The State of the ACA Marketplaces: Making Sense of Individual Market Rate Filings

More than 20 million Americans have gained coverage due to the Affordable Care Act (ACA), bringing the uninsured rate to its lowest level in history.[1] Those gains are due in part to the ACA’s individual market reforms, which prevent discrimination against people with pre-existing health conditions, provide millions of Americans with tax credits that help pay for coverage, and allow all Americans to shop and compare plans in a transparent marketplace.

Health insurers across the country are now in the process of submitting proposed individual market plan offerings and premiums for 2018 to state and federal regulators. These rate filings will contribute to the ongoing debate about health insurance affordability and the state of the ACA marketplaces. Here are a few key points to keep in mind.

The Marketplaces Were Poised for Greater Stability and Success

It’s increasingly clear that the Trump Administration inherited a marketplace poised for greater price stability and growing insurer competition going forward. For example, the Kaiser Family Foundation found that individual market insurers substantially narrowed the gap between premiums and costs in 2016, meaning premium increases already in place for 2017 should put them on track to break even or earn a profit this year. Standard & Poor’s (S&P) found that Blue Cross Blue Shield plans, critical marketplace participants in many states, made even more progress toward profitability in 2016.

For consumers, these improvements should translate into lower premium increases and more insurer competition. Consistent with that, Centene, one of the largest marketplace insurers, recently announced that it will be entering markets in three additional states and expanding its participation in another six states for 2018. And S&P concluded its analysis by noting, “if it remains business as usual, we expect 2018 premiums to increase at a far lower clip than in 2017.”

Proposed Rate Filings Instead Reflect Trump Administration Sabotage

But instead of “business as usual,” the Trump Administration acted to sabotage marketplace progress, by:

- Threatening to withhold billions of dollars owed to insurers. Under the ACA, insurers are required to offer plans with lower deductibles and copays (“cost-sharing reductions” or CSRs) to lower-income consumers; the government then reimburses them for the roughly $10 billion annual cost. The Trump Administration has repeatedly threatened to withhold these CSR payments. To make up for the lost payments, insurers would have to raise premiums for affected plans by 19 percent or more — or they might decide not to offer coverage at all.

- Creating uncertainty about whether it will enforce the ACA’s individual mandate. The individual mandate encourages healthy consumers to buy health insurance by requiring them to pay a penalty if they don’t. But the Administration has intimated that it may stop enforcing the mandate. If insurers believe the mandate won’t be enforced, they will raise premiums by up to 20 percent to cover the resulting increase in per-enrollee costs.

- Discontinuing outreach during one of the most critical weeks of open enrollment. In its first week in office, the Administration abruptly halted outreach and marketing activities for the final week of the 2017 open enrollment period. That decision likely led to tens or hundreds of thousands fewer sign-ups for 2017, especially among younger, healthier consumers, which will mean higher per-enrollee costs and premiums going forward.

- Finalizing rules that will cut tax credits and make it harder for people to sign up for coverage. Under new rules finalized in April, millions of consumers will likely receive less help paying for coverage, and the open enrollment period for 2018 will be shorter. These changes are likely to mean fewer sign-ups, also contributing to higher per-enrollee costs and premiums going forward.

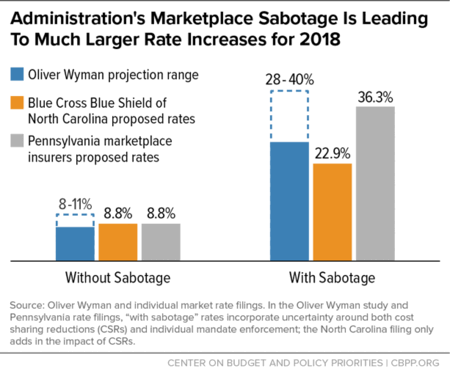

In a recent analysis, actuaries at Oliver Wyman concluded that uncertainty about CSRs and the individual mandate will add 20 to 29 percent to rate increases for 2018 and that 2018 rate increases would be about two-thirds lower without these factors. In states where insurers have submitted two sets of proposed rate increases for 2018 — with and without Trump Administration sabotage — these rates are in line with the Oliver Wyman projections (see graph).

Final Marketplace Options Will Depend on What Policymakers Do Next

Even more troubling, Trump Administration sabotage may lead some insurers to exit the ACA marketplaces altogether. Already, Anthem has withdrawn from Ohio’s marketplace, citing uncertainty around CSRs as a key factor in its decision.

In the ACA marketplaces’ first four years, every consumer nationwide had options for marketplace coverage. To ensure that the same is true this year, policymakers must, at a minimum:

- Give insurers certainty that they will receive the cost-sharing reduction payments they’re owed, as governors and insurance commissioners of both parties, insurers, providers, and the Chamber of Commerce have urged.

- Commit to administering the law of the land. That means enforcing the ACA’s individual mandate and undertaking the outreach needed to make sure consumers know about the coverage options available to them.

- Work with insurers and state insurance commissioners — as the previous Administration did — to facilitate insurer entry into new markets and make sure consumers everywhere in the country have options.

Provided There Are Marketplace Options, Most Consumers Will Be Protected

Fortunately, the ACA is designed to shield most consumers from the rate increases that could result from the Trump Administration’s actions, as well as from normal increases due to health care cost growth. Consumers will be protected as long as the Administration’s sabotage does not leave people in some parts of the country without marketplace options — and as long as the ACA itself stays intact.

That’s because, under the ACA, most marketplace consumers don’t pay sticker price for their health coverage. Instead, more than 80 percent qualify for tax credits that are designed to keep coverage affordable for consumers no matter what headline premiums are. Specifically, people with incomes up to 400 percent of the federal poverty level — about $100,000 for a family of four — pay no more than a set percentage of their income for benchmark health coverage. If the price of benchmark coverage increases, tax credits increase to compensate, and the amount families pay stays the same.

This year, for example, headline premiums rose significantly, as insurers adjusted their premiums to make up for earlier underpricing. Even so, average premiums for the more than 80 percent of consumers with tax credits stayed exactly the same — $106 per month — from 2016 to 2017, because tax credits shielded consumers from premium increases.

The House ACA Repeal Bill Would Dramatically Increase Marketplace Costs

Along with sabotage by the Administration, legislative efforts to repeal the ACA threaten marketplace consumers’ access to affordable coverage. The House-passed ACA repeal bill would significantly worsen disruption in the individual market next year, raising individual market premiums by 20 percent and reducing individual market enrollment by about 30 percent, according to Congressional Budget Office estimates. Over the longer run, the bill would slash tax credits that help people afford coverage and would increase deductibles, copays, and coinsurance costs, raising total out-of-pocket costs for current HealthCare.gov marketplace consumers by an average of $3,600 in 2020 and by far more for older and lower-income people and people in high-cost states. These increases would cause millions of marketplace consumers to lose coverage altogether and leave millions more burdened with unaffordable costs.

End Notes

[1] For a version of this fact sheet with links to sources, see https://www.cbpp.org/research/health/the-state-of-the-aca-marketplaces-making-sense-of-individual-market-rate-filings.