ACA Marketplaces Poised for Greater Price Stability and Competition, But Also Vulnerable to Sabotage

A new analysis from Standard and Poor’s (S&P) Global Ratings, along with earnings announcements from health plans themselves, show that major individual-market insurers made significant progress toward profitability in 2016.[1] With sizable premium increases in place for 2017, the S&P analysis concludes these insurers have now largely recovered from initial underpricing for the Affordable Care Act (ACA) marketplaces, and their individual-market premiums are now generally in line with costs. The new analysis is consistent with other evidence that insurers are on track to break even or earn profits this year, and the ACA marketplaces are on track for smaller annual rate increases and growing competition going forward. Progress could easily be reversed if the Trump Administration continues to sabotage the individual market.But the S&P analysis — as well as recent statements from state insurance commissioners, health plans, hospitals, business leaders, and others — also emphasizes that this progress could easily be reversed if the Trump Administration continues to sabotage the individual market.[2]

S&P Analysis Finds Blue Cross Blue Shield Insurers Curbed Losses in 2016, on Track to Break Even This Year

Starting in 2014, the ACA prohibited insurers from denying coverage or charging higher prices to people with pre-existing health conditions, a crucial reform for more than 130 million Americans.[3] But because the individual market had previously shut out people with expensive health problems, insurers had little data on the cost of extending coverage to everyone. In 2014, they set individual-market premiums well below costs, leading to large financial losses.[4] Likewise, in 2015, insurers set premiums before seeing most of their actual 2014 data, and they raised premiums by just 2 percent on average, even as the ACA’s temporary reinsurance funding phased down, increasing insurer costs by an amount equal to about 7 percent of premiums. As a result, insurer losses generally deepened in 2015, even though the individual-market risk pool improved as enrollment grew. [5]

In 2016, insurers increased individual-market premiums by about 8 percent on average, while reinsurance payments phased down by another roughly 7 percent of premiums.[6] But with actual claims data available on which to base prices, some insurers — including a number of those experiencing particularly large losses — increased their premiums more significantly.[7] In addition, many insurers redesigned their products, renegotiated rates with providers, adjusted care management practices, and made other changes to reduce costs based on their growing experience with the new, post-ACA individual market.[8]

Insurer data recently filed with the National Association of Insurance Commissioners (NAIC) provide the first comprehensive look at how premium and product changes in 2016, along with continued evolution of the individual-market risk pool, affected health plans’ profitability. S&P analyzed these data for (primarily) non-profit Blue Cross Blue Shield insurers (“Blues plans”).[9] Blues plans included in the S&P analysis accounted for 5.5 million individual-market enrollees in 2016, or over a quarter of the individual market — so while their experience does not necessarily mirror trends for the full individual market, they comprise a substantial share of it. Also important, most insurers that are the sole insurer in a state or county are non-profit Blues plans, so the S&P analysis captures the financial performance of the insurers that may be most critical to ensuring that consumers nationwide continue to have marketplace options.

