I-1033's Problematic Measure of Inflation

Each year, the cost of providing health care, education, roads and other services rises. As a result, state and local governments have to spend more to provide the same level of services. Washington’s Initiative 1033 would dictate the amount of these increases in spending based not on the actual cost of those services, but rather on a rigid “inflation plus population” formula. The measure of inflation that I-1033 would utilize is called the “implicit price deflator for personal consumption expenditures” (IPD). Under I-1033, per-capita spending could rise no faster than the IPD.

IPD’s inclusion in the I-1033 formula makes little sense logically, and it would cause a lot of harm. Two features are particularly problematic. First, it does not reflect changes in costs faced by state and local government, but rather reflects changes in costs faced by consumers, which are lower. This is a flaw that the IPD has in common with another, more commonly used measure of inflation, the Consumer Price Index. The Consumer Price Index is the measure that underlies Colorado’s TABOR formula, a formula that has led to deep reductions in school funding, health care services, roads, and other areas.

But the IPD is even less appropriate than the CPI as a measure of government costs. The IPD assumes consumers can shift their spending from one area to another to take advantage of lower prices. But state and local governments’ budget rules typically prohibit this option, with good reason: the services of state and local governments, like education and health care, are essential to the state’s wellbeing and prosperity, and therefore should not be cut back or rearranged every time prices change. As a result of this assumption, the IPD always generates a lower growth rate than the CPI. In this respect, I-1033 would be even more restrictive than the Colorado’s TABOR. Had Colorado’s TABOR included the IPD, that state’s cuts to education, health care, and other services would have been substantially more severe than they were.

These two shortcomings to the implicit price deflator – its disconnect from the true costs of public services and its unusually restrictive nature – are elaborated below.

- The Implicit Price Deflator is a poor mechanism for setting levels of spending on public services because it does not actually reflect the cost of those services. State and local governments in Washington spend three-fourths of their non-federal revenues — the revenues that would be subject to I-1033 — on K-12 education, higher education, health care, transportation, and public safety. But those items receive relatively little consideration in the IPD. The IPD gives much heavier weight to such items as housing and food. For example, in Washington, K-12 and higher education spending accounts for 53 percent of current state expenditures. But for households, education is just two percent of expenditures, so it represents just two percent of the weight in the IPD. Since education costs are rising faster than the general rate of inflation, this and other mismatches of consumer versus state expenditures means that the overall index understates the rate of inflation the state faces. Health care also has a lower weight in the IPD than in the state budget. Over the last ten years the average inflation rate using the IPD has been about 2.4 percent. With health care costs rising at double digit rates in many years and little that any state can do to curb cost increases — other than to leave some state residents with increasingly inadequate access to health care — a 2.4 percent per capita growth rate is clearly inadequate.Imagen

Using a general measure of inflation to control the costs specifically incurred by state and local governments is a flaw that I-1033 shares with Colorado’s TABOR measure. The TABOR measure uses a version of the Consumer Price Index (CPI) to limit the amount of money that can be spent on public services.[1] The CPI, like the IPD, is a measure of inflation in consumer goods, and thus they both understate the cost of providing services. In Colorado, the use of the CPI-based TABOR formula led to deep cuts in services. [2] The Colorado example suggests that using any consumer-based price index to dictate overall public spending levels may undermine the ability of the state and its communities to meet their obligations.

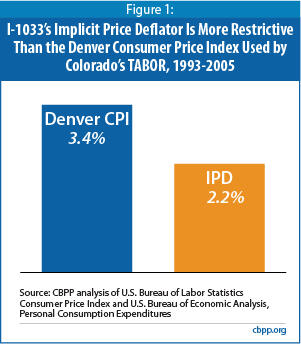

- The Implicit Price Deflator is more restrictive than the CPI used in Colorado’s TABOR, so I-1033 would produce even bigger problems in Washington than TABOR has caused in Colorado . The section above notes that the IPD is similar to the CPI in being a measure of inflation faced by consumers, but the measures are not identical. The two measures rely on different data sources and use different formulas to compute changes in prices faced by consumers. [3] One major difference is that the IPD formula is adjusted to reflect the fact that consumers have the freedom to alter their spending patterns every time they shop, substituting cheaper categories of products for those that have gotten too expensive. For example, families might eat at home more often when the price of restaurant meals rise. These “savings” are incorporated in the IPD. As a result, the IPD is nearly always lower than the CPI. State and local governments, however, cannot realize such savings, because their budget rules typically allow little such reallocation of spending from one area to another. For example, the state cannot simply move money from its education budget to its highway trust fund during periods when school-related costs (such as health care for teachers) are rising faster than road-building costs (such as asphalt and concrete). Nor would the state necessarily want to do so even if it could, since both education and transportation are so important to the state’s long-term prosperity.

This seemingly technical distinction has large and very problematic consequences when incorporated into a government spending limit. As noted above, Colorado’s TABOR has led to significant cutbacks in public services in that state. It is based on the Consumer Price Index for the Denver metro area. (Unlike the IPD, the CPI has regional versions.) During the period in which the Colorado TABOR was in effect, from 1993 to 2005, the Denver CPI averaged 3.4 percent annual growth. During that same period, the IPD averaged 2.2 percent annual growth. This means that over the 12-year period, if Colorado had been operating under an I-1033-style IPD-based formula, the state would have had to cut services by an additional 10 percent beyond what the state enacted under the actual CPI-based formula. As it was, by the end of the 1993-2005 period, the cutbacks in health, education, transportation and other services had become so significant that voters in Colorado chose to suspend the formula for five years.

The state Office of Financial Management has predicted a similar consequence for Washington state government. Over the next three years, the OFM predicts that the IPD will grow at a rate 1.2 percent below that of the CPI. Through 2012, state data show the I-1033 limit will reduce by $1.5 billion the funds available for education, health care and other services. Of that amount, $200 million is attributable to I-1033’s use of the IPD as its preferred measure of inflation. Comparable levels of cuts would occur at the local level.

In short, the IPD, a key component of the revenue formula that is the basic element of I-1033, is arbitrary because it has virtually nothing to do with the actual cost of providing public services. And it is way too restrictive, forcing even lower growth than a similar formula that caused major problems in Colorado. It is a formula for dramatic cuts in education, health, public safety, transportation, and other key services.

End Notes

[1] See David Bradley, Nicholas Johnson and Iris J. Lav, “The Flawed 'Population Plus Inflation' Formula: Why TABOR’s Growth Formula Doesn’t Work,” Center on Budget and Policy Priorities, January 2005.

[2] See Iris J. Lav, “A Formula for Decline,” Center on Budget and Policy Priorities, revised October 9, 2009.

[3] See Bureau of Economic Analysis, “Comparing the CPI and the PCE Price Index,” Survey of Current Business, November 2007.

Más de los autores