Robert Greenstein: Speech Before the Mt. Sinai Health Care Foundation, Cleveland, Ohio

Remarks as prepared for delivery

Thank you for that very kind introduction.

I’m very honored to be here, with such an esteemed audience of health care leaders, at a time of so much potential change in the field, with so much at stake for millions of people both here in Ohio and across the country.

The Starting Point: The House Bill

The House bill to “repeal and replace” the Affordable Care Act is deeply problematic — and in ways that would hurt Ohio. There’s a broad consensus among mainstream experts that the House bill to “repeal and replace” the Affordable Care Act is deeply problematic — and in ways that would hurt Ohio. The Congressional Budget Office estimates show that:

- 23 million fewer people would be covered.

- For many who still have coverage — especially people who are older, have medical conditions, or live in high health cost areas — the coverage would be much more expensive, with smaller tax credits to help pay for it.

- Protections that have kept insurance affordable for those with pre-existing conditions would be much weaker and could largely or entirely disappear in a number of states, putting coverage out of reach for many people with these conditions.

- The bill would cut Medicaid and federal subsidies to help people with modest incomes afford coverage by more than $1 trillion over ten years — and then use the money mainly to provide hundreds of billions of dollars in tax cuts overwhelmingly to those at the top, with people who make over $1 million a year getting nearly half of these tax cuts.

- Ohio would be among the harder hit states in three ways:

- First, because it expanded Medicaid under the ACA in very successful fashion, it has more to lose than a number of other states. The expansion would almost certainly end over the coming years, so coverage for Ohio’s 700,000 Medicaid expansion enrollees would be at grave risk.

- Second, all 3 million of the state’s Medicaid beneficiaries — and the state’s health care providers — would be at risk because the bill cuts federal support for Ohio’s entire Medicaid program, and the cuts would grow larger with each passing year. Ohio would have to decide how to cut its Medicaid program in response. And because Ohio already pays providers less and has a larger share of its Medicaid population in managed care than most other states, it would have less room to economize in those areas.

- Third, the 210,000 people in Ohio who have coverage through the ACA marketplace would also be at risk because the bill reduces premium subsidies, eliminates cost-sharing subsidies, and erodes consumer protections — all of that would put people who are older or sicker, and people in rural areas at the greatest risk. There would be little prospect the state could or would provide the billions of dollars of new resources it would take to fill the resulting very large gaps.

Impending Senate Action

In the Senate, Republicans are working behind closed doors on their version of the repeal bill, and the Senate may vote on it as early as the week of June 26. Just like in the House, Senate leaders are refusing to hold any public hearings even though this would clearly be one of the most consequential pieces of legislation in decades. By contrast, the ACA was enacted after dozens of congressional hearings.

So what will be in the Senate bill? Senator John Cornyn, the #2 Senate Republican leader, said, and I quote, “80% of what the House did we’re likely to do.” End quote. We’ve been closely following the Senate Republican deliberations, and they seem to be headed in precisely that direction.

Let’s take a look at some critical areas where there is broad consensus that the House bill is deeply problematic — and at how Senate Republicans will likely respond in their bill.

- Let me start with a brief look at the progress that’s been made under the ACA and what’s at risk under legislation to repeal it.

- Before the ACA, 16.3% of Ohio adults were uninsured. By 2016, that share had fallen by nearly half, to 8.9% — and that’s because of the Medicaid expansion and the ACA marketplaces.

- The Medicaid expansion has been particularly important in helping to address opioid addiction, a critical issue in Ohio. Ohio has the third highest death rates from overdoses of opioids of any state and the highest number of deaths from opioid overdoses — and those figures will likely grow worse if the Medicaid expansion is repealed.

- Both the expansion and marketplace coverage have been particularly crucial for many people with pre-existing conditions, for women seeking coverage for maternity care, and for people seeking mental health or substance use coverage.

- The House-passed bill reverses this progress. What will the Senate do? Let’s look first at the Medicaid expansion.