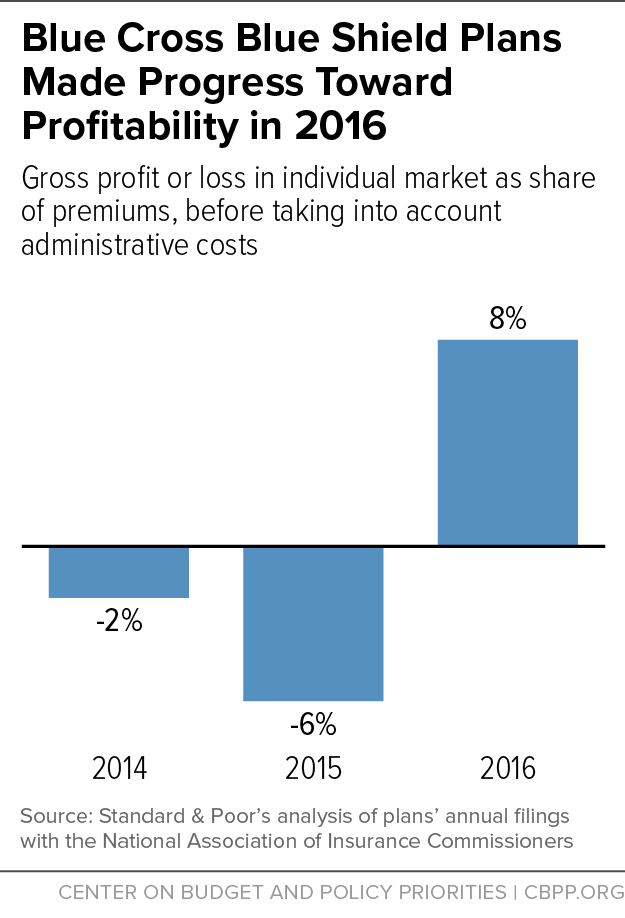

The S&P analysis finds that non-profit Blues plans sharply reduced their individual-market losses in 2016. In fact, as Figure 1 shows, these plans earned gross profits for the first time since the ACA’s individual-market reforms took effect in 2014 — although most plans are still likely to report net losses after subtracting administrative costs (not included in the study). Specifically, Blues plans went from gross losses averaging 2 and 6 percent of premiums in 2014 and 2015, respectively, to gross profits averaging 8 percent of premiums in 2016, a year-over-year improvement in financial performance averaging 14 percent of premiums.

Moreover, as the S&P report notes, “insurers have put in place meaningful premium rate increases, along with product and network changes, for 2017.” Based on the 2016 financial data, the S&P report concludes that 2017 increases have also largely brought premiums in line with costs. Many non-profit Blues plans are now sustainably priced and should be on track to at least break even, net of administrative costs, this year. This is consistent with other analyses, for example from the Council of Economic Advisers and the Centers for Medicare & Medicaid Services Office of the Actuary, that also conclude that large 2017 individual-market premium increases were one-time adjustments, calibrated to bring premiums in line with costs.[10] Notably, insurers’ 2017 premium increases have brought ACA individual market premiums in line with the Congressional Budget Office’s initial projections.[11]

As the S&P report also notes, consumers have been largely insulated from these pricing adjustments, because the ACA’s premium tax credits have increased as needed to protect consumers from price increases. Among the 85 percent of marketplace consumers eligible for tax credits, premiums after accounting for premium tax credits increased by just $4 per month between 2015 and 2017, from $102 to $106.[12] Partly as a result, marketplace enrollment for 2017 is above 2015 levels, even though average pre-tax credit premiums have increased substantially since then.

