Phasing in State Tax Cuts Doesn’t Make Them Fiscally Responsible

Some states in recent years have enacted deep cuts in income taxes that phase in over several years rather than take effect all at once. Eleven states[1] have enacted large, phased-in cuts in corporate or personal income taxes since 2011 that will cost a combined $8 billion a year once fully implemented.[2] A number of these tax cuts will come on top of other large income tax cuts the state has already implemented. Phasing in deep tax cuts can create major structural problems in state revenue systems.Phasing in policy changes over time can be prudent in some cases, but phasing in deep tax cuts can create major structural problems in state revenue systems, weakening states’ ability to support a strong education system and other essential public services that provide a foundation for future prosperity.

Large income tax cuts that phase in over time:

- Are typically enacted without the basic information needed to determine if they are affordable. The 11 states that adopted phased-in tax cuts in recent years did so largely without information critical to assessing the likely impact on the state’s ability to provide services. None of them produced a careful estimate of the cost of providing existing services — taking into account caseload or enrollment changes, inflation, and any pending rule changes — over the tax cuts’ full phase-in period, leaving policymakers in the dark as to whether the tax cuts will force future legislatures to reduce services in ways that harm the state’s people and diminish its economy.

-

Can create structural problems for state budgets. Since lawmakers often adopt large, phased-in tax cuts not knowing whether or not they will be affordable, and since large tax cuts sharply reduce state revenues, they can lead to major structural problems for state budgets, or the chronic inability of revenues to grow in tandem with economic growth and the cost of government. Because of states’ balanced-budget requirements, major revenue losses force states to cut services, raise other revenues, or both.

For example, in Arizona, which is phasing in large corporate income tax cuts, general state funding per student for K-12 schools is down 13 percent since before the Great Recession took hold, after adjusting for inflation, and average tuition at four-year public colleges and universities has soared by 88 percent to offset a steep decline in state support. And since Kansas started phasing in large tax cuts, it has cut funding for services multiple times, drained its operating reserves, raised sales tax rates, and shifted funds away from planned transportation projects to pay for the immediate needs of schools and other services. The tax cuts also helped spark a budget crisis that forced Kansas to slow the phase-in.

The structural problems created by phasing in tax cuts add to existing difficulties in many states due to long-term trends that are causing revenues to fall behind the cost of services. These trends include the shift in household purchases toward services (which are largely untaxed) and online sales (many of which are effectively untaxed), the tendency of health-care costs to grow faster than other expenses, and the need to make long-deferred investments in schools, roads, and other forms of critical public infrastructure.

- Enable lawmakers to avoid accountability. Policymakers can immediately claim credit for voting for tax cuts that — given state balanced-budget requirements — would force politically unpopular service cuts if they took effect in the near term, and gamble that the cuts will not harm public services or the state’s financial stability down the road. Enacting tax cuts that will begin and/or continue beyond the budget period also increases the odds they will take precedence over spending needs and priorities at the time they take effect.

- Often shift costs away from the wealthy to middle- and low-income residents. By making income tax cuts easier to enact, delayed effective dates promote the shifting of tax responsibilities from wealthy residents to less-affluent ones. Income taxes require more of wealthier residents than middle- and low-income families, while the opposite is true for the other major state taxes, such as sales and excise taxes. As a result, when states cut income taxes they shift the cost of state services away from the rich and toward the middle class and poor.

- Are hard to reverse. Proponents respond to criticisms of phased-in tax cuts by noting that future policymakers can always reduce, postpone, or cancel them. It is true that a future effective date in tax cut legislation constitutes a political obstacle to setting different priorities, not a legal one. But at a time when a large number of state lawmakers have signed public pledges never to vote for a tax increase — and many who haven’t are concerned that voting to scale back or suspend a scheduled tax cut would open them to attack for raising taxes, it is a significant obstacle. The political difficulties are especially challenging in the 16 states that require a supermajority vote to raise taxes.[3]

- Offer no meaningful benefits compared with deferring action on tax cuts until closer to the implementation date, when policymakers will know more about whether they are affordable. At any future point when lawmakers decide that tax cuts are affordable and/or a priority, they can be put into effect quickly. While knowing future tax rates may help individuals and businesses decide whether to make certain long-term investments, these benefits are likely quite limited when it comes to state taxes. State personal and corporate income tax rates are relatively low to begin with and thus unlikely to tip investment decisions. Also, most of the phased-in tax cuts enacted in recent years involve personal income taxes, and only a small minority of income tax payers are business owners making significant capital investment decisions.