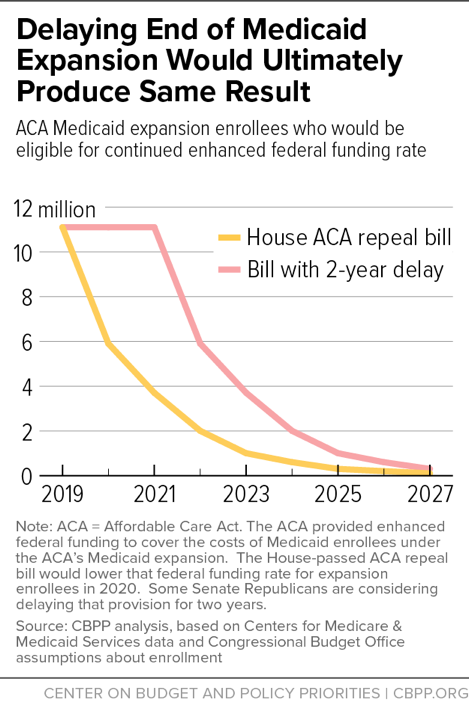

- The House bill would eliminate in 2020 the higher federal matching funds for expansion enrollees who don’t remain continuously enrolled under the expansion. By 2023, if Ohio wished to continue covering new and returning enrollees, it would have to pay more than three times as large a share of the costs of doing so as under the ACA. That would increase Ohio’s costs by more than $1.25 billion a year.

-

Figure 1 We expect that few states would agree to find the extra funding to keep covering new and returning beneficiaries, especially when they know that the federal funding for those beneficiaries will keep dropping year by year, so the state share of the costs will keep rising. Instead, most expansion states would freeze enrollment. Once someone’s prospects improved temporarily, making him or her ineligible for Medicaid, that person wouldn’t be able to get Medicaid again when his or her income fell. Because the adults covered by the expansion tend to cycle in and out of poverty, the number of people insured through the expansion would fall by about two-thirds by 2023 — and by more than 90% by 2025 — in the average state that froze enrollment.

-

I’m surprised and deeply disappointed that Republican senators from expansion states aren’t insisting that the Senate bill fix this problem. Instead, they’re asking only to phase out the higher funding over several more years for everyone who doesn’t remain continuously enrolled. Let’s be clear: the ultimate result would be exactly the same — the Medicaid expansion that covers 700,000 Ohioans would eventually die, as this graph illustrates.

-

Moreover, even the immediate effect might not be different than under the House bill. As I said, most states would likely freeze enrollment as soon as the matching rate starts to phase down, regardless of how long the phase-down takes. And in Ohio, a provision in the state budget that the state House passed this spring would end the entire Medicaid expansion as soon as the federal matching rate fell at all, so the entire expansion would end in the first year of the phase-down.

-

Let’s also be clear that no bill to repeal the ACA can pass the Senate without the support of most Republican senators from expansion states, like Ohio. As a result, they’re in the driver’s seat. And yet, they seem prepared to settle for nothing more than taking a few more years to kill the expansion.

- Some of these senators, including Senator Portman, suggest that when the Medicaid expansion ends, people who otherwise would have been eligible for Medicaid will buy private coverage with the tax credit subsidies the bill will provide. Let’s take a closer look.

- As I’m sure most of you know, for people living below the poverty line, even modest premiums are a major barrier to enrollment, and even modest cost-sharing can impede access to needed care. Yet under the bill the Senate is drafting, even with some additional funding for premium subsidies beyond what’s in the House bill — the out-of-pocket premium and cost-sharing charges for poor people who’d lose Medicaid coverage would be far too high. An overwhelming majority of them would end up uninsured.

- Let’s get specific. Under the House bill, in Ohio, a 45-year-old with income of half the poverty line — or just $6,030 — would have to spend 20% of his or her very low income just in premiums to buy individual market coverage comparable to marketplace coverage today, and that’s before counting additional charges for deductibles and co-payments. A 60-year-old with income at or below the poverty line —at or below $12,060 — would spend half or more of his or her income on premiums.

