Projected Ten-Year Deficits Have Shrunk by Nearly $5 Trillion Since 2010, Mostly Due to Legislative Changes

Recent Spending Cuts Outweigh Tax Increases 3 to 1

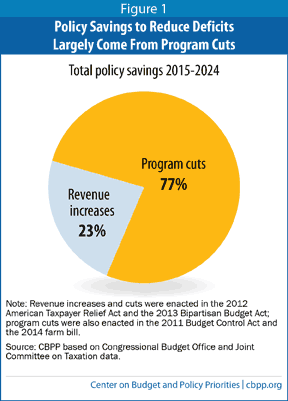

Since 2010, projected ten-year deficits over the 2015-2024 decade have shrunk by almost $5.0 trillion, $4.1 trillion of which is due to four pieces of legislation enacted in the intervening years. Some 77 percent of the savings from those pieces of legislation — which include the Budget Control Act of 2011 and the American Taxpayer Relief Act of 2012 — come from program cuts, 23 percent from revenue increases. Projected deficits have also fallen because of a dramatic slowdown in health spending.

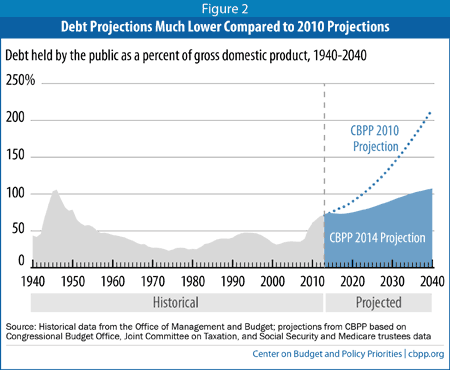

The reduction in ten-year deficits improves the long-term budget picture as well, relative to the outlook of several years ago. In 2010 we projected that, under current budget policies, the debt held by the public would reach 218 percent of gross domestic product (GDP) by 2040. Our new estimate, derived from the Congressional Budget Office’s (CBO) new ten-year baseline, shows debt at slightly less than 110 percent of GDP in 2040.

Although far more favorable than those of 2010, our current projections still show that significantly more deficit reduction will ultimately be needed to put the debt on a stable path as a share of the economy over the medium and long term. But, because the economy has not yet fully recovered from the Great Recession, the desirability of additional long-term deficit reduction should not displace the need for up-front job and income creation. The appropriate mix is one of short-term measures to bolster the still-sluggish recovery and increases in investments that can boost long-term growth (e.g., infrastructure, education, early childhood programs, and basic research), along with revenue and spending measures that reduce mid- and long-term deficits and take effect as the economy strengthens.

Improvement Reflects Deficit-Cutting Legislation and Slower Health Spending

Table 1 summarizes the $5.0 trillion improvement in ten-year deficits over the current budget window, 2015 through 2024.[1]

| Table 1 Deficit Savings Over 2015-2024 Relative to 2010 Projections, dollars in billions |

|||

| Major policy changes enacted by Congress (see Table 2): | Policy changes | Resulting interest | Total savings |

| Revenue increases (ATRA and BBA) | 778 | 175 | 953 |

| Program cuts (BCA, ATRA, BBA, and the farm bill) | 2,546 | 646 | 3,192 |

| Total, major policy changes | 3,324 | 821 | 4,145 |

| All other changes in projected deficitsa | 839 | ||

| Grand total, reductions in projected deficits | 4,984 | ||

| May not add due to rounding Source: CBO cost estimates of legislation and CBO baselines of August 2010 and February 2014, as adjusted by CBPP. See Appendix for details. Note: ATRA = American Taxpayer Relief Act of 2012; BBA = Bipartisan Budget Act of 2013; BCA = Budget Control Act of 2011; farm bill = Agricultural Act of 2014. aThis figure primarily reflects CBO’s economic and technical reestimates, though it also includes many small pieces of legislation that had little or no net effect on projected deficits. |

|||

As Table 1 shows, Congress and the President have enacted measures that will reduce deficits by $4.1 trillion over the 2015-2024 period, including the debt service (interest) savings that program reductions and revenue increases generate automatically (because there is less debt on which interest must be paid). The remaining deficit reduction reflects the net effect of CBO’s revised estimates of spending and revenue (excluding the effects of legislative changes) since its August 2010 baseline projections. The improvement outside the major deficit reduction legislation essentially reflects much lower costs for health care, as discussed below.

