States Still Playing "Catch-Up" in New Budgets

A new survey by the Center on Budget and Policy Priorities of recently adopted state budgets provides the first 50-state data on spending for fiscal year (FY) 2007, which began July 1 in most states. The survey shows:

-

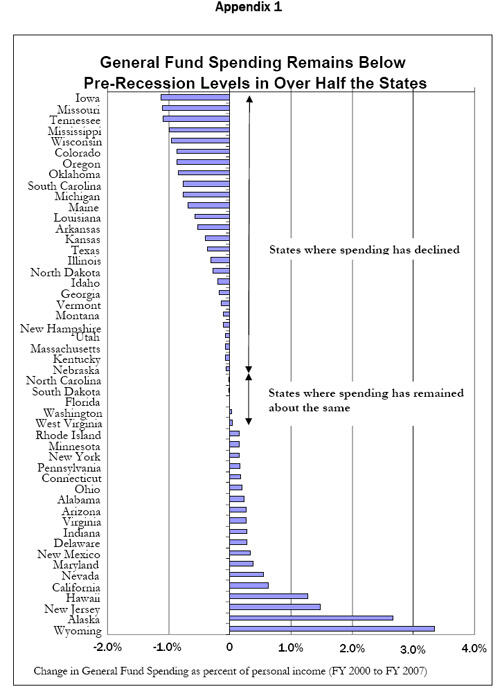

For the second year in a row, state spending will grow at above-average rates. This recent growth, however, follows several years of state budget cutbacks; just one year ago state spending was at its lowest level in 15 years as a share of GDP. In over half the states, general fund spending for FY 2007 — five years into the economic recovery — remains below pre-recession levels as a share of GDP. The states where spending is farthest below FY 2000 levels are Iowa, Missouri, Tennessee, Mississippi, Wisconsin, Colorado, Oregon, Oklahoma, South Carolina, and Michigan. In these states, state spending as a share of the economy is more that ten percent less than it was in FY 2000.

-

The states with the fastest spending growth between FY 2005 and FY 2007 are primarily those that were trying to catch up from the deep cuts of the recession. On average, spending grew 3 percentage points faster in states where spending in FY 2005 remained below pre-recession levels than in states where spending exceeded pre-recession levels.

-

A number of states have significant budget growth for FY 2007 in part because they are either reversing the budget gimmicks they employed to balance their budgets during the fiscal crisis (for example, by making up for skipped payments to pension funds) or filling depleted rainy day funds. This kind of spending does not expand the public sector.

-

As a result of better-than-projected revenue collections, most states ended FY 2006 in the black. Surpluses are common at times when the economy is improving, since state budgets are based on revenue estimates made months before the start of the upcoming fiscal year. Surpluses reflect only the difference between estimated and actual revenue collections; they do not mean that the state has sufficient revenues to reverse previous spending reductions, or even to maintain services at their current levels.

The economic downturn hit state revenues unusually hard, and states relied to a large degree on spending cuts to close budget gaps. As a result, it will take a number of additional years of above-average growth to restore state budgets to pre-recession levels. A state that responds immediately to the recent good news of strong revenue growth or year-end surpluses with tax cuts or large unfunded program expansions – before the state has reached full recovery -- is likely to be overreaching and risking its future fiscal health.

Spending Remains below Pre-Recession Levels in Most States

During May, June, and early July, the Center on Budget and Policy Priorities conducted a phone and email survey of state legislative and executive budget officials to learn states’ actual General Fund spending for FY 2005, their best estimate of FY 2006 spending, and the amount of FY 2007 spending included in their recently enacted budget.

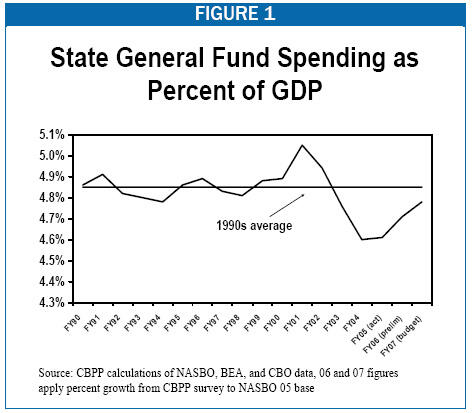

The survey found that state budgets grew by 8.9 percent on average in FY 2006 and are expected to grow by 7.3 percent in FY 2007. (See Table 1.) Even at these above-average rates of growth, though, spending in more than half the states will remain below its pre-recession (FY 2000) level as a share of GDP.[1]

|

Table 1: |

|

| Fiscal Year | Nominal Percent Change |

| FY2007 budgeted | 7.3% |

| FY2006 prelim. actual | 8.9% |

| FY2005 | 6.5% |

| FY2004 | 3.0% |

| FY2003 | 0.6% |

| FY2002 | 1.3% |

| FY2001 | 8.3% |

| FY2000 | 7.2% |

This is because states are working their way out of a deep hole. Just one year ago — at the end of FY 2005 — state spending as a share of the economy was at its lowest level in 15 years. Expenditures stood at 4.6 percent of GDP, well below the 1990s average of 4.9 percent.

