Federal Action Needed to Close Medicaid “Coverage Gap,” Extend Coverage to 2.2 Million People

The American Rescue Plan, which President Biden signed into law in March, gives the 12 states that have not expanded their Medicaid program under the Affordable Care Act (ACA) a big financial incentive to do so: a two-year, 5-percentage-point increase in the share of costs in their underlying Medicaid program that the federal government will pay. Because most of these states will likely still reject the ACA’s Medicaid expansion, however, policymakers should enact policies as part of upcoming recovery legislation that would provide health coverage to the 2.2 million people who would otherwise be covered by the expansion.

Closing this Medicaid “coverage gap” would be among the most important steps that policymakers can take to reduce racial health disparities. Recovery legislation presents a rare opportunity to make transformational progress toward coverage for these 2.2 million people — most of whom live in the South and are people of color — an opportunity that won’t likely occur again in the near future.

Policymakers should provide coverage that is as closely aligned with Medicaid as possible. They have two basic options: (1) to direct the Centers for Medicare & Medicaid Services (CMS) to run a federalized Medicaid program for states that refuse to expand their Medicaid program under the ACA, or (2) to allow people to get fully subsidized coverage through the ACA’s marketplaces.

While pursuing either approach, policymakers would need to enact policies to discourage or prohibit states that have expanded Medicaid from undoing their expansions — both to protect current Medicaid beneficiaries (because state Medicaid programs will likely be significantly better for low-income residents than a federally run plan) and to limit federal costs. Policymakers will also have to address the cost of closing the Medicaid coverage gap. One good option is to finance these costs through cost savings that would be achieved by letting Medicare negotiate drug prices; President Biden favors this approach, and it would have the added benefit of lowering prescription drug prices for everyone.

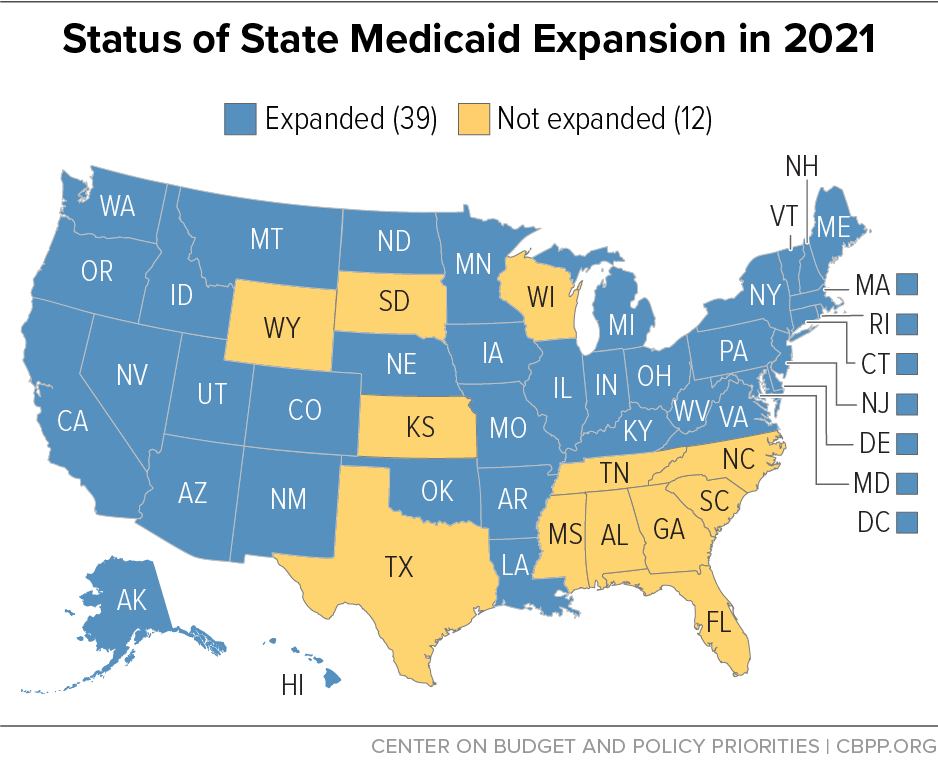

The ACA was supposed to provide Medicaid coverage to all adults with low incomes but, in its NFIB v. Sebelius decision of 2012, the Supreme Court ruled that states would have the option to expand their Medicaid programs rather than face a federal requirement to do so. To date, 38 states and the District of Columbia have implemented Medicaid expansion (see Figure 1), and the expansion is providing health care to over 12 million adults. Those who gained coverage are healthier and more financially secure as a result, a large body of research shows.