Most Blues Plans Saw Improved Individual-Market Performance in 2016

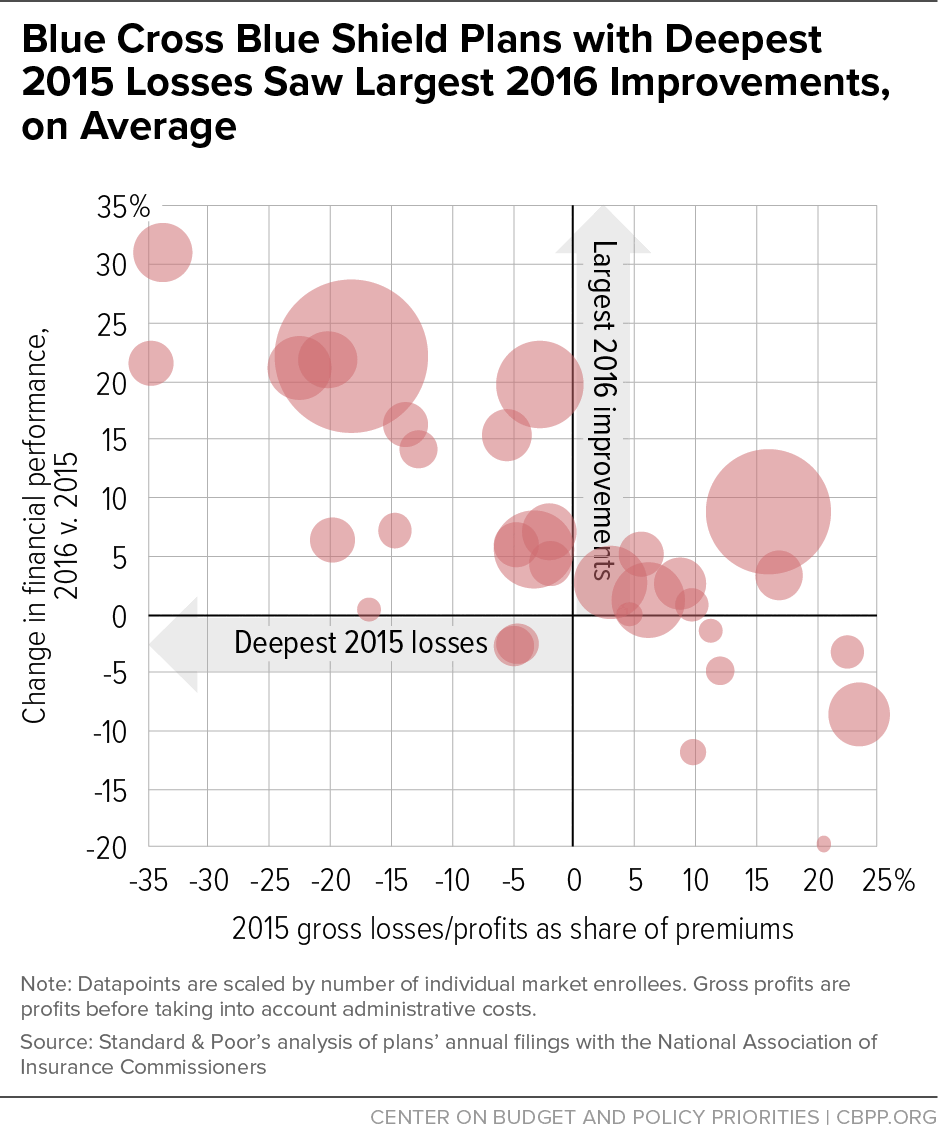

The S&P report also examines the experience of individual health plans around the country. As Figure 2 shows, insurers with the largest 2015 losses generally also saw the largest improvements in their financial position in 2016. Overall, Blues plans accounting for 1.8 million individual-market enrollees had gross profits (not accounting for administrative costs) of at least 10 percent of premiums in 2016, while Blues plans accounting for another 3.4 million individual-market enrollees reduced their losses. The remaining Blues plans included in the S&P analysis, accounting for about 300,000 individual-market enrollees, had gross profit margins of less than 10 percent of premiums in 2016 (or gross losses) and worse financial performance in 2016 than 2015.

More specifically, the S&P report, combined with other news accounts and statements from plans themselves, shows:

- Blues plans that earned profits or broke even in the first two years of the ACA’s individual-market reforms generally continued to do so in 2016. For example, a separate analysis found that Florida Blue earned almost $1.1 billion in gross profits on ACA individual-market plans in 2016, an increase over already large profits in 2015.[13] The S&P data show that Horizon Healthcare Services in New Jersey and Blue Cross Blue Shield of Michigan also remained profitable. Arkansas Blue Cross Blue Shield and Blue Cross Blue Shield of North Dakota, which have publicly noted their companies’ success in the ACA marketplaces to date, maintained stable margins, as did Blue Cross Blue Shield of South Carolina.[14]

- A few plans with losses in 2014 and 2015 broke even or earned profits in 2016. After two years of deep losses, Premera Blue Cross in Alaska announced that it earned $20 million in profits on individual-market plans in 2016.[15] A separate analysis also found that Blue Cross Blue Shield of North Carolina likely broke even or earned a profit on individual-market plans in 2016.[16] And the S&P analysis finds that Blue Cross Blue Shield of Arizona went from large losses in 2015 to gross profits equal to about 10 percent of premiums in 2016, indicating that it should have come close to breaking even after administrative costs — and before additional premium increases for 2017.

-

Most of the plans that saw the deepest losses in 2014 and 2015 sharply reduced those losses in 2016. Plans in this category include dominant or major insurers in a number of states that saw among the largest rate increases in the country in 2017, including Alabama, Illinois, Montana, Oklahoma, Pennsylvania, Tennessee, and West Virginia. Those additional rate increases should put these insurers on track to break even or earn profits in the individual market this year, all else equal. For example:

- After two years of very large losses, Health Care Services Corporation (HCSC), which is the sole insurer in Oklahoma and parts of Texas and Illinois and also offers plans in New Mexico and Montana, cut its losses by 22 percent of premiums and earned a gross profit, not taking into account administrative costs, on individual-market plans.[17]

- Blue Cross Blue Shield of Tennessee, which is the sole insurer in parts of Tennessee and withdrew from the marketplace in other parts of the state in 2017, cut its losses by 21 percent of premiums.

- Highmark, the sole insurer in parts of West Virginia and a major insurer in Pennsylvania and Delaware, cut its losses by 31 percent of premiums.

- Blue Cross Blue Shield of Alabama, the sole insurer in that state, cut its losses by 22 percent of premiums and earned a gross profit, not taking into account administrative costs, on individual-market plans.

