Lessons From New Hampshire: Senate Health Bill Could Drive Up Health Insurance Premiums for Many Small Businesses

In early May, Senate Majority Leader Bill Frist is expected to bring to the Senate floor the “Health Insurance Marketplace Modernization and Affordability Act of 2005” (S. 1955), introduced by Senator Enzi (R-WY) and reported out of the Senate Health, Education, Labor and Pensions Committee on March 15. While the intent of S. 1955 is to make health insurance more affordable for small businesses, the bill could end up substantially increasing the health insurance premiums now paid by many small businesses, particularly small firms that employ workers who are older and in less good health than average workers.

S. 1955 would preempt state insurance laws that limit how much insurers may vary the premiums they charge small firms due to factors like the health status and age of a firm’s employees. Some states now require “community rating,” under which health insurers must charge nearly the same premium to all small businesses. Most other states permit insurers to charge different premiums but set tight restrictions on how much premiums can differ among individual businesses and classes of businesses based on such factors as differences in the age and health status of a firm’s workers. S. 1955 would establish a new federal rating standard that would preempt these state laws, with the federal standard being much weaker than the limits currently in place in the vast majority of states. S. 1955 thus would allow insurers to charge many small firms that already offer health insurance much higher premiums than the firms currently pay.[1] As a result, some small businesses could face unaffordable premium increases and have little choice but to drop the health insurance coverage they now provide to their workers.

The risk that S. 1955 poses to the small group markets of the states is not merely theoretical. The experience of the state of New Hampshire essentially serves as a real-life experiment that indicates what may occur if S. 1955 is enacted. In 2003, New Hampshire repealed its adjusted community rating law for its small business health insurance market[2] — the state defines a small group as a business with 50 or fewer workers, including firms with only one worker — and replaced it with a law permitting substantial variation in health insurance premiums. The standard that the New Hampshire law set was similar to the federal standard that S. 1955 would put in place. Under the law that New Hampshire enacted in 2003, health insurers in the state were permitted (beginning in 2004) to vary small business health insurance premiums substantially, based on the health and age of workers, firm size, geographic location, the firm’s industry, and other factors.[3] Some firms in New Hampshire with disproportionately younger or healthier workers saw their premiums decrease or remain flat. Many other small firms, however, particularly the smallest firms with less healthy workers and those that were located in high cost areas of the state, had their premiums skyrocket when they renewed their health insurance plans. Due to the large premium increases faced by these small businesses, New Hampshire repealed the 2003 law last year and essentially returned to its prior community rating system.

To assess the effects of the 2003 law on its small business health insurance market, the New Hampshire Department of Insurance collected information on the health insurance premiums that small businesses covered by the three dominant insurers in the state were charged for 2004, the first year that the law was effective.[4] Analysis of this premium data shows the following:

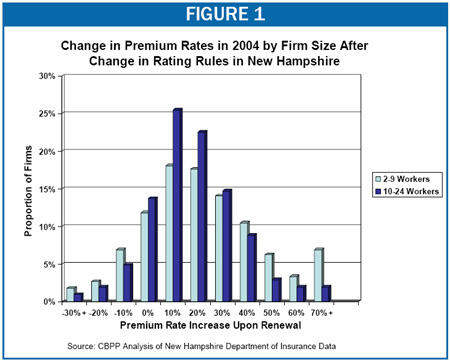

1. Many of the smaller firms faced significantly higher premiums when the 2003 change in New Hampshire’s rating rules became effective, while some firms saw their premiums reduced or remain unchanged (see Figure 1).

- Among firms with 2 to 9 employees, 41 percent had their premiums rise by 30 percent or more in 2004. Nearly 17 percent saw their premiums increase by 50 percent or more, and seven percent faced premium increases of 70 percent or more.[5] At the same time, 23 percent of such businesses were charged lower premiums or the same premiums as in 2003.