Enacted Deficit Reduction Shrinks Deficits by $4.1 Trillion

The four major pieces of deficit-reduction legislation enacted since the fall of 2010 are:

- The Budget Control Act of 2011 (BCA), which is by far the most significant of the four; its caps on discretionary funding and automatic sequestration constitute three-fourths of the total enacted deficit reduction. Our figures for the budget cuts implemented by the BCA caps and sequestration include the effects of cuts in discretionary funding that policymakers enacted in April 2011; the BCA, enacted that August, both locked in those earlier savings by establishing caps and made the cuts deeper.

- The American Taxpayer Relief Act of 2012, also known as the “fiscal cliff” agreement.

- The Bipartisan Budget Act of 2013, the deal between Senate Budget Committee Chair Patty Murray and House Budget Committee Chair Paul Ryan.

- The Agricultural Act of 2014, commonly known as the farm bill.

Table 2 provides the dollar amounts associated with this legislation. Tables 1 and 2 reveal two important points.

More than three-fourths — 77 percent — of the policy changes in these four pieces of legislation represent program cuts rather than revenue increases (see Figure 1). Put differently, for every $1.00 of revenue increases, Congress has enacted $3.27 in program cuts. The unbalanced nature of the deficit reduction to date strongly suggests that further deficit reduction should place greater emphasis on revenue increases (particularly in “tax expenditures”).

| Table 2 Major Legislation Has Reduced Projected Deficits by $4.1 Trillion Cumulative effects over 2015-2024 of legislation enacted since 2010; dollars in billions |

|||

| Major deficit-reduction measures enacted by Congress: |

Policy changes | Resulting interest | Total savings |

| 2011 funding cuts and BCA capsa | 1,466 | 394 | 1,859 |

| BCA sequestrationb | 978 | 276 | 1,253 |

| (discretionary sequestration from 2016 on, included above) | (731) | (142) | (874) |

| ATRA, BBA, and farm bill | 880 | 151 | 1,032 |

| Total, reduction in projected deficits | 3,324 | 821 | 4,145 |

| May not add due to rounding Note: ATRA = American Taxpayer Relief Act of 2012; BBA = Bipartisan Budget Act of 2013; BCA = Budget Control Act of 2011; farm bill = Agricultural Act of 2014. aThe BCA both capped funding for discretionary programs and established an automatic sequestration to further cut funding if the 2011 “supercommittee” failed to achieve its targeted savings. Cuts in funding for discretionary programs started in the spring of 2011, even before the BCA was enacted. bThese figures include discretionary and mandatory sequestration from 2013 on. |

|||

Slowdown in Health Care Costs Contributes Significantly to Improved Outlook

The recent slowdown in health care cost growth has contributed significantly to shrinking deficit projections. Projected spending over 2015-2024 for mandatory health programs — primarily Medicare, Medicaid, and the subsidies to purchase health insurance through the exchanges established by the Affordable Care Act — has fallen by more than $1.3 trillion since 2010. The Centers for Medicare & Medicaid Services recently reported a fourth consecutive year of low health spending growth in 2012.[2] Even better for the fiscal picture, CBO has concluded that the slowdown is at least partially a long-term one.[3]

Major CBO Reestimates Between August 2010 and February 2014

CBO’s downward reestimates of deficits — exclusive of the effects of budget cuts and revenue increases enacted by Congress — total $839 billion in lower debt over the 2015-2024 decade.

Our calculations show that slower growth of mandatory health programs — primarily Medicare, Medicaid, and the subsidies to purchase health insurance through the exchanges established by the Affordable Care Act — amounts to more than $1.3 trillion in lower projected health care expenditures over this period. Of this amount, about 58 percent comes from lower Medicare costs and 42 percent from lower Medicaid and other costs, indicating that the slowdown in health care costs has been widespread. Indeed, the growth of private-sector health care costs is also moderating.

Outside of health care, reestimates of other program spending, revenues, and interest costs raised projected deficits by about $500 billion, so the net reduction in debt ($1.3 trillion minus roughly $500 billion) is $839 billion.

The issue here is essentially macroeconomic; CBO now expects lower economic growth over this period than it did in 2010. Lower growth has two largely offsetting effects: it produces significantly smaller revenues but also lowers interest rates, which generates significant debt-service savings.

Specifically, our analysis shows a significant reduction in estimated revenues, costing the Treasury $3.3 trillion over the 2015-2024 decade — a decline averaging almost 8 percent annually. But this reduction is essentially offset by the large decline in interest costs due largely to lower Treasury interest rates. In fact, lower interest rates by themselves generate an estimated $3.5 trillion in interest savings over the 2015-2024 decade, reducing projected interest costs by an average of 37 percent over this period. These savings are independent of other changes in interest costs associated with legislation, lower revenues, or lower costs for health care and other programs.

