Faulty Foundations: State Structural Budget Problems and How to Fix Them

Executive Summary

Many critical government services in this country rely on the ability of states and localities to raise sufficient revenues to provide them. Highways and public transportation, schools and universities, health care for children and elderly individuals, environmental protection, recreational facilities, and many more services depend on state and local funds, largely raised from taxes and fees.

Yet state revenues have an imperfect track record as a stable and reliable source of funding for services. Part of the problem is cyclical. State revenues decline when the economy experiences a downturn, and because most states are required to balance their budgets even during recessions, the decline in revenues often leads to cuts in public services. Also, while states sometimes raise taxes during downturns to reduce the severity of public service cuts, often they overcompensate for these tax increases after the economy recovers by cutting taxes below the level required to maintain services.

In addition to these cyclical issues, state revenues face a more enduring problem often called a structural deficit, or the chronic inability of state revenues to grow in tandem with economic growth and the cost of government. States have structural deficits largely because they have failed to modernize their revenue systems to reflect far-reaching changes in the economy. Several states have changed their revenue systems little since the 1930s or 1940s; others have revenue systems that are twenty or thirty years out of date. While tax reform can be a difficult undertaking, failure to modernize state revenue systems can cause substantial problems.

Structural deficits received significant attention from researchers and public finance practitioners in the early 1990s, and a number of states seemed poised to begin addressing the problem. But when the unusual economic boom of the mid-1990s began to swell state revenues, the need to fix structural deficits was soon forgotten.

The following are some of the main contributors to state structural deficits; the chapters of this report discuss each factor in greater detail. (See the appendix for a full review of the literature on the issue.)

- The U.S. economy’s shift from goods to services. The increasing importance of the production and consumption of services has reduced the growth of state and local sales tax revenues, because in most states, sales taxes are levied largely on tangible goods and not on services. It also has constrained property tax revenue growth, because a service industry may have little property to tax compared to a comparably sized manufacturing industry.

- The erosion of state corporate taxes. Advances in transportation and communication have allowed corporations to operate anywhere in the country or even the world. This has largely rendered obsolete the manner in which many states tax corporations, and has made it extremely difficult for states to identify profits that should be taxable. Moreover, corporations have exploited their increasing mobility by demanding special tax breaks from states and localities as a condition of maintaining or establishing a location in a particular community.

- The growth of interstate sales. The rapid growth of the Internet and of online sales is beginning to reduce sales tax revenues significantly. Commerce over the Internet may also open up opportunities for avoiding state income taxes.

- The aging of the population. The baby boom generation will begin to turn 65 in 2011. Many states provide special income or property tax reductions based on age, often without regard to need; these tax breaks are likely to become prohibitively expensive over the next two decades. In addition, elderly people spend less than younger people — especially on taxable goods such as furniture, clothes, cars, and gasoline — so state sales tax collections will erode as the population ages.

- The erosion of state income taxes. State income tax structures are much flatter (that is, less progressive) than the federal income tax. They also have become flatter over time, as many states have failed to change their most basic tax laws in a half century or more. In addition, a number of states have reduced their top income tax rates, further reducing the growth of income tax collections relative to economic growth.

- States’ failure to maintain a mix of taxes that can grow with the cost of government. States face a number of spending pressures. Medicaid — which makes up one-sixth of state budgets — and other health-related programs continue to grow much faster than the general rate of inflation. As the baby-boom generation ages, states will face escalating costs for prescription drugs (even after the new Medicare drug benefit takes effect) and long-term care. Also, many states are facing public demands for improved education. Yet a number of states have jeopardized their ability to handle these spending pressures by making themselves more dependent on revenues from slower-growing tax sources such as sales and excise taxes, while weakening the faster-growing taxes such as the income tax and failing to maintain the estate tax.

- States’ adoption of tax and expenditure limitations and supermajority requirements. A number of states have rigid requirements in their state and local fiscal systems, such as constitutional restrictions on taxation and expenditures or supermajority requirements for increases in taxes. These restrictions make it difficult for policymakers to modernize tax codes and adjust to changing budgetary needs.

- Federal policies that harm state revenues. A number of federal laws prohibit states from taxing certain activities. The Internet Tax Freedom Act, for example, prohibits states from taxing the fees consumers pay for Internet access. As the ways in which the Internet is used for communications grow, this prohibition will increasingly undermine states’ ability to modernize their tax systems. Moreover, the federal government has so far refused to address the problem of state sales taxation of electronic commerce, which it easily could do.

Structural Deficits

When a state has a structural deficit, its normal growth of revenues is insufficient to finance the normal growth of expenditures year after year. As a result the state faces gaps between estimated revenues and expenditures.[1]

The term “normal growth of expenditures” generally refers to the amount it would cost the state to continue providing the existing level of programs and services. (This is often called a continuation budget or a current services budget.) Even if no programs or services are improved, costs generally rise from year to year because inflation pushes up the costs of purchased goods and services, because states must provide their employees with reasonable increases in wages and benefits in order compete with the private sector, and because the populations that require services may be growing. In addition to normal growth in spending, states sometimes face increased costs over which they have little control, such as natural disasters and new federal mandates.