Other Blues plans also reduced their losses, though less dramatically. These include plans in Washington, D.C., Idaho, Kansas, Louisiana, Maryland, Minnesota, Missouri, Nebraska, Oregon, Pennsylvania, and Washington.

Sabotage Could Easily Reverse Recent Gains

Improvements in plans’ financial performance are important to consumers because they mean smaller premium increases and more competition going forward, all else equal. As the S&P analysis notes, “if it remains business as usual, we expect 2018 premiums to increase at a far lower clip than in 2017.” Likewise, under normal circumstances, improved financial performance would lead plans to maintain or expand their marketplace participation, and evidence that insurers now participating in the market are earning profits would draw new competitors.

Unfortunately, President Trump indicated again last week that he is considering active sabotage of the ACA marketplaces. Already, the Trump Administration has pulled down advertising during one of the most crucial weeks of open enrollment, created uncertainty about whether it plans to enforce the ACA’s individual mandate, and proposed a regulation that would effectively cut premium tax credits, reducing demand for marketplace plans.[18]

Now, President Trump is threatening to hold hostage billions in ACA cost-sharing reduction payments to insurers to try to force congressional Democrats to agree to some version of the House ACA repeal bill. Uncertainty about whether the federal government will continue these payments, which reimburse insurers for providing plans with lower deductibles, copays, and coinsurance to lower-income marketplace enrollees, could lead insurers to raise premiums on silver plans by up to 19 percent.[19] Equally important, halting these payments — or even prolonging the uncertainty around whether payments will continue — could convince insurers that the Administration plans to keep sabotaging the individual market, which could lead many to stop offering plans altogether.

Already, two insurers have announced plans to withdraw from Iowa’s marketplace next year, citing administrative and legislative uncertainty as among the factors driving their decisions.[20] S&P, state insurance commissioners, and insurer, hospital, and business groups have all emphasized that the Administration’s actions over the coming weeks, especially its decisions about cost-sharing reduction payments, will determine whether consumers nationwide will have marketplace insurance options next year, and at what cost.

- S&P’s analysis concludes: “any significant overhaul or increased uncertainty may lead to a different result than we have forecasted for 2017 and 2018. If the legal battle over CSRs [cost-sharing reductions] isn’t concluded soon, or if insurers don’t have clear assurances that they will be paid for CSRs in 2018, they will have to make a decision on pricing and participation without adequate information…. If insurers are uneasy regarding the future of the market, they may have to decide between adding an ‘uncertainty buffer’ to their pricing or — worst case — exiting the exchanges altogether.”

- In a joint letter, the Chamber of Commerce, American Hospital Association, Federation of American Hospitals, Blue Cross Blue Shield Association, America’s Health Insurance Plans, American Academy of Family Physicians, and American Benefits Council implored President Trump and Congress to offer certainty regarding cost-sharing reduction payments. Otherwise, “choices for consumers will be more limited … premiums for 2018 and beyond will be higher … [and] providers will experience more uncompensated care.”[21]

- Teresa Miller, Pennsylvania’s Insurance Commissioner, recently observed that Pennsylvania’s market is improving but still at risk: “We should have a pretty decent market. I feel cautiously optimistic, but the uncertainty is driving everybody crazy.” She also commented, “You had a couple of members of Congress talking about how they’ll wait for the marketplace to collapse. All of a sudden our insurers are like, ‘Oh no. If you all want to make it fail, that can happen.’” Likewise, Mike Kreidler, Washington’s Insurance Commissioner, wrote in a joint letter with the Association of Washington Healthcare Plans, “[We] strongly believe that market stability is achieved when issuers can engage in long-range planning in a stable financial and regulatory context… Currently, the most significant and immediate drivers of market uncertainty are the weakening of individual mandate enforcement, the uncertain status of cost-sharing reduction funding, and the lack of funding for broader market stabilization measures.”[22]

The data are increasingly clear: the Trump Administration inherited an individual market that, far from “imploding,” is poised for greater price stability and increased competition going forward. The decision about whether to capitalize on that opportunity or sabotage it rests with the Administration.

End Notes

[1] S&P Global Ratings, “The U.S. Individual Market Showed Progress in 2016, But Still Needs Time to Mature,” April 7, 2017, https://www.globalcreditportal.com/ratingsdirect/renderArticle.do?articleId=1828594&SctArtId=421970&from=CM&nsl_code=LIME&sourceObjectId=10047007&sourceRevId=5&fee_ind=N&exp_date=20270408-00:16:31.

