Meeting the Goals of the Federal Tax System

Testimony of Jared Bernstein, Senior Fellow, Before the Joint Economic Committee

Thank you very much for the invitation to testify. Today’s hearing is nominally about the complexity in the tax code, but we cannot adequately address that issue without asking a broader question: what is the goal of the federal tax system? To underscore this point, consider a simple, flat tax code wherein filing taxes took minutes instead of hours yet significantly increased the tax burden on the broad middle class. I suspect such “simplicity” would be unacceptable to members of this committee.

The goal of the system should be to raise the revenue necessary to fund the government services and public goods Americans want and need, and to do so in a way that’s fair, equitable, pro-growth, and avoids unnecessary complexity.

- An equitable tax code is a progressive one with rates that rise with income so as to reduce, as opposed to exacerbate, market-driven inequalities.

- A tax code that privileges some types of income over others, contains unnecessary exemptions and deductions, and offers numerous opportunities for tax avoidance and evasion is unfair, wasteful, and too complex.

- A pro-growth tax code raises ample revenue to provide households and businesses with the infrastructure and security they need to prosper, and does so in ways that best promote work and investment. Moreover, the relationship between taxes and growth is not simplistic: the empirical record shows strong growth periods amidst higher tax rates and weak growth periods amidst lower tax rates.

In what follows, I evaluate the extent to which the current U.S. federal tax code meets these criteria and where it falls short. I also offer suggestions to boost its fairness, simplicity, growth, and revenue-adequacy objectives.

My three main findings are:

- Fairness, simplicity, and revenue raising are often complementary: by closing regressive loopholes in the tax code, we reduce incentives to game the system, eliminate wasteful tax breaks that exacerbate inequality without promoting growth, and raise more revenues.

- Based on demographics, inflation, debt service, and rising health costs (though measures in the Affordable Care Act have helped to slow that growth rate), a sustainable fiscal policy will likely require more, not less, revenues going forward.

- I find no evidence to support the claim that supply-side tax cuts come anywhere close to paying for themselves or are even particularly pro-growth.

Tax Fairness and Tax Complexity: How Can We Have More of the Former and Less of the Latter?

Complexity has nothing to do with the number of tax brackets and rates.Policymakers and taxpayers often lament the complexity of the tax code, and with good reason. But it’s important to remember that complexity has nothing to do with the number of tax brackets and rates. If taxable income were easy to define, it wouldn’t matter how many rates existed in the code; all taxpayers would have to do is look up their liabilities in a table or online calculator. Any computation, including one based on dozens of rates, would be easily done in the background.

What makes our system so complex are the exemptions, deductions, other tax subsidies, and privileges for one type of income, industry, or activity over another. On the corporate side, these include “transfer pricing” opportunities (the ability to book income in low-tax countries and deductible expenses in high-tax countries), deferral of foreign earnings, inversions, and the many other loopholes that explain why the effective corporate rate is at least 10 percentage points below the top statutory rate (about 25 percent versus 35 percent).

To be clear, not all subsidies in the tax code are poorly targeted and inefficient. Research shows the Earned Income Tax Credit and Child Tax Credit, for example, encourage work and prevent millions of people from falling into or deeper into poverty, and children in families receiving the tax credits do better in school, are likelier to attend college, and can be expected to earn more as adults. But well-targeted, effective subsidies like the EITC and CTC are unfortunately more the exception than the rule.

I asked one very busy and experienced tax preparer, “What makes filing taxes complicated?” She responded that blaming “too many rates” was “gut-busting laughable.” Once you determine taxable income, calculating liabilities takes seconds. “But,” she went on, “how much time do I, a seasoned professional with great software and lots of research resources, spend dealing with the complexities of the tax code? Too often, it’s hours and hours (and I can’t often bill for it).”[1]

A flat tax (one rate), though often touted as the pinnacle of simplicity, could be immensely complex if taxpayers have to spend hours categorizing different types of income, taking deductions, and so on before applying the rate to their taxable income.

When a particular income source is privileged by the tax code, people and businesses are incentivized to spend considerable time and money redefining their income as coming from the privileged source. Such complexities in the tax code may thus create jobs for tax lawyers, but they often don’t contribute to productive activities. They also often reduce fairness and erode the tax base.

Consider:

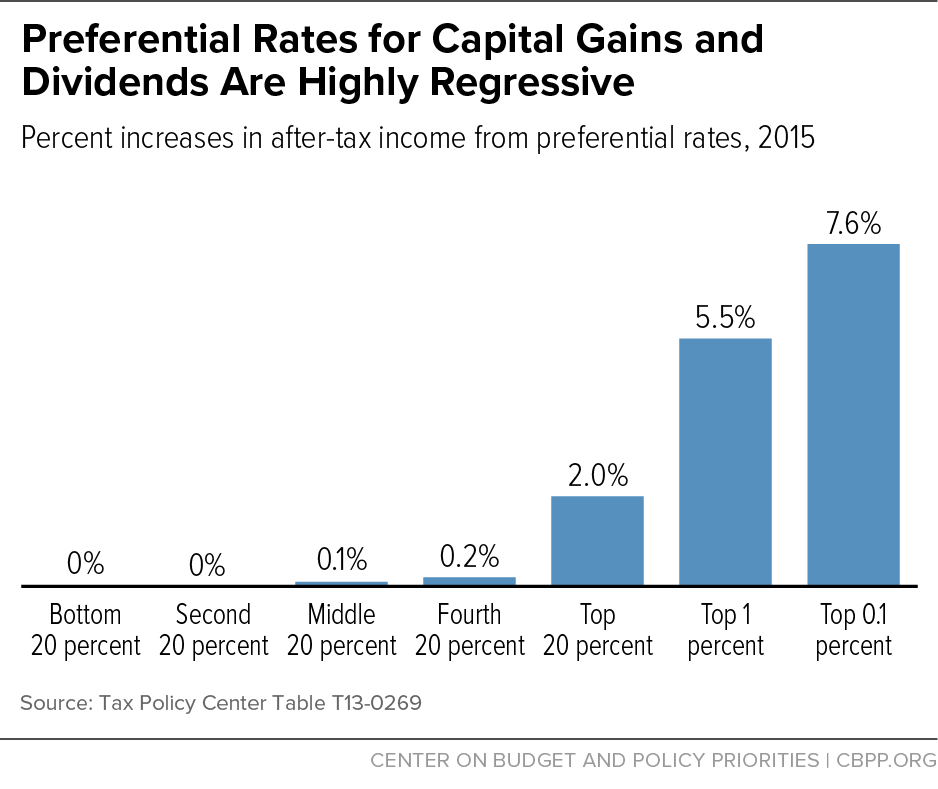

- Preferential rates for investment income (capital gains, dividends) mostly benefit the wealthy, who receive a disproportionate share of non-labor income. As the figure below shows, lower rates for these income sources have virtually no impact on those in the bottom 80 percent but raise the post-tax income of the wealthiest families by about 5 to 8 percent, thus exacerbating market-driven income inequalities.

Figure 1

- Our tax code heavily favors very high levels of inherited incomes. Due to the high exemption threshold ($10.9 million for couples, $5.4 million for individuals), our current estate-tax base is extremely narrow, reaching only 2 of every 1,000 estates. Numerous loopholes also ensure that the millionaires who do pay the estate tax pay low effective rates (on average, less than 17 percent) on their fortunes. And then there’s “step-up basis,” which wipes out the taxes on capital gains (already taxed at a privileged rate relative to earned income) when a wealthy individual passes them on to a descendant.

- On the corporate side of the tax code, many of the loopholes cited above explain why the effective corporate tax rate is at least 10 percentage points below the top statutory rate (35 percent). As noted, a source of this difference is the ability to indefinitely defer foreign earnings. The huge differential between how the code treats debt- and equity-financed investment is underappreciated but also important. Because interest payments, unlike dividend payments, are deductible from corporate income, the effective marginal tax rate on debt-financed investment is minus 39 percent. The rate on equity financing for corporations is 27 percent (see Figure 2 here). In other words, there is a very large subsidy for debt-financed investment; it’s little wonder that American businesses are prone to excessive leverage.

- Business income “passed through” to the individual level (to take advantage of the lower tax rate on capital gains) is the single largest source of the “tax gap” (the difference between what people owe and what they pay). When last measured for the year 2006, the tax gap amounted to some $385 billion a year, or about 10 percent of the federal budget and 2 percent of today’s GDP. Sole proprietors, for example, have been found to report less than half of their income to the IRS.

- In research that has become especially topical with the discovery of extensive tax evasion in Panama, economist Gabriel Zucman documents that, since the early 1980s, the share of profits that U.S.-based firms book in tax havens has grown from about 20 percent to 50 percent. New analysis by Kimberly Clausing “suggests that base erosion and profit shifting is a larger problem today than even before.” She estimates the revenue loss from such activities to be between $77 billion and $111 billion by 2012, about 4 percent of federal revenues that year.[2]

- Further evidence of increasingly aggressive profit shifting is easily gleaned from the amount of income that U.S.-based multinationals book in tax havens known for their extremely low-tax rates. As a joint report from the White House and the U.S. Treasury recently reported, in 2010, foreign subsidiaries of U.S. firms “reported profits in the Cayman Islands that were more than 20 times that country’s entire economic output.”[3] This simple fact alone provides overwhelming evidence of base-eroding profit shifting from where income is earned to where it will be least taxed.

- As Austin, Burman, and Rosenthal show in a forthcoming paper, the share of corporate stock held in taxable household accounts has fallen from around 80 percent in the mid-1960s to about 25 percent now, meaning most such stock is now untaxed by U.S. authorities or held in tax-favored vehicles like individual retirement accounts or by nonprofits or foreigners.