Certainly states need not continue every program and service they currently provide, and it is healthy for a state to review its budget and determine what programs or services no longer are needed. On the other hand, new circumstances frequently arise that require an increase in expenditures, such as the popular pressure throughout the country for smaller public school classes. On balance, then, the concept of “normal growth of expenditures” remains a useful gauge of how well a state can meet its obligations.

The term “normal growth of revenues” means the revenue level that would occur in the absence of any changes in tax rates or in what is taxable. For taxes such as income taxes and sales taxes, this means the normal change in such revenues that occurs as a result of economic growth. For other taxes and revenue sources, such as cigarette taxes or lottery revenues, it may reflect changes in population or per-capita consumption.

No research has definitively determined how many states have structural deficits, but it generally is thought that most states do have this problem to some degree. Over the last ten years, three studies have examined the structural balance of each of the 50 states. These studies were prepared by Hal Hovey, a state policy expert consulting with the National Education Association; Don Boyd of the Rockefeller Institute of SUNY, Albany; and economists at Boston University and the Department of Commerce. Though these studies differed in their assumptions, techniques, and results, all three found that more than two-thirds of the states face structural deficits.

Throughout this report, we identify ten factors that contribute to a state’s propensity to face structural budget problems. These factors are:

- The extent to which services are taxed under the sales tax

- The strength of corporate income tax

- The amount of untaxed electronic commerce

- The extent of tax preferences for the elderly

- The degree of progressivity of personal income tax

- The growth of expenditure needs for residents

- Tax policy choices that worsen structural gaps

- The presence of process barriers such as tax and spending limits

- The failure to delink from federal tax changes that reduce state revenues

- The presence of structural gaps found by other studies

These factors are discussed in detail in the chapters of this report, along with discussions of policy responses.

The more of these issues that a state faces, the more likely it is that the state is currently experiencing — or is likely to experience — serious structural gaps in its budget. In order to assess the risk of structural problems faced by each state we developed a scale based on the measures discussed in this report.

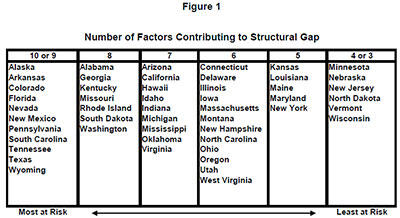

Each state received points for the factors on this list that significantly affects its budget or tax system. (See Chapter 10 for a detailed description of the construction of this scale.) The overall results are summarized in Figure 1 below. Data for the District of Columbia are included in the tables throughout the report where it was available, but, the District does not appear in Figure 1 because information was not available on many of the measures used to compute the risk scores. No state received lower than a 3 on the scale, as all states have some structural problems in their fiscal systems. Over half the states (27 states) scored 7 or higher — reflecting the many structural problems facing most states. The states most at risk for structural deficits are Alaska, Arkansas, Colorado, Florida, Nevada, New Mexico, Pennsylvania, South Carolina, Tennessee, Texas and Wyoming.

The scores assigned to states are intended to summarize the degree of risk a state faces for structural problems that result in a gap between the rate of growth of revenues and expenditures. States also face gaps between revenues and expenditures that result from other factors such as the use of one-time measures to balance budgets or the use of temporary surpluses for permanent tax cuts or spending increases. As discussed in more detail in the box on page 42 the solutions to these problems differ from the solutions to the structural growth problems that are the focus of this paper.

A number of studies in specific states have also documented structural deficits. The results of several of these studies are summarized in Appendix 2. For example:

- A long-term projection of Kentucky’s spending and revenues by Professor William Fox of the University of Tennessee found that the state faces a gap equal to 12.5 percent of its budget by 2007.

- The New Mexico Legislative Finance Committee projects a gap equal to 3.5 percent of the states’ budget by 2007.

State studies have found sizeable structural gaps even in states with a moderate number of risk factors.

- As of February, 2005, New YorkState’s Division of the Budget projected that the state’s budget would be out of balance by $5.8 billion (13 percent) by 2007 unless taxes are raised or spending is cut.

- A study of New Hampshire’s budget by the New HampshireCenter for Public Policy Studies projects a gap equal to 8.0 percent of the state’s budget by 2007.

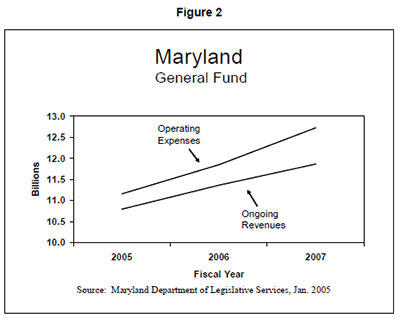

Figure 2 which shows the results of a structural deficit study in Maryland demonstrates how structural problems result in a gap between revenues and spending that widens over time.

