Testimony: Iris Lav, Senior Advisor, Before the House Oversight Committee Subcommittee on TARP, Financial Services and Bailouts of Public and Private Programs

Mr. Chairman, Mr. Quigley, and members of the committee, I appreciate the invitation to appear before you today.

A spate of recent articles regarding the fiscal situation of states and localities have lumped together their current fiscal problems, stemming largely from the recession, with longer-term issues relating to debt, pension obligations, and retiree health costs, to create the mistaken impression that drastic and immediate measures are needed to avoid an imminent fiscal meltdown. That is far from true.

Operating Deficits

States are projecting large operating deficits for the upcoming 2012 fiscal year, totaling about $125 billion in aggregate. These deficits, which states have to close before the fiscal year begins (on July 1 in most states), are caused largely by the weak economy. State revenues have stabilized and in some states resumed at least weak growth after record losses, but they remain 12 percent below pre-recession levels after adjustment for inflation. Localities also are experiencing diminished revenues. At the same time that revenues have declined, the need for public services has increased due to the rise in poverty and unemployment. Over the past three years, states and localities have used a combination of reserve funds and federal stimulus funds, along with budget cuts and tax increases, to close these recession-induced deficits.

As states release their proposed budgets, we find that nearly all states are proposing to spend less money than they spent in 2008 (after inflation), even though the cost of providing services will be higher. Most state spending goes toward education and health care, and in the 2012 budget year, there will be more children in public schools, more students enrolled in public colleges and universities, and more Medicaid enrollees in 2012 than there were in 2008. But among 26 states that have to date released the necessary data, 21 states plan to spend less in 2012, after inflation, than they did in 2008, and only two — Alaska and North Dakota — expect to spend significantly more. Total proposed spending would be over 10 percent below 2008 levels, after adjustment for inflation. Many of the budget cuts are reducing core services — in K-12 education, higher education, and health care.[1]

There are three primary reasons for the deep cuts.

Revenues remain weak, as noted above.

- Costs are rising. In the 2011-12 school year there will be about 260,000 more public school students and another 960,000 more public college and university students than in 2007-08, for example. Some 4 million more people are projected to receive subsidized health insurance through Medicaid in 2012 than were enrolled in 2008, as employers have cancelled their coverage and people have lost jobs and wages.

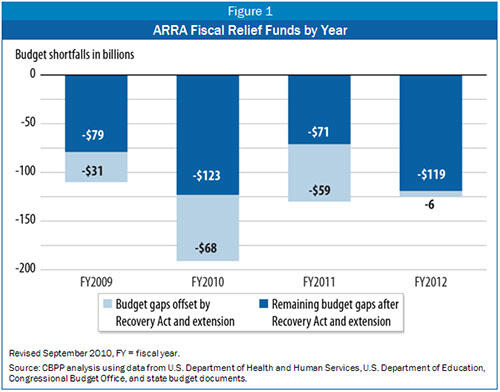

- Federal aid is ending. The fiscal relief provided through the American Recovery and Reinvestment Act of 2009 has been enormously helpful in allowing states to avert some of the most harmful potential budget cuts. States have used emergency fiscal relief from the federal government to cover about one-third of their budget shortfalls through the current (2011) fiscal year. But only about $6 billion in fiscal relief will be left for fiscal year 2012, a year in which shortfalls will total at least $125 billion. (See Figure 1.) That is, the remaining fiscal relief will cover less than five percent of state budget shortfalls next year.Imagen

It is worth saying a few more words about the role of the ARRA funding. ARRA initially provided about $140 billion in fiscal relief through increased federal matching rates for state Medicaid spending and through a new State Fiscal Stabilization Fund, primarily targeted at education.

- A little less than $50 billion was delivered through the State Fiscal Stabilization Fund. Most of this (more than 80 percent) was targeted to education.

- Roughly $90 billion was delivered through enhanced FMAP, the enhanced federal match for state Medicaid expenditures to help compensate for the large increase in Medicaid enrollees the recession caused.