- Numerous small businesses with 10 to 24 workers also experienced large premium increases in 2004. More than 30 percent had increases of 30 percent or more. Nearly 7 percent faced premiums that were 50 percent higher or more, and nearly 2 percent had increases of 70 percent or more, as compared to the rates charged in 2003. Twenty-two percent had their health insurance rates reduced or were charged the same rates they were charged in 2003.

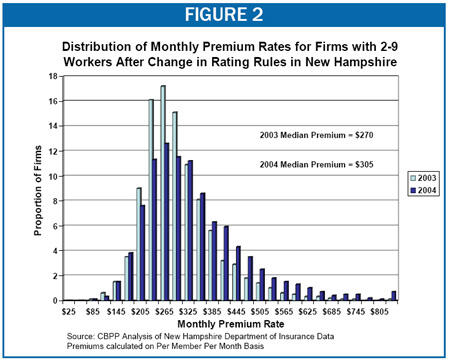

2. The variation in the health insurance premiums charged to the smallest businesses increased, with a larger proportion having premiums well above the median rate for all small businesses.

-

Prior to the change in rating rules, the large majority of small employers faced premiums — calculated on a per-member-per-month basis — at or near the median rate of $270. In 2004, while a majority of small businesses still were charged at or near the new median of $305, a larger proportion of firms faced premiums well in excess of the median. Among firms with 2 to 9 workers, 87 percent had premiums set within an estimated 25 percent of the median in 2003. That figure fell to 74 percent in 2004 (see Figure 2).

-

The range between the lowest and highest health insurance premium rates increased significantly for employers with 2 to 9 workers in 2004. The difference between the lowest and highest monthly premium charged to firms with 2 to 9 workers rose by nearly 55 percent from $1,052 in 2003 to $1,626 in 2004.

-

The highest monthly premium for a small business with 2 to 9 workers increased by 51 percent from $1,113 in 2003 to $1,677 in 2004. At the same time, the lowest monthly premium charged a firm of that size fell from $61 to $51.

New Hampshire Governor Opposes S. 1955

On March 28, 2006, New Hampshire Governor John Lynch (D) wrote a letter to Senator Judd Gregg (R-NH) expressing his opposition to S. 1955. Excerpts include:

“I am writing to oppose the provisions in Title II of S. 1955 that would preempt state rating rules for the small group health insurance market and that could force our businesses and citizens to return to the unfair and expensive small business health insurance rating system that New Hampshire just rejected....”

“In 2003, New Hampshire passed a law establishing rating rules similar to those contemplated under S. 1955. With the rules allowing insurance companies to discriminate against businesses with sick workers or based on geography, this law sent small business health insurance costs skyrocketing across New Hampshire. Small businesses could not grow, could not hire new workers, and some considered ending their health insurance plans altogether....”

“After much debate and careful consideration, the New Hampshire legislature passed [legislation] in 2005 prohibiting price discrimination against small businesses based on their employees’ health status or geography and limiting rating discretion.... The goal was to ensure that coverage would be affordable for the people who need it most.”

* Letter from Governor John H. Lynch to the Honorable Judd Gregg, March 28, 2006

Lessons from the New Hampshire Experience

A straightforward conclusion can be drawn from New Hampshire’s experience in moving its small group health insurance market to a less restrictive premium rating system similar to the federal standard that S. 1955 would establish. The conclusion is that a federal mandate that overrides the limits that many states have established on permitted variations in health insurance premium rates will lead to much greater divergence in the premiums that small businesses are charged and result in significant losers, as well as winners, among small firms.

Some small businesses (and their workers) will end up paying less for their health insurance than they do now. For example, firms with younger and healthier workers, that are of relatively larger size, and are not located in high cost geographic areas of a state are likely to see their premiums decrease, remain flat, or grow more slowly than expected. Some businesses not currently offering health insurance may now be able to afford it if they have a very healthy workforce.

