Gap Between Trump, CBO Predictions on Economic Growth the Largest on Record

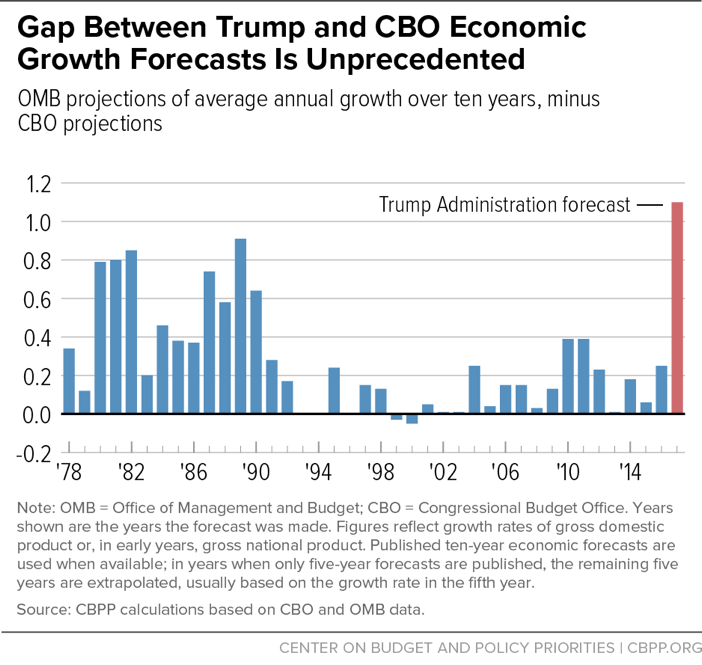

President Trump’s fiscal year 2018 budget is predicated on the assumption that the economy will expand at 2.9 percent per year, on average, over the 2018-2027 decade — 1.1 percentage points per year more than the Congressional Budget Office (CBO) assumes. This large a gap between an administration’s growth forecast and CBO’s is unprecedented. This large a gap between an administration’s growth forecast and CBO’s is unprecedented, CBPP analysis finds (see Figure 1). Because of its rosy growth forecast, the Trump budget projects cumulative deficits over the next decade that are roughly $3 trillion less than they would be using CBO’s forecast.[1] Unrealistic growth projections not only make deficit-increasing tax cuts appear more affordable than they actually are, but could also add to pressure for cuts in programs for low- and middle-income families if the promised growth fails to materialize.

New Estimates Compare President’s Budget Growth Projections and CBO’s

In 2015, CBO published an analysis of its forecasting record that included a comparison of its five-year economic projections from each year since 1976 with those in the President’s budget and with the subsequent actual economic outcomes.[2] For most of this period, economic and budget projections only went out five years, but ten-year projections are now the norm.

CBPP has therefore updated CBO’s analysis by extending the original five-year projections forward another five years, generally by extrapolating from the growth assumption in the fifth year of the original forecast, and by including forecasts released in the years since CBO’s analysis was published. As Figure 1 shows, the 1.1 percentage-point gap between the Trump forecast and CBO’s is the largest for which published CBO forecasts are available and is far larger than any gap since the Reagan-Bush era.[3] Between 1993 and 2016, the largest gap between the Administration and CBO forecasts was 0.4 percentage points; the typical gap was less than 0.2 percent.

CBO’s Five-Year Forecasting Errors Smaller than Those of Presidential Budgets

CBPP has also updated CBO’s 2015 five-year forecast analysis by adding three more years of forecasts that can be compared with actual outcomes. That comparison indicates that when Administration forecasts have been particularly optimistic, actual economic growth turned out substantially lower than the Administration forecast.

In particular,

- Both the Administration and CBO five-year growth estimates tended to be too optimistic, with the Administration estimates somewhat more optimistic than CBO’s. Actual economic growth has come in about 0.6 percentage points per year lower than Administration estimates and 0.4 percentage points lower than the CBO estimates, on average.

- In 11 years, the Administration’s five-year growth estimate exceeded CBO’s by 0.5 percentage points or more, and every single time, actual economic growth turned out lower — usually far lower — than the Administration projections. In other words, whenever the Administration projections were particularly optimistic relative to CBO’s, the Administration projections turned out to overstate actual growth, typically by a wide margin. The Trump budget growth forecast exceeds CBO’s by an average of 0.8 percentage points a year over the next five years.