The August 2010 jobs bill provided approximately another $25 billion in state fiscal relief. It extended ARRA’s enhanced FMAP for two more quarters until June 30, 2011 (about $15 billion), and provided support to help states retain or create education jobs (Education Jobs Fund – $10 billion).

The Government Accountability Office finds that states spent this money as intended.

- GAO has studied how 16 states and DC are spending the fiscal relief provided to states under ARRA, and concluded that states spent the money as intended, to reduce spending cuts and avoid tax increases that would have further slowed the economy.

- “Overall, states reported using Recovery Act funds to stabilize state budgets and to cope with fiscal stresses,” GAO concluded. “The funds helped them maintain staffing for existing programs and minimize or avoid tax increases as well as reductions in services.” [2]

Moreover, state fiscal relief is a very effective form of stimulus.

- Mark Zandi, the chief economist at Moody’s Analytics, estimates that state fiscal relief provides $1.41 in economic activity for every $1 spent.[3]

- The Congressional Budget Office finds that state fiscal relief is one of the most effective of the forms of economic stimulus it studied.[4]

ARRA’s fiscal relief had an immediate impact on state spending decisions when ARRA was enacted in February 2009, when economic activity was declining rapidly. Most states were in the process of developing their budgets for the fiscal year that began in July 2009, and some were considering immediate cuts in their current-year budgets. ARRA’s relief mitigated the spending cuts (and tax increases) states imposed during those crucial first months after ARRA’s passage.

The difficulty of coping with the end of the ARRA funding — which is occurring before the economy has regained sufficient strength and before state revenues have recovered — will be exacerbated if the budget cuts in “non-security discretionary” spending federal policymakers are considering are enacted. These budget cuts would significantly reduce the amount of ongoing federal funding to states. About one-third of the category of the federal budget known as “non-security discretionary” spending flows through state governments in the form of funding for education, health care, human services, law enforcement, infrastructure, and other areas. House leaders have proposed cutting that spending by $40 billion. That would be a 15.4 percent reduction from the level provided in the current continuing resolution for the remainder of the federal fiscal year, which ends in September. This would reduce federal support for services provided through state and local governments, forcing states to make still-deeper cuts in their budgets for next year.

While the economy-induced deficits have caused severe problems and states and localities are struggling to maintain needed services, this is a cyclical problem that ultimately will ease as the economy recovers.

Unlike the projected operating deficits for fiscal year 2012, which require near-term solutions to meet states’ and localities’ balanced-budget requirements, longer-term issues related to bond indebtedness, pension obligations, and retiree health insurance — discussed more fully below and in the attached January 20, 2011 report, Misunderstandings Regarding State Debt, Pensions, and Retiree Health Costs Create Unnecessary Alarm[5]— can be addressed over the next several decades. It is not appropriate to add these longer-term costs to projected operating deficits. Nor should the size and implications of these longer-term costs be exaggerated, as some recent discussions have done. Such mistakes can lead to inappropriate policy prescriptions.

Bond Indebtedness

Some observers claim that states and localities have run up huge bond indebtedness, in part to finance operating costs, and that there is a high risk that a number of local governments will default on their bonds. Both claims are greatly exaggerated.

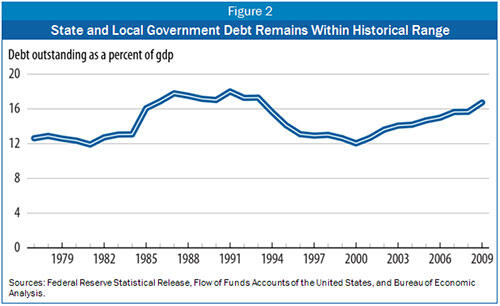

- States and localities have issued bonds almost exclusively to fund infrastructure projects, not finance operating costs, and while the amount of outstanding debt has increased slightly over the last decade it remains within historical parameters. (See Figure 2.) Recently, the Build America Bond provisions of the Recovery Act encouraged borrowing for infrastructure building as a way to improve employment; these bonds can only be used to finance infrastructure. Imagen