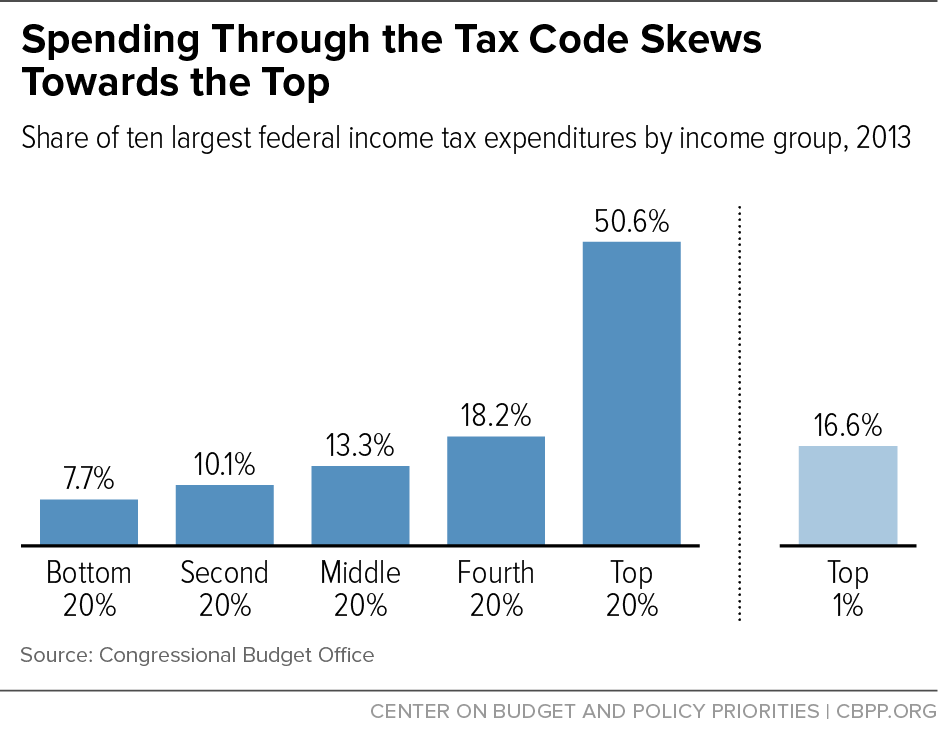

All told, the extensive set of legal subsidies to individuals or businesses through exemptions, deductions, and other tax subsidies, generally referred to as tax expenditures, cut federal income tax revenue by over $1.2 trillion last year — more than the cost of Social Security or the combined cost of Medicare and Medicaid. Moreover, as shown in the figure below, these tax breaks disproportionately benefit higher-income households, often wastefully subsidizing behavior that would occur anyway. The top 1 percent of households get almost 17 percent of the benefit of the ten largest tax expenditures, almost as much as the bottom 40 percent of households.

Why do all of these loopholes, deductions, and favorable rates exist? One explanation, often proffered with no supporting evidence, is that these complexities create incentives for growth. In some cases, such claims are prima facie indefensible. Step-up basis, for instance, encourages wealthy individuals to hold assets until death even if the gains from selling the assets might be more productively deployed elsewhere in the economy. As another example, the huge discrepancy in the tax cost of debt financing versus equity financing has no obvious growth justification. And the fact that it’s cheaper, from an effective-tax-rate perspective, for multinational American companies to create real economic activity abroad rather than here disincentivizes job creation in the United States.

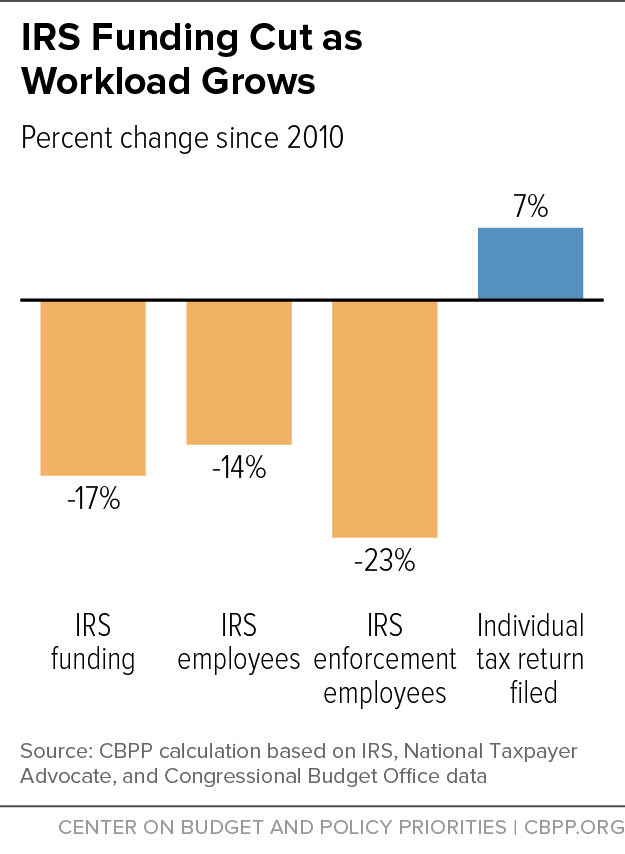

There’s also no defense at all for exacerbating the problem of illegal tax evasion, as congressional conservatives have been doing by cutting the budget of the IRS. As the figure below from CBPP Tax Policy Director Chuck Marr reveals, compared to 2010, the IRS budget is down 17 percent in real dollars and enforcement staffing is down by 23 percent, while individual filings are up 7 percent. Treasury estimates that each additional $1 spent on IRS enforcement yields $6 of additional revenue.