Proposals to phase in deep tax cuts are often based on the misleading claim that states can cut taxes significantly without undermining their ability to continue funding services as long as they cut taxes gradually over time. This claim ignores the fact that the cost of providing a given level of services rises over time due to inflation, population growth, and other factors. Phasing in tax cuts offers the appearance of prudence even when the tax cuts are fiscally irresponsible.

States considering phased-in tax cuts should therefore evaluate carefully the cost and consequences. To help with this, they could implement a “pay-as-you-go rule” requiring any new tax cut to be paid for through an increase in other taxes and/or reduction in spending.[4]

More States Phasing in Large Tax Cuts

After the 2010 election, a number of governors and legislative leaders pushed for major income tax cuts. Governors in Kansas, Louisiana, Maine, Nebraska, and other states even called for eliminating the personal income tax, though it is the largest single funding source for state services in most states.

Some of these proposals failed. For example, in 2013, Louisiana Governor Bobby Jindal floated a plan to phase out the personal and corporate income taxes in exchange for expanding the sales tax base, but scrapped his plan due to widespread opposition. The plan, which heavily favored the state’s richest residents, likely would have forced cuts in public services over time, and it imposed sales taxes for the first time on some business services, dooming it with multiple constituencies.[5]

Other proposals were enacted. The most aggressive income tax cut, in Kansas, eliminated income taxes on certain forms of businesses and phased in a cut in personal income tax rates.[6] The nearly immediate loss of hundreds of millions of dollars in revenue led to an ongoing fiscal crisis, the use of various imprudent budget gimmicks to hide the damage, and multiple credit-rating downgrades for the state, while failing to give the state economy a meaningful boost.[7] These impacts made Kansas a cautionary tale for other states seeking to eliminate personal and business income taxes.

More recently, state lawmakers have typically avoided large tax cuts that take effect immediately, seeking instead to phase them in over time. (In some cases, these tax cuts will only be “triggered” if certain conditions are met, an approach discussed in a companion paper.[8] This paper covers only recent tax cuts that are phased in but not triggered.)

Eleven states have enacted personal or corporate tax cuts since 2011 that will phase in over time regardless of conditions or the state’s evolving needs.[9] (See Table 1.) The largest, relative to the state’s budget, is Mississippi’s, which will cut state revenue by roughly 7 percent once fully implemented. New York’s phased-in tax cut is the largest in dollar terms, with an annual cost over $4 billion once fully implemented.

A number of these phased-in tax cuts will come on top of other large income tax cuts the state has already implemented. For example, Arizona, New Mexico, and Ohio began long-term efforts to cut individual and corporate income taxes in the early to mid-2000s before adding the latest round of phased-in tax cuts.[10] More recently Indiana, Kansas, Mississippi, and North Carolina passed immediate tax cuts as well as long-term phase-ins. Just the phased-in tax cuts in these 11 states —not including the immediate tax cuts — will cost roughly $8 billion a year once fully implemented.[11]

| TABLE 1 | |||||

|---|---|---|---|---|---|

| Phased-In Cuts to Corporate Income Tax (CIT) and Personal Income Tax (PIT), Fiscal Years (FY) 2011 to 2016 | |||||

| State | Description | Year(s) enacted | Phase-in begins | Phase-in ends | Cost when fully implemented |

| Arizona | CIT – Rate Reduction | 2011 | 2014 | 2017 | $270 million 2.9% of FY17 Revenue |

| Indiana | CIT for Financial Institutions | 2013, 2014 | 2014 | 2024 | $504 million 2.9% of FY17 Revenue |

| CIT – Rate Reduction | 2011, 2014 | 2012 | 2022 | ||

| PIT – Rate Reduction | 2013 | 2015 | 2017 | ||

| Kansasa | PIT – Rate Reduction | 2013 | 2014 | 2018 | $460 million 7.3% of FY17 Revenue |

| Maine | PIT – Rate Reduction and Change in Brackets | 2015 | 2016 | 2017 | $181 million 5.4% of FY17 Revenue |

| Mississippib | CIT – Elimination of Franchise Tax | 2016 | 2018 | 2028 | $415 million 7.4% of FY17 Revenue |

| PIT – Exemption for First $5,000 in Taxable Income | 2018 | 2022 | |||

| Missouri | CIT – Elimination of Franchise Tax | 2011 | 2012 | 2016 | $127 million 1.4% of FY16 Revenue |

| North Carolinac | CIT – Rate Reduction | 2013 | 2014 | 2015-17 | $1.3 billion 5.9% of FY17 Revenue |

| PIT – Rate Reduction | 2014 | 2015 | |||

| New Mexico | CIT – Rate Reduction | 2013 | 2014 | 2018 | $71 million 1.1% of FY17 Revenue |

| New York | PIT – Rate Reduction | 2016 | 2018 | 2025 | $4.2 billion 5.7% of FY17 Revenue |

| Ohio | PIT – Rate Reductions | 2013 | 2013 | 2015 | $1.0 billion 3.3% of FY15 Revenue |

| PIT - Acceleration of Rate Reduction | 2014 | 2014 | 2014 | ||

| South Carolina | PIT for Business Income | 2012 | 2012 | 2014 | $64 million 1.0% of FY14 Revenue |