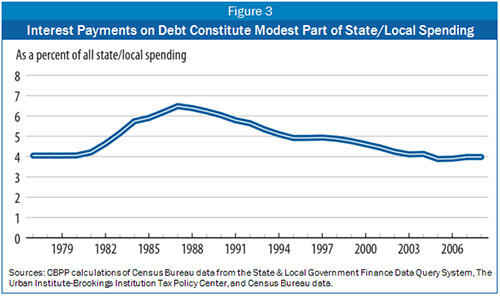

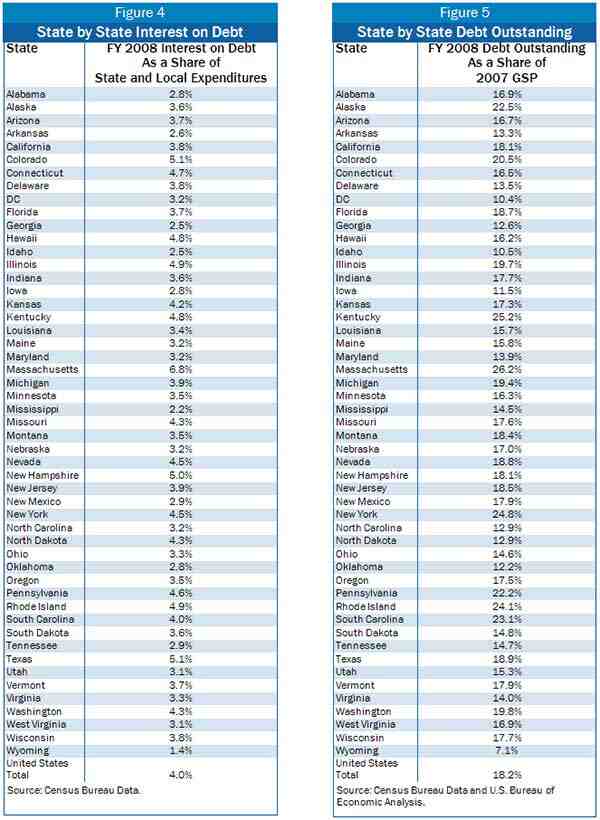

- Interest payments on state and local bonds generally absorb just 4 to 5 percent of current expenditures — no more than they did in the late 1970s. (See Figure 3, and Figures 4 and 5 for state-by-state data on debt outstanding and interest expense.)Imagen

Imagen

Imagen

- Municipal bond defaults have been extremely rare; the three rating agencies calculate the default rate at less than one-third of 1 percent.[6] Between 1970 and 2009, only four defaults were from cities or counties. Most defaults are on non-general obligation bonds to finance the construction of housing or hospitals and reflect problems with those individual projects; they provide no indication of the fiscal health of local governments.

- The person most vociferously proclaiming the potential of defaults in the media has been shown to lack data to back up her claims. Meredith Whitney’s report, which few have seen, apparently does not present evidence substantiating the potential of sizeable defaults. In a recent interview with Bloomberg News, she said “Quantifying is a guesstimate at this point.”[7]

- While some have compared the state and local bond market to the mortgage market before the bubble burst, the circumstances are very different. There is no bubble in state and local bonds, nor are there exotic securities that hide the underlying value of the asset against which bonds are being issued (as was the case with subprime mortgage bonds). Most experts in state and local finance do not expect a major wave of defaults. For example, a Barclays Capital December 2010 report states, “Despite frequent media speculation to the contrary, we do not expect the level of defaults in the U.S. public finance market to spiral higher or even approach those in the private sector.”

Pension Obligations

Some observers claim that states and localities have $3 trillion in unfunded pension liabilities and that pension obligations are unmanageable, may cause localities to declare bankruptcy, and are a reason to enact a federal law allowing states to declare bankruptcy. Some also are calling for a federal law to force states and localities to change the way they calculate their pension liabilities (and possibly to change the way they fund those liabilities as well). Such claims overstate the fiscal problem, fail to acknowledge that severe problems are concentrated in a small number of states, and often promote extreme actions rather than more appropriate solutions.