It is therefore essential, in the name of fairness, simplicity, and revenue collection, to curb tax avoidance and evasion. The next section focuses on the revenue issue and the final section examines the fundamental claim of “supply-side” tax cuts: that rate cuts reliably generate significant economic growth. Both theory and evidence find little support for this claim.

Meeting Our Revenue Needs

Even with no policy changes in major government programs, our revenues must increase for “mechanical” reasons. Simply holding real spending per capita constant, population growth and inflation together will require a 40 percent increase in revenues over the next decade. As the share of Americans who are 65 and older will increase from the current 15 percent to 20 percent by around 2040, Medicare and Social Security will cost more. CBO estimates that, by 2026, spending on these two programs will need to go up by just under 2 percent of GDP (over $500 billion of projected 2026 GDP).

Along with demographics, another source of pressure on future revenues is health-care cost growth, which has historically outpaced overall growth, thus absorbing an increasing share of GDP. Clearly, attacking the inefficiencies behind this excess growth rate was a goal of the Affordable Care Act (ACA), and it has been a notable success thus far. Today’s budget projections of health care costs are down 30 percent from those made prior to the ACA, and that improvement includes the costs of the health care reform itself.

Finally, CBO expects interest payments on government debt to rise from 1.4 to 3 percent of GDP over the next decade. Like other forecasters, CBO has overestimated the path of interest rates in recent years, so perhaps, if rates remain as low as forward market indicators expect them to, there will be some debt relief. But the path of future interest rates is unknowable, so fiscal rectitude should lead us to plan for the possibility of rising interest payments.

To meet these needs and leave ourselves room for necessary additional investments in infrastructure and human capital while sticking to the principles outlined above, we should adopt revenue raisers that increase fairness and simplicity (or, at least, that avoid new complexities).

The price of admission to any discussion of tax reform should thus be a willingness to close the so-called “carried interest loophole,” which allows hedge fund managers to face favorable asset-based rates on their earnings at a cost of $19 billion in lost revenue over ten years. Those who claim to want to do major tax reform yet are unwilling to simplify the code by first closing this loophole — one with virtually no defenders — should be considered akin to those who say they’re ready to run a marathon but get winded walking up the stairs.

The preferential treatment of wealthy inheritances would be another great place to start. The President’s recent budget would lower the estate-tax exemption threshold from $10.9 million to $7 million for couples (and from $5.4 million to $3.5 million for individuals) and increase the top marginal estate-tax rate from 40 percent to 45 percent. It would also close a few estate and gift-tax loopholes, one of which (the Grantor Retained Annuity Trust loophole) allows an estate to put an investment in a trust to avoid paying capital gains. Under these changes, which would raise $226 billion over 10 years, the estate tax would still affect only about 0.3 percent of decedents.[4]

In a similar vein, the President’s budget proposes to close the “step-up” loophole discussed above, while leaving in significant exemptions so that the change only affects wealthy heirs. Combined with his proposal to raise the capital gains rate from its current 23.8 percent to 28 percent, ending step-up basis raises $235 billion over ten years. Note that reducing the tax differential between capital gains and income helps to simplify the system as well, by reducing a distortionary incentive to redefine earnings and income (one exploited, for example, by those who tap the carried interest loophole).

When it comes to some of the other wasteful subsidies in the tax code, it’s hard politically to target one over another — behind every loophole is a lobbyist whose salary depends on defending that tax break as a treasured “job creation” program. Rather than go after these loopholes one at a time, it would thus be both easier and fairer to limit all deductions to 28 percent instead of the top income tax rate of almost 40 percent.

This approach avoids picking winners and losers and boosts economic efficiency by reducing the extent to which we subsidize behaviors that would occur anyway among the wealthy, like saving for retirement or buying a home. Applied to incomes of $250,000 or more, this cap would generate savings of more than $640 billion over ten years.

Turning to the corporate side of the tax code, the simplest way to shut down companies’ deferral of foreign earnings is a minimum tax that multinationals must pay on those earnings when they earn them, after which they could repatriate their earnings without further taxation. The Obama administration plugs in 19 percent for this tax, which would raise $350 billion over ten years.[5]

Finally, it is time to raise the federal gas tax. This tax is how we fund both highway infrastructure and the federal contribution to public transit, and it has been stuck at 18.4 cents a gallon in nominal terms since 1993. Meanwhile, the costs of maintenance have gone up, as has vehicle mileage, leading to perennial shortfalls in the Highway Trust Fund. A tax on fossil fuels is also smart environmental policy, and there’s even been some bipartisan support for the idea. One plan would raise the gas tax by 12 cents a gallon over two years (6 cents per year) and then index it to inflation. That would raise $180 billion over ten years. With gas prices still very low, the sooner such an increase goes into effect, the better.

