Tax Cuts for the Wealthy Would Do Little to Help Small Businesses and the Economy

Testimony of Chye-Ching Huang, Deputy Director, Federal Tax Policy, Center on Budget and Policy Priorities, Before the Committee on Ways and Means, Subcommittee on Tax Policy, U.S. House of Representatives

Chairman Roskam, Ranking Member Doggett, and other members of the Subcommittee, thank you for the opportunity to testify today on how tax reform could affect small businesses. I would like to offer five points:

- A special rate cut for “pass-through” businesses would overwhelmingly benefit the wealthy and tax avoiders, not small businesses. This is a central element of both President Trump’s tax plan and the “Better Way” tax plan. Some proponents say it would be a boon for small businesses. In reality, it would mostly help wealthy filers — such as hedge fund managers, investment bankers, and real estate investors — as well as high-earners who engage in tax avoidance by converting their salaries to pass-through income. Few typical Main Street small businesses would see a benefit. And domestic small businesses would not benefit President Trump’s proposed “territorial” corporate tax system, and may be hurt by it.

- Eliminating the estate tax would be a boon to the heirs of the wealthiest estates in the country, not to small farms and small businesses. Proponents of proposals to repeal or scale back the estate tax often assert that doing so would help small business owners and farms. But only about 50 small farms and businesses nationwide face any estate tax in a typical year, and those that do pay an effective rate of 6 percent. This is primarily because the estate tax exempts $11 million in assets per couple — the same reason why repealing it would be a windfall for the heirs of only the wealthiest 2 of every 1,000 estates in the country.

- Kansas’ failed experiment of large, top-tilted income-tax cuts, including special treatment for pass-throughs, did not supercharge economic growth. Instead, it damaged services and investments that help businesses and communities thrive. Since its big tax cuts took effect in January 2013, Kansas has lagged the nation in both private employment growth and economic growth. To address budget deficits fueled by the tax cuts, Kansas cut services and investments, including delaying infrastructure repairs and underfunding education. In June, bipartisan supermajorities in the Kansas House and Senate overrode Governor Brownback’s veto and reversed most of the tax cuts. The federal government does not have to balance its budget every year, but in the long run, large deficit-increasing tax cuts will create pressure to cut services and investments that support a strong economy.

- Paying for the tax cuts for the affluent and large corporations in the Trump and “Better Way” tax plans could result in harm to education, infrastructure, and other federal investments critical to the economy and small businesses. These tax plans propose large, costly tax cuts that overwhelmingly flow to the wealthy and large profitable corporations, but the plans don’t propose credible ways to fully offset the cost by scaling back tax breaks or through other sources of revenue. Instead, President Trump’s budget, and the emerging House Budget Committee plan, apparently would pair tax cuts with cuts to domestic investments that could weaken the economy and harm small businesses over time. For example, the Trump budget proposes substantial cuts in areas including job training, education, and infrastructure.

- Tax provisions in the House and Senate health bills would hurt small businesses. These bills would cut the tax credits that help people purchase premiums in the marketplace and afford out-of-pocket costs, and undo other reforms that help people who buy coverage in the individual market. Small business owners and their employees would be disproportionately affected, as they disproportionately rely on the marketplace to buy health insurance. Not only would small businesses and workers face coverage losses or increased premiums and deductibles, but the bills could also make people more reliant on employer insurance and create a barrier to starting a business. In addition, the bills would use these cuts to coverage and care to help pay for tax cuts, which would mostly go to high-income households and large drug and insurance companies and other corporations.

I’ll now cover each of these five points in more detail.

(1) “Pass-through” tax break would benefit the wealthy and do little for typical small businesses

A centerpiece of President Trump’s tax plan and the “Better Way” tax plan is a special, much lower top rate for “pass-through” business income — income from businesses such as partnerships, S corporations, and sole proprietorships that is claimed on individual tax returns and currently taxed at the same rates as wages and salaries. Both the Administration and “Better Way” plans would sharply cut the top rate on this income, from 39.6 percent to 15 and 25 percent, respectively — well below the plans’ proposed top individual income tax rates of 35 and 33 percent. Far from benefiting the typical “Mom and Pop” small business owner, these proposals would overwhelmingly benefit high-wealth households and tax avoiders.

Tax cut would flow overwhelmingly to large businesses, the very wealthy, and tax avoiders

The biggest beneficiaries of a special pass-through tax rate would be wealthy households and very large, profitable businesses, since they receive most pass-through income and would receive the biggest rate cuts. They include (the list below contains overlapping categories):

- Households with incomes above $1 million, who would receive more than two-thirds of the $1.4 trillion cost of cutting the top tax rate on existing pass-through income to 15 percent, the Tax Policy Center (TPC) estimates.[1] Millionaires would receive tax cuts averaging $114,000 apiece in 2018, a more than 5 percent boost in their after-tax incomes.

