federal government with far less responsibility than today, and a country with a much smaller percentage of elderly people and considerably lower health care costs. Averages for federal spending and revenues in past periods consequently are not very relevant for discussions about how to reduce deficits to economically sustainable levels in the decades to come.

Specifically:

- The aging of the population and increases in per-person costs throughout the U.S. health care system (in both the public and private sectors) will increase the cost of meeting longstanding federal commitments to seniors and people with disabilities. Together, these factors will drive up spending for the three largest domestic programs — Medicare, Medicaid, and Social Security. Limiting total federal spending to 21 percent of GDP despite these developments would have enormous implications for those programs as well as the rest of government.

- The federal government’s responsibilities have grown since 2000, with developments at home and abroad pushing spending above the average for earlier decades. These responsibilities include homeland security (in the aftermath of September 11, 2001); aid to veterans of the Iraq and Afghanistan wars (many of whom need health care and income support); education (with the federal government providing more resources to improve educational quality and outcomes); the Medicare prescription drug benefit (which Congress added in 2003); and health reform (which extends health coverage to tens of millions of Americans who would otherwise be uninsured and will increase federal spending, even though it will reduce the deficit).

- Spending for interest on the federal government’s debt also will be substantially higher in coming decades than it was during the past 40 years. By the end of 2010 — largely as a result of the wars in Iraq and Afghanistan, the large Bush-era tax cuts, and the current severe recession — debt held by the public will be nearly twice as large (as a percentage of GDP) as in 2001, with a commensurate increase in interest costs.

Simply put, aiming to stabilize the budget at the recent historical spending average of 21 percent of GDP might be appropriate for the years ahead if the age distribution of the population remained the same as it was in recent decades; if health care costs grew no faster than the economy; if Medicare had no drug benefit; if we were willing to leave more than 30 million Americans without health coverage; if there were no terrorist threats and hence no need for homeland security spending; if no wounded veterans of Iraq and Afghanistan needed medical care and income support; and if decisions and events over the last decade had not nearly doubled the national debt as a share of GDP. But that’s not the world in which we live, and it’s not the target at which we should aim.

Author and commentator Matt Miller has noted that federal spending under President Reagan averaged 22 percent of GDP — at a time when no baby boomers were retired and health care costs were more than one-third lower as a share of the economy than they are today. “As a matter of math,” Miller notes, “if you run the government at a smaller level than did Ronald Reagan while accommodating this massive increase in the number of seniors on our health and pension programs, you have to decimate the rest of the budget.”[3]

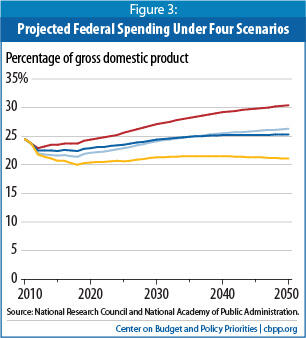

Indeed, when an expert committee on the deficit convened by the National Academy of Sciences and National Academy of Public Administration issued a major report earlier this year, it outlined four possible paths to stabilize the debt. Committee co-chair Rudolph Penner explained that the panel designed paths at two “extremes” — one that achieved nearly all its deficit reduction by cutting programs and another that got nearly all its deficit reduction by raising taxes — and two intermediate paths that blended program and tax changes. The extreme low-spending path included deep cuts in Social Security, Medicare, and Medicaid, and reductions of about 20 percent in all other spending, including defense, veterans programs, and the like. Under this extreme path, federal spending would be about 21 percent of GDP.

Meeting Longstanding Federal Commitments Will Cost More

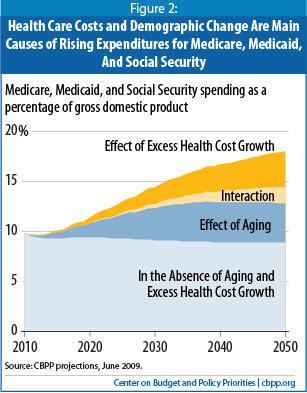

The two main sources of rising federal expenditures relative to GDP over the long run are rising per-person costs throughout the U.S. health care system (both public and private) and the aging of the population. Together, these factors will drive up spending for the three largest domestic spending programs: Medicare, Medicaid, and Social Security. Spending for all other federal programs is projected to shrink as a share of the economy in coming decades.

