The High Cost of Estate Tax Repeal

Making permanent the repeal of the estate tax after 2010 — repeatedly proposed by President Bush— would add almost $1.3 trillion to the deficit between fiscal years 2012 and 2021, the first ten years in which the full costs of extending repeal would be reflected in the budget. This cost includes $1 trillion of lost revenues and $277 billion of higher interest payments on the national debt. Each year of repeal would cost slightly more, in today’s terms, than everything the federal government now spends on homeland security, and considerably more than it now spends on education.

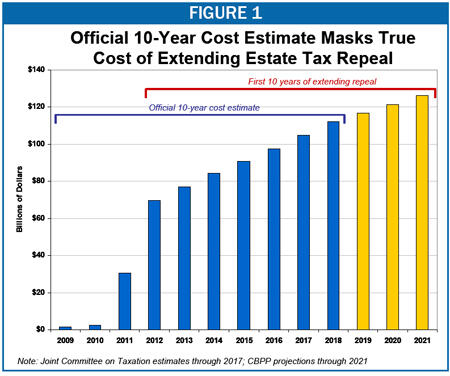

The revenue-loss projection is based on official Joint Committee on Taxation estimates of the cost of repeal, which show lost revenues of $670 billion between 2009 and 2018, including a $112 billion revenue loss in 2018 alone.[1] These estimates understate the full fiscal impact of estate tax repeal, however, because the ten-year period covered by the official estimates includes only eight years in which the costs of making repeal permanent would be fully felt (see Figure 1).[2]

To develop a ten-year cost estimate that reflects the cost of ten years of repeal requires producing an estimate that extends for an additional three years, through 2021. This can readily be done by using the Joint Tax Committee estimate of the cost of repeal through 2018 and simply assuming that the revenue loss from estate tax repeal remains constant, as a share of the economy, in years after 2018.[3]

Some have tried to argue that the $1.3 trillion cost estimate is implausible since the estate tax raised only $22.5 billion in revenue in 2007, according to the most recent IRS data.[4] The amount of estate tax revenue collected in 2007, however, is not a good indicator of the long-term budgetary impact of estate-tax repeal, for three basic reasons.

- First, the Joint Tax Committee finds that repealing the estate tax will reduce not only estate tax revenue but also income and gift tax revenue. In particular, the Joint Tax Committee expects repeal of the estate tax to reduce capital gains revenue by increasing the “lock-in effect,” whereby people choose to hold appreciated assets until they die rather than to sell the assets while they are alive and pay the capital gains tax.

- Second, unlike the IRS figure, the $1.1 trillion cost includes the additional interest payments on the national debt that will have to be paid as a result of repeal, because the cost of repeal would be financed through higher debt rather than through offsetting budget cuts or tax increases. This estimate of the interest costs uses the Congressional Budget Office’s standard methodology for estimating the increase in interest payments that results from tax cuts and spending increases that are not paid for.

- Finally, the $1.1 trillion estimate covers the 2012-2021 period, because that is the first decade in which the full cost of repeal is captured in all ten years. This period includes years in which the economy is projected to be larger and the country wealthier, and prices higher, than today. A comparable estimate for the 2008-2017 period likely would be about one-sixth lower.

It also should be noted that the official cost estimates of a tax or spending proposal measure the cost of such a proposal relative to current law. Estimates of the cost of estate tax repeal consequently compare its costs to what would transpire under the current law, under which the estate tax is slated to be reinstated in 2011 with a $1 million exemption ($2 million a couple) and a 55 percent tax rate. Most changes in the estate tax that have been proposed would have significant costs relative to current law. For instance, making permanent the estate tax as it will exist in 2009 — with a $3.5 million exemption ($7 million per couple) and a 45 percent rate — would cost about $609 billion over the 2012-2021 period, or about 48 percent of the cost of repeal.

Actuaries Estimate Estate Tax at 2009 Levels Could Cover One Quarter of Social Security Shortfall

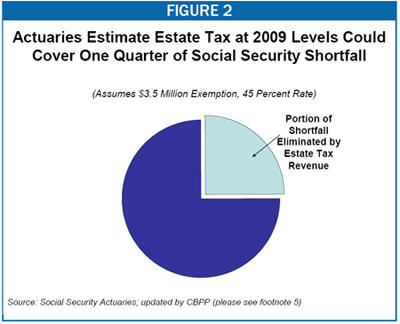

Despite the significant cost associated with reforming the estate tax by freezing it at the 2009 levels, however, such a reform still would bring in considerable revenue. For instance, in 2005 the actuaries at the Social Security Administration examined the long-term impact of a proposal by Robert Ball, who served as Social Security Commissioner under Presidents Kennedy, Johnson, and Nixon. Ball proposed maintaining the estate tax at its 2009 level and dedicating the revenues to Social Security. The actuaries estimated that such an estate tax would raise enough revenue to close more than one-quarter of the Social Security shortfall over the next 75 years (see Figure 2).[5] An estate tax with a lower exemption level or higher tax rate than would be in place in 2009 would close an even larger share of the Social Security shortfall.

The estimates by the Social Security actuaries of the impact of a reformed estate tax on the Social Security shortfall are an indication of the substantial revenues that an appropriately reformed estate tax can produce. Dedicating estate tax revenue to Social Security is, of course, just one example of how such revenue could serve important goals. The revenue also could be used to reduce the deficit or to address other critical national needs. In contrast, eliminating the estate tax not only would mean that large amounts of revenue would be lost, but also that tens of millions of other U.S. taxpayers — nearly all of whom are less wealthy than the households who would benefit handsomely from estate-tax repeal — ultimately would have to foot the bill, by being subject to reductions in other government benefits and services on to which they rely or to increases in other taxes, or by bearing the burden of a significantly higher national debt.

End Notes

[1] Joint Committee on Taxation (JCS-1-08).

[2] Since there normally is a lag of about a year between an individual’s death and the payment of any tax owed on that individual’s estate, the cost of extending estate-tax repeal so that it remains in effect in 2011 and succeeding years will not be felt in full until fiscal 2012. Thus, only eight full years of the measure’s cost show up in estimates that cover the ten-year period from fiscal 2009-2018.

[3] Assuming that the cost of a tax cut remains constant in future decades, when measured as a share of the economy, is a common approach that the Congressional Budget Office, the Government Accountability Office, and other institutions use in making long-term budget projections. Moreover, this estimate would most likely understate the long-term cost of estate tax repeal, in large part because the exemption level under current law is not indexed for inflation.

[4] Internal Revenue Service, Source of Income Estate Tax Tables, 2007. http://www.irs.gov/pub/irs-soi/07es01fy.xls

[5] Stephen C. Goss, "Memorandum to Robert M. Ball: Estimated OASDI Financial Effects for a Proposal With Six Provisions That Would Improve Social Security Financing," Social Security Chief Actuary, April 14, 2005.

In their 2005 estimate, the Social Security actuaries assumed that the amount exempt from the estate tax would be fixed (not indexed) for years after 2009. We have updated the calculation using current revenue estimates and projections of the Social Security shortfall and assuming that the exempt amount is indexed. Even under this more conservative assumption, we estimate that maintaining the estate tax at its 2009 level would still cover about one-quarter of the Social Security shortfall, because the estimated size of the shortfall has decreased since 2005.

Más de los autores