- Hedge fund managers, lawyers, consultants, and investment managers, who make up a significant share of pass-through business owners in the top tax bracket.[2]

- The 0.4 percent of S corporations that have receipts exceeding $50 million annually and make 40 percent of all S corporation income, and the 0.3 percent of partnerships that have receipts exceeding $50 million and make 70 percent of partnership income.[3]

- The country’s 400 highest-income households, whose average annual incomes exceed $300 million apiece and who receive an average of one-fifth of their income from pass-throughs.[4] Estimated conservatively, President Trump’s pass-through rate cut would give these households a tax cut averaging about $9 million each compared to current income tax rates, and about $7.5 million each compared to the 35 percent top rate on “ordinary” income under the Trump tax plan.

- Business owners like President Trump, who reportedly holds about 500 pass-through businesses.[5]

A special lower tax rate for pass-through income would also spur large-scale tax avoidance by high earners, who would have a major incentive to reclassify their salaries as “business income” to get the lower pass-through rate. For example, a lawyer who reclassified her $1 million salary as business income from the law firm would save $200,000 in taxes under the Trump provision.

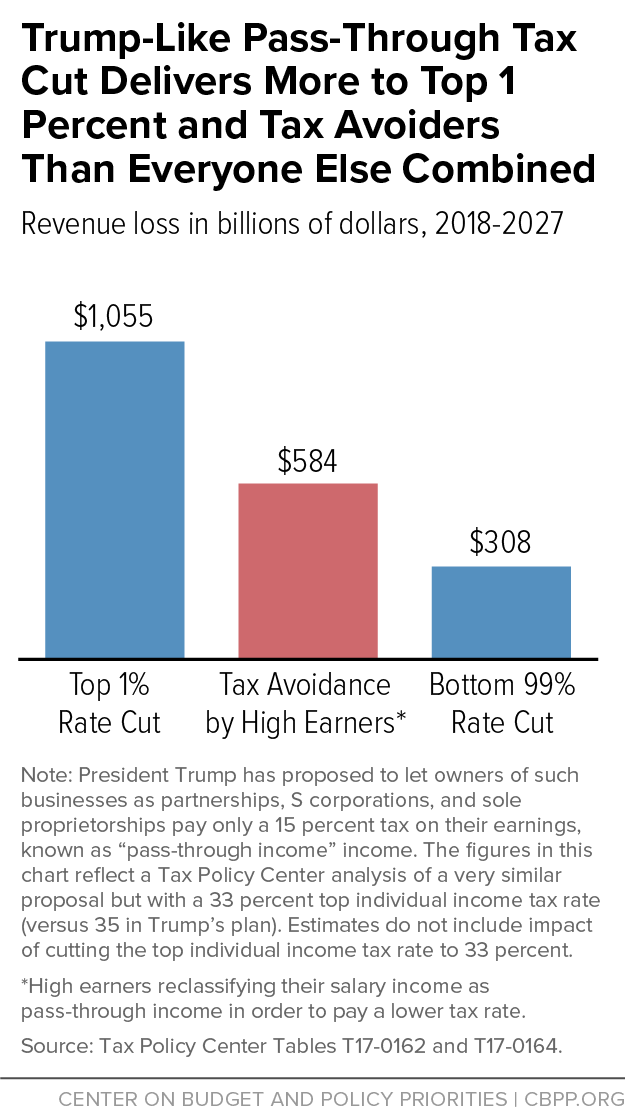

Indeed, TPC estimates that about 30 percent of the $1.9 trillion cost of cutting the top tax rate on pass-through income to 15 percent would come purely from such tax avoidance. That is, the proposal would lose $584 billion to tax avoidance by high earners alone. That substantially exceeds the total tax cut the proposal would provide for the bottom 99 percent of the population. (See Figure 1.)

It would be hard to prevent such gaming. Congress and the IRS already struggle to design and enforce rules to stop high earners from reclassifying their salaries as business income to avoid payroll taxes. This tax break would greatly increase the incentive to use these types of schemes, and tax experts from across the political spectrum are rightly skeptical that it would be possible to design and enforce effective anti-avoidance rules.[6] This is especially so given that the IRS budget has been cut substantially in recent years, leading to weaker enforcement activities including fewer audits of high-income taxpayers and businesses.[7] The Administration and the House Financial Services and General Government Appropriations subcommittee have proposed new cuts in the IRS budget on top of that.

Tax cut wouldn’t help most small businesses

Most small businesses are in fact small, and most small business owners’ incomes are already taxed at lower rates than the top rate in the Trump and “Better Way” proposals, so they would not benefit from cutting tax rates that high-income filers face.