State Policymakers Typically Have No Idea if Phased-in Tax Cuts Will Be Affordable

State policymakers have a responsibility to assure that their actions will not undermine their state’s future finances, but policymakers enacting tax cuts that phase in over time typically have no idea if these cuts will be affordable. They typically lack basic information necessary to make this assessment, leaving their state’s future financial health at risk.

- Forecasts of state finances are usually unavailable. Lawmakers often lack up-to-date, multi-year forecasts of how much states expect to spend in the year a phased-in tax cut would take full effect or an estimate of total revenues at that time. Such forecasts could be done in most cases, but they are almost never done.[12] And without that information, policymakers cannot responsibly evaluate the tax cuts’ impact on state services.

- The best economic and financial forecasts have limitations. Even if such a forecast is available, it cannot predict the occurrence or magnitude of an economic downturn before a tax cut takes effect. Nor can it predict random events that can also drastically affect state finances, such as natural disasters or cuts in federal aid to states.

- Policymakers’ and voters’ priorities can change. Even the best forecast cannot predict how state needs and citizen preferences might change between the time the tax cuts are enacted and the time they’re implemented, or whether policymakers and the public will still see them as a priority.

The 11 states that adopted phased-in tax cuts in recent years did so largely without information critical to assessing the likely impact on the state’s ability to provide essential services. None of them produced a careful estimate of the cost of providing existing services — taking into account caseload or enrollment changes, inflation, and any pending rule changes — over the tax cuts’ full phase-in period, leaving policymakers in the dark as to whether the tax cuts will force cuts in services.[13]

While ten of the 11 states produce some form of multi-year expenditure estimates, only five covered the full duration of the phase-in: Maine, New Mexico, North Carolina, Ohio, and South Carolina. And Mississippi, with the longest phase-in (11 years), does not produce multi-year expenditure forecasts.[14]

Phased-In Tax Cuts Can Create Structural Problems for State Budgets

Since lawmakers often adopt large, phased-in tax cuts not knowing whether or not they will be affordable, and since large tax cuts sharply reduce state revenues, they can lead to major structural problems for state budgets, or the chronic inability of revenues to grow in tandem with economic growth and the cost of government. Because of states’ balanced-budget requirements, major revenue losses force states to cut services, raise other revenues, or both.

That’s exactly what is happening in states that have phased-in large tax cuts in recent years. For instance:

- Arizona in 2011 phased in a cut in the corporate income tax rate and enacted a separate tax cut for multi-state corporations, at a combined cost of more than $200 million annually by 2020.[15] The revenue loss from the tax cuts has added to the state’s difficulty in funding education, exacerbating the harm caused by other tax cuts and the Great Recession and resulting in extraordinary funding cuts for schools and colleges. General state funding per student for K-12 schools is down 13 percent since before the Great Recession took hold, after adjusting for inflation,[16] and average tuition at four-year public colleges and universities has soared by 88 percent to offset a steep decline in state support.[17]

- Kansas in 2012 sharply reduced income tax rates and exempted certain business income from tax. In 2013, Kansas adopted a plan to phase in additional income tax rate cuts over time and eventually eliminate the income tax.[18] Two years into the phase-in, faced with an ongoing budget crisis, lawmakers paused the phase-in for three years and made subsequent reductions contingent on meeting certain conditions. Since the tax cutting started, the state has cut funding for services multiple times, drained its operating reserves, raised sales tax rates, and shifted funds away from planned transportation projects to pay for the immediate needs of schools and other services. [19] The state’s bond rating has been downgraded twice, its general funding per student for K-12 schools is still 13 percent below pre-recession levels adjusted for inflation, and state officials project shortfalls of $346 million this fiscal year and more than $580 million next year.[20] Between fiscal years 2013 and 2018 the cumulative value of the changes to income tax will have cost the state roughly $4.6 billion[21] leading to a structural gap between the cost of ongoing state services and projected recurring revenue of more than $900 million beginning in fiscal year 2018.[22]

- Mississippi in 2016 enacted an 11-year phase-out of the franchise tax and a four-year phased-in cut to the personal and corporate income taxes. When fully implemented, it will cost $415 million annually — likely more than 7 percent of the state’s budget — due mostly to the elimination of the franchise tax.[23] These large revenue reductions will phase in even though the state has failed for several years to meet its own standards for school funding, and general state support per student for K-12 schools is down 9 percent since before the recession took hold, after adjusting for inflation. The phased-in tax cuts will limit Mississippi’s ability to respond to crises going forward and has already affected the state’s credit outlook. Last year Moody’s Investor Service cited the state’s use of reserves to close a budget hole and the fact that “Mississippi just passed a record $415 million tax cut” as reasons for giving the state a negative outlook.[24] Mississippi is one of 16 states that requires a supermajority legislative vote to raise taxes, making it particularly difficult to reverse course if the tax cuts prove unaffordable.