Because the bad news on revenues and the good news on interest costs are almost surely linked to the lackluster economic recovery from the Great Recession, one can reasonably expect that if the recovery is prolonged or becomes more robust, revenues will recover at least in part while interest rates will rise. If so, the eventual good news on revenues will be largely but not entirely offset by bad news on interest.

| Table 3 Ten-Year Deficit Estimates Are Lower Even Aside From Major Legislation Cumulative reduction (-) or increase (+) in projected deficits, 2015-2024, in trillions of dollars, excluding savings from major legislation (shown in Table 2) |

|||

| Program / revenue reestimates | Resulting interest savings | Total changes in estimates | |

| Downward reestimates of mandatory health costs | -1.3 | -0.3 | -1.6 |

| Net upward reestimates of other programs | 0.2 | * | 0.2 |

| Downward reestimates of revenues | 3.3 | 0.8 | 4.1 |

| Lower interest rates and costs, independent of above | -3.5 | ||

| TOTAL, lower deficits | -0.8 | ||

| May not add due to rounding *less than $50 billion |

|||

To be sure, health care costs are still rising, and the share of the population relying on Medicare and Medicaid will continue to grow as the baby boom generation ages. Costs will also rise when baby boomers move from “young old age” to “old old age.” Still, current costs and projected cost growth are not as severe as they looked several years ago.

Table 1 shows that changes in CBO’s estimates due to revisions in its economic and technical assumptions (not due to enacted legislation) reduced deficits over the 2015-2024 decade by $839 billion. Lower spending on health care programs more than explains the net deficit reduction due to reestimates shown in Table 1. (The rest of the budget includes a mix of upward and downward reestimates; see box.)

Reduction in Ten-Year Deficits Improves Long-Term Budget Picture

Long-term budget projections necessarily suffer from a high degree of uncertainty. (We are mindful of the admonition often attributed to Casey Stengel, “Never make predictions, especially about the future.”) But they give a sense of the degree to which future deficit reduction, or unexpectedly favorable economic outcomes, will be needed to stabilize the debt ratio (i.e., to keep the debt from continually growing faster than the economy). They can also highlight the growing importance over time of factors such as the growth rate of health care costs. In this context, the considerable improvement in the projections since 2010 is encouraging, although the job is not yet done.

Appendix:

Estimating the 2010 and 2014 Baselines

CBO’s baselines follow rules specified in Section 257 of the Balanced Budget and Emergency Deficit Control Act of 1985, as amended. Those rules generally require CBO to make literal interpretations of existing budget law, often producing results greatly different from what is widely viewed as plausible or representing current policy.

In 2010, for example, CBO’s baseline of necessity assumed that all of the 2001/2003/2009 tax cuts would expire on schedule that December and that the parameters of the Alternative Minimum Tax (AMT) would revert to their 2000 levels, even though Congress had unfailingly changed them in the intervening years to keep the AMT from generating sudden, large revenue gains. CBO’s baselines also assume that whatever level of war funding is in place in the current year will continue forever, growing with inflation.

In this analysis, we adjust the 2010 and 2014 CBO baselines, both to better reflect current budget policies and to make their policy assumptions conceptually similar or identical. Our adjustments to the 2010 and 2014 CBO baselines are shown in Tables 4 and 5, respectively.

| Table 4 Adjustments to and Extrapolation of CBO’s 2010 Baseline, dollars in billions |

|||||||||||

| ‘15 | ‘16 | ‘17 | ‘18 | ‘19 | ‘20 | ‘21 | ‘22 | ‘23 | ‘24 | Total | |

| CBO baseline deficits (+)(a) | 507 | 585 | 579 | 562 | 634 | 685 | 743 | 854 | 873 | 888 | 6,909 |

| Adjustments (+ means higher deficit): | |||||||||||

| phase down war costs | -104 | -124 | -135 | -141 | -146 | -150 | -154 | -159 | -163 | -168 | -1,444 |

| continue 2001/2003/2009 tax cuts and AMT relief(b) |

380 | 403 | 428 | 452 | 479 | 508 | 537 | 568 | 600 | 634 | 4,989 |

| continue “normal” tax extenders(c) |

10 | 21 | 30 | 39 | 47 | 53 | 60 | 68 | 77 | 87 | 491 |

| debt service changes resulting from the above adjustments (d) |

69 | 93 | 120 | 147 | 176 | 209 | 246 | 289 | 340 | 397 | 2,085 |

| Adjusted baseline deficits (+) | 862 | 978 | 1,021 | 1,059 | 1,190 | 1,305 | 1,431 | 1,621 | 1,727 | 1,838 | 13,031 |