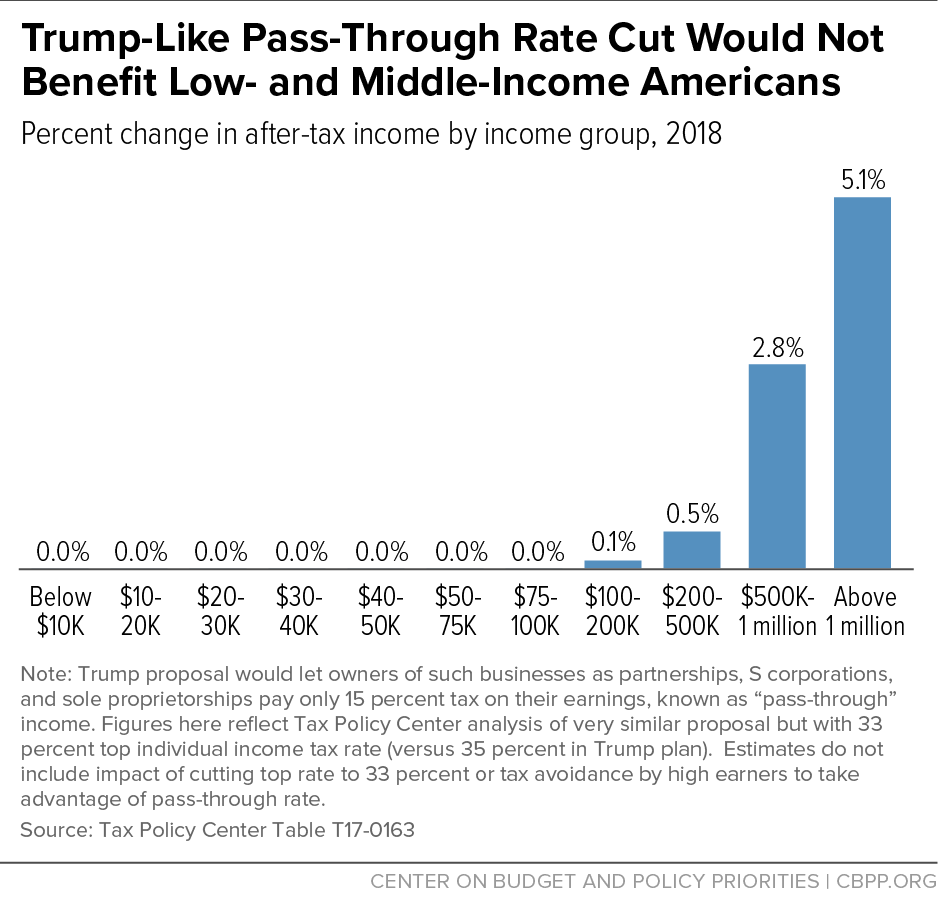

Almost 70 percent of filers with pass-through income are currently taxed at a statutory marginal income tax rate of 0, 10, or 15 percent. [8] More than 97 percent of filers with pass-through income face statutory marginal income tax rates below 33 percent. TPC analysis finds that only about 2 percent of households with incomes below $100,000 would get any tax cut from the provision. (See Figure 2).

Proponents argue that a lower pass-through rate is necessary to establish “parity” between taxes paid by pass-throughs and C corporations, which pay the corporate income tax. But pass-throughs pay only the individual tax, while C corporation profits may face the corporate income tax and, when distributed to shareholders, the tax on dividends. Setting the top rate on pass-through income equal to the top corporate tax rate therefore means that pass-through income will, on average, be taxed at lower rates than C corporation income.[9] Indeed, many businesses already choose to be taxed as pass-through entities instead of as corporations because it lowers their total taxes.

The Trump plan would pair a pass-through proposal that does little for small businesses with a “territorial” tax system that gives a zero tax rate to large multinationals’ foreign profits

President Trump has proposed a territorial tax system: U.S.-based multinational corporations wouldn’t pay U.S. corporate taxes on their foreign profits, while domestic businesses would face a 15 percent rate. This could make U.S. domestic and small businesses less competitive relative to large U.S. multinationals.

Large U.S. multinationals can pay tax lawyers millions of dollars in fees to find ways to report U.S. profits as being earned offshore in order to get the zero tax rate on “foreign” profits under a territorial system. That would give them a huge tax advantage over U.S. businesses — including small businesses — that don’t have foreign operations and can’t orchestrate complex tax avoidance maneuvers. The tax avoidance savings that corporations would reap would favor profitable U.S. multinationals, especially those in industries that can easily move profits overseas, such as pharmaceuticals and software.[10]

(2) Few small business and small farm estates would benefit from estate tax repeal