In many states, structural deficits generally remain hidden from public attention. States manage to cover them up in a variety of ways. Some states use periodic tax increases: the substantial erosion of the sales tax base over the past few decades, for example, has been offset by increases in the sales tax rate. Between 1970 and 2003, states raised sales tax rates 72 times and lowered them only a few times. In other states, structural deficits are masked by a gradual decline of programs and services, as program benefit levels and/or payments to service providers (such as day care centers or hospitals) erode over time.

Many of the ways that states cope with structural deficits tend to reduce public confidence in government. When taxes must be increased simply to maintain current services rather than provide new ones, or when taxes remain constant but services deteriorate, the public may conclude that government is being wasteful. Thus, rather than take ad hoc measures to hide structural deficits, states would be much better off modernizing their tax systems so they appropriately reflect economic and population growth.

There are a number of changes to state tax systems that can reduce structural gaps and improve fiscal stability. These options are summarized below and discussed in more detail in the report:

- Expanding the sales tax base to include more services. State sales tax bases could be expanded to include more services in order to account for the shift in the U.S. economy from manufacturing to services.

- Closing corporate tax loopholes. States can adopt “combined reporting” under which all related corporations that are operated as a single business enterprise are treated as one taxpayer for apportionment purposes thereby preventing the shifting of profits to low- or no-tax jurisdictions. In the absence of combined reporting, states could close a specific loophole that is common to most states that allows certain types of profit-shifting. States also could enact a rule to ensure that profits earned in a state in which a corporation may not be subject to an income tax are taxed instead by its home state. Finally, they could amend the definition of apportionable “business income” to include some types of income that now go untaxed.

- Streamlining sales tax provisions among states. Forty of the 45 states with a sales tax have embarked on a project to simplify the design, administration, and compliance requirements of their sales tax. That would make it easier for companies to collect sales taxes on online purchases by out-of-state residents which should encourage Congress to pass legislation allowing states to require remote sellers to collect sales and use taxes. As of early 2005, twenty states had adopted legislation to implement the sales tax streamlining arrangement. Additional states could adopt the arrangement and could work to persuade Congress to pass the legislation.

- Reducing or eliminating tax breaks based on age. States and local governments cannot change some of the impacts that the aging of the population has on tax collections, but they can scale back or eliminate the age-related tax exemptions they enacted over the years in their property taxes and personal income taxes. One way these exemptions could be reduced is by replacing them with exemptions targeted by income as well as age.

- Updating state income taxes. States can periodically revisit and update their income tax rates and brackets to avoid a flattening of the tax structure over time.

- Adopting a state value-added tax. A value-added tax with a low rate can be used as a backstop to the corporate income tax; it would tax the business activity of companies that are not subject to the corporate income tax, as well as service companies whose products are not subject to the traditional sales tax. Such a tax could be designed in such a way that no company would have to pay both the corporate income tax and a value-added tax.

- Strengthening property taxes. States could improve the administration of the property tax — that is, the process of identifying, locating, and valuing taxable property as well as levying the tax. Also, states could carefully examine the types of property that are exempted from the tax with an eye to eliminating some exemptions.

- Resisting new tax and spending limits or modifying existing ones. States that do not have tax and spending limits, super-majority requirements, or property tax limits in place should avoid these measures, which act as barriers to addressing structural deficits. States already subject to such limits could consider modifying them to allow policymakers more flexibility to adapt to changing conditions.

- Adopting state laws to increase sales tax collections on remote sales. Without waiting for Congressional action, states can proceed on their own to address the problem of taxation of sales through the Internet and catalogs. States can expand their definition of when a company has presence in their state, require that the state do business only with companies that collect sales tax on purchases from state residents, and collect the tax on these purchases directly from consumers through the income tax.

- Improving budget transparency. State policymakers need longer-term projections of current services spending and revenues to help them understand the implications of their decisions for the state’s structural balance. This information is also critical to building support for policies that will improve the state’s fiscal stability over the long term.

- Other ideas. Additional ways to bolster state revenue growth include greater interstate cooperation in business taxation and other areas, preventing federal preemption of state and local taxes, and pursuing federal restrictions on the use of state and local tax preferences for interstate competition.

No single policy will work in every state, of course, and many of the options considered here will not be easy to implement. Yet states’ future growth and the well-being of their residents depend on the ability of state policymakers to ensure that their tax and budget decisions enhance the state’s long-term fiscal stability.

(82pp.)

End Notes

[1] When a state faces a gap between estimated revenues and expenditures in any given budget year, the problem may be the result of both a structural deficit and a revenue adequacy problem. This paper focuses on structural deficits. For a discussion of the differences between a structural deficit and a revenue adequacy problem see box on page 42.

Más de los autores

Areas of Expertise

Areas of Expertise