[2] Sarah Lueck, “How the Trump Administration Might Sabotage ACA Insurance Markets,” Center on Budget and Policy Priorities, April 4, 2017, https://www.cbpp.org/health/commentary-how-the-trump-administration-might-sabotage-aca-insurance-markets.

[3] Office of the Assistant Secretary for Planning and Evaluation, “Health Insurance Coverage for Americans with Pre-existing Conditions: the Impact of the Affordable Care Act,” Department of Health and Human Services, January 5, 2017, https://aspe.hhs.gov/system/files/pdf/255396/Pre-ExistingConditions.pdf.

[4] See, for example, McKinsey Center for U.S. Health Reform, “2014 Individual Market Post-3R Financial Performance,” February 5, 2016, http://healthcare.mckinsey.com/sites/default/files/infographics/2016%20Post-3R%20Infographic.pdf.

[5] While many insurers raised premiums for given plans by more than 2 percent, average ACA individual market premiums increased by only 2 percent after consumers shopped and selected new coverage. For these data and data on per-enrollee claims costs, see Centers for Medicare & Medicaid Services, “Changes in Individual Market Costs from 2014-2015: Near-Zero Growth Suggests an Improving Risk Pool,” August 11, 2016, https://www.cms.gov/cciio/resources/forms-reports-and-other-resources/downloads/final-risk-pool-analysis-8_11_16.pdf. For a more extended discussion of insurers’ initial pricing challenges in the ACA individual market, see Council of Economic Advisers, “Understanding Recent Developments in the Individual Market,” January 2017, https://obamawhitehouse.archives.gov/sites/default/files/page/files/201701_individual_health_insurance_market_cea_issue_brief.pdf.

[6] The 8 percent average captures only marketplace premiums (not premiums for individual market plans subject to ACA rules but offered outside the ACA marketplaces), and it includes only states using the HealthCare.gov eligibility and enrollment platform. Premium data for the full individual market for 2016 are not yet available, but the 2015 experience suggests the HealthCare.gov marketplace average provides a reasonable proxy. Assistant Secretary for Planning and Evaluation, “Health Insurance Premiums After Shopping, Switching, and Tax Credits, 2015-2016,” Department of Health and Human Services, April 12, 2016, https://aspe.hhs.gov/system/files/pdf/198636/MarketplaceRate.pdf.

[7] For example, certain states saw 2016 increases in “benchmark” premiums (premiums for the second-lowest cost silver plan, which are used to determine premium tax credits) that were well above the national average, including Alaska, Montana, North Carolina, New Mexico, Oklahoma, Oregon, South Dakota, and Tennessee. Kelsey Avery et al., “Health Plan Choice and Premiums in the 2016 Health Insurance Marketplace,” Department of Health and Human Services Assistant Secretary for Planning and Evaluation, October 30, 2015, https://aspe.hhs.gov/system/files/pdf/135461/2016%20Marketplace%20Premium%20Landscape%20Issue%20Brief%2010-30-15%20FINAL.pdf.

[8] See, for example, McKinsey Center for U.S. Health Reform, “2016 Exchange Market Remains in Flux: Plan Type Trends,” January 4, 2016, http://healthcare.mckinsey.com/sites/default/files/2016%20Plan%20Type%20Trends%20Infographic%20v29.pdf and materials from the Centers for Medicare & Medicaid Services conference on marketplace innovation, available at https://www.cms.gov/CCIIO/Resources/Forms-Reports-and-Other-Resources/.

[9] The S&P report excludes Anthem (the major for-profit Blues plan) and California Blue Cross Blue Shield (because it uses a different reporting template than other Blues plans).

[10] Council of Economic Advisers, “Understanding Recent Developments in the Individual Market,” and Sean P. Keehan et al., “National Health Expenditure Projections, 2016-25: Price Increases, Aging Push Sector to 20 Percent of Economy,” Health Affairs, February 2017, http://content.healthaffairs.org/content/early/2017/02/14/hlthaff.2016.1627.full.

[11] Assistant Secretary for Planning and Evaluation, “Health Plan Choice and Premiums in the 2017 Health Insurance Marketplace,” October 24, 2016, https://aspe.hhs.gov/system/files/pdf/212721/2017MarketplaceLandscapeBrief.pdf, Appendix C.

