más allá de los números

Remaining States Should Opt Out of Costly Corporate Tax Break

I listed four reasons recently why states shouldn’t cut their corporate income taxes. In a new paper, I describe a tax change that they should make: cancel a corporate tax break that costs them hundreds of millions of dollars each year.

The federal government created the tax break, known as the “domestic production deduction,” in 2004. Since most states’ tax codes are tied to the federal tax code, the deduction took effect automatically in most states as well, without policymakers’ explicit approval — or even their knowledge in many cases.

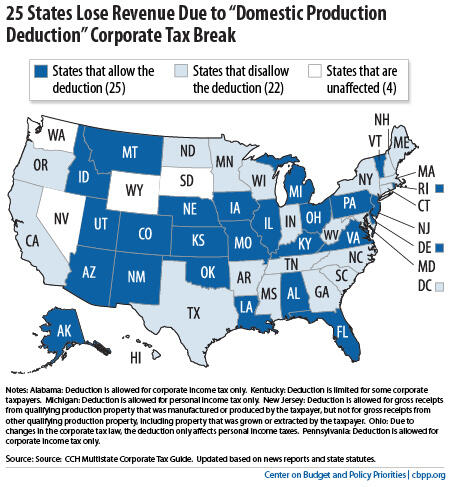

Twenty-two of the 46 states with a corporate income tax (including the District of Columbia) have since “decoupled” their tax codes from the deduction, but 25 haven’t (see map). The revenue loss to states that still allow the deduction has grown steeply over the past few years. By 2014, the deduction will cost them over $600 million per year.

There is no good reason to accept such revenue losses. The deduction:

- is unlikely to protect or create jobs within a particular state because multi-state corporations can claim it for “productive activities” in any state;

- gives little or no help to financially ailing businesses, since only profitable firms have taxable income for it to offset;

- is heavily slanted towards large corporations: in 2009, more than 90 percent of the tax benefits went to firms with assets over $100 million apiece; and

- most importantly, makes less and less sense given the large cuts that most states have had to make in education, healthcare, and many other critical services.

To decouple from the deduction, a state need only add a single sentence to its tax law. That’s a simple change — and a smart one.