más allá de los números

Health Reform Strengthens Medicare, Doesn’t “Rob” It

The 2010 health reform law (the Affordable Care Act, or ACA) has significantly improved Medicare’s long-term financial outlook, as we have previously pointed out. Recent claims that health reform “robs Medicare” and does not “shore up Medicare’s finances” are flatly false, as the recent report of the program’s trustees shows.

The Congressional Budget Office estimates that the ACA will reduce Medicare’s projected spending by $716 billion over the 2013-2023 period. As John McDonough of Harvard’s School of Public Health explains: “None of these reductions were financed by cuts to Medicare enrollees' eligibility or benefits; benefits were improved in the ACA. Cuts were focused on hospitals, health insurers, home health, and other providers.”

Medicare’s trustees confirm that health reform has improved the program’s finances: “The financial status of the HI [Hospital Insurance] trust fund was substantially improved by the lower expenditures and additional tax revenues instituted by the Affordable Care Act.” (See page 4 here.)

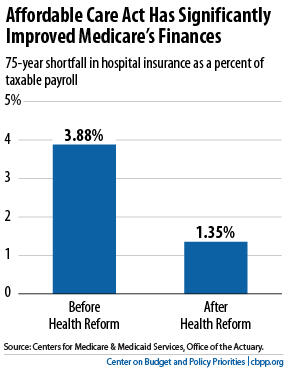

In their annual report issued this spring, the trustees estimate that the Medicare hospital insurance program now faces a shortfall over the next 75 years equal to 1.35 percent of taxable payroll — that is, 1.35 percent of the total amount of earnings that will be subject to the Medicare payroll tax over this period. This is much less than the size of the shortfall that the trustees estimated before the enactment of health reform: 3.88 percent of taxable payroll (see chart).

The trustees also find that the HI trust fund will remain solvent — that is, able to pay 100 percent of the costs of the hospital insurance coverage that Medicare provides — through 2024. If health reform were fully repealed, however, as the House of Representatives has voted to do, the Centers for Medicare & Medicaid Services estimates that the Medicare hospital insurance program would become insolvent eight years earlier, in 2016.

These projections underscore the importance of successfully implementing the cost-control provisions in the Affordable Care Act. While history shows that most major Medicare savings measures have been implemented as scheduled, Medicare’s chief actuary has expressed concern that some of the ACA’s savings provisions may not be sustainable. The actuary urges reliance instead on an “illustrative alternative” projection, which assumes that only 60 percent of the ACA’s Medicare savings will actually be achieved in the long run. Even under this alternative projection, the projected insolvency date of the Hospital Insurance trust fund remains at 2024. To be sure, the 75-year shortfall in the Medicare trust fund would rise to 2.43 percent of payroll under the alternative projection, but this still is a dramatic improvement over the outlook without the Affordable Care Act.

Claims that the health reform law weakens Medicare’s finances are far off base. The truth is that the ACA strengthens the program.