- The Senate is reportedly talking about making tax credits a bit more generous for older consumers. Senators have suggested adding something like $85 billion to the subsidies over ten years. If so, a 60-year-old Ohioan with income at or below the poverty line would still have to spend one-third of more of his or her very small income on premiums. Premiums that consume that much of the limited income of people living in poverty price them out of the market — and leave them uninsured. The research is unambiguous on this.

- Nor is the push that Senator Portman is making for some new funding to states for opioid addiction treatment a solution for the effects of ending the Medicaid expansion. People don’t just need treatment after they’re addicted. They need health coverage to address problems that drive so many to opioids in the first place — chronic pain, an acute health event, depression, other mental illness. And, for people already suffering from addiction, they don’t just need anti-opioid medication; they also need treatment for their underlying health conditions, which means they badly need insurance. So make no mistake: ending the Medicaid expansion is bound to make the opioid problem worse.

- That’s not the end of the problems for Medicaid in the emerging Senate legislation. Like the House bill, not only will it end the Medicaid expansion and shrink the ACA’s premium subsidies, but it also adds another big Medicaid cut on top that has nothing to do with the ACA.

- Both the House bill and the emerging Senate bill would impose a new and unprecedented cap on the amount of federal Medicaid funds that each state can get for each Medicaid beneficiary it serves. The bills would set the cap at levels below what Medicaid is expected to cost in the years ahead, as the caps would not keep pace with the rising health care costs that state Medicaid programs will face.

- This cap is designed for one main purpose — to cut federal Medicaid spending, shift costs to the states, and force states to make the tough decisions on how to cut their Medicaid programs to fit within the cap. The cap poses serious threats to Ohio beneficiaries, its health care providers, and the state budget.

- The Center for Community Solution estimates that as a result of the House bill’s cap and its termination of the enhanced federal funding for the Medicaid expansion, Ohio would have to put up $16 to $22 billion in new state money from 2019-2025 if it wished to maintain Medicaid enrollment. The Urban Institute’s estimate is similar.

- And it could get even worse. Today, if a state’s Medicaid costs turn out higher than expected due to an epidemic — or due to medical breakthroughs that improve health and save lives but add to costs, such as blockbuster drugs like Sovaldi — the federal government bears its full share of the higher Medicaid costs, which in Ohio is 63% of those costs. By contrast, under the proposed House and Senate caps, once a state reached its increasingly inadequate cap limit, it would have to pay 100 percent of the added costs resulting from epidemics, medical advances, and other unforeseen developments.

- Suppose there were a new epidemic like HIV/AIDS? Or that new, much more effective — but more expensive — drugs or treatments emerged for various types of cancer, diabetes, Parkinson’s, or Alzheimer’s? Would Ohio deny these treatments to people on Medicaid? Would it sharply cut other aspects of Medicaid, like dental care, to come up with the money?

- There’s more. Under the House bill and the emerging Senate bill, the per-beneficiary cap would be based on Ohio’s average cost today for each of five categories of beneficiaries, one of which is the elderly. That’s another dagger aimed at Medicaid. Medicaid beneficiaries 85 and over have average Medicaid costs 2.5 times those of beneficiaries aged 65-75. So, Ohio and other states would be slammed when the huge baby-boomer cohort moved into old-old age and Medicaid costs per beneficiary rose farther beyond the cap.

- The bottom line is that Medicaid would be left considerably weaker than before the ACA was enacted.

- Senator Portman has tried to make the cap a bit less onerous by having it rise from year to year at a somewhat faster rate than under the House bill — but the reports are that he’s not been successful. Other Republican senators are pushing hard to go in the opposite direction — to make the Medicaid cap even more severe so it cuts federal Medicaid funding for states even more deeply. And they are calling for that in return for agreeing to let the Medicaid expansion take a few more years to phase out. Such a trade would make the permanent Medicaid cuts in the Senate bill even more severe than those in the House bill.