Yet, 12 states still refuse to expand Medicaid, leaving 2.2 million people in the coverage gap and deprived of the significant benefits that expansion provides. Nor, based on recent developments in several states, do non-expansion states seem inclined at the moment to reverse course, despite the Rescue Plan’s substantial financial incentives. That strongly suggests that the only way to ensure that adults with incomes below the poverty line have access to health coverage regardless of what state they live in is for policymakers to take additional steps to expand coverage as part of recovery legislation, which would help to correct inequities in coverage and access that the Supreme Court decision helped to create.

Medicaid Expansion Improves Access to Care and Health Outcomes

Medicaid expansion significantly lowered uninsured rates across the country for adults with low incomes, providing coverage to over 12 Million people.Medicaid expansion significantly lowered uninsured rates across the country for adults with low incomes, providing coverage to over 12 million people with incomes below 138 percent of the poverty line (which is about $17,600 for a single adult). Overall, 7.3 percent of people in expansion states were uninsured in 2019, compared to 12 percent of people in non-expansion states, which helps illustrate expansion’s impact.[1]

Medicaid expansion has improved access to care and made it more affordable for enrollees, and it has increased their financial security. Along with coverage gains, greater access to care, and more financial security, expansion is linked to improvements in some measures of health outcomes and health status as well as financial benefits for states and providers, according to a review of over 400 studies.[2] Expansion is also associated with reductions in food insecurity, poverty, and evictions, research shows.[3] Moreover, Medicaid expansion has saved the lives of at least 19,200 adults aged 55 to 64 from 2014 to 2017.[4]

While long-standing health disparities caused by racism, economic and health system inequities, limits on health coverage for immigrants, and other factors remain, the ACA’s major coverage provisions that took effect in 2014 have helped to narrow them.[5] By 2018, for example, the gap between Black and white uninsured rates narrowed by 4.1 percentage points while the gap between Latino rates shrunk by 9.4 percentage points. Meanwhile, the gap between white and Black adults who had trouble obtaining care due to cost fell from 8.1 percentage points in 2013 to 4.7 points in 2018, and the gap between white and Latino adults fell from 12.7 percentage points to 8.3 points.[6] (See Figure 2.)

Federal Action Needed to Cover Those Left Out

Millions of uninsured people with low incomes have experienced none of the gains of expansion simply due to where they live. The differences in health outcomes between expansion and non-expansion states are stark. While, as noted above, Medicaid expansion has saved the lives of at least 19,200 adults aged 55 to 64 from 2014 to 2017, non-expansion has cost the lives of another 15,600 such adults. The impact of expansion on racial disparities is particularly salient, because more than half of those who remain uninsured due to their states’ refusal to expand are people of color, most of whom live in the South.