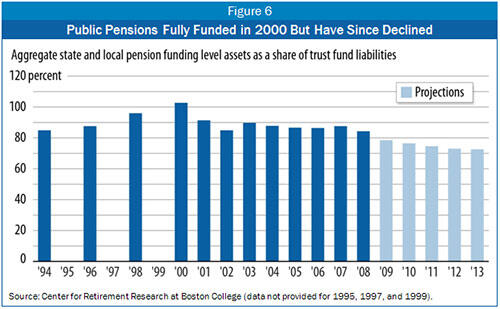

- State and local shortfalls in funding pensions for future retirees have gradually emerged over the last decade principally because of the two most recent recessions, which reduced the value of assets in those funds and made it difficult for some jurisdictions to find sufficient revenues to make required deposits into the trust funds. Before these two recessions, state and local pensions were, in the aggregate, funded at 100 percent of future liabilities. (See Figure 6.)Imagen

- A debate has begun over what assumptions public pension plans should use for the “discount rate,” which is the interest rate used to translate future benefit obligations into today’s dollars. The discount rate assumption affects the stated future liabilities and may affect the required annual contributions. The oft-cited $3 trillion estimate of unfunded liabilities calculates liabilities using what is known as the “riskless rate,” because the pension obligations themselves are guaranteed and virtually riskless to the recipients. In contrast, standard analyses based on accepted state and local accounting rules, which calculate liabilities using the historical return on plans’ assets, put the unfunded liability at about a quarter of that amount, a more manageable (although still large) $700 billion.

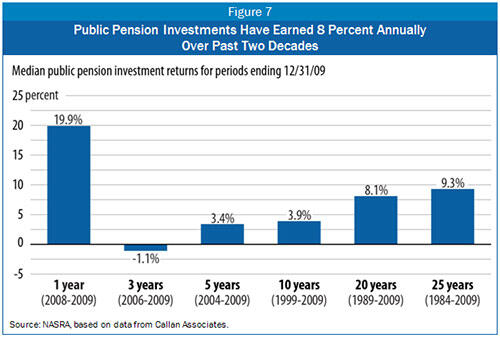

(As described below, the Government Accounting Standards Board is in the process of changing the rules for pension accounting, but they are not moving to using a “riskless rate” for all liabilities.) - Economists generally support use of the riskless rate in valuing state and local pension liabilities because the constitutions and laws of most states prevent major changes in pension promises to current employees or retirees; they argue that definite promises should be valued as if invested in financial instruments with a guaranteed rate of return. However, state and local pension funds historically have invested in a diversified market basket of private securities and have received average rates of return much higher than the riskless rate – 8 percent over the past two decades. And economists generally are not arguing that the investment practices of state and local pension funds should change. (See figure 7.)Imagen

- A key point to understand is that the two issues of how states and localities should value their pension liabilities and how much they should contribute to meet their pension obligations are not the same. The $3 trillion estimate of unfunded liabilities does not mean that states and localities should have to contribute that amount to their pension funds, since the funds very likely will earn higher rates of return over time than the Treasury bond rate, which will result in pension fund balances adequate to meet future obligations without adding the full $3 trillion to the funds. In fact, two of the leading economists who advocate valuing state pension fund assets at the riskless rate have observed, “…the question of optimal funding levels…is entirely separate from the valuation question.”[8] The required contributions to state and local pension funds should reflect not just on an assessment of liabilities based on a riskless rate of return, but also the expected rates of return on the funds’ investments, as well as other practical considerations. As a result, it is mistaken to portray the current pension fund shortfall as an unfunded liability so massive that it will lead to bankruptcy or other such consequences.

- States and localities devote an average of 3.8 percent of their operating budgets to pension funding.[9] In most states, a modest increase in funding and/or sensible changes to pension eligibility and benefits should be sufficient to remedy underfunding. (The $700 billion figure implies an increase on average from 3.8 percent of budgets to 5 percent of budgets, if no other changes are made to reduce pension costs.[10]) However, in some states that have grossly underfunded their pensions in past years and/or granted retroactive benefits without funding them — such as Illinois, New Jersey, and Pennsylvania (and to a somewhat lesser extent Colorado, Kentucky, Kansas, and California) — additional measures are very likely to be necessary.