- The impact of such a cap would be particularly harsh in Ohio. Ohio ties for 8th lowest among all states in what its Medicaid program pays physicians. It ties for 12th highest in the share of its Medicaid population in managed care. Because Ohio has already achieved various efficiencies in its Medicaid program and squeezed the program and its providers, the state would be particularly hard-pressed to get large further savings out of Medicaid without cutting eligibility and covered health services — and possibly cutting already low provider reimbursement rates even further. All Medicaid populations — children, parents, seniors, and the disabled — could be at risk.

- The cap is no minor issue. Once the federal government ends its commitment to pay a specified share of state Medicaid costs and imposes an arbitrary cap, we have crossed the Rubicon. Medicaid will be a different program, and a much less adequate one.

- All of this is why a number of leading health care experts noted this week that the Medicaid cuts in the House bill and the likely Senate bill represent the “largest reduction in a social insurance program in our nation’s history,” and one that would be particularly devastating for elderly and disabled people including those in need of nursing home or similar care.

The Justifications for These Changes

How do policymakers justify these cuts?

- We often hear is that Medicaid is a bad, wasteful, inefficient program. But is it?

- Research shows that Medicaid costs more than 20% less per beneficiary than private health insurance for comparable people, and that Medicaid costs have been rising less rapidly in recent years than those for private insurance. The Congressional Budget Office found that moving people from Medicaid to private coverage actually increases costs — unless the coverage is much skimpier. Medicaid certainly isn’t perfect, but it’s the least costly form of major health insurance we have.

- For another thing, we often hear that Medicaid costs are projected to rise quickly in coming decades.

- That’s true, but those cost increases are being driven by demographics — the aging of the population — and by rising health care costs systemwide, part of which is due to medical advances and breakthroughs that improve health and save lives but add to costs. Slashing Medicaid without finding ways to slow health care cost growth systemwide will create more of a two-tier health system than we already have.

- And speaking of two-tier health care, the House bill — and apparently the emerging Senate bill — would do more to increase inequality in our country than any other action policymakers have taken in decades. I’ve worked on these issues for 45 years. I’ve never seen such aggressive Robin-Hood-in-reverse legislation — causing tens of millions of Americans at or near the bottom to become uninsured or underinsured, while showering extremely generous tax cuts on those at the very top.

- One also hears the argument that the Senate has to approve a bill to repeal the ACA so we don’t leave lots of people with no coverage options — including thousands in Ohio as a result of Anthem’s recent announcement that it will withdraw from the market.

- Again, let’s be clear. Anthem didn’t withdraw because of inherent problems with the ACA. Nationwide, insurers including Anthem — as well as Standard and Poor’s and other analysts — have noted that insurers are on a firmer financial footing this year and that in most states, the ACA marketplace was stabilizing when President Trump took office. Anthem made clear that the problem was the uncertainty that the Trump Administration and Republican lawmakers have created about the ACA, especially about the continued payment to insurers of the cost-sharing reduction subsidies they’re owed under the law, as well as the enforcement of the ACA’s individual mandate. In announcing its decision to largely leave the Ohio market, Anthem specifically cited those factors. Anthem’s withdrawal reflects the damaging effects of actions taken to undermine the marketplace, apparently in order to build more pressure for ACA repeal.

In fact, the Trump Administration took the extraordinary step last month of offering insurers a deal: it would continue to make the cost-sharing subsidy payments if the insurers endorsed the ACA repeal legislation. In my view, that’s an abuse of executive power that’s beyond the pale.

The answer here is not to enact draconian legislation that compounds the damage. It’s to provide certainty for insurers about the cost-sharing reduction subsidies and other matters. If so, there’s a very reasonable chance that Anthem will re-enter the Ohio market. And in a positive development this week, the insurer Centene is planning to expand its participation in the Ohio insurance market, possibly entering the markets Anthem is leaving.