Thus, while it would appear at first glance that states have left the fiscal crisis behind and are well-positioned to address needs that were postponed in recent years — or to reduce taxes — a closer look reveals that states are still in the rebuilding process. Failure to recognize this fact would endanger states’ fiscal health.

If states want to restore the substantial reductions in services they imposed during the downturn and its aftermath, they have to hope for additional years of strong growth — and then use that growth to shore up expenditures on key programs and services. For example, revenues would have to grow by more than 9 percent for two years (through FY 2009) simply to restore the level of services states provided in FY 2000.

Budgets Growing Fastest in States with Largest Budget Cuts During Recession

In general, the largest growth in spending between FY 2005 and FY 2007 occurred in states that saw the largest declines in revenue and spending during the recession and are still trying to catch up from those declines. In states where FY 2005 spending remained below pre-recession levels, nominal spending will grow an average of 8.1 percent per year between FY 2005 and FY 2007. In states where FY 2005 spending was above pre-recession levels, nominal spending will grow an average of only 5.1 percent per year by 2007.

Similarly, some state spending “increases” in recently adopted budgets represent the undoing of budget gimmicks that states employed to weather the fiscal crisis. Arizona spent $191 million to reverse a previous shift in school aid payments and restored $245 million in funds it had borrowed from the transportation fund during the fiscal crisis. Minnesota spent some $700 million in FY 2006 to reverse shifts in school aid payments. California will spend $2.8 billion repaying debt, and New Jersey is depositing over $1 billion in its public employee pension funds to catch up for payments skipped during the fiscal crisis. In addition, some states are putting money in rainy day funds to help prepare them for the next downturn.

Surpluses in Some States Do Not Indicate “Excess” Revenues

A number of states are reporting budget surpluses for FY 2006; some of these surpluses are being carried over to fund spending in FY 2007. Accounts of these surpluses often imply that such money is “extra” and thus potentially available for a new round of tax cuts. In reality, these surpluses reflect only the difference between estimated and actual revenue collections.

Understandably, states were cautious in preparing their current budgets and assumed relatively low revenue growth. Because they are required to balance their budgets, they set their expenditure levels based on these overly conservative revenue estimates; some states cut services in order to reach balance. If a state’s revenues come in more strongly than these conservative estimates, the state is said to have a surplus. But a surplus does not mean that the state has more revenue than it needs to reverse recent service cuts and restore programs to pre-recession levels. It does not even mean that the state has enough revenue to maintain state programs at their FY 2006 levels.

The reported surpluses often mask operating deficits, unrestored service reductions, and other problems that have to be addressed before a state can be said to have fully recovered from the downturn.

Appendix 1

|

Change in General Fund Spending as % of Personal Income (FY2000 to FY2007) |

|||

| Alabama | 0.2% | Montana | -0.1% |

| Alaska | 2.7% | Nebraska | -0.1% |

| Arizona | 0.3% | Nevada | 0.5% |

| Arkansas | -0.5% | New Hampshire | -0.1% |

| California | 0.6% | New Jersey | 1.5% |

| Colorado | -0.9% | New Mexico | 0.3% |

| Connecticut | 0.2% | New York | 0.2% |

| Delaware | 0.3% | North Carolina | 0.0% |

| Florida | 0.0% | North Dakota | -0.3% |

| Georgia | -0.2% | Ohio | 0.2% |

| Hawaii | 1.3% | Oklahoma | -0.8% |

| Idaho | -0.2% | Oregon | -0.9% |

| Illinois | -0.3% | Pennsylvania | 0.2% |

| Indiana | 0.3% | Rhode Island | 0.2% |

| Iowa | -1.1% | South Carolina | -0.8% |

| Kansas | -0.4% | South Dakota | 0.0% |

| Kentucky | -0.1% | Tennessee | -1.1% |

| Louisiana | -0.6% | Texas | -0.4% |

| Maine | -0.7% | Utah | -0.1% |

| Maryland | 0.4% | Vermont | -0.1% |

| Massachusetts | -0.1% | Virginia | 0.3% |

| Michigan | -0.8% | Washington | 0.0% |

| Minnesota | 0.2% | West Virginia | 0.0% |

| Mississippi | -1.0% | Wisconsin | -1.0% |

| Missouri | -1.1% | Wyoming | 3.3% |

End Notes

[1] FY2000 is the year before the large increase in spending that occurred in FY 2001, when states embarked on a number of initiatives after nearly a decade of economic growth.

Más de los autores

Areas of Expertise