Full-Year Continuing Resolution Would Miss Chance for Sequestration Relief

Congress is expected to begin debate soon on a short-term “continuing resolution” (CR), which is needed to avoid a government shutdown when the new fiscal year starts on October 1. A short-term CR would temporarily continue defense and non-defense appropriations at the current 2015 levels. Policymakers should use that time to resolve issues around the 2016 appropriations, including reaching agreement on a plan to raise the funding caps that the 2011 Budget Control Act set and sequestration subsequently lowered.

A full-year Continuing resolution would be highly problematic.These negotiations will be difficult. Some have suggested that when the short-term CR expires, a better alternative could be simply to replace it with a full-year CR — that is, a bill that basically extends 2015 appropriations for the remainder of 2016. While such an approach might be a way to avoid some controversial legislative riders, a full-year CR would be highly problematic for at least three reasons:

- It would lock in the low sequestration levels. A full-year CR would not solve the fundamental problem that the existing appropriations caps are too low to meet national needs. The sequestration relief provided in the 2013 Bipartisan Budget Agreement covered only two years, 2014 and 2015, leaving sequestration’s full effects in place for 2016. The non-defense cap for 2016 is only $1.1 billion, or 0.2 percent, higher than the 2015 enacted level — but $9 billion lower than the 2015 level when accounting for inflation (and still farther below when increases in costs beyond inflation for veterans’ medical care are taken into account). In fact, the 2016 cap would result in spending on these non-defense programs equaling the lowest level in the last five decades, when measured relative to the size of the economy.

- It would not protect non-defense programs from cuts. A full-year continuing resolution, like any other appropriations legislation, would have to comply with the caps. While the 2016 caps are roughly equal to the 2015 enacted levels, various factors would push a full-year CR over the non-defense cap by several billion dollars and require offsetting cuts even if it did nothing but continue last year’s appropriations law. These factors include advance appropriations that already provide substantial increases for veterans’ medical care in 2016 and decreases in certain receipts that are deducted from appropriations, such as those for mortgage insurance programs. In addition, policymakers are sure to face pressures to meet selected high-priority needs in 2016 as part of a full-year CR, requiring further cuts in other non-defense programs to stay within the cap.

- It would enable higher defense spending and abrogate the parity principle that underlies sequestration and the Budget Control Act. On the defense side, if the full-year CR continued the special appropriations for war-related “Overseas Contingency Operations” at last year’s level, it would be providing considerably more of that funding than the Administration says it needs, with the excess being channeled to the regular defense budget. This would, in effect, provide relief for defense appropriations while doing nothing comparable for non-defense programs. This would violate the principle that sequestration relief be provided equally to both defense and non-defense programs, just as the sequestration cuts were equally divided between defense and non-defense.

Fundamentally, a full-year CR at the current post-sequestration caps would forgo the opportunity that an agreement on sequestration relief would provide to begin restoring lost purchasing power and to make more adequate investments in areas such as scientific and medical research; job training; transportation and other infrastructure; and elementary, secondary, and early childhood education, as well as to reverse declines in services to the public at core agencies such as the Social Security Administration and the Internal Revenue Service.

Further, whatever appropriations are enacted for 2016 are likely to continue for at least several months of the following fiscal year, as the election and presidential transition are almost certain to delay action on 2017 appropriations. Thus, if 2015 appropriations are extended for 2016, they can be expected to continue well into 2017, growing steadily more inadequate — and more outdated, with some programs whose needs have declined receiving too much while numerous other programs are inadequately funded.

The only real fix is for policymakers to agree to provide relief from the sequestration cuts now scheduled for 2016, offsetting the cuts with alternate deficit reduction measures, as they did on a bipartisan basis in 2013, and then to enact regular appropriations legislation for 2016 (even if combined into one or more omnibus packages). As long as the current sequestration limits remain in place, no amount of re-arranging the pieces within an inadequate total will allow for necessary funding levels to reflect new priorities, new conditions, or rising costs.

