CBPP's Updated Projections Show Long-Term Budget Outlook Is Significantly Improved but Remains Challenging

This report has been updated to reflect newly available data. Click here to view the new analysis.

No deficit or debt crisis looms, and the weak labor market remains the nation’s most immediate economic concern. But policymakers and the public should not ignore the long-run budget problems, which remain challenging. Policymakers should address the need both for immediate measures to strengthen the job market and for measures to reduce longer-term deficits, which should take effect when the economy has more fully recovered.

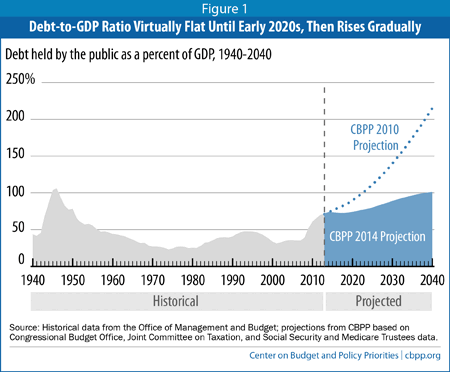

Under current policies, the federal debt will be virtually flat, in relation to the economy, for the next several years and then slowly rise. The projected ratio of debt to gross domestic product (GDP) — which was 72 percent at the end of fiscal year 2013 — will reach 74 percent by 2020 and 101 percent by 2040. That’s a marked improvement over the situation just four years ago (see Figure 1), but policymakers need to take further significant steps to address the problem.

A stable — or declining — debt-to-GDP ratio is a common goal for fiscal stability. Although a rising debt ratio may be advantageous when the economy is operating well below its potential, as it has been since 2008, a rising debt ratio in good times reflects an unsustainable budget policy that ultimately poses threats to financial stability and long-term growth. Policymakers should reduce projected debt-to-GDP ratios through carefully designed policies that strengthen (rather than weaken) the slow economic recovery in the near term, while putting in place equitable and balanced deficit reduction that grows in size over time.[1] (See box.)

Our new projections update those we published in June 2013 to reflect the latest Congressional Budget Office (CBO) baseline budget projections, changes in budgetary policies, and other recent developments.[2] The technical note at the end of this paper provides more information about how we made the projections.

The Revenue Outlook

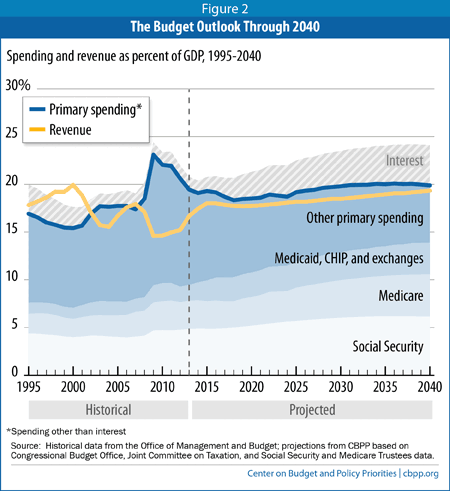

Federal revenues are projected to rise under current policies from 17.5 percent of GDP in 2014 to around 18 percent in 2015 through 2024, due largely to the economic recovery. After 2024, two trends — rising real incomes that push people into higher tax brackets (so-called “real bracket creep”) and growing, taxable withdrawals from tax-favored retirement accounts by an aging population — will help push up revenues gradually, as a percentage of GDP. By 2040, they are projected to reach 19.3 percent of GDP, roughly their level in the final years of the Clinton Administration, when the nation last ran budget surpluses.[3] (See Figure 2.)

The Debt-to-GDP Ratio

Generally, the debt-to-GDP ratio should rise only during hard times or major emergencies and then decline during good times. That enables the government to combat recessions through tax cuts and spending increases (and to alleviate hardship during bad times), while creating a presumption against policies that markedly increase the debt during good times.

A stable debt-to-GDP ratio is a key test of fiscal sustainability. Increases in the dollar amount of debt are not a serious concern as long as the economy is growing at least as fast. Between 1946 and 1974, for example, debt held by the public grew significantly in dollar terms but — thanks to economic growth — plummeted as a percentage of GDP, from 109 percent to 24 percent.

Some suggest that certain debt-to-GDP ratios have a particular meaning in terms of their effect on the economy. In reality, there are no absolute thresholds.