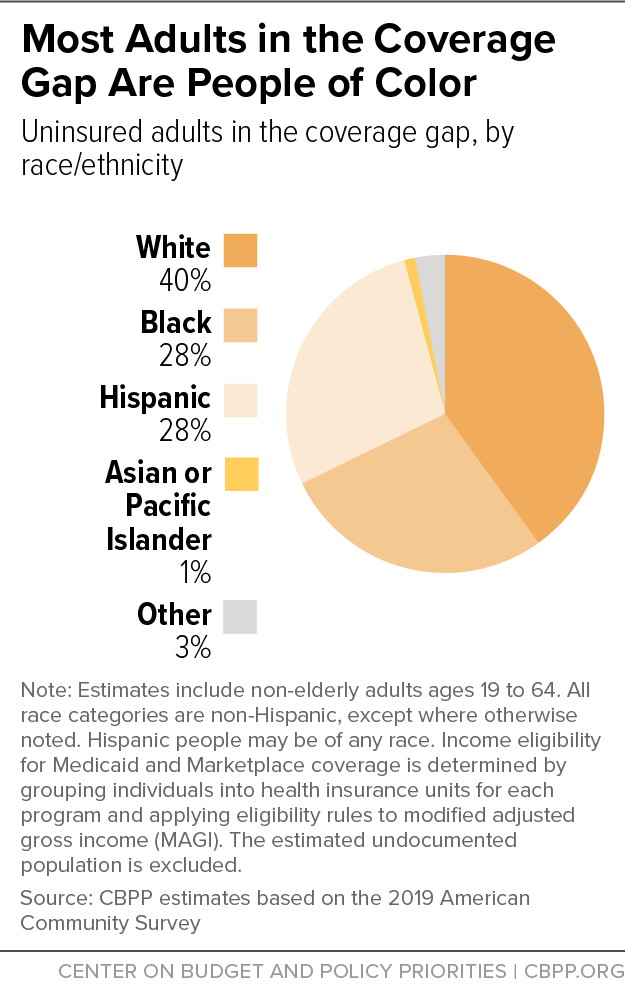

About 2.2 million adults with incomes below the poverty line are uninsured in the 12 states that haven’t expanded Medicaid (see Table 1).[7] They have no pathway to affordable coverage because their incomes are too low to qualify for subsidies in the marketplace and they don’t qualify for their states’ underlying Medicaid programs, which generally provide coverage for adults without a disability only for parents with very low incomes.[8] Those who lack coverage are mostly people of color — 28 percent are Black and 28 percent are Hispanic (see Figure 3).[9]

In addition to these 2.2 million adults, the Kaiser Family Foundation reports, another 1.8 million uninsured people in non-expansion states have incomes between 100 and 138 percent of the poverty line; they can buy subsidized coverage in the marketplace, but they would qualify for Medicaid if their states expanded.[10] Even with robust subsidies in the marketplace, Medicaid has lower costs, more comprehensive benefits, and can be more accessible for people who need help enrolling or who seek coverage outside of an enrollment period.

While the opponents of expansion often cite concerns about state costs, the financial incentive for states to expand Medicaid is substantial. For starters, the federal government pays 90 percent of the cost of covering the expansion group, which is well above the share of Medicaid costs that it pays in each state for other Medicaid enrollees, which ranges from 50 and 78 percent per state. In many states, research shows, the combination of expansion’s low state share of the costs and the offsetting savings and increased revenue that it generates, produces net budget savings.[11] As noted, the American Rescue Plan includes an added incentive for non-expansion states to expand: a two-year increase in federal Medicaid funding (beyond the cost of the expansion itself), beginning when a state implements the expansion. That would fully cover the non-federal share of expansion costs for between 3.1 and 6.5 years depending on the state, according to research by Manatt Health.[12] Georgia, for example, would receive almost $1.5 billion from the incentives, enough to fully fund its expansion for more than four years.[13]

Not even the Rescue Plan’s incentives, which come on top of state cost savings and reductions in uncompensated care that expansion has been shown to bring, has convinced non-expansion states to reverse course. Since the Rescue Plan was enacted, state legislatures in Texas and Wyoming voted against expansion, and Missouri legislators refused to appropriate funds for an expansion that voters adopted last summer as a state constitutional amendment, setting the stage for litigation if the state fails to enroll people in coverage beginning July 1 as the amendment prescribed.[14] In addition, other states have failed to seriously consider expansion during their legislative sessions.

Several Approaches to Designing a Federal Fallback

Unless policymakers address the coverage gap in recovery legislation, millions of people will likely remain uninsured for many years.[15] Policymakers have two basic options: (1) directing CMS to run a federalized Medicaid program in states that won’t expand, or (2) allowing people to enroll in marketplace coverage. For either approach, policymakers should seek to provide coverage that is aligned as closely as possible with Medicaid coverage.

For a marketplace plan, policymakers would need to make changes in benefits, cost sharing, and enrollment processes. For example, people should be allowed to enroll all year, and they should not have to reconcile the advance premium tax credits they receive when they file their federal taxes — that is, pay back any tax credits for which they become ineligible after they receive them because their income has risen. For a federalized Medicaid program, CMS would likely contract with one or more managed care companies to offer coverage that includes all Medicaid benefits that go to expansion enrollees. Enrollees, however, would likely have to enroll through HealthCare.gov, so policymakers would need to make adjustments that, for instance, allow individuals to enroll any time during the year.