Full-Year Continuing Resolutions Have Always Been Last Resorts

A continuing resolution is legislation that allows the federal government to continue operating even through policymakers have not enacted regular appropriations for the fiscal year. Rather than specifying amounts for each individual account or program, CRs set funding levels mostly by formula, usually permitting spending at the same rate as in the previous year (occasionally with an across-the-board cut or increase) and under the same terms and conditions as in the previous year’s appropriations legislation.

CRs also usually include at least a few “anomaly” provisions, which set spending rates for particular accounts or programs at different levels from what the general formula would provide. Anomaly language is also sometimes used to alter specific appropriations terms and conditions or extend expiring authorities.

The most common kind of CR is a part-year measure (a short-term CR) with a specific end date, used to keep the government operating while lawmakers conclude their negotiations on regular appropriations legislation for the full fiscal year. Occasionally, however, after efforts to enact regular appropriations have broken down, CRs have been used to provide spending authority through the end of the fiscal year.

Full-year CRs typically include more anomaly provisions than a short-term CR and tend to be rather lengthy and complex. Thus, the full-year CR approach is no guarantee against the addition of new and problematic legislative riders — policy provisions attached to appropriations bills — although there are likely to be fewer than in regular appropriations legislation. In this case, however, there will be pressure to minimize controversial riders in whatever final appropriations are enacted for 2016 — whether in a full-year CR or a regular appropriations package — in order to avoid opposition from Democrats in the House and Senate and veto by the President.

Full-year CRs have been used only four times in the past 30 years, in 1992, 2007, 2011, and 2013. None covered all appropriated programs.[1] And all were enacted four to six months after the fiscal year had begun, after a series of short-term CRs had been tried first. Full-year CRs have always been last resorts rather than a preferred approach to appropriations.

Existing Caps Tightly Constrain 2016 Funding

Unless agreement is reached to alter the law, the overall cap on non-defense appropriations will rise by only 0.2 percent in 2016, or $1.1 billion. The increase in the defense cap is only slightly larger: 0.3 percent or $1.8 billion.[2]

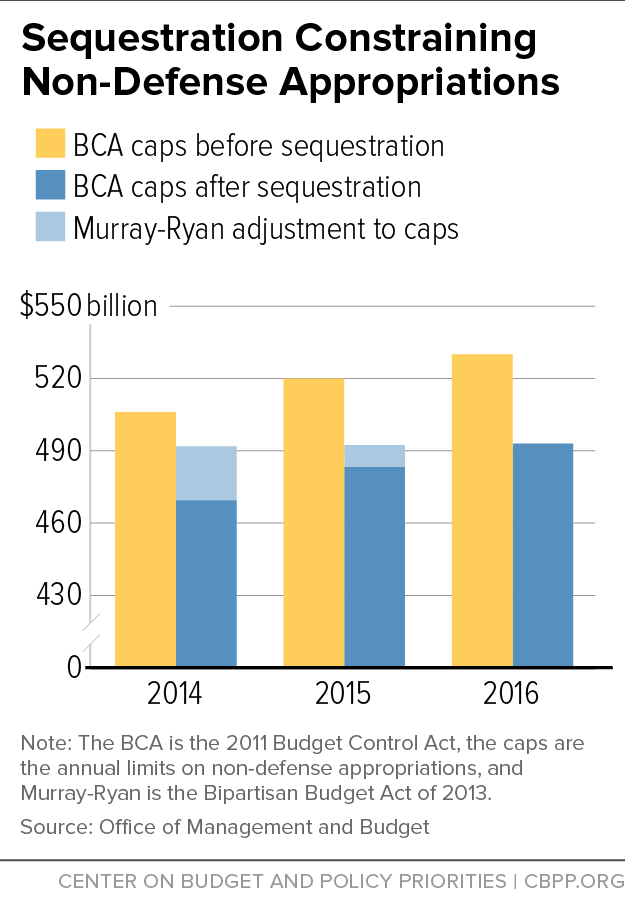

The caps were set by the Budget Control Act (BCA) and then subsequently lowered by sequestration. The 2013 Bipartisan Budget Agreement reached in December 2013 (often called the “Murray-Ryan Agreement” for Sen. Patty Murray and Rep. Paul Ryan, the then-Budget Committee chairs who negotiated the deal) provided some relief from sequestration in 2014 and 2015, with other deficit reduction measures offsetting the cost of the relief.