Pre-Existing Conditions

Finally, a few words about pre-existing conditions.

This is another area where the devil’s in the details and, if you don’t dig in, you risk being misled. Recent news stories report that Senate Republicans will likely keep the ACA provision that bars insurers from charging higher premiums to people with pre-existing conditions. But please don’t think this will eliminate the threat that the emerging bill poses to people with pre-existing conditions. Under the bill, many of them would still be at great risk, because the Senate likely will also keep the House provision that lets states scale back what’s known as the ACA’s “essential health benefits” standard, which lays out the basic types of coverage that insurance policies must include.

Consider what would happen in a state that scaled back the standard, so insurers no longer had to cover various health services. Insurers would have strong incentive to offer stripped-down policies that carry lower premiums and could appeal to younger and healthier people. Insurers almost certainly would feel a need to do so to compete for such customers. But, for people with medical conditions who need treatments that the stripped-down policies don’t cover, that coverage wouldn’t work. As Andy Slavitt, the former head of the Centers for Medicare and Medicaid Services, noted, many insurers would — in Andy’s words — offer “Swiss cheese policies that drop benefits people with pre-existing conditions need most.” These people would have to buy either costly supplemental policies or more comprehensive insurance plans like those offered under the ACA today. But because of the availability of the stripped-down policies, the pool of people enrolling in the comprehensive plans or supplemental policies would consist largely of sicker-than-average people — and, as a result, premiums for those plans would be very high — and likely unaffordable for many people.

So, even though people with pre-existing conditions wouldn’t be charged higher premiums than others who bought the same policies, they’d still pay a lot more because they’d be enrolled in policies that would cost a lot more. Plus, as I mentioned earlier, premium subsidies would shrink substantially under the emerging Senate bill. The bottom line is that many people of modest means who have pre-existing conditions would be left high and dry — just as they were before the ACA.

So, here’s the question: Why make such harmful changes? More than anything else, the proponents say that we have to because the Marketplace is failing and its premiums are unaffordable. But the data don’t support that. In Ohio:

- 210,000 people are enrolled in Marketplace plans this year.

- Marketplace premiums now are 23% below premiums for comparable coverage in the employer-based market.

- And most marketplace consumers had a plan option this year for less than $100 a month in out-of-pocket premium costs, thanks to the ACA’s premium subsidies.

The marketplace has been working in Ohio, not perfectly but reasonably well — for healthy and sick people alike — at least it was until White House actions and the prospect of an ACA repeal created great uncertainty.

Conclusion

Where do we go from here? I see two potential paths.

One path — repealing and replacing the ACA — will mean that tens of millions of people will become uninsured or underinsured, health care providers serving large numbers of lower-income people will face increasingly severe financial pressures, and state budgets will face serious new problems. That path also will likely cost a considerable number of jobs in the health care and related sectors — a particular concern for Cleveland, where health care is one of the largest sectors of employment, as a recent report from Policy Matters Ohio explains.

There is, however, another possible path. Last weekend one of Governor Kasich’s advisers indicated the governor doesn’t support a plan that, and I quote “would dislodge millions from health care coverage.” End quote. That indeed should be a key test. Unfortunately, it’s one that, at this point, the bill coming to the Senate floor will almost certainly fail.

Governor Kasich also said on Tuesday that health care should be addressed through a process that is bipartisan and transparent. The prudent and responsible path now is to persuade enough Republican senators — there only need to be three — to oppose the highly ill-advised legislation coming to the Senate floor. Then, congressional leaders should undertake a true bipartisan effort, one that’s not fixated on repealing the ACA, to build on the progress in making health coverage accessible and affordable to more than 20 million Americans — and to make improvements to stabilize insurance markets, improve access, and hold down costs. That’s the right course for our nation.

But, to get there, we must first ensure that the emerging Senate bill fails to secure the necessary 51 votes in the Senate. With the crucial vote perhaps just days away, it is critical that everyone who shares that viewpoint make the case as forcefully as he or she can.

Thank you.