más allá de los números

Light at the End of the Tunnel for State and Local Pensions?

The news for the last several years about underfunded pension programs for teachers, nurses, and other state and local workers has been bad. But that may be changing.

The stock market’s rebound from its depths in the recession has lifted pension assets substantially over the past two and half years, Federal Reserve data show. The most recent data show assets at the end of 2011 were $680 billion more than in early 2009 (see Table L.119 here).

The effects of the recovering market haven’t yet shown up in most state pension funds’ financial reports, but they will over the next few years. When most funds estimate their available assets, they phase in the impact of investment gains and losses over several years in order to minimize year-to-year changes in the amount of money that the state must deposit in the fund.

Also, states have taken a number of steps since 2009 to improve their pension systems’ fiscal health. Forty-three states have made changes in the last three years, according to the National Conference of State Legislatures: 30 states have upped employee contributions, for example, and more than 30 states have reduced benefits. These changes and other factors have slowed the growth in pension costs.

It will take time for pension reforms and an improving market to have their full impact on pension trust funds. But a new report from the Center for Retirement Research at Boston College suggests that states might not have to wait too much longer.

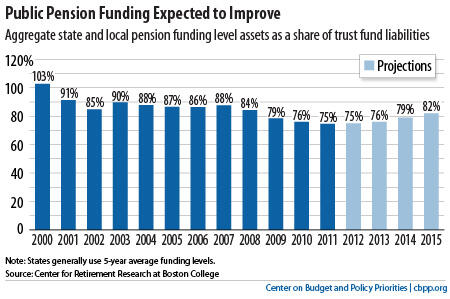

The report finds that the funding ratio — a comparison of the assets in state and local trust funds to the estimated cost of providing future benefits — likely stopped falling in 2012 and will slowly begin to recover over the next few years (see graph). These figures are based on pensions’ standard method of calculating the cost of future benefits, which is to use the historical average return on pension plans’ assets (roughly 8 percent) to discount future costs. (Some analysts believe that a lower discount rate should be used, however, which would result in lower reported funding ratios.)

Under what they consider the most likely scenario for future growth in the stock market and the economy, the Boston College researchers project that state and local pension trust funds will be large enough by 2015 to cover 82 percent of future liabilities. Many experts consider a funding ratio of 80 percent or higher to be adequate.

To be sure, that 82 percent is just a projection, which assumes continued growth in the stock market and future returns on pension-plan assets close to the historical average. In addition, the 82 percent figure is a national average, so some states will be above that figure and some will be below it — a few state and local pension plans will remain seriously underfunded.

As we’ve explained, restoring pensions to full health is a long-term goal that states should address with well-thought-out measures, not an immediate crisis that requires drastic action. By relying on common-sense reforms and taking the long-term view, states and localities can restore pension systems to fiscal heath without undermining their employees’ retirement security or their ability to fund education, health care, infrastructure, and other public services necessary for long-term prosperity.