Administration forecasts that turn out to be excessively optimistic can be rooted in optimism about how fast the economy can recover from a recession or how fast the economy’s capacity to supply goods and services is expanding. With the economy already close to full employment, both five-year and ten-year Trump growth forecasts primarily reflect unrealistic expectations about the latter (see box).

Budget Implications

Large differences in growth assumptions can have large budgetary effects. All else being equal, each 0.1 percentage-point increase in the average annual growth rate over a decade lowers cumulative projected budget deficits by about $300 billion, analyses by CBO and the Office of Management and Budget (OMB) indicate. Thus, the 1.1 percentage-point gap between the Administration and CBO ten-year growth forecasts lowers projected cumulative budget deficits by roughly $3 trillion compared with what they would be using CBO’s growth assumptions.[4] This figure should not be confused with the $2.1 trillion of lower deficits the Administration attributes to “economic feedback” effects because OMB uses baseline assumptions that are different from CBO’s.

When CBO analyzes the President’s budget in coming months, many factors besides different projections of economic growth will contribute to the difference it finds between the deficits in the President’s budget and in its own baseline budget projections. First, CBO’s forecast will assume that current laws and policies remain in place, while the President’s budget incorporates estimates of how his policy proposals will affect the economy. Second, CBO’s forecast will include assumptions about other economic variables, including inflation and interest rates, that also affect revenue and spending projections, and hence the deficit. Finally, CBO and OMB can differ in the non-economic and program-specific technical assumptions they use to project revenues and spending.

Nevertheless, the President’s reliance on excessively optimistic growth projections has several negative implications, besides underestimating likely deficits. First, rosy economic assumptions obscure the effects of tax cuts on deficits and debt, making it easier for the President to argue for large tax cuts for the wealthy and corporations — thereby squandering national resources better used to help struggling families or invest in high-priority programs. Also, the emergence of larger deficits than predicted would likely prompt policymakers to further cut programs that help low- and middle-income families, or perhaps even raise taxes on them.

Thus, even if the Administration’s tax plan provides a tax cut to working and middle-income families, the larger deficits that will emerge if growth falls short of the Administration’s rosy projections could lead to further damaging cuts to programs that help them, leaving those families worse off in the end.

Why Forecasts Can Differ

Five-year economic forecasts can sometimes be dominated by business-cycle considerations. When the economy has just entered or is just beginning to recover from a recession, forecasters may differ over how fast it will recover. When the economy is closer to full employment, and over the longer term, however, a forecast is determined largely by the forecaster’s estimate of how fast the labor force and productivity (output per hour worked) will increase.

CBO estimates that the economy is now close to full employment and that any “slack” in productive capacity due to excess unemployment or underutilized capital services from existing machines, factories, offices, and stores will be squeezed out of the economy by the end of next year. Thus, the difference between the Trump and CBO five- and ten-year forecasts primarily reflects different assumptions about how much slack is left before bumping up against capacity constraints or how fast the economy can grow when it is operating at full capacity. Long-term trends in productivity are difficult to predict accurately, and differences in these projections are an important source of past differences in projections of longer-term economic growth. That said, most economists think the Trump forecast is far too rosy in its growth projections.a

a Chad Stone, “In Forthcoming Trump Budget, Rosy Forecasts of Economic Growth Likely to Produce Highly Unrealistic Budget Estimates,” Center on Budget and Policy Priorities, May 3, 2017, https://www.cbpp.org/research/federal-budget/in-forthcoming-trump-budget-rosy-forecasts-of-economic-growth-likely-to.

End Notes

[1] Chad Stone, “In Forthcoming Trump Budget, Rosy Forecasts of Economic Growth Likely to Produce Highly Unrealistic Budget Estimates,” Center on Budget and Policy Priorities, May 3, 2017, https://www.cbpp.org/research/federal-budget/in-forthcoming-trump-budget-rosy-forecasts-of-economic-growth-likely-to.

[2] “CBO’s Economic Forecasting Record: 2015 Update,” Congressional Budget Office, February 2015, https://www.cbo.gov/publication/49891. CBO’s analysis begin in 1976 because that is the year in which CBO began issuing these projections on a regular basis.

[3] Years shown in the chart are the years the forecast was made, for the budget year beginning in October. Thus, the 2017 Trump forecast is for the fiscal year 2018 budget.

[4] Stone, op. cit.

Más de los autores