- North Carolina in 2013 enacted a flat personal income tax with a phased-in rate cut, expanded the sales tax base, and phased in a cut in the corporate income tax, at a combined cost of more than $1.4 billion in fiscal year 2017 and an estimated $2 billion annually once the cuts are fully implemented.[25] It did so even though state funding per student for K-12 schools is down nearly 10 percent since the recession took hold, after adjusting for inflation,[26] and four-year public college tuition shot up 42 percent after the state cut funding.[27]

- New Mexico is phasing in a corporate income tax rate cut as part of a broader tax package that will cost the state more than $70 million annually when fully implemented in 2018.[28] These cuts have exacerbated the fiscal problems caused by the sharp drop in oil prices, which weakened the state’s economy and state revenues. The state cut funding for services and used one-time revenue last year to balance its budget, and faces a shortfall this fiscal year of $70 million — an amount that’s identical to the cost of the tax package when fully implemented. [29] Some lawmakers are considering reinstituting a sales tax on groceries to raise additional funds, a move that would fall hardest on low-income families since they spend a higher share of their earnings on food.[30]

The structural problems created by phasing in tax cuts add to the difficulties many states faced even before the tax cuts due to long-term trends that prevent revenues from keeping up with the cost of existing state services.[31] On the revenue side, these trends include the shift in household purchases toward services (which are largely untaxed) and online sales (many of which are effectively untaxed), declining alcohol and tobacco taxes as consumption falls, and states’ failure to adapt their corporate income taxes to the growing sophistication of corporate tax-avoidance strategies. On the spending side, they include the tendency of health-care costs (which represent a disproportionate share of state budgets) to grow faster than other expenses, the growing demand for a college education, and the need to make long-deferred investments in schools, roads, and other forms of critical public infrastructure.

These trends imply that — regardless of the level of services they choose to provide — states will eventually need to generate additional revenue, for example by closing loopholes, scaling back ineffective economic development giveaways, and/or increasing tax rates.

Phased-In Tax Cuts Enable Lawmakers to Avoid Accountability

States do not legally lock in the path of future spending; they typically budget two years into the future at most. Enacting tax cuts that will begin and/or continue beyond the budget period increases the odds they will take precedence over spending needs and priorities at the time they take effect. The tax cuts present a fait accompli to any future policymakers or citizens who might prefer to allocate the higher amount of revenue that would otherwise be available to different priorities: for example, making new investments in education or infrastructure, expanding the state’s “rainy-day” fund, addressing a long-range fiscal problem (like an underfunded pension fund), or substituting a different type of tax cut.

Delayed effective dates also enable policymakers to avoid accountability for their actions. They can immediately claim credit for voting for tax cuts that — given state balanced-budget requirements — would force politically unpopular service cuts if they took effect in the near term, and gamble that the cuts will not harm public services or the state’s financial stability down the road.[32]

Cutting Income Taxes Typically Shifts Costs From Wealthy to Middle- and Low-Income Residents

