más allá de los números

Learning About the Tax Gap Before Tomorrow’s House Hearing

The House Ways and Means Committee will hold a hearing tomorrow on the “tax gap” —between what taxpayers owe the federal government and what they pay on time. It’s particularly timely given the IRS’ depleted enforcement division and the challenges that the 2017 tax law poses for compliance. With some members of both parties proposing ways to begin to restore tax compliance funding, this hearing offers an opportunity to identify compliance needs and priorities.

There are many resources to help learn more about the tax gap, and there are important questions that lawmakers should probe at the hearing.

Size and sources of the tax gap. The IRS most recently estimated the tax gap at $406 billion, or 18 percent of federal tax liability, in a 2016 report for tax years 2008-2010. Several aspects of the report are striking. First, despite lawmakers’ past emphasis on compliance efforts focused on the Earned Income Tax Credit (EITC), all tax credits — including the EITC and the other credits — account for less than 10 percent of the tax gap. By contrast, the largest single source of the tax gap — at $125 billion, or over 30 percent of the total — is revenue that’s not paid on underreported business income that goes to owners of firms such as partnerships, S corporations, and sole proprietorships (which is often referred to as “pass-through” business income). As discussed below, this type of income received a large new tax deduction in the 2017 tax law, despite this rampant tax avoidance. The underreporting rates of various types of pass-through income ranged from 19 to 63 percent for tax years 2008-2010, the IRS tax-gap report shows.

And the tax-gap report doesn’t address the extent to which foreign tax evasion, such as Americans’ sheltering of their income in foreign bank accounts, contributes to the tax gap. As the Government Accountability Office (GAO) recently reported, the “IRS does not have an estimate of the revenue loss due to offshore noncompliance. However, international tax policy experts believe that the losses are in the billions of dollars annually.” If the IRS could estimate these losses, the $406 billion tax gap would be even larger.

All of that raises several questions that lawmakers should pursue at the hearing. Is IRS reporting on the tax gap sufficiently comprehensive, and is the tax-gap report issued on a sufficiently regular and timely basis? In addition, given the high under-reporting of income by pass-through entities and the large share of the tax gap that’s attributable to these firms, do the IRS, Treasury Department, and GAO report enough to Congress on pass-through noncompliance rates and provide sufficient analysis on how to address that noncompliance? And, given that foreign bank accounts are used to evade taxes, should the IRS tax-gap report seek to include information on this form of tax evasion?

Depleted IRS enforcement. Since 2010, the IRS budget, and the IRS enforcement division in particular, have been targeted for deep budget cuts. Inadequate IRS funding for enforcement reduces compliance activity, which increases the tax gap. As we recently observed:

IRS enforcement is now so depleted that the agency has only about the same number of revenue agents (auditors who tend to audit the most complex returns) as it had in the 1950s when the economy was roughly one-seventh its current size. The share of returns that the IRS audits has fallen by 40 percent since 2010, and audit rates for high-income people and large corporations are especially low. For example, fewer than 1 in 20 individuals whose income exceeded $1 million were audited in 2017, roughly half the share in 2010.

In that CBPP report, we recommend reversing — over something like a four-year period — the budget cuts in IRS enforcement since 2010. We also discuss promising bipartisan proposals to create a budgetary mechanism that could help accomplish this goal.