The Non-Relationship Between Supply-Side Tax Cuts and Growth

For decades, some policymakers and economists have maintained that cuts in tax rates will lead to faster growth by raising “supply-side” inputs including labor, capital, and other forms of investment. The argument is that lowering the after-tax cost of investment and raising the after-tax wage will cause the economy’s labor supply and capital investment to go up, boosting productivity and growth. The gains will then trickle down to the jobs and incomes of low- and middle-income people.

There’s a degree of logic to the first part of this claim, but it is woefully incomplete, even in a theoretical sense. Tax economists Bill Gale and Andrew Samwick recently noted three ways in which this simple supply-side theory must be amended.[6]

First, Gale and Samwick point out that, “while there is no doubt that tax policy can influence economic choices, it is by no means obvious … that tax rate cuts will ultimately lead to a larger economy in the long run.” They note the predicted impacts on wages and investing, but go on to stress that tax cuts “would also raise the after-tax income people receive from their current level of activities, which lessens their need to work, save, and invest. The first effect normally raises economic activity (through so-called substitution effects), while the second effect normally reduces it (through so-called income effects).” On net, some empirical research finds substitution effects to dominate income effects, but Gale and Samwick point out that this outcome is often conditional on the design of the tax cut.

Second, they point out that the growth effects of tax cuts also depend on how they are financed: “Tax cuts financed by immediate cuts in unproductive government spending could raise output, but tax cuts financed by reductions in government investment [e.g., in productive infrastructure or human capital] could reduce output.” They add that deficit-financed tax cuts that increase federal borrowing can reduce long-term growth: “The historical evidence and simulation analyses suggest that tax cuts that are financed by debt for an extended period of time will have little positive impact on long-term growth and could reduce growth.”

Finally, Gale and Samwick argue that rate cuts matched with base-broadeners — the central mantra of tax reform — will raise the effective tax rates faced by some households and firms (due, for example, to the elimination of various tax expenditures). Such increases, they argue, will operate “…in a direction opposite to rate cuts and mitigate their effects on economic growth.” Conversely, they entertain the possibility that base-broadening could reallocate “resources from sectors that are currently tax-preferred to sectors that have the highest economic (pre-tax) return, which should increase the overall size of the economy.”