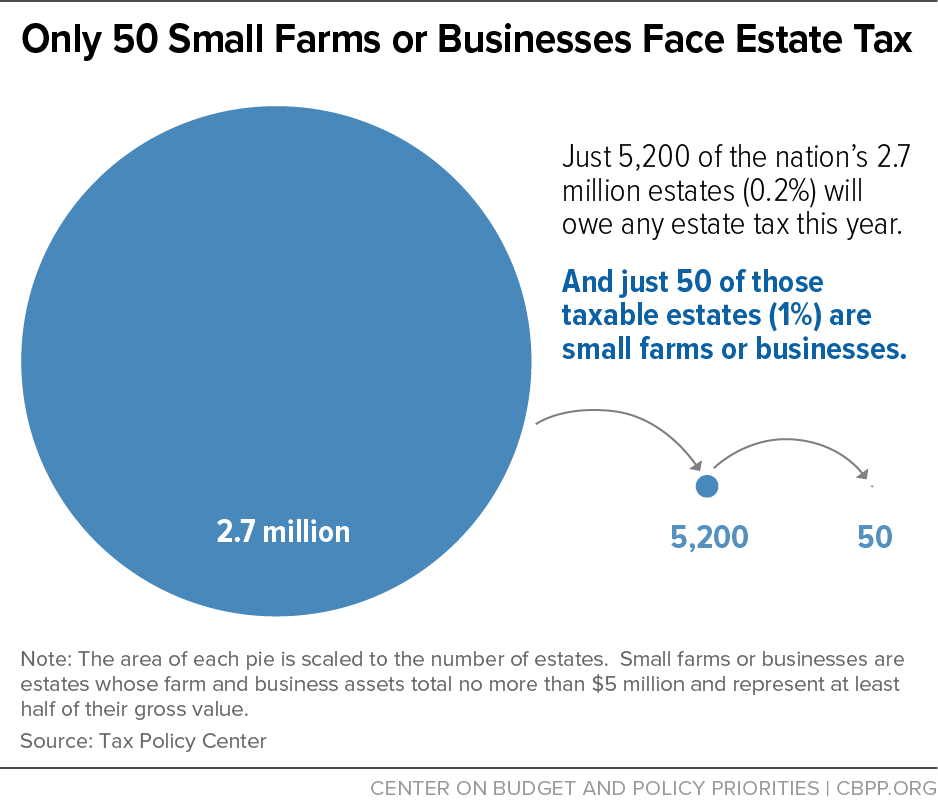

The estate tax affects very few small farms and businesses and is not a heavy burden for those that do face the tax. Only 50 small farm or business estates nationwide will face the tax in 2017 (see Figure 3), TPC estimates, and these few estates will owe less than 6 percent of their value in tax, on average.[11] This is primarily because the first $5.49 million of assets per person ($10.98 million per couple) are exempt from the estate tax.

The New York Times reported in 2001, when the estate tax applied to far more estates than it does today: “Even one of the leading advocates for repeal of estate taxes, the American Farm Bureau Federation, said it could not cite a single example of a farm lost because of estate taxes.”[12] Moreover, most farmers and business owners with estates large enough to owe any tax have sufficient liquid assets (such as bank accounts, stocks, and bonds) to pay the tax without having to touch other assets or liquidate their farm and business, a 2005 Congressional Budget Office (CBO) study found.[13] Today’s estate tax rules are much more generous than those in 2001, and more generous than CBO assumed in its analysis.

Further, farm and business estates that are large enough to owe estate tax can benefit from a variety of other rules that lessen the impact of the tax. For example, farm and business estates are generally eligible to defer payment of estate tax (paying only interest) for five years and then to pay the tax in up to ten annual installments. This enables farm and business owners with large estates but few liquid assets to pay the estate tax without selling the farm or business.[14]

While doing very little for small farms and small businesses, repeal would provide a windfall to the wealthiest 0.2 percent of estates — the only ones large enough to pay the tax. The repeal proposal introduced in the House and Senate this year would provide the 0.2 percent of wealthiest estates with an average tax cut of more than $3 million in 2017, the Joint Committee on Taxation (JCT) estimates. Roughly 330 estates worth more than $50 million would get more than $20 million apiece in tax cuts, JCT estimates. Repeal would cost $269 billion over ten years.[15]

(3) The failed Kansas tax cut experiment of large, top-tilted income tax cuts, including special treatment for pass-throughs, did not supercharge economic growth. Instead, it damaged services and investments that help businesses and communities thrive.

Kansas is a clear case of how costly top-tilted tax cuts — including a special rate for pass-throughs — do not supercharge economic growth but instead dig a revenue hole leading to damaging cuts to services and investments. As part of an aggressive set of tax cuts championed by Governor Sam Brownback, in 2012 Kansas cut income tax rates steeply and exempted pass-through income from all state income taxes.

The promised immediate economic boom failed to occur. Since the tax cuts took effect in January 2013, Kansas has lagged the nation in both private employment growth and economic growth. Meanwhile, the tax cuts wreaked havoc on the state’s budget, with the pass-through exemption alone costing hundreds of millions a year. To balance its budget, the state employed gimmicks and one-time revenues, delayed road projects, cut services, and nearly drained funds it had set aside to prepare for the next recession. Earlier this year, the Kansas Supreme Court ruled that state funding for K-12 education was now inadequate. In addition, two bond rating agencies downgraded the state due to its budget problems. A recent study of the pass-through exemption did not find any measurable boost in real economic activity because of it; instead, the results suggested that “the primary effect of the policy was to induce taxpayers to re-characterize income as pass-through business income.”[16]

A bipartisan two-thirds majority of the Kansas legislature overrode Gov. Brownback’s veto in June and reversed most of the tax cuts — including repealing the pass-through exemption. The Republican Majority Leader of the Kansas House of Representatives Don Hineman wrote:[17]

… As predicted by those of us who opposed [Gov. Brownback’s tax cut measure], Kansas faced massive budget deficits. And when they came, the governor urged the Legislature to increase the sales tax, issue billions in new debt, sweep from the highway fund and use one-time sources of funding just to pay the bills. Finally, the Legislature said “enough is enough” and rejected the governor’s short-term fixes as being neither responsible nor conservative.