But many of the smallest employers whose workers are disproportionately older or sicker are likely to face sharply higher health insurance premiums. That could make health coverage increasingly unaffordable for a number of these firms. Moreover, for businesses with older and sicker employees that currently are unable to offer health insurance, S. 1955 would place health care coverage still further out of reach.[6]

The intent of S. 1955 is to make health insurance more affordable for all small businesses. Analysis of health insurance data from New Hampshire indicates, however, that S. 1955 is likely to make health insurance less affordable for many small firms, and in particular for firms containing the very employees who need health coverage the most — older and less healthy workers. This is one of the key reasons why the Governor of New Hampshire opposes S. 1955 and why numerous state insurance commissioners have raised serious concerns about the small group premium rating rules required under S. 1955.[7]

End Notes

[1] Mary Beth Senkewicz, “Senate Health Bill Would Preempt States’ Small Group Rating Rules,” Center on Budget and Policy Priorities, April 26, 2006. See also Mila Kofman and Karen Pollitz, “Health Insurance Regulation by States and the Federal Government: A Review of Current Approaches and Proposals for Change,” Georgetown Health Policy Institute, April 2006.

[2] Under the New Hampshire “adjusted community rating system,” insurers were prohibited from varying small business premiums based on workers’ health status, but insurers were allowed to only vary premiums to a limited extent based on the age of employees and firm size.

[3] See New Hampshire Department of Insurance, "The Small Group Health Insurance Market," February 16, 2005.

[4] New Hampshire Department of Insurance, “Special Data Request to Carriers,” February 2005. These data played a significant role in persuading state policymakers to repeal the 2003 law and reinstate adjusted community rating. Because most states do not consider an individual as a “small group” as New Hampshire does, this paper does not analyze the premium data related to employers with only one worker.

[5] The New Hampshire Department of Insurance does not have comparable data for 2003 but it is clear that it was the change in rating rules, rather than health inflation, that primarily drove these large premium increases in 2004. See, for example, Letter from David Sky, Life, Accident and Health Actuary, New Hampshire Department of Insurance, to a Small Business, October 15, 2004 (finding that in the absence of the change in rating rules, a particular small business’ health insurance premiums would have risen only 13 percent in 2004 rather than 48 percent).

[6] The state of Minnesota had an experience similar to New Hampshire when it phased out community rating and instituted less restrictive small group rating rules over a number of years starting in 2001. See Deborah Chollet, “State Regulation and Initiatives to Expand Small Group Coverage,” Written Testimony before the Senate Finance Committee, April 6, 2006.

[7] See Letter from Kevin M. McCarty, Florida Insurance Commissioner, to the Honorable Michael Enzi, March 7, 2006; Letter from Mike Kreidler, State Insurance Commissioner of Washington to the Honorable Patty Murray, March 6, 2006; Letter from John Garamendi, California Insurance Commissioner to the Honorable Michael Enzi, March 7, 2006; Letter from Howard Mills, Superintendent of Insurance, State of New York, to the Honorable John M. McHugh, March 17, 2006; Letter from John P. Crowley, Vermont Insurance Commissioner to the Honorable James Jeffords, March 27, 2006; Letter from Jorge Gomez, Commissioner of Insurance, State of Wisconsin, to the Honorable Michael Enzi, March 14, 2006; Letter from Christopher Keller, Health Insurance Commissioner, State of Rhode Island, to the Honorable Michael Enzi and the Honorable Edward Kennedy, March 13, 2006; Letter from Susan Voss, Commissioner of Insurance, State of Iowa, to the Honorable Charles Grassley and the Honorable Tom Harkin, March 15, 2006; Letter from James Donelon, Louisiana Insurance Commissioner to the Honorable Michael Enzi, April 18, 2006 and Letter from Matthew Denn, Delaware Insurance Commissioner, to the Honorable Joseph Biden and the Honorable Thomas Carper, April 21, 2006. See also Letter from the National Association of Insurance Commissioners to the Honorable Michael Enzi and the Honorable Ben Nelson, March 7, 2006.

Más de los autores