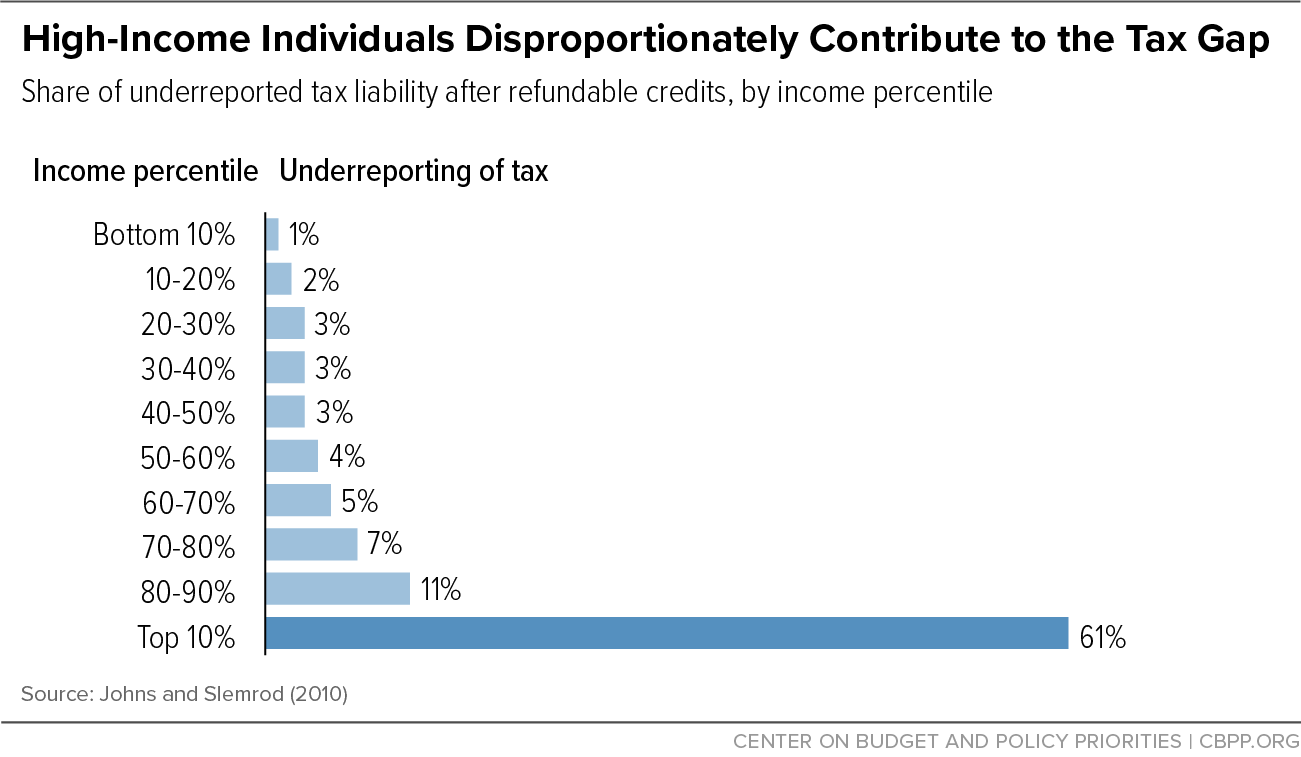

Reducing audits of high-income taxpayers is shortsighted, as wealthy filers contribute the highest dollar amount to the tax gap, according to a 2010 report (see chart).

A series of ProPublica reports further illuminate these issues and are must-reads on IRS enforcement funding. They include: “How the IRS Was Gutted,” “Where in the U.S. Are You Most Likely to Be Audited by the IRS?,” “After Budget Cuts, the IRS Work Against Tax Cheats is Facing ‘Collapse,’” “Why the Rich Don’t Get Audited,” and “You Can’t Tax the Rich Without the IRS.”

This raises a number of issues for lawmakers about how to begin rebuilding IRS enforcement. Both President Trump’s fiscal year 2020 budget and some House proposals would provide additional IRS enforcement funding outside the statutory caps on appropriations for discretionary (i.e., non-entitlement) programs, an approach dating back to the bipartisan 1990 Budget Enforcement Act. That strongly merits exploration.

In addition, lawmakers should examine the extent to which the IRS needs more auditors to handle complex returns from high-income individuals and to reverse the sharp decline in the audit rates for those filers. Lawmakers should consider what a reasonable multi-year path to rebuilding this capacity would be.

Compliance and the 2017 tax law. True tax reform would simplify the tax code and narrow the gaps between how different types of income are taxed. As we have noted, the 2017 tax law does the opposite, adding complexity to the tax code and introducing new, arbitrary distinctions between different kinds of income, which creates new gaming opportunities. Lawmakers should probe whether the IRS and Treasury Department have analyzed the compliance challenges that the 2017 law poses, particularly its pass-through deduction.

Foreign tax evasion. A New York Times article documented ways in which wealthy individuals hide money overseas to evade U.S. taxes. The recent examples of Paul Manafort and Richard Gates further highlight such tax compliance concerns; as their indictment stated, they “hid the existence of the foreign companies and bank accounts, falsely and repeatedly reporting to their tax preparers and to the United States that they had no foreign bank accounts.” As noted above, foreign tax evasion isn’t included in the IRS tax-gap analysis. Lawmakers can probe whether the IRS can broaden its tax-gap analysis to include these revenue losses.

Lawmakers also should raise additional questions. Paul Manafort’s foreign tax evasion was discovered not through a typical tax audit, but through a separate criminal investigation. Have the IRS, GAO, or the Treasury Inspector General for Tax Administration focused on the extent to which other high-income individuals may be evading taxes in similar ways? Should there be a more vigorous tax compliance response to address this problem?

On a related front, GAO recently studied the IRS’ implementation of the Foreign Account Tax Compliance Act (FATCA), which was enacted in 2010 to reduce evasion by increasing transparency of offshore accounts. It found the “IRS documentation states that only 7 of 31 capabilities outlined in the FATCA Compliance Roadmap were delivered due to funding constraints.” Lawmakers should look into whether the IRS has the resources it needs to vigorously pursue this important area of tax compliance.