Until recently, for instance, many pointed to a 2010 analysis by economists Carmen Reinhart and Kenneth Rogoff suggesting that debt-to-GDP ratios of 90 percent or more are associated with significantly slower economic growth. But the authors have acknowledged computational errors in their original work and clarified that there is no “magic threshold” for the debt ratio above which countries suddenly pay a marked penalty in terms of slower economic growth. To the extent that countries with higher levels of debt experience slower growth, there is not much evidence that the high debt caused the slow growth; the reverse is just as likely to be true — that the slow growth caused the high debt — or some combination of the two effects.

Similarly, some analysts call for a debt ratio of 60 percent of GDP or less, a goal that the European Union and the International Monetary Fund (IMF) adopted some years ago. No economic evidence, however, supports this or any other specific target, and IMF staff have made clear that the 60 percent criterion is arbitrary and should not guide near-term fiscal policy in the wake of the recent financial crisis, which drove up government debt worldwide.

All else being equal, a lower debt-to-GDP ratio is preferred because of the additional flexibility it provides policymakers facing economic or financial crises and the lower interest burden it carries. But, all else is never equal. Lowering the debt ratio comes at a cost, requiring larger spending cuts, higher revenues, or both. That is why we emphasize the importance of not only the quantity but also the quality of deficit reduction, which should not hinder the economic recovery or cut spending in areas that can boost future productivity or harm vulnerable members of society.

The Spending Outlook

Total federal outlays are expected to rise from 20.4 percent of GDP in 2014 to 24.1 percent of GDP in 2040. Only about one-fifth of the rise stems from primary, or non-interest, spending — that is, spending on programs that pay benefits to ordinary Americans and carry out the functions of government. (See Figure 2.) The bulk of the rise stems from net interest, as interest rates return to normal from their recent historic lows and as the federal debt gradually mounts. If interest rates rise less than CBO assumes — as the International Monetary Fund and some other analysts expect — interest spending, deficits, and debt will also rise less rapidly.[4]

The composition of federal non-interest spending will also change significantly between now and 2040. Because of an aging population and rising health care costs, Social Security, Medicare, Medicaid, and health insurance subsidies will grow substantially — both as a percentage of GDP and as a share of total federal spending — while the reverse is true, in aggregate, for all other programs. Social Security and the major health programs, which today account for 51 percent of non-interest spending, are projected to reach 70 percent of the total in 2040, with all other programs representing a correspondingly smaller share.

Social Security. Benefits under the Old-Age, Survivors, and Disability Insurance programs (together known as Social Security) will rise slowly but steadily in the next two decades — from a bit under 5 percent of GDP today to just over 6 percent in the 2030s — and then stabilize. That pattern largely mirrors the aging of the population, and is dampened by the scheduled rise in the program’s full retirement age — which was historically 65, is now 66, and will climb to 67 between 2017 and 2022. (Each year that the full retirement age is raised lowers benefits across the board for future retirees by about 7 percent, regardless of whether they claim benefits early or work until the full retirement age or beyond).[5]

Medicare. Net outlays for Medicare benefits — that is, total payments minus the premiums that enrollees pay — are expected to rise from just under 3 percent of GDP today to about 4½ percent in the late 2030s. Medicare fundamentally faces the same demographic pressures as Social Security. Unlike Social Security, Medicare faces an extra source of cost pressure: the tendency of medical costs, fueled by technological advances and increased utilization, to outpace GDP growth. The cost controls and delivery system reforms in the Affordable Care Act (ACA), plus other developments in health care delivery, are expected to curb (though not erase) that pressure. Our projections are based on current law and assume that policymakers will retain the ACA’s cost-control provisions.

Medicaid, CHIP, and health insurance subsidies. Medicaid — a joint federal and state program — provides health coverage and often nursing home care to eligible low-income people, while the Children’s Health Insurance Program (CHIP) covers many low-income children through capped grants to states. The ACA expanded the reach of Medicaid, at state option, and also created new state-based marketplaces to enable millions of people without other coverage to buy health insurance at reasonable prices and without exclusions for pre-existing conditions or other restrictions that often made coverage unaffordable. The combination of an aging population, health-cost growth, and the ACA expansions will push up spending for this trio of programs by nearly a percentage point of GDP in the coming decade — from 1.9 percent this year to 2.7 percent in 2024, with most of that growth occurring by 2017. After 2024, cost and demographic pressures will lead this category of health spending to reach 3.3 percent of GDP in 2040.