The Murray-Ryan deal expired at the end of 2015, however, and therefore the 2016 BCA caps have been reduced by the full sequestration amount. As a result, the 2016 defense and non-defense appropriations limits are essentially the same as those for 2015 in nominal terms and are below the 2015 levels once inflation is taken into account. (See Figure 1.)

Moreover, the cumulative effect of the cuts enacted since 2010 is growing. The 2016 cap is 17 percent below the 2010 level, in inflation-adjusted terms.[3]

Full-Year CR Would Require Non-Defense Program Cuts

Appropriations must comply with the BCA caps on defense and non-defense spending regardless of whether they are enacted through regular appropriations legislation or a full-year CR. If one or both of the caps is breached, the law requires automatic across-the-board spending cuts to eliminate the breach.[4]

A full-year continuing resolution is unlikely to be a painless way of adhering to the BCA caps. Rather, the tight caps would create problems for a full-year CR just as they have created problems for the development of regular 2016 appropriations bills. Even a “clean” CR that does nothing more than extend the 2015 appropriations legislation would breach the non-defense appropriations cap by roughly $7 billion, according to preliminary estimates the Congressional Budget Office (CBO) has provided to congressional committees.[5]

The single biggest reason for this is a $3 billion increase for veterans’ medical care that has already been enacted for 2016, through advance appropriations made in last year’s bill.[6] The increase is almost three times larger than the $1.1 billion total increase allowed under the cap for all of non-defense discretionary funding, meaning this factor alone would trigger a breach.

A second factor is receipts from federal mortgage insurance programs, which CBO projects will fall by $1.1 billion in 2016. These are appropriated programs, and their receipts, net of costs, are credited to the applicable appropriations bill. Lower receipts mean higher overall costs for 2016 appropriations.

CBO has identified several other technical factors that could cause the cost of even a clean CR to exceed 2015 funding levels. Many involve rescissions or limitations on spending that would not produce as much savings in 2016 as they did in 2015 — for example, because there are less funds to rescind. Some, but not all, of those costs could probably be eliminated by adjusting the language of the CR. But such adjustments might be considered controversial departures from the idea of a clean continuing resolution.

In addition, in some cases, a funding increase is needed to keep an activity from running out of money. A good example is the appropriation that covers the cost of maintaining federal prisoners in state, local, or private jails. The 2015 appropriations legislation transferred $1.1 billion in surplus proceeds from asset forfeitures to help cover these costs. But no similar surplus is expected for 2016, and therefore regular appropriations will need to be increased to keep the account from running out of funds during the year.

Moreover, there may be a desire to meet some very high priority needs, even in a full-year CR. For example, the President’s budget and the House and Senate appropriations bills all propose increases for veterans’ programs in addition to those already enacted through advance appropriations, for things like processing disability benefit applications, improving information technology, and covering additional health care expenses. It seems likely that Congress would want to address these needs in a full-year CR.

Another example might be the costs of renewing housing assistance for people currently receiving it. Those costs rise because of rising rents, but also because of other factors such as one-time savings achieved last year by shifting contract renewal dates. The House and Senate versions of the 2016 appropriations bill provide increases of $1.65 billion and $1.59 billion, respectively, to cover the costs of simply renewing existing Housing Choice Vouchers and project-based rental assistance contracts, and both amounts are less than the $1.87 billion the Administration says is needed for that purpose. If the eventual 2016 appropriations legislation — full-year CR or otherwise — does not include the necessary increases, tens of thousands of low-income families could lose their housing assistance. Some could become homeless.

Full-Year CR Would Provide Unequal Relief from Defense Cap

In contrast, a full-year CR at 2015 levels would provide relief to defense appropriations. This is because it would continue special war-related appropriations, known as Overseas Contingency Operations (OCO) funding, at current levels (unless special anomaly language were included to lower those levels). The Administration has proposed to reduce OCO defense funding below the 2015 level, reflecting reduced U.S. military operations in Iraq and Afghanistan. CBO estimates that the CR level would be nearly $15 billion more than what the Pentagon says it needs for OCO.

