más allá de los números

Ways and Means Bills Would Expand HSA Tax Breaks, Weaken Insurance Marketplaces

The House Ways and Means Committee is marking up several bills this week that would raise contribution limits for health savings accounts (HSAs) and expand the allowable uses of these accounts, at a cost of $41 billion over ten years, the Joint Committee on Taxation (JCT) estimates. As we’ve written, expanding HSAs would mostly benefit high-income taxpayers while doing little to help moderate-income families or the uninsured. The bills also include other problematic provisions providing premium tax credits to people who buy plans offered outside the Affordable Care Act (ACA) marketplaces and delaying the ACA’s excise tax on high-cost plans, among other things. In all, the bills would cost $92 billion over the next decade, though interactions among them could raise or lower that figure.

People with a high-deductible health plan (that is, with a deductible of at least $1,350 for individuals and $2,700 for families) can now create an HSA to save for out-of-pocket health expenses. HSAs already offer tax-sheltering opportunities, enabling taxpayers to: (1) make tax-deductible contributions of up to $3,450 a year for individuals and $6,900 for families; (2) put their contributions in stocks, bonds, or other investments, with the earnings accruing tax free; and (3) make tax-free withdrawals if they use the money for out-of-pocket medical costs or long-term care.

No other savings vehicle offers all three tax benefits. For example, 401(k) contributions and earnings are tax-free but withdrawals are taxed. Moreover, there are no income limits on HSA participation, so affluent people who have “maxed out” their individual retirement account and 401(k) contributions can use HSAs to shelter more funds.

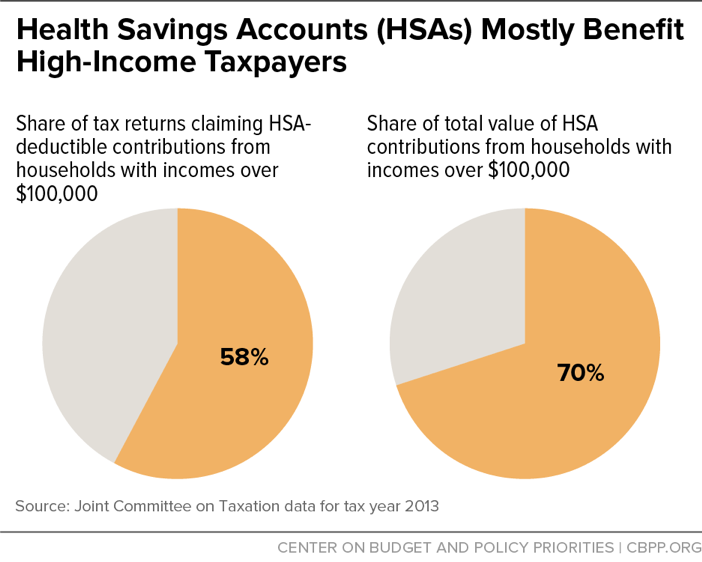

HSAs mainly benefit high-income people, for two reasons. First, high-income people can best afford to save for health care expenses and are therefore the most likely to contribute to HSAs. This explains why higher-income filers are much likelier to establish HSAs than lower-income filers, why they’re likelier to max out their contributions, and why 70 percent of HSA contributions come from households with incomes over $100,000, according to JCT (see chart). Second, high-income people receive the biggest tax benefit for each dollar contributed to an HSA because the value of a tax deduction rises with an individual’s tax bracket.

The main — and costliest — of the bills to expand HSAs (H.R. 6306) would nearly double the annual contribution limits, to $6,650 for individuals and $13,300 for families. That would tilt HSAs’ tax benefits even more toward the top because only people who are wealthy enough to max out their contributions under the current limits would benefit. This and related changes would cost $15 billion between 2019 and 2028, JCT estimates. And the cost would likely grow over time because much of the cost associated with HSAs occurs when people make tax-free withdrawals from the accounts in retirement — in lieu of sources that are taxable — to pay for medical and long-term care.

Costly provisions of other bills would allow Medicare beneficiaries to contribute to HSAs (H.R. 6309) and allow accountholders to use HSA funds for things other than medical care, such as gym memberships and cycling classes (H.R. 6312).

Another bill before Ways and Means (H.R. 6311) would likely reduce choice and competition in the ACA marketplaces. It would allow people buying individual-market plans outside the ACA marketplaces to receive ACA tax credits, although the credits would only be available when they file their tax returns the following year, not up front to help them pay premiums. And it would eliminate the requirement that insurers, in order to sell plans eligible for the ACA tax credit, must offer at least one “silver” and one “gold” plan through the marketplace. If this bill were enacted, an insurer could offer coverage only outside the marketplace while still giving consumers access to premium tax credits.

Reducing the incentives for insurers to offer marketplace coverage could make it easier for insurers to engage in strategies to attract only healthier enrollees, such as offering only bronze or catastrophic plans, which have higher deductibles and other cost-sharing expenses for consumers than silver and gold plans. It also could reduce plan choices for consumers within the marketplaces, if insurers shift to off-marketplace business. And it could prompt fewer consumers to comparison shop in the marketplaces, where they can compare premiums and benefits for multiple insurers, thus reducing competitive pressure on insurers to hold down premiums.