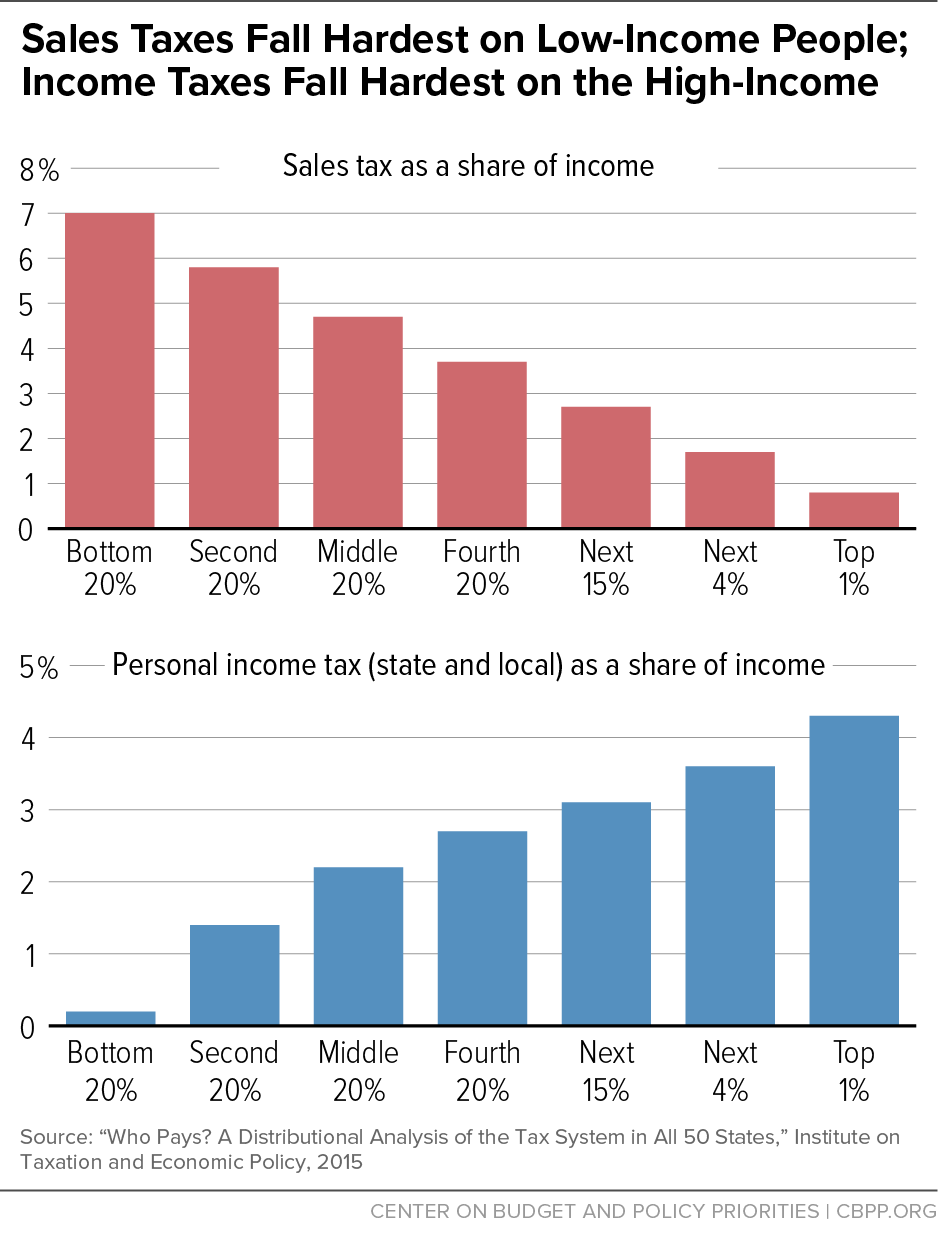

Income taxes typically ask more of wealthier residents than middle- and low-income families. In general, income tax rates increase as incomes rise, and states with a single income tax rate typically use various deductions, exemptions, and credits to reduce taxes for lower-income taxpayers relative to wealthier ones. In the average state, the poorest fifth of households pay about 0.2 percent of their income in personal income taxes, while the top 1 percent of households pay about 4.3 percent.[33] (See Figure 1.)

In contrast, the other major state taxes — sales, property, and excise taxes (such as those on gas or cigarettes) — tend to fall harder on middle- and low-income families. In the average state, for example, the poorest fifth of households pay about 7 percent of their income in sales taxes, compared to less than 1 percent for the very richest households.[34]

As a result, when states cut income taxes they typically shift responsibility for who pays for state services away from the rich and toward the middle class and poor. Often states raise sales taxes to make up part of the revenue lost to income tax cuts, directly shifting tax payments from the relatively well-off to lower-income people. These tax cuts sometimes result in other forms of tax-shifting, such as to college students (as state universities hike tuition to make up for cuts in state support) and property owners (as localities raise property taxes to make up for receding state aid.)

Phased-In Tax Cuts Are Hard to Reverse

Proponents respond to criticisms of phased-in tax cuts by noting that future policymakers can always reduce, postpone, or cancel them. It is true that a future effective date in tax cut legislation constitutes a political obstacle to setting different priorities, not a legal one. But at a time when a large number of state lawmakers have signed public pledges never to vote for a tax increase — and many who haven’t are concerned that voting to scale back or suspend a scheduled tax cut would open them to attack for raising taxes, it is a significant obstacle. Simply stated, “once a tax cut is set in law, it is politically hard to reverse.”[35]

| TABLE 2 | ||

|---|---|---|

| States Requiring a Legislative Supermajority or Vote of the People to Increase Taxes | ||