The fiscal strain created by the 2012 tax cuts caused public schools to suffer, increasing class sizes and reducing program offerings. Medicaid reimbursements were reduced, straining rural hospital budgets heavily reliant on those payments. Highway funds for preservation and maintenance were cut to unsustainably low levels. And despite the assurances of adviser Art Laffer that economic nirvana was just around the corner, Kansans continued to move out of state. Brownback and his allies insisted that his tax plan was working, offering as evidence cherry-picked data such as unemployment rate and new business starts. Those are not reliable indicators of economic growth, however, and plenty of other data shows a Kansas economy which continues to lag its neighbors and the nation. . . . It took years to get us into such a dire situation, and it will take years for us to recover.

The federal government does not have to balance its budget in every year like Kansas, but it cannot allow debt to grow ever larger as a share of the economy in the long run, and both the Trump Administration and the House GOP leadership have adopted budget frameworks and policy proposals that would pair their tax cuts with large cuts to domestic investments. As Duane Goossen, a former Kansas budget director, said of the Kansas experiment: “This is a major lesson certainly for other states but also for Congress because what Trump has proposed is kind of the Brownback tax plan on steroids … and we’re going to get the same result out of that. Congress, the rest of the United States ought to look carefully at what happened to us.”[18]

(4) Paying for tax cuts for the wealthy and large corporations could harm education, infrastructure, and other federal investments important to the economy and small businesses

The Administration and “Better Way” tax plans would enlarge budget deficits and thus make it more likely that various investments that support a strong economy would be underfunded or cut in the future. The Administration’s budget — and, reportedly, the forthcoming plan from the House Budget Committee chair, as well — call for cuts in areas vital to the economy and businesses.

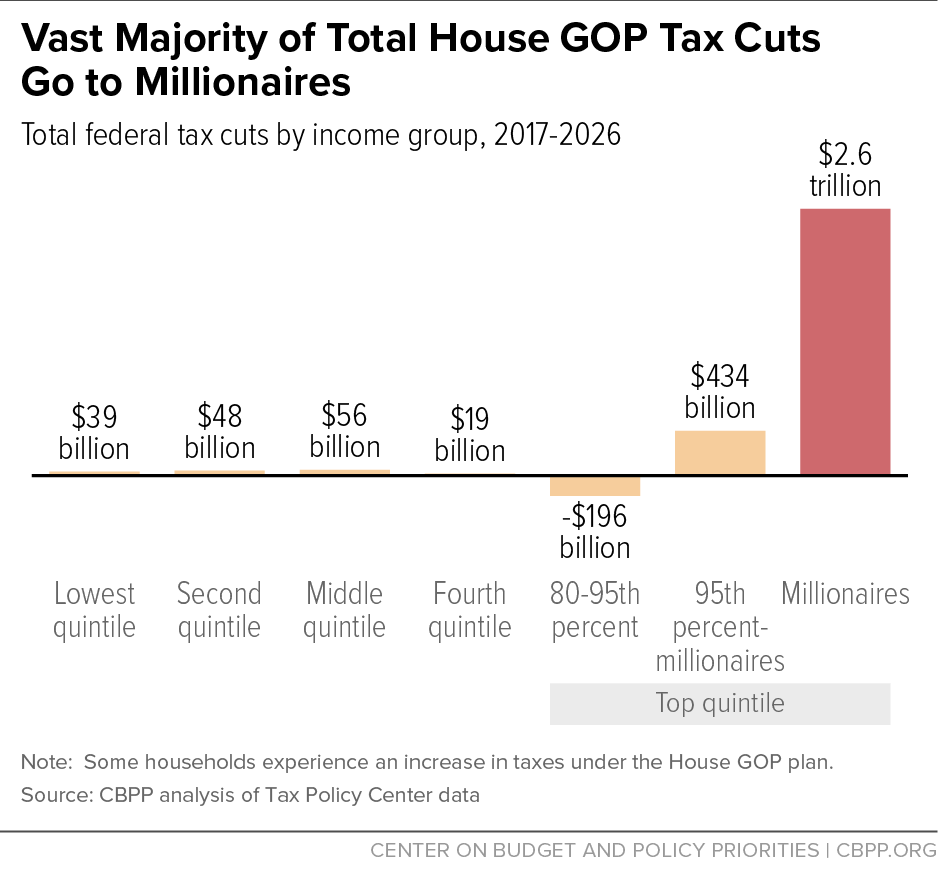

The Administration and “Better Way” plans both propose costly tax cuts that overwhelmingly would go to the wealthy and to large, profitable corporations, but give no credible way to fully offset the cost. The “Better Way” plan would reduce revenues by $3.1 trillion from 2016 through 2026, even counting its revenue-raising provisions, TPC estimates. Millionaires would receive tax cuts averaging $302,000 in 2025, an 11 percent increase in their after-tax incomes. Indeed, millionaires would reap 96 percent of the Better Way plan’s total tax cuts in 2025, and roughly $2.6 trillion in tax cuts over the first decade (see Figure 4).[19] Moreover, using mainstream economic models and assumptions, TPC estimates that because of the adverse effect of increased deficits on growth over time, by the end of the decade the “Better Way” plan would reduce economic growth.[20]