The fact that health care costs remain the largest driver of increased future spending should not obscure how dramatically those projected costs have fallen over the last few years. As Figure 1 shows, in January 2010 we projected that debt would exceed 200 percent of GDP by 2040; we now project less than half that ratio. Much of the improvement is from lower health care costs: in January 2010 we projected that Medicare and Medicaid together would cost 11.1 percent of GDP in 2040, but we now project that Medicare, Medicaid including the expansion, CHIP, and the new marketplace subsidies will together cost 7.7 percent of GDP, or about 30 percent lower than the previous estimate. The ACA directly and substantially reduced the rate of growth of Medicare spending. In addition, in response to a broad and persistent slowdown in the rate of growth of health care costs, the Congressional Budget Office has reduced its projections of Medicare and Medicaid spending by a further $1.2 trillion over the 2010-2020 period. These developments have substantially improved the long-run fiscal outlook.[6]

Other program spending. This category includes hundreds of programs for which Congress appropriates funding on an annual basis — known as defense and nondefense discretionary programs — as well as entitlement or mandatory programs such as SNAP (formerly known as food stamps); pensions for federal civilian and military retirees; veterans’ disability and education benefits; the refundable portions of the Earned Income Tax Credit and certain other tax credits; Supplemental Security Income (SSI) for poor elderly and disabled people; unemployment insurance; Temporary Assistance for Needy Families (TANF); farm price supports; and various smaller programs.

Over the next ten years, this broad category — which peaked at nearly 14 percent of GDP during the economic downturn — will fall, as a percentage of GDP, from 9.3 percent in 2014 to 7.2 percent in 2024. Most of this drop occurs in discretionary spending and is concentrated between now and 2021, as the caps and sequestration provisions of the Budget Control Act (BCA) squeeze defense and nondefense programs alike, and as the war in Afghanistan continues to wind down. Spending for the entitlement and other mandatory programs in this part of the budget also drifts down as a percentage of GDP, though less precipitously; unlike Social Security and the major health programs, most other entitlement and mandatory programs do not face particular demographic or cost pressures, and some — such as unemployment insurance and SNAP — will shrink naturally as the economy recovers.[7]

After 2021 (for discretionary programs) and after 2024 (for the entire “other program spending” category), we assume that outlays keep up with inflation and population growth — in other words, that real spending, per capita, remains constant. That’s consistent with the historical pattern, in which such spending rose (in per-capita terms), except during recessions, only when policymakers took steps to expand these programs. Our approach implies a continued downward drift in “other spending” as a percentage of GDP, from 7.2 percent in 2024 to 6.0 percent in 2040.[8]

Interest. Unlike every other spending category, net interest doesn’t reflect explicit funding decisions by lawmakers. Instead, it’s jointly determined by the amount of borrowing fueled by policymakers’ other spending and revenue decisions (in other words, the debt) and by the interest rates set in financial markets.

Today, federal net interest costs represent just 1.3 percent of GDP, almost matching the historic lows posted in the 1950s through early 1970s and again in the early 2000s, when federal debt was far smaller. But today’s low interest rates, which are holding down borrowing costs, will not last forever. As a result, by 2024, net interest costs — at 3.3 percent of GDP — are expected to be about two and a half times today’s level, even though the debt climbs only modestly (from 74 percent to 79 percent of GDP) during that period. By 2040, we expect that both net interest and debt will grow by another quarter — from 3.3 to 4.2 percent of GDP (in the case of net interest), and from 79 to 101 percent of GDP (in the case of debt).

Assuring Solvency for Social Security and Medicare

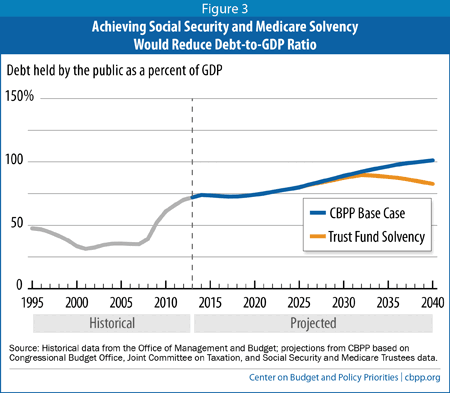

Bringing the Social Security and HI trust funds into financial balance — through tax increases, benefit cuts, or some combination of the two — would also forestall much of the projected rise in the debt-to-GDP ratio. If Social Security and HI expenditures were equal to their revenues in each year after the programs’ projected insolvency, federal debt would peak at 90 percent of GDP in 2032 and decline to 83 percent of GDP by 2040. (See Figure 3.)