| State | Majority Required | Applies to… |

| Arizona | 2/3 | All Taxes |

| Arkansas | 3/4 | All Taxes Except Sales and Alcohol |

| California | 2/3 | All Taxes |

| Colorado1 | 2/3 | All Taxes |

| Delaware | 3/5 | All Taxes |

| Florida2 | 3/5 | Corporate Income Taxes |

| Kentucky3 | 3/5 | All Taxes |

| Louisiana | 2/3 | All Taxes |

| Michigan | 3/5 | State Property Taxes |

| Mississippi | 3/5 | All Taxes |

| Missouri4 | 2/3 | All Taxes |

| Nevada | 2/3 | All Taxes |

| Oklahoma | 3/4 | All Taxes |

| Oregon | 3/5 | All Taxes |

| South Dakota | 2/3 | All Taxes |

| Wisconsin | 2/3 | Sales, Income, and Franchise Taxes |

The political difficulties are especially challenging in the 16 states that require a supermajority vote to raise taxes — which in many cases includes eliminating tax credits, deductions, or exemptions (see Table 2).[36] This requirement can also limit a state’s ability to respond to budget shortfalls in times of crisis.

Supermajority requirements raise the bar for passing a specific type of legislation in a system already resistant to change. To become law, most state legislation must receive majority approval at many points along the way, from committee on up to the governor’s office. At any point along the way, a bill can be stopped, changed, or voted down. Supermajority requirements for tax increases effectively declare that the will of the majority is sufficient to cut taxes but not to raise them.

No Meaningful Benefits to Enacting Tax Cuts Far in Advance

There are no practical benefits to enacting tax cuts, triggered or un-triggered, far in advance of when they will take effect. Whenever elected officials decide that taxes can be cut without requiring cutting services or are a priority even if they might negatively affect services, the cuts can be implemented almost immediately. New withholding schedules for individual income taxes can be published by state tax departments and implemented by payroll processors in a few weeks’ time. Point-of-sale systems that calculate sales taxes can be reprogrammed quickly. Even an immediate corporate income tax cut only requires action two to three months down the road when companies calculate their quarterly estimated payments.

Indeed, most “immediate” cuts in individual and corporate income taxes do not actually take effect until the beginning of the next calendar year, which is adequate time to ensure proper compliance.

With regard to the potential economic benefits, knowing future tax rates may help individuals and businesses decide whether to make certain long-term investments, but these benefits are likely quite limited when it comes to state taxes. Most of the phased-in tax cuts enacted in recent years involve personal income taxes, and only a small minority of income tax payers are business owners making significant capital investment decisions.[37] Also, state personal and corporate income tax rates are relatively low to begin with — especially in comparison to federal rates — and thus unlikely to tip investment decisions. And because elected officials may cancel or postpone previously enacted tax cuts, investors can never be 100 percent certain of future tax rates.

In short, any theoretical economic benefits of delayed tax cuts are relatively minor, especially when compared to the very real economic damage and disruption if the tax cuts turn out to be unaffordable. The lack of concrete benefits suggests that the fundamental objective of delayed tax cuts (whether or not they have triggers) is to avoid the political backlash that could arise if state services had to be cut immediately while erecting a political obstacle to making different fiscal policy choices down the road.

Conclusion

Most states face major fiscal challenges in coming years and should proceed with caution regarding phased-in income tax cuts, which can create or worsen structural budget problems and can increase inequality by shifting taxes from wealthier taxpayers to the middle class and poor. They also can be extremely costly and are generally difficult to roll back. The self-inflicted loss of revenue can limit a state’s ability to respond to a crisis or recession or to invest in the cornerstones of a thriving community, such as high-quality public education, infrastructure, and health care.

States could better evaluate the cost and consequences of proposed phased-in tax cuts by adopting a “pay-as-you-go” rule requiring any new tax cut to be paid for through an increase in other taxes and/or reduction in spending.[38]

End Notes

[1] The 11 states are Arizona, Indiana, Kansas, Maine, Mississippi, Missouri, New Mexico, New York, North Carolina, Ohio, and South Carolina.

[2] Other states have enacted tax cuts that only become effective if certain fiscal conditions are met. For more on these “triggered” tax cuts see Michael Mazerov. “Revenue ‘Triggers’ for State Tax Cuts Provide Illusion of Fiscal Responsibility,” Center on Budget and Policy Priorities, February 2, 2017.

[3] Legislative supermajorities are required to increase taxes in 16 states. See “Policy Basics: State Supermajority Rules to Raise Revenue,” Center on Budget and Policy Priorities, revised February 11, 2015, https://www.cbpp.org/sites/default/files/atoms/files/PolicyBasics-StateSupermajorities-4-22-13.pdf.

