Statement by Chad Stone, Chief Economist, on the September Employment Report

Today’s generally solid report shows that employers are back on track creating more than 200,000 jobs a month after a dip in August (see chart). Nevertheless, the economy has substantial room for further expansion, allowing the Federal Reserve to keep interest rates low to spur higher employment without igniting unacceptable inflation. Moreover, policymakers should not worry about inflation even if wages begin to grow faster than they have so far in the recovery.

The litany of labor market indicators with further room for improvement — that is, “slack” — is well known. At 5.9 percent, the unemployment rate remains about a half point higher than the Fed’s and most other analysts’ estimates of the lowest sustainable rate that we could achieve. Many people who want to work and would be working if the labor market were stronger have stopped looking until their job prospects improve, so they are not counted among the unemployed. Indeed, the labor force shrank in September, contributing to the fall in unemployment. In addition, many people working part-time jobs would prefer full time work if it were available.

Under these conditions, employers have faced little pressure to raise wages. Moreover, a significant share of the wage increases that they’ve provided has been offset by increases in workers’ productivity (output produced per hour worked). Together, the modest wage increases and ongoing productivity gains have kept increases in employers’ labor costs per unit of output very modest. Consequently, employers have been able to widen their profit margins significantly, even in the face of weak demand for goods and services that limited their ability to raise prices. Labor compensation has fallen as a share of total income while the share going to profits has risen.

As the jobs recovery continues and labor market “slack” shrinks, employers may have to start providing larger wage increases to attract the workers they need. But as long as those wage increases are offset partly by productivity growth and partly by a return to more normal profit margins, inflation should not rise beyond what the Fed should be willing to tolerate.

Strong demand for goods and services is the cure for labor market slack and sluggish wage growth. To achieve that, the Fed must not raise interest rates too quickly and lawmakers must eschew near-term budget cuts that would stifle economic growth.

About the September Jobs Report

Employers reported solid payroll growth in September. In the separate household survey, the unemployment rate fell to 5.9 percent, but some of the decline resulted from labor force attrition, not employment growth. Average hourly earnings were essentially unchanged.

- Private and government payrolls combined rose by 248,000 jobs in September and the Bureau of Labor Statistics revised job growth in the previous two months upward by a total of 69,000 jobs. Private employers added 236,000 jobs in September, while overall government employment rose by 12,000. State government employment rose by 22,000, while federal government fell by 2,000 and local government fell by 8,000, despite a gain of 6,000 local education jobs.

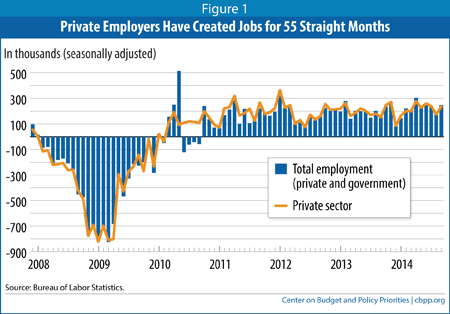

- This is the 55th straight month of private-sector job creation, with payrolls growing by 10.3 million jobs (a pace of 188,000 jobs a month) since February 2010; total nonfarm employment (private plus government jobs) has grown by 9.8 million jobs over the same period, or 178,000 a month. Total government jobs fell by 557,000 over this period, dominated by a loss of 322,000 local government jobs.

- The job losses incurred in the Great Recession have been erased. There are now 1.6 million more jobs on private payrolls and 1.1 million more jobs on total payrolls than at the start of the recession in December 2007. Because the working-age population has grown since then, however, the number of jobs remains well short of what is needed to restore full employment. Employers have expanded their payrolls at a 237,000-a-month pace this year, and such growth must continue to restore normal labor market conditions in a reasonable period of time.

- Average hourly earnings on nonfarm payrolls fell by a penny in September to $24.53. Over the last 12 months they have risen just 2.0 percent. For production and nonsupervisory workers, average hourly earnings remained $20.67, or 2.3 percent higher than 12 months earlier.

- The unemployment rate fell to 5.9 percent in September, and 9.3 million people were unemployed. The unemployment rate was 5.1 percent for whites (0.7 percentage points higher than at the start of the recession), 11.0 percent for African Americans (2.0 percentage points higher than at the start of the recession), and 6.9 percent for Hispanics or Latinos (0.6 percentage points higher than at the start of the recession).

- The recession drove many people out of the labor force, and the ongoing lack of job opportunities has kept many potential jobseekers on the sidelines and not counted in the official unemployment rate. This problem remained evident in September. The labor force shrank by 97,000 people, as the increase in employment of 232,000 people fell short of the decline in unemployment of 329,000 people. (Data on the number of people with a job and the number of jobs on employers’ payrolls come from separate surveys.)

- As a result of the decline in the labor force, the labor force participation rate (the share of the population aged 16 and over in the labor force) edged down to 62.7 percent in September. While the sharp decline in labor force participation during the recovery has abated, September’s rate is the lowest since 1978.

- The share of the population with a job, which plummeted in the recession from 62.7 percent in December 2007 to levels last seen in the mid-1980s and has remained below 60 percent since early 2009, was 59.0 percent in September. It has been at that level for the last four months.

- The Labor Department’s most comprehensive alternative unemployment rate measure — which includes people who want to work but are discouraged from looking (those marginally attached to the labor force) and people working part time because they can’t find full-time jobs — edged down to 11.8 percent in September. That’s well down from its all-time high of 17.2 percent in April 2010 (in data that go back to 1994) but still 3.0 percentage points higher than at the start of the recession. By that measure, about 18½ million people are unemployed or underemployed.

- Long-term unemployment remains a significant concern. More than three in ten (31.9 percent) of the 9.3 million people who are unemployed — 3.0 million people — have been looking for work for 27 weeks or longer. These long-term unemployed represent 1.9 percent of the labor force. Before this recession, the previous highs for these statistics over the past six decades were 26.0 percent and 2.6 percent, respectively, in June 1983, early in the recovery from the 1981-82 recession. A year after peaking at 2.6 percent, however, the long-term unemployment rate had dropped to 1.4 percent, well below the current rate.

Más de los autores