State Job Creation Strategies Often Off Base

To create jobs and build strong economies, states should focus on producing more home-grown entrepreneurs and on helping startups and young, fast-growing firms already located in the state to survive and to grow ― not on cutting taxes and trying to lure businesses from other states. That’s the conclusion from a new analysis of data about which businesses create jobs and where they create them.

The data show that:

- The vast majority of jobs are created by businesses that start up or are already present in a state — not by the relocation or branching into a state by out-of-state firms. Jobs that move into one state from another typically represent only 1 to 4 percent of total job creation each year, depending on the state. Jobs created by out-of-state businesses expanding into a state through the opening of new branches represent less than one-sixth of total job creation. In other words, “home-grown” jobs contribute more than 80 percent of total job creation in every state.

- During periods of healthy economic growth, startups and young, fast-growing companies are responsible for most new jobs. During the Internet-driven boom of the late 1990s and early 2000s, for example, startup firms (those less than one year old) and high-growth firms — which are likely to be young — accounted for about 70 percent of all new jobs in the U.S. economy. Firms older than one year actually lost jobs on average; any new jobs they created were more than offset by jobs they eliminated through downsizing or closure. In short, startups and young, fast-growing firms are the fundamental drivers of job creation when the U.S. economy is performing well.

State economic development policies that ignore these fundamental realities about job creation are bound to fail. A good example is the deep income tax cuts many states have enacted or are proposing. Such tax cuts are largely irrelevant to owners of young, fast-growing firms because they generally have little taxable income. And, tax cuts take money away from schools, universities, and other public investments essential to producing the talented workforce that entrepreneurs require. Many policymakers also continue to focus their efforts heavily on tax breaks aimed at luring companies from other states — even though startups and young, fast-growing firms already in the state are much more important sources of job creation.

It is too soon to know what strategies will work best, as many states and localities experiment with various ways to boost the number and success rates of startups and young, fast-growing firms. In the meantime, policymakers should reject major income tax cuts and new corporate relocation subsidies, and reconsider those already enacted. Public investments that help build a skilled workforce and improve the quality of life for local residents are better bets ― successful entrepreneurs report these factors are key to where they founded their companies.

Recent Data Have Changed Our Understanding of Which Businesses Create Jobs

Prior to the last 15 years or so, a lack of useful data severely limited research about which kinds of firms create jobs. It was very difficult, if not impossible, to track job creation accurately over time by the size or age of companies. The increasing tendency of large multistate and multinational corporations to buy successful smaller businesses and to divest themselves quickly of poorly performing subsidiaries made it even more challenging to determine whether changes in a given corporation’s employment levels represented real job creation or destruction or resulted from these kinds of ownership changes.

In more recent years, however, the federal government has developed new databases that track over time the job-creation record of specific businesses of various sizes and ages while accounting for ownership changes. The U.S. Census Bureau has developed two such “longitudinal” databases. The U.S. Labor Department has developed one as well, and a private company using the private Dun & Bradstreet business registry has created yet another.

Research using the new data has revolutionized our understanding of which businesses create jobs — and where they create them.

Startups and Young, Fast-Growing Companies Drive Job Creation

One crucial discovery flowing from the new data is that “startups” ― firms in their first year of existence ― play a critical role in job creation. Startups created an average of almost 3 million jobs per year between 1990 and 2009.[1] By contrast, businesses older than one year in aggregate lost jobs relative to their prior-year employment levels.[2] (See the “Job Creation and Job Elimination” text box, below.)

Job Creation and Job Elimination — “Gross” and “Net”

Businesses are constantly creating and eliminating jobs as demand for the goods and services they produce rises and falls. A state sees a net increase in private sector employment in a given period when businesses create more jobs in the state than they eliminate during that period.

Gross job creation in a state arises from four conceptually distinct processes:

- New, free-standing businesses start up with a certain number of initial employees (“job creation from startups”)

- Existing businesses in a state hire more people at an existing business location (“job creation from expansions”)

- Existing businesses create jobs by establishing a new business location (“job creation from branching”). The new branch (“establishment”) may be created by a business that is headquartered in the state or in another state.

- Existing businesses in another state move jobs into the state (“job creation from relocation”). That relocation may be of either the entire business or a portion of it.

Similarly, gross job elimination (usually referred to by economists who study these dynamics as job “destruction”) results from three distinct processes:

- Existing firms or entire branches of existing firms shut down completely (“job deaths”)

- Existing firms or branches reduce their employment levels (“job contractions”)

- Existing firms or portions of firms shut down in one state and move to another state (“job elimination from relocation”).

The amount of net job creation or elimination that occurs in a particular state over a particular period of time is the combined outcome of all of these processes.

To a certain extent, startups’ outsized role in job creation results from how they are defined and how their jobs are measured. Unlike older businesses, startups cannot reduce the number of people they employ through failure or downsizing because if a business fails before it reaches its first anniversary, it is not counted as a startup. Likewise, its employment levels can’t shrink because there is no “year-zero” employment level to which its first-year employment level can be compared. In other words, by definition startups can only create jobs.