The U.S. population is growing older, which will add to the number of people eligible for Medicare, Medicaid, and Social Security over the next 25 years. As the members of the post-war Baby Boom (those born between 1946 and 1964) reach retirement, the fraction of the U.S. population ages 65 and over will grow by more than half — from 13 percent in 2010 to 20 percent by 2035 — and then level off at about that share. [5]

Rising health care costs account for the rest of the projected long-run growth. (See Figure 2.) For decades, costs per person throughout the health care system — both public and private — have been growing about 2 percentage points faster per year than GDP per person. Although the Affordable Care Act will slow this growth somewhat, health care costs will almost certainly continue to grow faster than GDP as continued medical breakthroughs occur that improve health and prolong lives but add to health care costs.

While Social Security will largely stop growing as a share of GDP after 2035, when the demographic shift is mostly complete, Medicare and Medicaid will continue rising because health care costs are projected to continue growing faster than GDP.

The Federal Government Has Taken On More Responsibilities

Another reason that the historical average level of federal spending is not an appropriate benchmark is that the federal government’s responsibilities have grown significantly in recent years. Since 2000, developments at home and abroad have pushed federal spending significantly above its average in earlier decades. Here are some examples:

- Homeland Security . Following the attacks of September 11, 2001, federal spending for homeland security increased significantly. Total homeland security budget authority has grown from $21 billion (0.2 percent of GDP) in fiscal year 2001 to $71 billion (0.5 percent of GDP) in 2010. [6]Imagen

- Veterans of Iraq and Afghanistan . The wars in Iraq and Afghanistan have increased the numbers of wounded veterans needing health care and income support. Budget authority for veterans’ benefits and services has grown from $45 billion (0.5 percent of GDP) in 2000 to $125 billion (0.9 percent of GDP) in 2010. [7]

- Education. With the No Child Left Behind Act of 2001, the College Cost Reduction and Access Act of 2007, and other legislation over the past decade, the federal government has taken a greater role in educating the future workforce to compete in the global economy. The federal government is providing more resources for public schools, tied to standards designed to improve educational quality and outcomes. Budget authority for elementary, secondary, and higher education programs has increased from $29 billion (0.3 percent of GDP) in 2000 to $60 billion (0.4 percent of GDP) in 2010.[8]

- Medicare Prescription Drug Benefit. The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 added a prescription drug benefit to the Medicare program. The drug benefit adds about 0.3 percent of GDP to federal spending in 2010 and more in later years.[9]

- Health Reform . The Affordable Care Act of 2010 extends health coverage to tens of millions of Americans who would otherwise be uninsured. CBO estimates that the new law will increase federal spending by about 0.4 percent of GDP after it is fully phased in. [10] CBO also estimates that the bill will reduce the deficit by $143 billion over its first ten years and roughly $1.3 trillion in the second decade. Under rules that seek to hold spending and revenues to historical averages, however, the fact that this legislation reduces the deficit would be ignored.

Federal Government Will Owe More Interest

In addition, spending for interest on the federal government’s debt will be substantially higher in coming decades than it was during the past 40 years. Over the 1970-2009 period, interest costs averaged just 2.2 percent of GDP, and debt held by the public averaged 36 percent of GDP. But by the end of 2010 — largely as a result of the wars in Iraq and Afghanistan, the large Bush-era tax cuts, and the current severe recession — debt held by the public will reach about 63 percent of GDP.

The Fiscal Commission has been charged by President Obama with developing a plan to reduce the deficit to about 3 percent of GDP around mid-decade. If that interim target is achieved, the debt would peak at slightly over 70 percent of GDP — a level twice as large relative to the economy as the average level that prevailed in 1970 through 2009. Interest costs would be commensurately higher. Once interest rates rise from today’s record-low levels, that debt level would imply interest costs of about 3.5 percent of GDP — more than a percentage point higher than the 1970-2009 average.

In short, the rising costs of Social Security and health care, new governmental responsibilities, and a larger debt-service burden all point to one clear conclusion: historical spending levels are not a realistic or appropriate goal for the future.