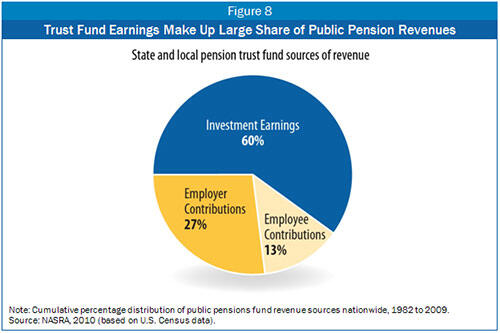

- States and localities have managed to build up their pension trust funds in the past without outside intervention. They began pre-funding their pension plans in the 1970s, and between 1980 and 2007 accumulated more than $3 trillion in assets. There is reason to assume that they can and will do so again, once revenues and markets fully recover. Imagen

- States and localities have the next 30 years in which to remedy any pension shortfalls. As Alicia Munnell, an expert on these matters who directs the Center for Retirement Research at Boston College, has explained, “even after the worst market crash in decades, state and local plans do not face an immediate liquidity crisis; most plans will be able to cover benefit payments for the next 15-20 years.”[11] States and localities do not need to increase contributions immediately, and generally should not do so while the economy is still weak and they are struggling to provide basic services.

Retiree Health Insurance

Observers claiming that states and localities are in dire crisis typically add to unfunded pension liabilities about $500 billion in unfunded promises to provide state and local retirees with continued health coverage. These promises are of a substantially different nature than pensions, however, so it is inappropriate to simply add the two together.

- While pension promises are legally binding, backed by explicit state constitutional guarantees in some states and protected by case law in others, retiree health benefits generally are not. States and localities generally are free to change any provisions of the plans or terminate them entirely.

- States’ retiree health benefit plans differ widely. For example, 14 states pay the entire premium for retirees participating in the health plan, while 14 other states require retirees to pay the entire premium. States clearly have choices in the provision of retiree health benefits.

- With health care costs projected to continue to grow faster than GDP and faster than state and local revenues, it is highly likely that current provisions for retiree health insurance will be scaled back. Many states are likely to decide that their current plans are unaffordable and move to modify them.

- This would be a good time for states and localities offering the more generous plans to decide whether they want to maintain and fund these liabilities, or whether they want to substantially reduce their liabilities by changing the provisions of their plans.

Avoid Changes that Could Harm Fiscal Conditions

Given the different origins, scope, and potential solutions to problems in each of these areas, calls for a “global” solution — such as recent proposals to allow states to declare bankruptcy or to limit their ability to issue tax-exempt bonds unless they estimate pension liabilities using a riskless discount rate — make little sense in the real world of state and local finances.

For example, some people have suggested enacting federal legislation that would allow states to declare bankruptcy, potentially enabling them to default on their bonds, pay their vendors less than they are owed, and abrogate or modify union contracts.[12] Such a provision could do considerable damage, and the necessity for it has not been proven.

As discussed above, states have a strong track record of repaying their bonds. In most states, bonds are considered to have the first call on revenues; debt service will be paid before any public services are funded. (In California, education has the first call on revenues because of the provisions of a ballot initiative, but bonds are right behind.)

There are no modern instances of a state defaulting on its general obligation debt. One has to reach back to the period before and during the Civil War, when several states defaulted, or the single state that defaulted during the Great Depression (Arkansas), to find examples.

It would be unwise to encourage states to abrogate their responsibilities by enacting a bankruptcy statute. States have adequate tools and means to meet their obligations. The potential for bankruptcy would just increase the political difficulty of using these other tools to balance their budgets, delaying the enactment of appropriate solutions. In addition, it could push up the cost of borrowing for all states, undermining efforts to invest in infrastructure.