[12] Data for 2015 and 2016 are available from Assistant Secretary for Planning and Evaluation, “Health Insurance Premiums After Shopping, Switching, and Tax Credits, 2015-2016,” Department of Health and Human Services, April 12, 2016, https://aspe.hhs.gov/system/files/pdf/198636/MarketplaceRate.pdf; data for 2017 are available from Centers for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period Final Open Enrollment Report,” March 15, 2017, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-03-15.html.

[13] Bob Herman, “Florida Blue Increases Obamacare Profits,” Axios, April 3, 2017, https://www.axios.com/florida-blue-increases-profits-under-obamacare-2338273526.html.

[14] Bob Herman, “How Some Blues Made the ACA Work While Others Failed,” Modern Healthcare, October 15, 2016, http://www.modernhealthcare.com/article/20161015/MAGAZINE/310159989 and Tom Dennis, “Tim Huckle Interview: Obamacare and North Dakota Nice,” Grand Forks Herald, November 27, 2016, http://www.grandforksherald.com/opinion/op-ed-columns/4167359-tim-huckle-interview-obamacare-and-north-dakota-nice.

[15] JoNel Aleccia, ‘“It’s Not Like Other States’: High-Cost Alaska Sits in the Eye of Health Reform Storm,” Kaiser Health News, April 5, 2017, http://khn.org/news/its-not-like-other-states-high-cost-alaska-sits-in-the-eye-of-health-reform-storm/. Note that Alaska’s state-sponsored reinsurance program had not yet taken effect in 2016.

[16] Jayne O’Donnell, “Obamacare was profitable for some insurers despite public comments,” USA Today, December 4, 2016, https://www.usatoday.com/story/news/politics/2016/12/04/obamacare-profitable-some-insurers-despite-public-comments/94732188/.

[17] Kristen Schorsch, “Blue Cross Parent Stops the Bleeding, But at What Cost?” Modern Healthcare, March 14, 2017, http://www.modernhealthcare.com/article/20170314/NEWS/170319958.

[18] Center on Budget and Policy Priorities, “Sabotage Watch: Tracking Efforts to Undermine the ACA,” updated April 14, 2017, https://www.cbpp.org/sabotage-watch-tracking-efforts-to-undermine-the-aca.

[19] Kaiser Family Foundation, “Estimates: Average ACA Marketplace Premiums for Silver Plans Would Need to Increase by 19% to Compensate for Lack of Funding for Cost-Sharing Subsidies,” April 6, 2017, http://kff.org/health-reform/press-release/estimates-average-aca-marketplace-premiums-for-silver-plans-would-need-to-increase-by-19-to-compensate-for-lack-of-funding-for-cost-sharing-subsidies/?utm_campaign=KFF-2017-April-Web-Briefing-ACA-Cost-Sharing-Subsidies&utm_source=hs_email&utm_medium=email&utm_content=50113735&_hsenc=p2ANqtz--ETCChd1Smzc8fbJmgZgEqu8F8u2CUK4nJ8yTyQF5B-ssWnZ6Qcz2Ma3spizILL25hgmJKrdgz3x17hs1A4s3NHbgvkw&_hsmi=50113735.

[20] Bob Bryan, “One of the Nation’s Biggest Health Insurers Is Ditching Iowa’s Obamacare Exchanges,” Business Insider, April 6, 2017, http://www.businessinsider.com/aetna-leaving-iowa-obamacare-exchange-marketplace-2017-4 and Tony Leys, “Wellmark to Halt Sales of Individual Health Insurance Policies,” Des Moines Register, April 3, 2017, http://www.desmoinesregister.com/story/news/health/2017/04/03/wellmark-halt-sales-individual-health-insurance-policies/99994906/.

[21] Letter to President Trump from America’s Health Insurance Plans, Blue Cross Blue Shield Association, American Academy of Family Physicians, American Medical Association, American Hospital Association, Federation of American Hospitals, American Benefits Council, and the Chamber of Commerce, April 12, 2017, https://ahip.org/wp-content/uploads/2017/04/Joint-CSR-Letter-to-President-Trump-04.12.2017.pdf.

[22] Sarah Kliff, “Insurance Regulators Are Panicked About Obamacare’s Future,” Vox, April 10, 2017, http://www.vox.com/policy-and-politics/2017/4/10/15247724/obamacare-future-marketplaces and Letter to Secretary Price from Insurance Commissioner Mike Kreidler and the Association of Washington Healthcare Plans, April 8, 2017, https://www.insurance.wa.gov/current-issues-reform/affordable-care-act/documents/Kreidler-AWHP-letter-HHSSec-TomPrice.pdf.

More from the Authors