The Administration’s tax plan would cost more than $5 trillion over ten years and would also be skewed to the top, delivering net tax cuts of more than $250,000 a year to the top 1 percent.[21]

To reduce projected long-run deficits and debt, and to meet the fiscal demands of an aging population, federal tax reform should aim to increase revenues. Otherwise, the entire burden of reducing the deficit to prevent unsustainable debt levels will fall on federal programs, likely ultimately including Social Security and Medicare. This is why, at an absolute minimum, tax reform should certainly not lose revenues. The Administration and “Better Way” tax plans, however, lose trillions in revenue, increasing the pressure for damaging cuts to federal investments and services to pay for them and making it harder to make new investments in infrastructure, education, and other areas critical to U.S. businesses and workers.[22]

Further, even while the Administration’s budget shows no cost for its tax plan, it — and the emerging House budget plan — include calls for cuts to domestic investments that could damage small businesses and the economy. For example:

- The Administration’s budget — and reportedly House Budget Committee Chair Diane Black’s emerging budget plan — would cut non-defense discretionary (NDD) programs below the already inadequate sequestration levels. NDD funds key investments including education, job training, scientific and medical research, infrastructure, and other programs that promote economic growth and support domestic businesses, as well as an array of vital public services.[23]

- The Administration’s budget specifically proposes cuts in job training and education and hence would make it more challenging to develop the skilled workforce that small businesses need. It would in 2018: slash Workforce Innovation and Opportunity Act job training grants to the states for adults, dislocated workers, and youth by 40 percent; cut student aid and end a provision adjusting Pell Grants for inflation, making college less affordable for many low-income students; and cut the Education Department’s elementary and secondary programs by $4 billion.[24]

- The President’s budget would weaken federal support for infrastructure in the long run by reducing Highway Trust Fund spending, cutting discretionary infrastructure investments, and shifting costs to states and localities. The Trump budget proposes limiting Highway Trust Fund spending to the dedicated revenues it receives, starting in 2021. That means significant cuts in Highway Trust Fund spending that would grow over time, reaching $20 billion a year by the end of ten years and extending indefinitely.[25]

So far, neither the Administration nor House leaders have proposed any credible ways to fully offset the cost of their tax plans by scaling back tax breaks or through other sources of revenue. As a result, either immediately or eventually, small businesses and their employees would bear some of the burden of spending cuts to pay for these large tax cuts overwhelmingly tilted to those at the top of the income scale and profitable corporations — spending cuts that would come on top of those already proposed by the Administration and likely the House GOP.

(5) Tax and other provisions in the House and Senate GOP health bills would hurt small businesses

The House-passed American Health Care Act (AHCA) and the Senate’s Better Care Reconciliation Act (BCRA) include major tax changes and other provisions that would disproportionately hurt small businesses and their workers and could discourage entrepreneurship.

Small business owners and their employees would be disproportionately impacted by the large reductions the AHCA and BCRA would make to tax credits that help people buy health insurance in the marketplace and pay for out-of-pocket costs. The House and Senate bills would cut the tax credits that now help people with incomes below 400 percent of the poverty line — about $48,000 for a single person — purchase coverage in the marketplace (and would eliminate the subsidies that help people below 2½ times the poverty line afford out-of-pocket costs). Small business owners disproportionately depend on the marketplace for health insurance: small business owners and self-employed workers are more than three times more likely than other workers to buy insurance through the marketplace, and accounted for 1 in 5 marketplace consumers in 2014.[26] Likewise, people who work for small businesses have seen even larger gains in coverage under the ACA than other workers, reflecting the fact that they are less likely to have coverage through their employers and thus benefit disproportionately from the ACA’s subsidies and other reforms for people buying coverage in the individual market.[27] Small businesses and their employees would therefore disproportionately face the effects of the BCRA and AHCA’s changes to marketplace assistance: losses in coverage or large increases in net premiums and/or deductibles.[28]

The AHCA and BCRA could also discourage entrepreneurship. Health reform enabled millions of Americans to obtain affordable, quality health coverage in the marketplace, independent of an employer, making it less costly and risky for people to change jobs or start their own business. The Affordable Care Act’s marketplace reforms mean that 1.5 million more people are self-employed than would otherwise have been, Urban Institute and Georgetown University health researchers estimate.[29]

By making marketplace coverage less affordable, including through cuts to tax credits, the BCRA and AHCA could resurrect a barrier to starting a business. Further, staying with an employer to maintain insurance was a particular issue for many people with pre-existing conditions before health reform and would be again under the AHCA and BCRA, which would (at state option) let plans go back to excluding key benefits that people with pre-existing conditions need.[30] As Senator Collins notes, “There is no denying that the Affordable Care Act has made insurance available to millions of Americans and allowed people to leave corporate jobs and start businesses.”[31] Cutting subsidies and reversing the ACA’s reforms would reverse those gains.