Uncertainty of Long-Run Projections

Users of these or any long-run budget projections should keep in mind that they are highly uncertain. CBO has estimated, for example, that if productivity in the economy grew by ½ percent a year less or more rapidly than it projects, the debt-to-GDP ratio in 25 years would be about 45 percentage points higher or lower.[11] Thus, the debt-to-GDP ratio in 2040 under current budgetary policies could easily be as high as 150 percent or as low as 50 percent, given our mid-range projection of 101 percent. Since other critical variables, such as interest rates and health care costs, are also inherently difficult to predict, the actual range of uncertainty surrounding these long-run projections is even greater.

Policymakers shouldn’t ignore long-run budget projections just because they’re uncertain. After all, some of the important underlying trends — notably the aging of the population and rising health costs — are highly probable, even if we can’t precisely predict their magnitude. But the uncertainty grows dramatically as the time horizon expands. That’s why we and CBO focus on the next three decades or so for long-run budget estimates, a period that amply documents future fiscal pressures and presents a reasonable horizon for policymakers.

Technical Note

We base the first ten years of our projections on CBO’s baseline budget projections that were published in April 2014.[12] We adjust those projections in a few respects to better reflect current tax and spending policies. Specifically, we assume that a collection of business and individual tax deductions and credits, known as “normal tax extenders,” will not expire on schedule, but rather will continue indefinitely without offsetting savings; that improvements to refundable tax credits (the Child Tax Credit, Earned Income Tax Credit, and American Opportunity Tax Credit) in the 2009 Recovery Act — which policymakers have extended twice — will not expire in 2017 but will be permanently extended; and that the United States will reduce troop levels in Afghanistan to 30,000 by 2017. All of these adjustments are based on alternatives published by CBO, and are described in an earlier CBPP report.[13]

In addition, the projections assume that funding for non-entitlement programs will grow with both inflation and population after caps on this category of funding expire in 2021. In contrast, the CBO baseline adjusts these programs only for inflation.

Here are some important adjustments we don’t make to CBO’s ten-year projections. We do not assume that Congress will breach the BCA caps on discretionary funding, or repeal sequestration; we assume that the costs of any relief in this area will be offset. (In the Murray-Ryan budget agreement of December 2013, legislators raised the caps for 2014 and 2015 but paid for the costs with other savings; we view that as a precedent.) After the BCA caps expire in 2021, we assume discretionary spending will grow with inflation plus population.

Similarly, we do not assume that lawmakers will repeal or waive the sustainable growth rate (SGR) provision that constrains Medicare’s payment rates to physicians; Congress has set a precedent of paying, over time, for such measures, and we assume that pattern continues.[14]

CBO’s latest ten-year projections — on which, with the adjustments explained above, we base our estimates through 2024 — don’t extend past that date. Therefore, we based our extrapolation through 2040 on other recent sources. Those include CBO’s most recent long-term outlook (published in September 2013) and the latest reports of the Social Security and Medicare trustees (published in May 2013). Naturally, those sources have slightly different values for spending and revenues in 2024 (the “jump-off” point) than our new ten-year projection does. We handle that by taking our 2024 value and then growing it at the same rate, as a percentage of GDP, as the relevant CBO or trustees’ projection.[15] As a result, whatever (small) difference exists in the 2024 value will persist over time. Our approach therefore avoids a sudden discontinuity in the projections.

Specifically, we assume that after 2024:

- Revenues grow with the projections in CBO’s September 2013 extended baseline.

- Social Security and Medicare costs grow with those from the trustees’ intermediate projections.

- Medicaid, CHIP, and health insurance subsidy costs grow with those in CBO’s September 2013 extended baseline.

- “Other program spending” — for defense and nondefense discretionary appropriations, plus outlays for entitlement and mandatory programs other than Social Security and the big health programs — grow with inflation plus population, thus keeping real per-capita spending constant at 2024 levels.

- For net interest, we calculate how much borrowing results from the revenue and spending totals already calculated, and we apply the overall interest rate on federal debt, assuming the average interest rates that CBO projects over the 2018-2024 period.

