más allá de los números

Costly Estate Tax Giveaway Should Expire After 2012

A little-noticed feature of last December’s tax cut-unemployment insurance deal between President Obama and congressional Republicans was a further cut in the estate tax below its already-low 2009 level. The current estate tax rules run through the end of 2012, and in a new paper we explain why Congress should let them expire on schedule.

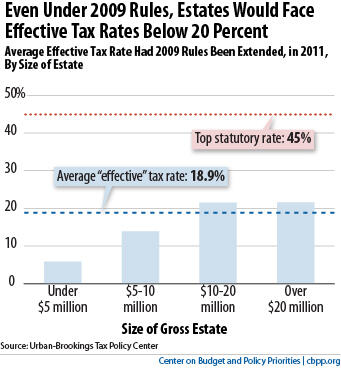

If policymakers had extended the 2009 rules last year, only 6,460 estates nationwide would have owed any estate tax in 2011, according to the Tax Policy Center. And they would have owed only 18.9 percent of the estate’s value in tax, on average —far below the statutory rate of 45 percent that applied to the value of the estate above the exempted amount (see chart).

Instead, policymakers cut the tax further. The December agreement raised the exemption level to $5 million ($10 million for couples) and lowered the marginal rate to 35 percent for 2011 and 2012. Taxable estates will average more than $1 million apiece in tax breaks this year from the new rules. Estates worth more than $20 million will receive nearly $3.8 million apiece, on average.

Extending the current rules past 2012 would be very expensive — over a full decade, about $80 billion more expensive than maintaining the more-than-generous 2009 rules. That would be hard to justify even if we weren’t facing serious long-term budget problems. But we are, and members of Congress are proposing to slash programs ranging from education to infrastructure to Medicare to programs that help the poorest Americans meet basic necessities. Given these facts, extending the current rules would be unseemly.