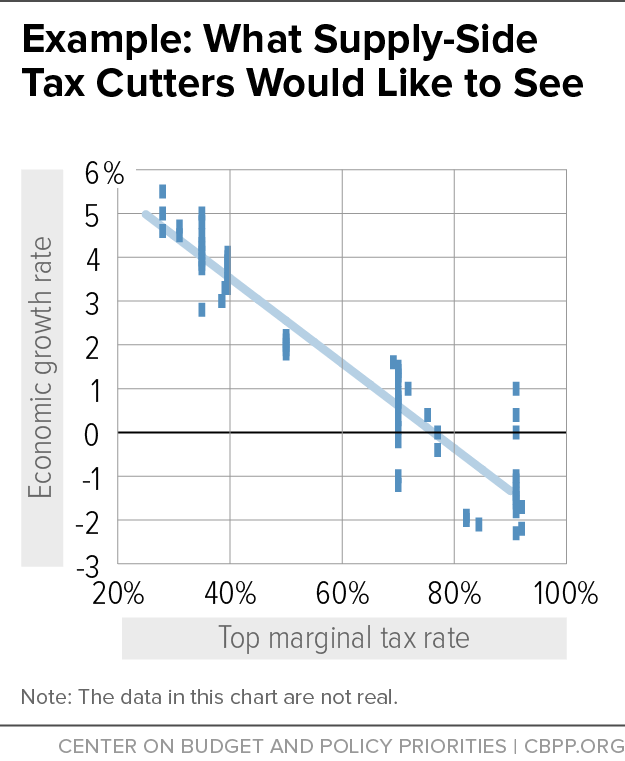

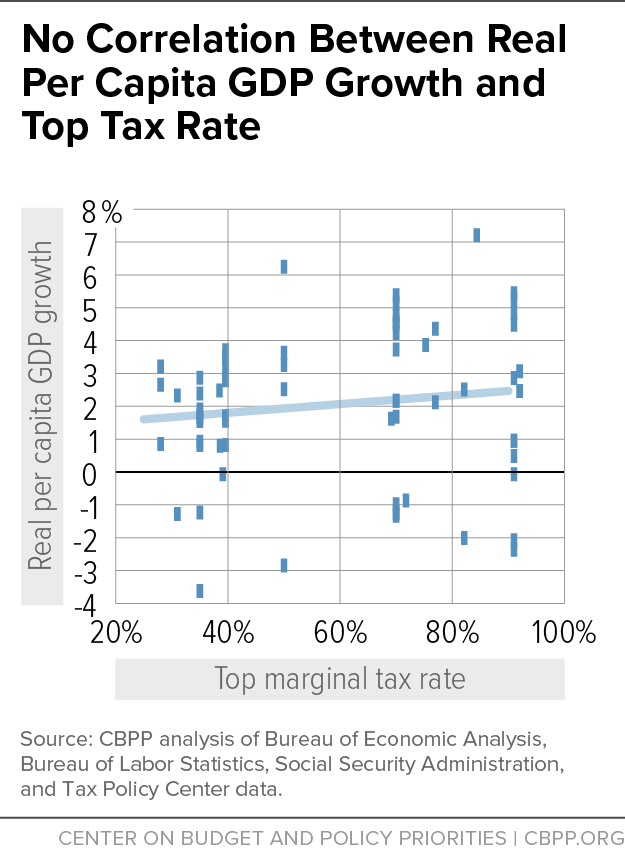

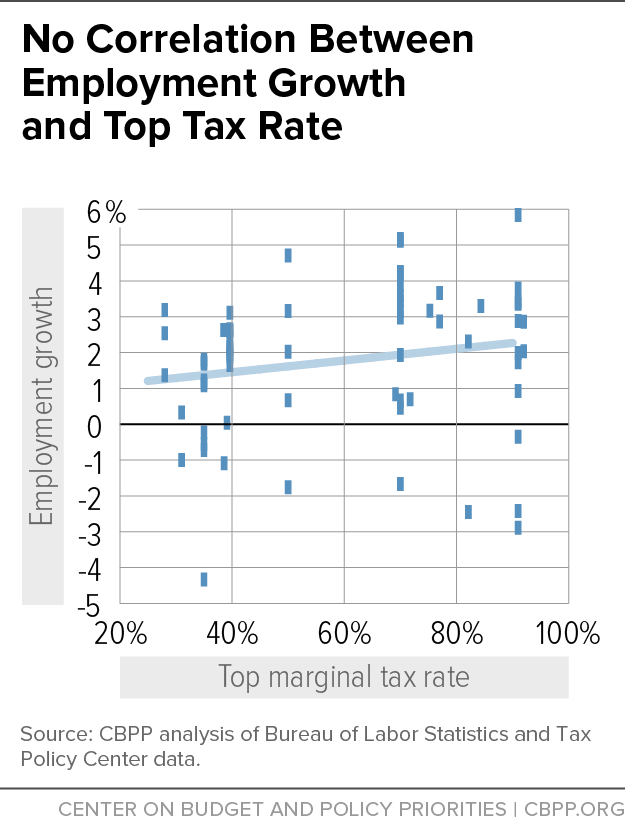

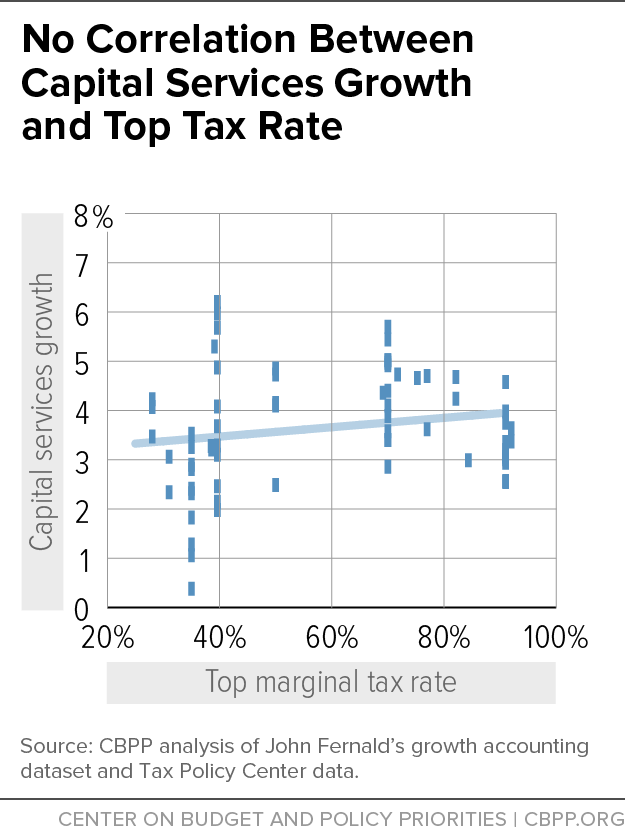

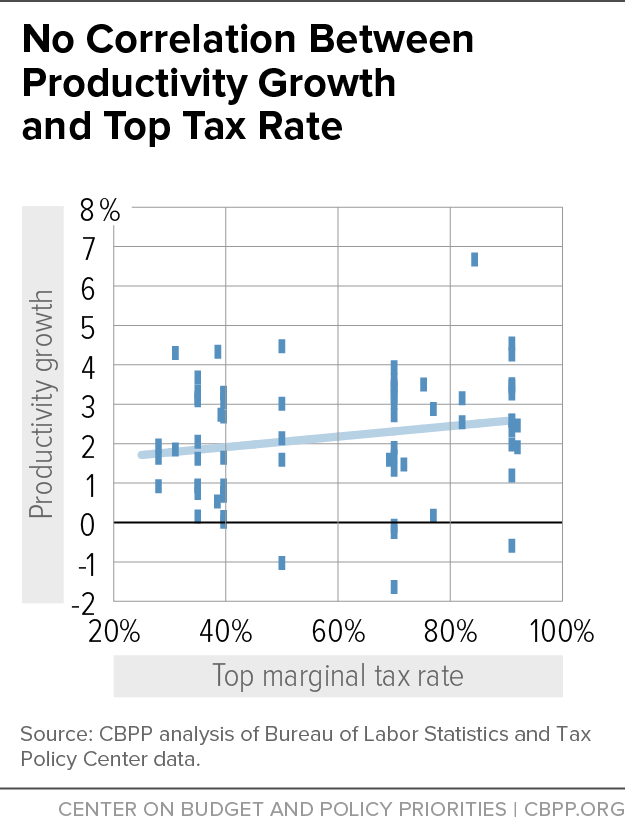

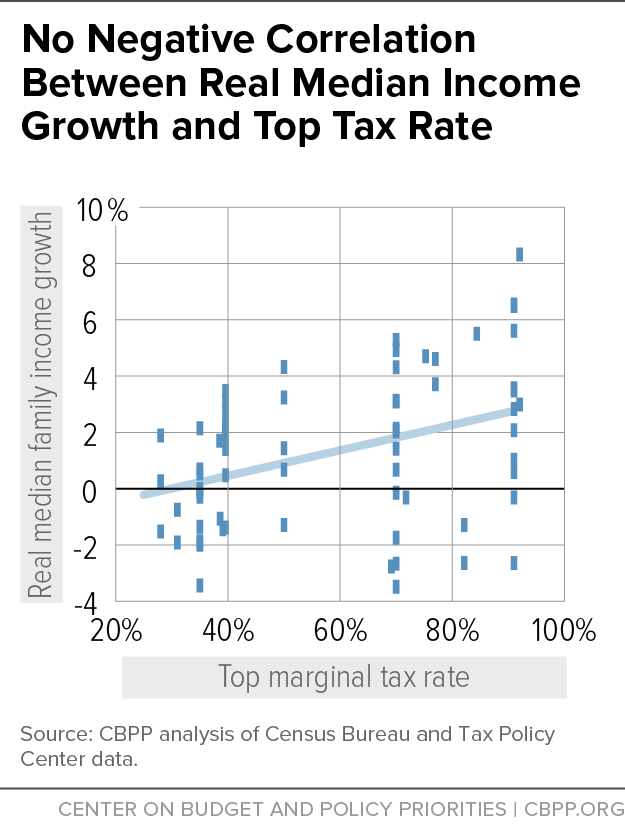

Given these considerations, the claim that supply-side tax cuts boost investment, jobs, and GDP growth, like any economic theory, must be empirically scrutinized. One simple way to do so is to make scatterplots of the top tax rate in a given year against the growth in the economic variables that those rates are supposed to push up. If the theory is correct, high top marginal rates should be associated with weaker growth and low top marginal rates with stronger growth — that is, we’d expect the dots on the scatterplot to line up as they do in the next figure, showing a made-up inverse relationship between rates and growth, just to give a reference point by which to judge the following plots.

Unfortunately for supply-side theory, the actual graphs, as opposed to the above imaginary one, do not reveal this pattern at all. The five scatterplots below plot the annual percentage change in real per capita GDP, employment, capital investment, productivity, and pretax median family income (respectively) relative to top marginal rates, with annual data running from 1947 to the most recent observation (2014 or 2015). In each case, the top marginal rate is plotted on the X-axis against the percent change in the variable in question on the Y-axis. A “best-fit” line is plotted through the dots.

In no case is the relationship negative, as predicted by supply-side theory. To the contrary, the slope of the regression line tends to be positive, though its rise is too mild to be statistically significant (with the exception of pretax median family income).

To be clear, these graphs do not show that higher tax rates promote investment, growth, and jobs. First, as noted above, the impact of tax cuts on growth is conditional on numerous factors, including the tradeoff between income and substitution effects, how the cuts are financed, changes in effective rates, and, I’d add, broader economic conditions (for example, temporary tax cuts for low- and middle-income people are likely to be growth-inducing during recessions through demand-side impacts).

Second, the factors that determine growth and its supply-side inputs are many and varied, including demographics, “innovation” (total factor productivity, or output growth net of all relevant inputs), monetary policy, other fiscal policies, and much more, including intangibles such as “animal spirits” and consumer confidence.

But the fact that the simple empirical record is uniformly hostile to the supply-side story, coupled with that story’s theoretical shortcomings, should put the burden of proof squarely on those arguing that supply-side tax cuts will be pro-growth.