The ACHA and BCRA’s cuts to tax credits and other coverage provisions that help small businesses, their workers, and millions of other Americans would, in part, go to fund hundreds of billions of dollars in tax cuts overwhelmingly for high-income households and large drug companies, insurers, and other corporations.[32]

End Notes

[1] Jeffrey Rohaly, Joseph Rosenberg, and Eric Toder, “Options to Reduce the Taxation of Pass-Through Income,” TPC, May 16, 2017, http://tpc.io/2qoxsmJ. Also see Chuck Marr, Chye-Ching Huang, Brandon DeBot, and Guillermo Herrera, “Trump Tax Plan’s Pass-Through Tax Break Would Provide Massive Windfall to the Wealthy,” CBPP, May 22, 2017, http://bit.ly/2v7SoQ0 for description of TPC estimates.

[2] Frank Sammartino, “Taxation of Pass-Through Businesses,” TPC, January 30, 2017, http://tpc.io/2t9hyfN.

[3] Joint Committee on Taxation tabulations using IRS Statistics of Income data. See Tables 4 and 5 in Joint Committee on Taxation, “Background on Business Tax Reform,” April 22, 2016, http://bit.ly/2uMaA25.

[4] Marr, Huang, DeBot, and Herrera.

[5] Sheri A. Dillon and William F. Nelson, “Re: Status of U.S. federal income tax returns,” Morgan, Lewis & Bockius LLP, March 7, 2016, http://bit.ly/2sZZoBU.

[6] See Box 2 in Marr, Huang, DeBot, and Herrera, and Joseph Henchman, “Kansas May Drop Pass-Through Exclusion After Revenue Projections Miss Mark Again,” Tax Foundation, April 30, 2015, http://bit.ly/2u96p2L.

[7] Brandon DeBot, Emily Horton, and Chuck Marr, “Trump Budget Continues Multi-Year Assault on IRS Funding Despite Mnuchin’s Call for More Resources,” CBPP, March 16, 2017, http://bit.ly/2npTvYb.

[8] Similarly, a Treasury analysis of small business owners — more narrowly defined — in 2010 shows 67 percent already face rates of 15 percent or lower. These estimates define a small business owner as someone deriving at least 25 percent of his or her adjusted gross income from a small business. They define a small business as one with at least $5,000 in deductions for activities considered “businesslike” (such as expenses related to employees, inventories, office supplies, and rent) and income and deductions of less than $10 million. Matthew Knittel et al., “Methodology to Identify Small Businesses and Their Owners,” Office of Tax Analysis Department of the Treasury, Technical Paper 4, August 2011, Table 17, http://bit.ly/2v7G7Ly.

[9] For new investments, pass-through businesses would face marginal effective tax rates of 2.6 and 2.5 percent under the Trump campaign tax plan and House GOP proposal, respectively, according to TPC. In comparison, C corporations would face marginal effective tax rates of 9.5 and 8.8 percent under these plans, respectively. See James R. Nunns, Leonard E. Burman, Jeffrey Rohaly, and Joseph Rosenberg, “An Analysis of Donald Trump’s Revised Tax Plan,” TPC, October 18, 2016, http://tpc.io/2f5xYjZ ; and James R. Nunns, Leonard E. Burman, Jeffrey Rohaly, Joseph Rosenberg, and Benjamin R. Page, “Dynamic Analysis of the House GOP Tax Plan: An Update,” TPC, June 30, 2017, http://tpc.io/2uKUhlt.

[10] CBPP, ““Territorial Tax” Is a Zero Rate on U.S. Multinationals’ Foreign Profits, Threatens U.S. Revenues and Wages,” May 16, 2017, http://bit.ly/2uNwJx6.

[11] TPC table T16-0277, http://tpc.io/2t9BwHd. TPC defines a small business or small farm estate as one for which farm and business assets are at least half of gross estate and these assets total no more than $5 million. Similarly, the Department of Agriculture (USDA) finds that only about 0.4 percent of all farm estates face the tax. This figure includes estates that may not have accumulated the bulk of their assets or income from farming activity. For more details, see USDA, Economic Research Service, “Federal Estate Taxes,” updated March 15, 2017, http://bit.ly/2tE9mHN.

[12] David Cay Johnston, “Talk of Lost Farms Reflects Muddle of Estate Tax Debate,” New York Times, April 8, 2001, http://nyti.ms/1Of3vvD.

[13] Congressional Budget Office (CBO), “Effects of the Federal Estate Tax on Farms and Small Businesses,” July 2005, https://www.cbo.gov/publication/16897.