Reductions in Spending Alone Cannot Solve the Long-Term Problem

Although Medicare, Medicaid, and Social Security account for all of the projected increase in program spending relative to the size of the economy through 2050, cuts in these programs alone cannot realistically be expected to solve the long-term budget problem. [11] The growth of Medicare and Medicaid costs cannot be held below the growth of private-sector medical costs for very long without endangering access to medical care for low-income beneficiaries or shifting costs to private payers. Advances in medical technology will also make it difficult — and probably undesirable — to keep both private and public spending on health care from growing faster than the economy. As economic growth raises national income, Americans will likely want to devote a larger share of that income to medical advances that hold promise of improving health and prolonging life, but also entail new costs.

Similarly, there are limits to how much Social Security can be cut without undermining its crucial role in reducing poverty and replacing income lost when a wage earner retires, dies, or becomes disabled. Social Security benefits are quite modest, averaging only $1,170 a month (or $14,040 a year) for a retired worker. Social Security checks now replace about 39 percent of an average worker’s pre-retirement earnings — one of the lowest percentages of any western industrialized country — and that figure will gradually fall to about 32 percent over the next two decades, largely because of the scheduled increase in the full retirement age to 67.[12]

Prospects for deep reductions in other spending in coming years are also limited. Spending for programs besides the “big three” is already projected to decline as a percentage of GDP under current policies. Although cuts can doubtless be made in some individual programs, there will also be pressures to increase spending in areas of emerging national need, such as infrastructure investment, environmental protection, and medical and scientific research. “The rest of the outlay side of the budget is too small,” writes Martin Feldstein, chair of President Reagan’s Council of Economic Advisers, “to provide much scope for reducing annual budget deficits.”[13]

Under the committee’s extreme low path that secured almost all of its deficit reduction through budget cuts, federal spending would be about 21 percent of GDP. The 21-percent-of-GDP path included the following measures.

- Large cuts in Social Security benefits . The full retirement age would be increased to 67 by 2017 and further increased by one month every two years thereafter; for new retirees, benefits would also be reduced below the levels scheduled under current law for all but the poorest 30 percent of earners; and benefits would grow more slowly after initial receipt. By 2050, the benefit of a newly retired worker with average earnings would be 27 percent lower than the benefit scheduled under current law.[16]

- Unspecified policies to hold the growth of Medicare and Medicaid costs per beneficiary to the same rate as the growth of GDP per capita, even as general health care costs continue to rise more rapidly. Compared to current law, expenditures for Medicare and Medicaid would be cut 20 percent by 2025 and over 40 percent by 2050. The committee observed, “This steep, sustained slowdown of spending growth is possible only under a regime of tough cost controls in at least the near and medium term. Many analysts would consider this trajectory to be politically unrealistic. It also may be regarded as implausible to the extent that competing policy objectives of expanding access to care and improving quality are taken seriously.” [17] The only way of achieving this outcome would likely be to replace Medicare’s guaranteed benefit with a voucher, and Medicaid with a block grant, whose value would grow much less rapidly than the actual cost of health care, thus subjecting Medicare and Medicaid beneficiaries to cuts in health care services that would grow larger each year.

- Cutting all other programs (other than Social Security, Medicare, and Medicaid) by about 20 percent overall. If some large parts of the budget — like defense and veterans’ programs — were cut substantially less than 20 percent, or if new programs were needed, other parts of the budget would have to be cut much more severely.

In the committee’s three other illustrative paths, spending and revenues would exceed their averages over the decades since 1970. In the path that accomplished most of its deficit reduction through revenue increases, total spending (including interest) would reach 26 percent of GDP by 2025 (and 30 percent of GDP by 2050). In the two intermediate paths spending would total 23 percent of GDP in 2025 (and 25 or 26 percent of GDP in 2050). The committee noted that even the intermediate paths required instituting major budget cuts to hold spending well below the levels that would be reached under a continuation of current policies.

Historical Average Revenues Generated Chronic Deficits

Like the historical average level of spending, the historical average level of revenues does not provide a reasonable benchmark for the future. Revenues at the historical average level were not sufficient to support essential public services over the past 40 years, and they will be even less adequate in the face of future challenges, with an older population and a health care system that has made major advances in medical treatment but has higher costs.