Table 1 shows our projections for each major category of the budget as a share of GDP between 2000 and 2040. Data for each year, including historical values since 1962, are posted on our website.

| Table 1 Outlays, Revenues, Deficits, and Debt as a Share of GDP Through 2040 |

|||||||||

| Social Security | Medicare | Medicaid, CHIP, and exchanges | Other program outlays | Total program outlays | Net interest | Revenues | Surplus(+)/ deficit(-) | Debt held by the public | |

| 2000 | 4.0% | 1.9% | 1.2% | 8.3% | 15.4% | 2.2% | 19.9% | 2.3% | 34% |

| 2005 | 4.0% | 2.3% | 1.4% | 10.0% | 17.7% | 1.4% | 16.7% | -2.5% | 36% |

| 2010 | 4.7% | 3.0% | 1.9% | 12.4% | 22.0% | 1.3% | 14.6% | -8.8% | 61% |

| 2013 | 4.9% | 3.0% | 1.7% | 10.0% | 19.4% | 1.3% | 16.7% | -4.1% | 72% |

| 2014 | 4.9% | 3.0% | 1.9% | 9.3% | 19.1% | 1.3% | 17.5% | -2.9% | 74% |

| 2015 | 4.9% | 2.9% | 2.2% | 9.4% | 19.3% | 1.5% | 18.0% | -2.7% | 74% |

| 2020 | 5.2% | 3.0% | 2.6% | 7.7% | 18.5% | 2.8% | 17.7% | -3.6% | 74% |

| 2024 | 5.6% | 3.2% | 2.7% | 7.2% | 18.7% | 3.3% | 18.1% | -3.9% | 79% |

| 2025 | 5.7% | 3.5% | 2.8% | 7.2% | 19.2% | 3.3% | 18.2% | -4.3% | 80% |

| 2030 | 6.0% | 3.9% | 2.9% | 6.9% | 19.8% | 3.7% | 18.5% | -5.0% | 89% |

| 2035 | 6.2% | 4.2% | 3.1% | 6.5% | 20.0% | 4.0% | 19.0% | -5.1% | 96% |

| 2040 | 6.1% | 4.4% | 3.3% | 6.0% | 19.9% | 4.2% | 19.3% | -4.8% | 101% |

| Source: Historical data from the Office of Management and Budget; projections from CBPP based on Congressional Budget Office, Joint Committee on Taxation, and Social Security and Medicare Trustees data. | |||||||||

Our new projections are mildly more pessimistic than those we published in June 2013, when we projected that the debt would reach 99 percent of GDP in 2040. Based on recent congressional practice, we now assume that the BCA caps, sequestration, and Medicare’s SGR mechanism will all remain in place or that the cost of their repeal will be offset. Taken by themselves, these changes in policy assumptions reduce the debt-to-GDP ratio in 2040 by about 11 percentage points. The Commerce Department has also completed a comprehensive revision of the national income and product accounts, which has increased estimated GDP and reduced the ratio of debt to GDP.

Countering those changes, however, is a modest deterioration in CBO’s ten-year economic and budget outlook. Furthermore, last June, there were no CBO long-run projections of revenues that incorporated the American Taxpayer Relief Act (ATRA), enacted in January 2013. We had made our best estimate based on the available sources; however, we slightly overstated revenue growth after the first ten years.

The result of these various revisions is that the 2040 debt-to-GDP ratio is now 2 percentage points higher than we projected last June.

End Notes

[1] Chad Stone, “From a Deficit to a Surplus and Back Again,” U.S. News, April 25, 2013, http://www.usnews.com/opinion/blogs/economic-intelligence/2013/04/25/debt-economic-growth-relationship.

[2] Richard Kogan, Kathy A. Ruffing, and Paul N. Van de Water, Long-Term Budget Outlook Remains Challenging, But Recent Legislation Has Made It More Manageable, Center on Budget and Policy Priorities, June 27, 2013, https://www.cbpp.org/cms/index.cfm?fa=view&id=3983.

[3] In July 2013, the Commerce Department revised the National Income and Product Accounts — including levels of GDP — to improve the definitions, classifications, and methodologies used in the accounts as well as to use new and revised data. The revisions boosted past (and projected) levels of GDP and thus lowered historical levels of revenues, outlays, and debt when expressed as a percentage of GDP. See Kim Kowalewski and Amber Marcellino, Updated Historical Budget Data Following BEA's Recent Update of the National Income and Product Accounts, Congressional Budget Office, August 12, 2013, http://cboblog.cbo.gov/publication/44508.

