más allá de los números

Questions About Apple’s Tax Strategy Highlight Risks of a Territorial Tax System

U.S. corporations have lobbied aggressively in recent years for both a temporary tax holiday under which they would bring their foreign profits back to the United States and pay a much lower tax on them, as well as a permanent exemption of foreign profits from U.S. taxes (known as a “territorial” system). This week’s headlines about Apple’s reported use of offshore subsidiaries to lessen its U.S. tax bill have renewed the debate over these flawed ideas.

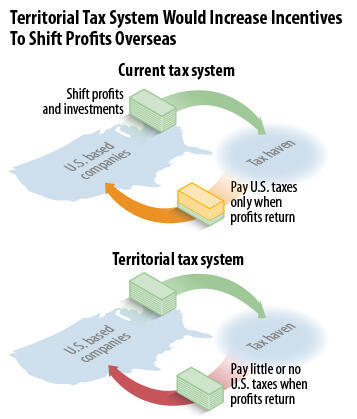

Multinational companies like Apple currently have a strong incentive to defer U.S. corporate taxes by shifting and keeping profits overseas (see chart). As we’ve explained, a territorial system would create greater incentives for those companies to invest and book profits overseas rather than at home — and that, in turn, risks reducing wages at home by encouraging investment to flow overseas, increasing budget deficits by draining revenues from the corporate income tax, or raising taxes on smaller companies and domestic businesses to offset the revenue loss.

Now, policymakers have begun to focus on the issue. The Senate Permanent Subcommittee on Investigations has issued a report that highlights the tax planning gymnastics that companies undertake to shift profits to overseas tax havens in order to avoid U.S. taxes.

Armed with more information about how these incentives are creating unfair advantages for multinationals and draining much-needed tax revenue, the President and Congress should resist the lobbying campaign and instead focus on reducing the incentive to shift profits and operations overseas.