más allá de los números

What Will the Fed Look at in the November Jobs Report?

All signs point to the Federal Reserve taking its first baby step to raise interest rates later this month, irrespective of what’s in tomorrow’s jobs report. But the jobs report will continue to bear watching as a critical determinant of the Fed’s pace of future rate changes.

Fed Chair Janet Yellen said in a speech yesterday that she’s not ready to “declare that the labor market has reached full employment,” pointing to three key indicators of remaining labor market slack, which should be familiar to followers of CBPP’s past job market analyses:

- Individuals now classified as out of the labor force who can be brought back in by a stronger labor market. The labor force is composed of people who are working or actively looking for work. In October, almost 2 million people classified as not in the labor force said they wanted work and were available to take a job, Yellen noted. These people are classified as “marginally attached to the labor force” rather than “unemployed.”|

An even stronger labor market would bring people back into the labor force and increase the labor force participation rate (the share of the civilian population aged 16 and over in the labor force) and the employment-to-population ratio (the share of that population with a job). This can happen even without the unemployment rate falling further, although there looks to be room for that to happen too. - Individuals who report that they are working part-time but would prefer a full-time job and cannot find one. Some 5.8 million people were classified as “part-time for economic reasons” in October. Because they have jobs, they don’t contribute to the unemployment rate, but they are not employed to their full capacity and willingness to work. Yellen reports that the share of such workers climbed from 3 percent of all workers before the Great Recession to a peak of 6.5 percent in 2010. The recent drop to below 4 percent is a welcome improvement, but Yellen believes there’s room for these workers to increase their hours in an improving labor market.

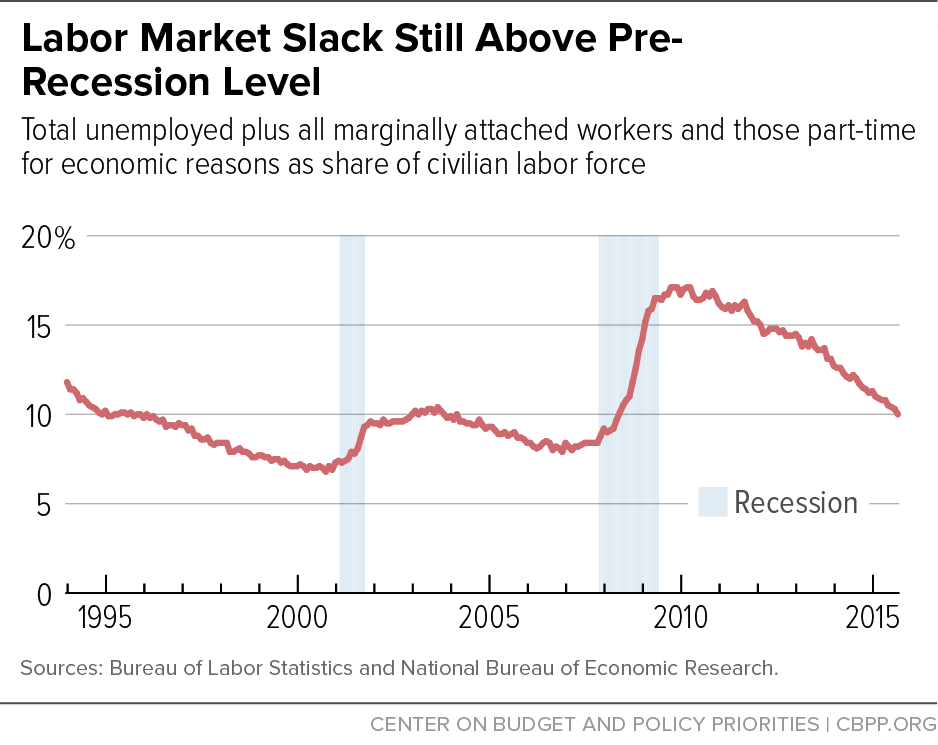

The Labor Department’s most comprehensive alternative unemployment measure (U-6), which incorporates not only the official unemployment rate but also marginally attached workers and those working part-time for economic reasons, remains above where it was at the start of the recession (see first chart) — in contrast to the unemployment rate alone, which is back to where it was at the start of the recession.

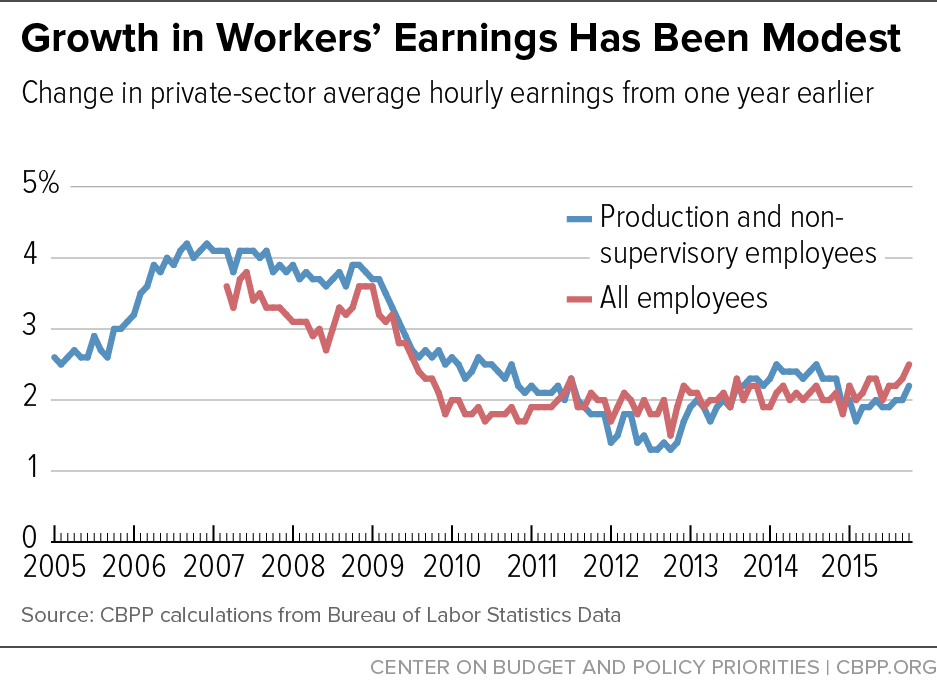

- Modest wage growth. Slow growth in workers’ pay and a rising share of national income going to profits are indirect evidence of labor market slack; when there are more job seekers than job openings employers have little incentive to raise wages. Yellen notes “a welcome pick-up” in some key measures of worker pay, including one — average hourly earnings of private-sector workers — reported in the monthly jobs report (see second chart).

To show continued acceleration, average hourly earnings of all employees would have to exceed $25.30 and those of production and non-supervisory employees would have to exceed $21.29 in November.

The Fed seems committed to making an initial rate hike this month. Yellen says, however, that the Fed isn’t on a pre-determined path for further rate changes. She observes that going forward it has more scope to deal with surprises calling for faster tightening than for unanticipated weakness and therefore should be cautious in raising rates further. Data in the monthly jobs report will continue to provide important evidence of how cautious the Fed should be.