The historical record shows a persistent mismatch between revenues and the funding needed for public services. Revenues at the 40-year average — a little over 18 percent of GDP — would not have balanced the budget in any of the last 40 years. The only balanced budgets over this period occurred from 1998 through 2001, years in which revenues were markedly above the 40-year average. Revenues in these years were in the 20-to-21-percent-of-GDP range. As a result of this mismatch between revenues and funding needs, the government ran deficits that averaged 2.6 percent of GDP over the past 40 years.

Maintaining revenues at their historical levels would almost certainly require either massive deficits or abandoning commitments to the elderly and the poor and shortchanging investment in areas important to economic growth, such as infrastructure, education, and basic research. If revenues return to their historical average after the recession, and if current program policies are maintained, the mismatch between the federal government’s revenues and its obligations will become huge. Deficits would rise to more than 20 percent of GDP by 2050, and the debt would exceed 300 percent of GDP. Stabilizing the debt-to-GDP ratio almost entirely through cuts in programs, however, would require deep cuts in Social Security, Medicare, and Medicaid — which would cause large increases in poverty and hardship among the nation’s senior citizens and children — and sharp reductions in discretionary spending that would put needed investments at risk.

Arbitrary Budgetary Targets Are Misguided

The bottom line is that arbitrary numerical targets for federal spending and revenues are misguided. Although history provides useful information and guidance, it should not be a straitjacket. What will be appropriate in 2020, 2030, or 2050 is not necessarily the same as in 1970 or 1980. Budgetary policies, like other policies, must respond to changing circumstances. “As our cause is new,” wrote Abraham Lincoln, “so we must think anew, and act anew.”[18]

Determining the appropriate levels of federal spending and revenues requires making a thoughtful assessment of national needs and weighing the benefits of federal spending programs and tax expenditures against each other and against the costs of the taxes to pay for them. Limiting spending and revenues to their historical average or another inflexible target would prevent these trade-offs from being made. For example, it would make it impossible to create a highly beneficial spending program that would be fully paid for by closing an egregious tax loophole. In our view, the aging of the population, the continued importance of Social Security and Medicare, the growth in federal responsibilities in recent years in areas such as homeland security, and rising health care costs justify higher levels of federal spending and revenues over the next 40 years than over the past four decades.

End Notes

[1] Brian M. Riedl, The Three Biggest Myths About Tax Cuts and the Budget Deficit, Heritage Foundation, June 21, 2010, Backgrounder No. 2423.

[2] David Broder, “Outside Washington, feeling hopeful on the budget crisis,” Washington Post, July 15, 2010.

[3] Matt Miller, “A pending goal too small for aging America,” Washington Post, January 28, 2010.

[4] Kathy Ruffing, Kris Cox, and James Horney, The Right Target: Stabilize the Federal Debt, Center on Budget and Policy Priorities, January 12, 2010. The projections do not include the effects of the Affordable Care Act.

[5] Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, 2009 Annual Report, Table V.A2, page 85.

[6] Congressional Budget Office, Federal Funding for Homeland Security, April 30, 2004; Budget of the United States Government, Fiscal Year 2011, Analytical Perspectives, “Homeland Security Funding Analysis,” Chapter 23.

[7] Budget of the United States Government, Fiscal Year 2011, Historical Tables , Table 5.1.

[8] Ibid.

[9] CBO estimate of net spending for Part D of Medicare less CBPP estimate of reduction in Medicaid spending.

[10] Douglas W. Elmendorf, Director, Congressional Budget Office, Letter to the Honorable Nancy Pelosi, March 20, 2010.

[11] Ruffing, Cox, and Horney, The Right Target.

[12] Virginia P. Reno, Building on Social Security’s Success, Economic Policy Institute Briefing Paper 208 (November 2007). These replacement rates are net of premiums for Part B of Medicare, which are deducted from most Social Security checks.

[13] Martin Feldstein, “The ‘Tax Expenditure’ Solution for Our National Debt,” Wall Street Journal, July 20, 2010.

[14] National Research Council and National Academy of Public Administration, Choosing the Nation’s Fiscal Future, Washington: National Academies Press, 2010.

[15] Rudolph G. Penner, Statement before the Senate Budget Committee, February 11, 2010.

[16] Choosing the Nation’s Fiscal Future , Appendix C.

[17] Ibid. , p. 79.

[18] Abraham Lincoln, Message to Congress, December 1, 1862.

Más de los autores