Another proposal would require states and localities to report their pensions liabilities to the federal government using the so-called “riskless rate” described above.[13] Jurisdictions that did not comply would not be allowed to issue tax-exempt bonds.

As discussed above, analysis of liabilities using the riskless rate can cause confusion about the amounts states and localities actually have to deposit to meet their responsibilities. It would create a lot of paperwork, but could result in less transparency rather than more because of the potential for confusion.

Such a requirement also is not necessary. For the last couple of years, the Governmental Accounting Standards Board (GASB) has been working on a standard for state and local pension reporting that balances the need for consistent disclosure across jurisdictions and the appropriate recognition of risk with the need to accurately assess the contributions required to fund the systems. The GASB process has included widespread participation of interested parties, and GASB is close to finalizing a rule. While GASB standards do not have the force of law, state and local governments generally adhere to them in their financial reports — largely because bond rating agencies look askance at governments that do not.

Thus state and local pension reporting will change in the near future, and will become more standardized across jurisdictions and more transparent, and will change with respect to the way risk is recognized. Federal intervention at this time is not needed, and could harm the ability of states to adopt the new GASB standards by requiring yet a different calculation for federal reporting.

Indeed, these and similar proposed solutions could worsen states’ long-term fiscal picture by undermining their ability to invest in infrastructure and meet their residents’ needs for education, health care, and human services. What are needed are targeted solutions that are appropriate to each state and to the nature of its fiscal problems, not federal intervention.

End Notes

[1] Michael Leachman, Erica Williams, and Nicholas Johnson, Governors are Proposing Further Deep Cuts in Services, Likely Harming Their Economies, Center on Budget and Policy Priorities, Updated February 7, 2011.

[2] GAO, “Recovery Act: States’ and Localities’ Current and Planned Uses of Funds While Facing Fiscal Stresses,” July 8,

2009. More recent GAO reports on ARRA fiscal relief spending in these states has reached similar conclusions.

[3] See http://www.economy.com/mark-zandi/documents/Final-House-Budget-Committee-Perspectives-on-the-US-Economy-070110.pdf

[4] http://www.cbo.gov/ftpdocs/119xx/doc11975/11-24-ARRA.pdf

[5] Iris J. Lav and Elizabeth McNichol, Misunderstandings Regarding State Debt, Pensions, and Retiree Health Costs Create Unnecessary Alarm, Center on Budget and Policy Priorities, January 20, 2011.

[6] Chris Hoene, “Crying Wolf about Municipal Defaults,” National League of Cities blog, December 22, 2010, http://citiesspeak.org.

[7] Max Abelson and Michael McDonald, Whitney Municipal-Bond Apocalypse Short on Specifics, Bloomberg, February 1, 2011. http://www.bloomberg.com/news/2011-02-01/whitney-municipal-bond-apocalypse-is-short-on-default-specifics.html

[8] Robert Novy-Marx and Joshua Rauh, “Public Pension Promises: How Big Are They and What Are They Worth?” Journal of Finance, forthcoming (posted October 8, 2010 on Social Science Research Network), p. 5.

[9] Data are for 2008, the most recent year available from Census.

[10] Alicia H. Munnell, Jean-Pierre Aubry, and Laura Quinby, The Impact of Public Pensions on State and Local Budgets, Center for Retirement Research at Boston College, October 2010.

[11] Alicia H. Munnell, Jean-Pierre Aubry, and Laura Quinby, “Public Pension Funding in Practice,” NBER Working Paper 16442, October 2010.

[12] See, for example, David Skeel, “Give States a Way to Go Bankrupt,” The Weekly Standard, November 29, 2010, http://www.weeklystandard.com/articles/give-states-way-go-bankrupt_518378.html and Grover G. Norquist and Patrick Gleason, “Let States Go Bankrupt,” Politico, December 24, 2010.

[13] A bill proposed by House of Representative members Paul Ryan, Darrell Issa, and Devin Nunes (H.R. 6484 in the 111th Congress) would require states and localities to report pension liabilities to the federal government using U.S. Treasury Bond rates to discount liabilities as a condition of issuing tax-exempt bonds.