Appropriating more OCO funds than the Pentagon believes necessary for that purpose would provide backdoor relief from the cap on defense appropriations, since OCO funds are exempt from the BCA caps but somewhat interchangeable with non-OCO funds. In this way, a full-year CR would serve as a scaled-back version of the gimmick included in the 2016 congressional budget resolution, which called for evading the BCA cap on defense appropriations by providing $38 billion more than is needed for OCO and explicitly making those funds available for non-OCO needs.[7] In fact, the House-passed defense authorization bill explicitly describes the additional $38 billion as being for “support of base budget requirements.”

By providing relief from sequestration only on the defense side of the budget, a full-year CR would violate the basic principle of parity between defense and non-defense sequestration cuts and relief. This principle reflects the fact that the BCA divides the sequestration cuts evenly between defense and non-defense programs. The two previous rounds of sequestration relief followed the parity principle.

Full-Year CR Would Likely Continue 2015 Funding Decisions Into 2017

In four of the past five presidential or congressional election years, final action on appropriations for the fiscal year beginning on October 1 was delayed until the following calendar year.[8] During all of these long delays, much of the government was kept operating under part-year continuing resolutions based on the prior year’s funding levels.

There’s no reason to expect things to be much different for fiscal year 2017, which begins in October 2016. Therefore, whatever funding levels are set for 2016 are likely to continue for a number of months into 2017. If the outcome for 2016 is a full-year continuing resolution based on 2015 appropriations, those 2015 levels are likely to continue for not just an additional year but rather for close to a year and a half.

That is a long time to keep the government on autopilot. It’s also a long time to keep 2015 funding levels in place, with no increases or decreases to reflect changes in priorities, altered circumstances, or rising costs.

A far better solution would be regular appropriations decisions for 2016, based on higher caps resulting from a new round of sequestration relief. That would produce more adequate funding levels for 2016. And if those 2016 levels have to be extended into 2017, as history suggests they will be, at least the temporary appropriations for the first months of 2017 would be based on 2016 appropriations that are both more up-to-date and more adequate.

End Notes

[1] In fact, the 1992 full-year CR covered only programs in a single appropriations bill, the Foreign Operations bill.

[2] For more information on the BCA caps, sequestration, and the Murray-Ryan agreement, see David Reich, “Sequestration and Its Impact on Non-Defense Appropriations,” Center on Budget and Policy Priorities, February 19, 2015, https://www.cbpp.org/research/sequestration-and-its-impact-on-non-defense-appropriations.

[3] Part of the reductions to meet the caps came through a decrease in Census Bureau funding after the 2010 decennial census, increases in receipts from mortgage insurance programs (although those receipts are now decreasing), and certain changes in mandatory programs, rather than entirely through cuts in ongoing non-defense appropriations. On the other hand, the 17 percent overall figure doesn’t address other factors such as population growth, and substantial increases for veterans’ medical care have squeezed other non-defense appropriations significantly.

[4] Because the BCA specifies that compliance with the annual appropriations caps is to be initially measured 15 days after Congress adjourns at the end of a session, a part-year CR will not trigger across-the-board cuts even if it temporarily allows a spending rate that would exceed the caps, as long as Congress fixes any breach before it adjourns.

[5] The same is apparently not true for defense. The preliminary CBO estimate suggests that defense funding under a CR would be slightly under its 2016 cap.

[6] Advance appropriations for veterans’ medical care are now standard practice, done to make sure that the necessary funding is in place at the start of the fiscal year even if overall appropriations are delayed.

[7] David Reich, “House Bill Would Circumvent Budget Cap for Defense,” Center on Budget and Policy Priorities, May 14, 2015, https://www.cbpp.org/blog/house-bill-would-circumvent-budget-cap-for-defense.

[8] For fiscal year 2011 (which began on October 1, 2010), appropriations were not finished until April 2011 — more than halfway through the fiscal year. For fiscal years 2009 and 2013, finalizing appropriations took until March. For fiscal year 2007, final action came in February.

More from the Authors