Piketty, Saez, and Stantcheva have developed evidence similar to that above using cross-country variation. Looking at numerous economies between 1960 and 2010, they show that cuts in top marginal rates were not associated with faster per capita income growth. Instead, they were negatively and significantly correlated with a greater share of national income accruing to the top 1 percent. That is, supply-side tax cuts didn’t raise growth; they raised inequality.[7]

Evidence at the sub-national level — where various states, led by Kansas, have been aggressively cutting taxes while policy officials tout the benefits of supply-side tax cuts — also tilts strongly against tax cuts as a growth strategy. The cuts in Kansas that took effect in 2013, for example, have now blown a $400 million hole in the state’s budget. When one of my fellow witnesses, Art Laffer, helped design these cuts, he predicted (along with Stephen Moore of the Heritage Foundation) that they would provide an “immediate and lasting boost” to the Kansas economy. Yet not only have the cuts caused serious underfunding of the state’s education system, they’ve also coincided with weak job and GDP growth. The Kansas Legislative Research Department’s projections suggest that the economy will remain weaker than the overall US economy for the foreseeable future.

Advocates of supply-side theory may argue that the benefits of the cuts are just taking longer to appear than they originally predicted, but based on the wealth of empirical evidence shown here and in other analyses I’ve cited, policymakers would be wise to reject such arguments.

Conclusion

The goal of a tax code in an advanced economy must to be raise ample revenues in ways that are efficient, pro-growth, and, perhaps most importantly, widely perceived as fair. Complexity is not a function of the number of rates; it is driven by the spate of deductions, credits, exemptions, and myriad other opportunities to avoid taxes through complicated redefinitions of income into forms given preferential treatment by the code.

Of course, our economic lives can themselves be complex, and the tax code will inevitably reflect them to some degree. We very much want, for example, to both prevent poverty and incentivize work among the least well off, and the work-based refundable credits mentioned above have a been a highly successful tax expenditure. In fact, there is bipartisan support to increase the EITC for childless adults, who current receive only a very small amount from that worthy program.

We should, however, pursue changes that constitute a “three-fer” by simultaneously boosting revenues, fairness, and simplicity. That means adequately funding the IRS, closing the many loopholes identified in this testimony, and avoiding the supply-side tax cuts that cut strongly against fairness and progressivity with little to nothing to show for them in the way of economic growth. If we do that, we’ll have a much-improved tax code.

Data Note

Each data point in each chart represents a calendar year. The top federal marginal income tax rate (from the Tax Policy Center) is on the X-axis of each chart; the Y-axes represent the growth, from one year prior, of the variables in question. Productivity is for the nonfarm business sector; real capital services come from economist John Fernald’s growth accounting dataset; GDP has been adjusted for both inflation and population size; and the 2013 value for real median family income (Census Bureau) has been imputed because of changing survey methods.

While these charts only show the non-relationship between top marginal tax rates and contemporaneous economic activity, looking two, three, or four years out does not change the findings. In fact, longer lags often lead to an increased positive correlation with higher top marginal tax rates, a result that stands in direct contrast to what tax cut proponents typically predict.

End Notes

[1] Personal correspondence with Mary Ellen Arndorfer.

[2] Kimberly Clausing, The Effect of Profit Shifting on the Corporate Tax Base in the United States and Beyond,” 2016, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2685442.

[3] The President’s Framework For Business Tax Reform: An Update, April 2016, https://www.treasury.gov/resource-center/tax-policy/Documents/The-Presidents-Framework-for-Business-Tax-Reform-An-Update-04-04-2016.pdf.

[4] I discuss these and some of the other suggested revenue raisers in this section in a recent American Prospect article: “We’re going to need more revenue,” Vol 27, #2, Spring 2016.

[5] Don’t conflate this minimum tax on foreign earnings with a repatriation tax holiday. That’s a big money loser, as it allows multinationals to bring foreign earnings home from abroad at a much reduced rate, only to start storing them overseas again once the “holiday” has expired (note also that some foreign earnings are merely “booked” abroad to tap the benefits of deferral, but are already accessed by the US parent company). JCT scores tax repatriation as costing about $100 billion over 10 years. A tax holiday cannot constitute a “pay-for” for infrastructure investment (or anything else), as is often suggested, because it is a revenue loser in the long run.

Instead, “deemed” or compulsory repatriation as part of a transition to a more efficient international tax regime would be a very sensible source of income for a sizable, one-time infrastructure investment. Under any transition, there needs to be a process for dealing with the large stock on deferred earnings that is currently booked abroad, which is thought to be in the neighborhood of $2 trillion. The common approach is a one-time transition tax. President Obama’s proposal calls for a 14 percent transition tax, yielding over $200 billion that could be applied to infrastructure investment.

[6] “Effects of Income Tax Changes on Economic Growth,” by William Gale and Andrew Samwick, February 2016.

[7] One possible explanation is that at higher tax rates, the wealthiest individuals bargain less aggressively for higher pretax compensation (since they’ll be able to keep less of each marginal dollar they earn). See Bivens and Mishel (2013): https://www.aeaweb.org/articles?id=10.1257/jep.27.3.57.