[4] See Iris J. Lav, “PAYGO: Improving State Budget Discipline While Retaining Flexibility,” CBPP, September 22, 2011, https://www.cbpp.org/research/paygo-improving-state-budget-discipline-while-retaining-flexibility.

[5] “Bobby Jindal’s Louisiana is a Cautionary Tale for the Nation,” Tax Justice Blog, June 24, 2015, http://www.taxjusticeblog.org/archive/2015/06/bobby_jindals_louisiana_is_a_c.php#.WGLjrlUrI7Y.

[6] Kansas subsequently delayed the phase-down of the personal income tax in 2015. The new law freezes personal income tax rates at the 2015 levels until 2017, then drops the top rate in 2018 and allows for income tax rate reductions to continue beginning in 2021, subject to a revenue trigger.

[7] Chris Mai, “Kansas’ Projections Show Tax Cuts Aren’t Paying Off as Predicted,” CBPP, May 14, 2014, https://www.cbpp.org/blog/kansas-projections-show-tax-cuts-arent-paying-off-as-predicted. See also Michael Mazerov, “Kansas’ Tax Cut Experience Refutes Economic Growth Predictions of Trump Tax Advisers,” CBPP, updated August 12, 2016, https://www.cbpp.org/research/federal-tax/kansas-tax-cut-experience-refutes-economic-growth-predictions-of-trump-tax.

[8] Mazerov, 2017.

[9] Many other states have used phased-in tax cuts to reduce or eliminate a variety of tax types. This report focuses on the use of phase-ins to reduce or eliminate personal and corporate/franchise taxes because of the magnitude of the cuts and the importance of income taxes as a source of general fund revenue for most states.

[10] For an earlier analysis of states enacting phased-in tax cuts in the mid 2000’s, See Nicolas Johnson and Sarah Farkas, “Tax Cuts on Layaway,” CBPP, October 10, 2006, https://www.cbpp.org/research/tax-cuts-on-layaway.

[11] The $8 billion does not include the estimated impact of the personal income tax phase-in enacted in Kansas because of a subsequent pause in the reduction.

[12] Reliable forecasts may not be doable at all if the effective date of a scheduled tax cut is more than four or five years in the future or if a triggered tax cut has no time limit on when the cut can trigger.

[13] A “current services baseline” or “current services budget” estimates the cost of providing the current level of services in the future based on changes in population, cost of living adjustments, and other factors. Of the states discussed in this paper, only Arizona and New York produce baseline budget estimates extending beyond the current budget year, and both states are implementing phased-in tax cuts that extend far beyond their baseline estimates. For more on state budgeting tools, see Elizabeth McNichol, “Budgeting for the Future,” Center on Budget and Policy Priorities, February 4, 2014, https://www.cbpp.org/research/state-budget-and-tax/budgeting-for-the-future-fiscal-planning-tools-can-show-the-way.

[14] Based on data from “Budget Processes in the States,” National Association of State Budget Officers, Spring 2015, https://higherlogicdownload.s3.amazonaws.com/NASBO/9d2d2db1-c943-4f1b-b750-0fca152d64c2/UploadedImages/Reports/2015%20Budget%20Processes%20-%20S.pdf.

[15] Based on revenue projections published by the Arizona Joint Legislative Budget Committee, January 2017, http://www.azleg.gov/jlbc/revenuebudgetupdatepres011917.pdf

[16] Michael Leachman, Kathleen Masterson, and Marlana Wallace, “After Nearly a Decade, School Investments Still Way Down in Some States,” CBPP, October 20, 2016, https://www.cbpp.org/sites/default/files/atoms/files/10-20-16sfp.pdf.

[17] Michael Mitchell, Michael Leachman, and Kathleen Masterson, “Funding Down, Tuition Up State Cuts to Higher Education Threaten Quality and Affordability at Public Colleges, CBPP, revised August 15, 2016, https://www.cbpp.org/sites/default/files/atoms/files/5-19-16sfp.pdf.

[18] For more detail on the timing and impact of Kansas tax cuts see “Kansas Tax Facts,” Kansas Legislative Research Department, December 2016, http://www.kslegresearch.org/KLRD-web/Publications/TaxFacts/2016TaxFactsSupp.pdf.

[19] Chris Mai, “Kansas’ Projections Show Tax Cuts Aren’t Paying Off as Predicted,” CBPP, May 14, 2014, https://www.cbpp.org/blog/kansas-projections-show-tax-cuts-arent-paying-off-as-predicted. See also Michael Mazerov, “Kansas’ Tax Cut Experience Refutes Economic Growth Predictions of Trump Tax Advisers,” CBPP, updated August 12, 2016, https://www.cbpp.org/research/federal-tax/kansas-tax-cut-experience-refutes-economic-growth-predictions-of-trump-tax.