[4] Paul Krugman, “Interest Rates and the Budget Outlook,” The New York Times, April 14, 2014, http://krugman.blogs.nytimes.com/2014/04/14/interest-rates-and-the-budget-outlook/.

[5] See “Why Does Raising the Retirement Age Reduce Benefits?” in Kathy A. Ruffing and Paul N. Van de Water, Social Security Benefits Are Modest, Center on Budget and Policy Priorities, January 11, 2011, https://www.cbpp.org/cms/?fa=view&id=3368.

[6] Paul N. Van de Water, “Slowing of Health Care Spending Is Good News for the Budget,” Off the Charts Blog, January 8, 2014, http://www.offthechartsblog.org/slowing-of-health-care-spending-is-good-news-for-the-budget/.

[7] Robert Greenstein, President, Center on Budget and Policy Priorities, “Testimony before the Senate Committee on Finance,” February 26, 2013, p. 6, https://www.cbpp.org/cms/?fa=view&id=3908.

[8] Of course, a richer country might choose to spend increasing amounts per capita on infrastructure, research, education, and other programs in this category. But such a choice — which could keep this category from falling as a percent of GDP — is not consistent with the historical pattern, and (in the case of benefit programs) would require enacting increases in benefit amounts or expansions in eligibility, whereas we project spending based on current law. See Kogan, Ruffing, and Van de Water, Long-Term Budget Outlook, Appendix 2. Auerbach and Gale — who do assume in their budget projections that such spending keeps pace with GDP — clearly state that this is a policy shift, reflecting a choice by a “wealthier and more populous society” to maintain spending as a share of GDP. Alan J. Auerbach and William G. Gale, Forgotten but Not Gone: The Long-Term Fiscal Imbalance, Brookings Institution, March, 2014, p. 12, http://www.brookings.edu/~/media/Research/Files/Papers/2014/03/long%20term%20fiscal%20imbalance%20gale/longterm_fiscal_imbalance_gale.pdf.

[9] The separate Disability Insurance trust fund is expected to be exhausted in 2016, the much larger Old-Age and Survivors Insurance fund in 2035. Combined, the two funds could pay full benefits until 2033.

[10] Social Security and Medicare Boards of Trustees, Status of the Social Security and Medicare Programs, A Summary of the 2013 Annual Reports, May 31, 2013.

[11] Congressional Budget Office, The 2013 Long-Run Budget Outlook, September 2013, p. 95.

[12] Congressional Budget Office, Updated Budget Projections: 2014 to 2024, April 2014.

[13] Richard Kogan and William Chen, Projected Ten-Year Deficits Have Shrunk by Nearly $5 Trillion Since 2010, Center on Budget and Policy Priorities, March 19, 2014, https://www.cbpp.org/cms/index.cfm?fa=view&id=4106. If the normal tax extenders were allowed to expire, or if their extension were paid for, the projected debt-to-GDP ratio in 2040 would be 6 percentage points lower, or 95 percent.

[14] Committee for a Responsible Federal Budget, Actually, the SGR Has Slowed Health Care Cost Growth, March 13, 2014, http://crfb.org/blogs/actually-sgr-has-slowed-health-care-cost-growth.

[15] Several mandatory programs (SSI, veterans’ benefits, and military retirement) and a portion of Medicare may, because of calendar quirks, make 11, 12, or 13 “monthly” payments in a fiscal year. 2024 happens to be an 11-payment year, so outlays are unusually low in that year. To extrapolate spending in 2025 and beyond, we start with what 2024 outlays would have been had that been a normal 12-payment year.

[16] For the 2018-2024 period, CBO assumes three-month Treasury bills will yield 3.7 percent and ten-year notes 5.0 percent. Inflation (as measured by the consumer price index) is 2.4 percent a year over that period, so the real ten-year interest rate is 2.5 percent. Increasing the real rate to 3.0 percent after 2024 would raise the projected 2040 debt-to-GDP ratio by 7 percentage points — to 108 percent. A lower real interest rate would produce a comparable reduction in the debt ratio.

More from the Authors

Areas of Expertise

Areas of Expertise