| May not add due to rounding. (a)Figures shown are CBO estimates for 2015-2020 and CBPP extrapolations for 2021-2024. (b)Continuing these policies not only reduces revenues but also increases expenditures for refundable tax credits. (c)However, we assume that bonus depreciation expires on December 31, 2013, for consistency with our assumptions shown in Table 5. (d)The debt service costs shown on this row also reflect debt service on the higher debt occurring in 2011 through 2014 (not shown) as a result of the adjustments. |

|||||||||||

In addition, we have projected the 2010 adjusted baseline through 2024; CBO’s 2010 baseline figures ended with 2020. We did this by assuming that the level of revenues in the adjusted 2010 baseline would continue to grow in 2021-2024 as they had been growing in 2020. We made the same assumption for the level of program (non-interest) expenditures.[6] Finally, we calculated the growth of net interest costs over 2021-2024 based on the revenue and programmatic levels we had extrapolated and on interest rates consistent with those that CBO used in its 2010 baseline.

| Table 5 Adjustments to CBO’s February 2014 Baseline, Dollars in Billions |

|||||||||||

| ‘15 | ‘16 | ‘17 | ‘18 | ‘19 | ‘20 | ‘21 | ‘22 | ‘23 | ‘24 | Total | |

| CBO baseline deficits (+) | 478 | 539 | 581 | 655 | 752 | 836 | 912 | 1,031 | 1,047 | 1,074 | 7,904 |

| Adjustments (+ means higher deficit): | |||||||||||

| phase down war costs | -10 | -36 | -49 | -59 | -64 | -68 | -70 | -72 | -72 | -72 | -572 |

| continue “normal” tax extenders and other expiring tax provisions, except bonus depreciation |

39 | 39 | 41 | 47 | 74 | 76 | 78 | 81 | 86 | 89 | 650 |

| increase discretionary funding with population and inflation after Budget Control Act caps expire in 2021 |

6 | 15 | 25 | 45 | |||||||

| debt service changes resulting from the above adjustments(a) |

0 | 1 | 1 | 1 | 1 | 2 | 2 | 3 | 4 | 6 | 21 |

| Adjusted baseline deficits (+) | 508 | 544 | 573 | 643 | 763 | 845 | 922 | 1,050 | 1,079 | 1,120 | 8,047 |

| May not add due to rounding. (a)The debt service costs shown on this row also reflect debt service on the higher debt occurring in 2014 (not shown) as a result of the revenue adjustments. |

|||||||||||

The key sources of the nearly $5.0 trillion difference between the ten-year, 2015-2024 cumulative deficit of $13.0 trillion shown in Table 4 and the $8.0 trillion figure shown in Table 5 are summarized in Tables 1 and 2 in the body of this analysis.

End Notes

[1] The year-by-year figures associated with the five tables in this analysis are available in spreadsheet form at https://www.cbpp.org/sites/default/files/atoms/files/3-19-14bud-appendix.xls.

[2] See Paul Van de Water, “Slowing of Health Care Spending Is Good News for the Budget,” Off the Charts blog, January 8, 2014, http://www.offthechartsblog.org/slowing-of-health-care-spending-is-good-news-for-the-budget/.

[3] CBO’s 2013 projections of Medicare and Medicaid spending for the period 2010-2020 were $1.2 trillion lower than the projections it made for that period in March 2010, for reasons unrelated to enacted legislation or revised economic forecasts. See Doug Elmendorf, “The Slowdown in Health Spending,” CBO Blog, http://www.cbo.gov/publication/44596.

[4] Kathy Ruffing, Kris Cox, and James Horney, “The Right Target: Stabilize the Debt,” Center on Budget and Policy Priorities, January 12, 2010, https://www.cbpp.org/cms/index.cfm?fa=view&id=3049.

[5] This long-term projection supersedes the ones we released in June 2013, which relied on earlier CBO estimates. (A description of our updated long-term projections is forthcoming.)

[6] Four major entitlement programs — military retirement, veterans’ compensation and pensions, Supplemental Security Income (SSI), and Medicare capitation payments to insurance plans under parts B and D of the Medicare act — make benefit payments on the first day of each month. However, if that day falls on a weekend, the payments occur on the prior Friday. Occasionally this means that there will be either 11 or 13 such monthly payments during a fiscal year; in fact, there are scheduled to be 13 in 2022 and 11 in 2024, and this phenomenon is built into CBO’s current (2014) baseline. To achieve comparability with CBO’s 2014 baseline, therefore, after extrapolating program spending into 2021-2024 using the 2020 growth rate in CBO’s 2010 baseline, we adjust the extrapolated results to reflect 13 such payments in 2022 and 11 such payments in 2024.

More from the Authors