[20] Current revenue estimate projecting Kansas deficit “State General Fund Revenue Estimate for FY2017, FY2018, and FY2019,” Kansas Division on the Budget and Kansas Legislative Research Department, November 10, 2016, http://budget.ks.gov/files/FY2018/CRE_Short_Memo_Nov2016.pdf.

[21] See “SGF Receipts Estimates for FY 2017, FY 2018, and FY 2019,” Kansas Legislative Research Department, December 1, 2016, http://budget.ks.gov/files/FY2018/CRE_Long_Memo_Nov2016.pdf.

[22] Based on analysis of Kansas Legislative Research Department, “State General Fund Profile,” November 10, 2016, http://www.kslegresearch.org/KLRD-web/Publications/2016Appropriations/SGF-Profile-FY15-FY19-Nov2016.pdf.

[23] See “Fiscal Note for SB2858,” Mississippi Legislative Budget Office (2016).

[24] Associated Press, “Moody’s: Mississippi Has Negative Credit Outlook,” Jackson Free Press, July 13, 2016, http://www.jacksonfreepress.com/news/2016/jul/13/moodys-mississippi-has-negative-credit-outlook/.

[25] Tazra Mitchell and Cedric Johnson, “2017 Fiscal Year Budget Falls Short of Being a Visionary Plan for North Carolina’s Economic Future: Lawmakers Double Down on Tax Breaks, Set Limited Aspirations,” North Carolina Budget and Tax Center, July 2016, http://www.ncjustice.org/sites/default/files/BTC%20Reports%20-%20FINAL%20BUDGET.PDF.

[26] Leachman, Masterson, and Wallace, 2016.

[27] Mitchell, Leachman, and Masterson, 2016.

[28] “Fiscal Impact Report for HB641,” New Mexico Legislative Finance Committee, revised April 15, 2013, https://www.nmlegis.gov/Sessions/13%20Regular/firs/HB0641.PDF.

[29] “December 2016 Consensus Revenue Estimate,” New Mexico Legislative Finance Committee, December 5, 2016, https://www.nmlegis.gov/Entity/LFC/Documents/Revenue_Reports/General_Fund_Revenue_Forecast/2016/Consensus%20Revenue%20Estimate%20-%20December%202016.pdf.

[30] Andrew Oxford, “Food Tax Poised to be Divisive Issue in Session,” Santa Fe New Mexican, December 16, 2016, http://www.santafenewmexican.com/news/local_news/food-tax-poised-to-be-divisive-issue-in-session/article_eec2c5e5-94cd-5f3d-8570-727e9f7d45a1.html.

[31] These are not new challenges. For additional information on various other challenges states face, see Nicholas Johnson, “Improving State Fiscal Policies in the 2007 Legislative Session,” Center on Budget and Policy Priorities, revised January 26, 2007, https://www.cbpp.org/research/improving-state-fiscal-policies-in-the-2007-legislative-sessions.

[32] As former Oklahoma Senate President Cal Hobson has candidly acknowledged: “It’s irresistible. You get a tax reduction bill out there, and we don’t think past the end of our noses.” Warren Vieth, “Study Finds a Decade of Income Tax Cuts Deprived State of $1B This Year,” Oklahoma Watch, January 12, 2016.

[33] See “Who Pays? A Distributional Analysis of the Tax Systems in All 50 States,” Institute on Taxation and Economic Policy, 5th edition, January 2015, http://www.itep.org/pdf/whopaysreport.pdf.

[34] Ibid.

[35] Elaine S. Povich, “’Triggers’ Cut State Taxes; But are they Good Policy?” Pew Charitable Trusts, November 16, 2015, http://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2015/11/16/triggers-cut-state-taxes-but-are-they-good-policy.

[36] For more on legislative supermajorities see “Policy Basics: State Supermajority Rules to Raise Revenue,” CBPP, updated February 11, 2015, https://www.cbpp.org/sites/default/files/atoms/files/PolicyBasics-StateSupermajorities-4-22-13.pdf.

[37] See Michael Mazerov, “Cutting State Personal Income Taxes Won’t Help Small Businesses Create Jobs and May Harm State Economies,” CBPP, February 19, 2013, https://www.cbpp.org/research/cutting-state-personal-income-taxes-wont-help-small-businesses-create-jobs-and-may-harm. The vast majority of small business owners whose profits are subject to taxation under personal income taxes are self-employed professionals or tradesmen whose capital equipment needs are likely relatively modest.

[38] For more on the history and fiscal benefits of a “pay-as-you-go” rule, see Lav, 2011.

More from the Authors

Areas of Expertise

Areas of Expertise