[14] Other provisions that further reduce estate tax requirements on the very few farms and small businesses that are large enough to face it include the ability to value farmland for the purposes of calculating the estate tax based on its value as a farm (rather than at the land’s fair market value, which may be higher because the land could be more valuable if used for something other than farming), minority and marketability discounts, and easement donation rules. See Gillian Brunet and Chye-Ching Huang, “Unlimited Estate Tax Exemption for Farm Estates Is Unnecessary and Likely Harmful,” CBPP, June 29, 2010, http://bit.ly/2sLgVcX.

[15] JCT analyses of H.R. 1105, the “Death Tax Repeal Act of 2015,” at http://bit.ly/2u91aQu and http://bit.ly/1HeVtzH. The bill was reintroduced in 2017 as H.R. 631 and S. 205, both titled the “Death Tax Repeal Act of 2017.”

[16] Jason DeBacker, Bradley T. Heim, Shanthi P. Ramnath, and Justin M. Ross, “The Impact of State Taxes on Pass-Through Businesses: Evidence from the 2012 Kansas Income Tax Reform,” July 2016, http://bit.ly/2tDUfOG.

[17] Don Hineman, “Rep. Don Hineman: Why tax reform was necessary,” Topeka Capital-Journal, updated July 5, 2017, http://bit.ly/2udIJLv.

[18] Brian Lowry and Scott Canon, “Kansas tax ‘experiment’ offers lessons to the nation, analysts say,” Kansas City Star, June 7, 2017, http://bit.ly/2t09Sg9.

[19] CBPP analysis based on Page, “Dynamic Analysis of the House GOP Tax Plan: An Update.” See Isaac Shapiro, Chye-Ching Huang, and Richard Kogan, “House GOP Framework Would Give Millionaires $2.6 Trillion in Tax Cuts, While Cutting Programs for Low- and Moderate-Income People by $3.7 Trillion,” CBPP, September 29, 2016, http://bit.ly/2deCtbe.

[20] Ibid. TPC has not done a macroeconomic analysis of the Trump Administration tax plan, but found that the Trump campaign tax plan would reduce growth by the end of the decade: see James R. Nunns et al., “An Analysis of Donald Trump’s Revised Tax Plan,” TPC, October 18, 2016, http://tpc.io/2f5xYjZ.

[21] CBPP, “Trump Budget’s Radical, Harmful Priorities,” May 26, 2017, http://bit.ly/2s45IDr.

[22] CBPP, “Tax Reform Should Raise Revenues — And Certainly Not Lose Them,” April 26, 2017, http://bit.ly/2oSQfoB.

[23] See CBPP, “Trump Budget’s Radical, Harmful Priorities,” and also Joel Friedman, “Black’s Lopsided Budget Is a Dead End for Appropriations,” CBPP, June 26, 2017, http://bit.ly/2u9qKVr.

[24] Sharon Parrott, “Contrary to Rhetoric, Trump Budget Would Make It Harder for Many to Climb Economic Ladder,” CBPP, May 31, 2017, http://bit.ly/2sLDbmU.

[25] Jacob Leibenluft, “Trump’s Bait and Switch on Infrastructure,” CBPP, June 7, 2017, http://bit.ly/2tJs5QM.

[26] Adam Looney and Kathryn Martin, “One in Five 2014 Marketplace Consumers was a Small Business Owner or Self-Employed,” U.S. Department of Treasury, January 12, 2017, http://bit.ly/2lFdQa7.

[27] Figure 1 in Richard Frank, testimony to U.S. Senate Committee on Small Business and Entrepreneurship, “Impact of the ACA on Small Business,” May 18, 2016, http://bit.ly/2u4h7b8.

[28] Aviva Aron-Dine and Tara Straw, “Senate Bill Still Cuts Tax Credits, Increases Premiums and Deductibles for Marketplace Consumers,” CBPP, updated June 25, 2017, http://bit.ly/2sBCkaO.

[29] Linda Blumberg, Sabrina Corlette, and Kevin Lucia, “The Affordable Care Act: Improving Incentives for Entrepreneurship and Self-Employment,” Urban Institute, May 2013, http://urbn.is/2sOhjrV.

[30] Sarah Lueck, “If Senate Republican Health Bill Weakens Essential Health Benefits Standards, It Would Harm People with Pre-Existing Conditions,” CBPP, June 12, 2017, http://bit.ly/2tJi45W.

[31] Jennifer Steinhauer, “From Maine, a Call for a More Measured Take on Health Care,” New York Times, June 4, 2017, http://nyti.ms/2rCpUNP.

[32] The bills also repeal the tax credit that helps businesses with fewer than 25 employees afford premiums for their employees. For more on the tax cuts for drug and insurance companies and high-income individuals, see Chye-Ching Huang and Brandon DeBot, “House Health Bill: Tax Cuts for Wealthy, Insurers, and Drug Companies Paid for by Low-and Middle-Income Families,” CBPP, updated May 22, 2017, http://bit.ly/2qSmqZe.

Más de los autores