Either approach would effectively close the coverage gap in non-expansion states. But if the federal government simply offers to pay the full cost of coverage for people with incomes below 138 percent of the poverty line through the marketplace or a federally run Medicaid program, some expansion states may seek to drop their expansion, which would raise federal costs.

It also would hurt Medicaid enrollees. Even with changes in marketplace plans, for instance, current Medicaid enrollees would get less than they now get from Medicaid. Specifically, marketplace plans may not include safety net and other providers, from which people now get care. At the same time, many state Medicaid managed care plans have developed approaches to enrollees’ needs that go beyond health care, helping them get housing and other social services. In addition, states have made great strides in improving the delivery of behavioral health services in their Medicaid programs through special demonstration programs, especially treatment for substance use disorders in response to the opioid epidemic. Marketplace plans would have none of these features.

While a federally administered Medicaid plan may be able to align with Medicaid more fully, it would still be difficult for such a plan to achieve the same degree of collaboration with state agencies and social service programs as a state-administered expansion.

In upcoming recovery legislation, policymakers could provide fiscal incentives for states that have adopted the expansion to maintain their expansions, such as by increasing the share of expansion costs that the federal government covers. To further minimize the risk that states will drop their expansion, policymakers could make the federal fallback available only to non-expansion states. Moreover, once the federal government assumes responsibility for covering people in the coverage gap, policymakers could place limits on federal funding for uncompensated care or on other federal funding for non-expansion states, although these or other penalties could prompt states to make harmful cuts to their programs.

To be clear, non-expansion states would still be eligible for the American Rescue Plan’s significant financial incentives for adopting the expansion as well as any new incentives that policymakers provide to expansion states. With a penalty for states that don’t take the expansion, states would have to choose between adopting the expansion and securing its huge fiscal and other benefits (both temporary and permanent) or forgoing such benefits and paying one or more penalties. That choice could help drive more states towards adopting the expansion rather than having their residents enroll in the federal fallback.

Either way, closing the coverage gap will cost money, so enacting a policy to achieve that goal will depend on the amount of increased revenue and cost savings that the recovery legislation can generate. The Biden Administration has linked closing the gap to cost savings from negotiating Medicare drug prices.[16] Negotiating prices for Medicare drugs is a sound way to pay for closing the coverage gap. It not only would make funds available to do so, but it also would lower prescription drug costs for Medicare enrollees and people enrolled in other forms of coverage.

| TABLE 1 | ||||||

|---|---|---|---|---|---|---|

| Uninsured Adults in the Coverage Gap, by Gender and Age | ||||||

| State | Total | Female | Male | 19 to 34 | 35 to 39 | 50 to 64 |

| Non-expansion states | 2,211,000 | 1,091,000 | 1,120,000 | 1,082,000 | 591,000 | 539,000 |

| Alabama | 137,000 | 68,000 | 69,000 | 65,000 | 40,000 | 32,000 |

| Florida | 425,000 | 193,000 | 231,000 | 190,000 | 109,000 | 126,000 |

| Georgia | 275,000 | 136,000 | 139,000 | 136,000 | 73,000 | 66,000 |

| Kansas | 44,000 | 23,000 | 21,000 | 23,000 | 10,000 | 11,000 |

| Mississippi | 110,000 | 55,000 | 55,000 | 55,000 | 30,000 | 25,000 |

| North Carolina | 207,000 | 98,000 | 109,000 | 99,000 | 58,000 | 50,000 |

| South Carolina | 105,000 | 52,000 | 53,000 | 43,000 | 29,000 | 34,000 |

| South Dakota | 16,000 | 7,000 | 9,000 | 8,000 | * | 5,000 |

| Tennessee | 119,000 | 50,000 | 69,000 | 47,000 | 31,000 | 41,000 |

| Texas | 766,000 | 406,000 | 361,000 | 412,000 | 207,000 | 147,000 |

| Wyoming | 7,000 | 3,000 | 5,000 | 4,000 | * | * |

End Notes

[1] Matt Broaddus and Aviva Aron-Dine, “Uninsured Rate Rose Again in 2019, Further Eroding Earlier Progress,” Center on Budget and Policy Priorities, September 15, 2020, https://www.cbpp.org/research/health/uninsured-rate-rose-again-in-2019-further-eroding-earlier-progress.

[2] Expansion has reduced uncompensated care costs for hospitals and decreased state spending on behavioral health and uncompensated care, among other expenditures. Jesse Cross-Call, “Medicaid Expansion Continues to Benefit State Budgets, Contrary to Critics’ Claims,” Center on Budget and Policy Priorities, October 9, 2018, https://www.cbpp.org/research/health/medicaid-expansion-continues-to-benefit-state-budgets-contrary-to-critics-claims

[3] Madeline Guth, Rachel Garfield, and Robin Rudowitz, “The Effects of Medicaid Expansion under the ACA: Studies from January 2014 to January 2020,” Kaiser Family Foundation, March 17, 2020, https://www.kff.org/medicaid/report/the-effects-of-medicaid-expansion-under-the-aca-updated-findings-from-a-literature-review/.

[4] Sarah Miller, Norman Johnson, and Laura R. Wherry, “Medicaid and Mortality: New Evidence from Linked Survey and Administrative Data,” National Bureau of Economic Research working paper, July 2019, https://www.nber.org/papers/w26081.

[5] Jesse Cross-Call, “Medicaid Expansion Has Helped Narrow Racial Disparities in Health Coverage and Access to Care,” Center on Budget and Policy Priorities, October 21, 2020, https://www.cbpp.org/research/health/medicaid-expansion-has-helped-narrow-racial-disparities-in-health-coverage-and.

[6] Jesse C. Baumgartner et al., “How the Affordable Care Act has Narrowed Racial and Ethnic Disparities in Access to Health Care,” Commonwealth Fund, January 16, 2020, https://www.commonwealthfund.org/publications/2020/jan/how-ACA-narrowed-racial-ethnic-disparities-access.

[7] CBPP estimates using the 2019 American Community Survey. Income eligibility for Medicaid and marketplace coverage is determined by grouping individuals into health insurance units for each program and applying eligibility rules to modified adjusted gross income (MAGI). The estimated undocumented population is excluded.

[8] The exception is Wisconsin, which provides coverage to adults with incomes up to the poverty line.

[9] CBPP estimates using the 2019 American Community Survey. Income eligibility for Medicaid and marketplace coverage is determined by grouping individuals into health insurance units for each program and applying eligibility rules to MAGI. The estimated undocumented population is excluded.

[10] Rachel Garfield, Kendal Orgera, and Anthony Damico, “The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid,” Kaiser Family Foundation, January 21, 2021, https://www.kff.org/medicaid/issue-brief/the-coverage-gap-uninsured-poor-adults-in-states-that-do-not-expand-medicaid/.

[11] For example, expansion provides states with 90 percent federal matching funds for previously state-funded expenditures on behavioral health, and it also allows some people in traditional Medicaid to move to expansion, under which the federal government pays a higher share of Medicaid costs. It also increases revenue from state provider taxes. Bryce Ward, “The Impact of Medicaid Expansion on States’ Budgets,” Commonwealth Fund, May 5, 2020, https://www.commonwealthfund.org/publications/issue-briefs/2020/may/impact-medicaid-expansion-states-budgets.

[12] The amount of funding a state would receive over the two-year period would cover the states’ 10 percent share of expansion costs for a longer period.

[13] Manatt Health, “Assessing the Fiscal Impact of Medicaid Expansion Following the Enactment of the American Rescue Plan Act of 2021,” April 2021, https://www.manatt.com/Manatt/media/Documents/Articles/ARP-Medicaid-Expansion.pdf.

[14] Kurt Erickson, “Missouri Senate rejects funding for Medicaid expansion,” St. Louis Post-Dispatch, April 28, 2021, https://www.stltoday.com/news/local/govt-and-politics/missouri-senate-rejects-funding-for-medicaid-expansion/article_33249172-2601-51ff-b4fd-4ff541ed3331.html.

[15] Jonathan Cohn, “The Big Biden Policy Idea That Nobody (Not Even Joe Biden) Is Discussing,” HuffPost, May 2, 2021, https://www.huffpost.com/entry/biden-health-care-medicaid-gap-uninsured_n_608b38dce4b0b9042d904b5b?ncid=engmodushpmg00000004.

[16] The White House, “Fact Sheet: The American Families Plan,” April 28, 2021, https://www.whitehouse.gov/briefing-room/statements-releases/2021/04/28/fact-sheet-the-american-families-plan/.

Más de los autores