Moreover, most startups fail. Within five years, more than half are gone and many others go out of business a few years later.[3] Among the survivors, most start small and stay small.[4]

Startups’ most important role is in being the incubators of most of the rapidly growing firms that create a disproportionate number of new jobs during their early years — the so-called “gazelles.” These firms — the Googles, Amazons, Teslas, and Under Armours of the world — achieve very rapid job growth by developing a new service, technology, or business model. Researchers often define “gazelle” firms as those that produce average annual job growth of at least 20 to 25 percent.[5]

Startups created roughly 3 million jobs per year on average between 1980 and 2010.[6] While half of those jobs were gone within five years because the companies that created them did not survive, the other 1.5 million jobs remained. Even more, the surviving firms included some gazelles. As a result, the average surviving firm grew an astonishing 60 percent over the first five years, adding another 900,000 jobs to the economy.[7] As a result, at the end of the five-year period a given year’s batch of startups created 2.4 million jobs — a substantial contribution to total private sector employment, even if less than the original 3 million. And keep in mind that the 2.4 million job-creation record for each annual cohort of startups was repeated in each subsequent year.[8]

This process makes startups and young, fast-growing firms crucial to U.S. job creation. As economist John Haltiwanger and his colleagues summarize:

[Y]ounger firms have much higher rates of job growth than more mature firms. . . . Together, start-ups and high-growth firms (which are disproportionately young . . . ) account for about 70 percent of . . . gross job creation in a typical year. Balancing this positive contribution is the sharp job loss that occurs for many firms in the first several years after start-up. . . . Overall, the evidence shows that most start-ups fail, and most that do survive do not grow. But among the surviving start-ups are high-growth firms that contribute disproportionately to job growth. These high-growth young firms yield the long-lasting contribution of start-ups to net job creation.[9]

There aren’t many gazelle firms, but they have had a disproportionate impact on job growth. They accounted for about 15 percent of businesses, but 50 percent of gross job creation for the 1992-2011 period as a whole, Haltiwanger and his co-authors found.[10]

More recent research by Haltiwanger and his colleagues has uncovered a dropoff in the creation of gazelle firms starting around 2000.[11] They and other researchers have also reported a troubling decline in the rate at which new businesses have been started in the United States.[12] Whether these trends are permanent or the temporary outcome of two recessions just six years apart in the 2000s is unclear. The causes of these trends are also murky and require further research. Haltiwanger and his colleagues hypothesize, for example, that post-2000 gazelle firms could still be growing rapidly but substituting foreign workers or machines for U.S. employees more than their predecessors did, or are being acquired more quickly by larger, older firms and thus their jobs are not showing up in the data as coming from young, high-growth businesses.[13]

In any case, these new developments should encourage states to focus even more intensely on startups and young, high-growth firms as the centerpieces of their economic development efforts. During the 1980s and 1990s, the heyday of gazelles like Amazon and Google, annual private sector job growth averaged 2 percent. Job growth in the 2000s was flat. Boosting entrepreneurship thus remains key to achieving robust economic growth in individual states as well as in the United States as a whole.

Most Jobs Are Created by Businesses That Start Up or Are Already in a State

Another key insight made possible by the data tracking firms’ job creation over time is that the vast majority of jobs created in every state are “home grown” — they are produced by firms already located in that state.

With regard to startups, this is again true almost by definition. Although a firm could open multiple business locations in multiple states before reaching its one-year anniversary, this is likely to be rare. Most startups, from restaurants to biotech companies, are likely to operate from a single location in their first year. Even if they operate more than one establishment (for example, an administrative office and a factory or lab), the limited staff and other resources available to a small firm to coordinate these activities means that the establishments are likely to be in the same state.

Further, entrepreneurs on the cusp of starting a new business typically do not relocate prior to doing so. That is, entrepreneurs tend to start their business where they already live. A study of 150 founders of “Inc. [magazine] 500” companies (the fastest-growing companies in the United States) by the Endeavor Insight consulting firm found that “entrepreneurs at fast-growing firms usually decide where to live based on personal connections and quality of life factors many years before they start their firms . . . 80 percent of them had lived for at least two years in the city where they started their companies. . . .” The most commonly cited reason among the entrepreneurs for starting the companies where they did was that it was where they lived at the time.[14] Academic research on the location decisions of entrepreneurs supports these findings.[15]

Beyond startups, another large share of job creation results from the expansion of employment at existing business locations. Firms squeeze in additional cubicles, factories add a second shift, and office-based businesses lease additional floors of their buildings. Later, if the business grows enough, it may open a new establishment nearby. For example; a successful downtown restaurant may open a second location in the suburbs, and a manufacturer may open a new facility to make for itself a component whose production it previously outsourced. But again, these new establishments are likely to be located in the same state as their parent firm.

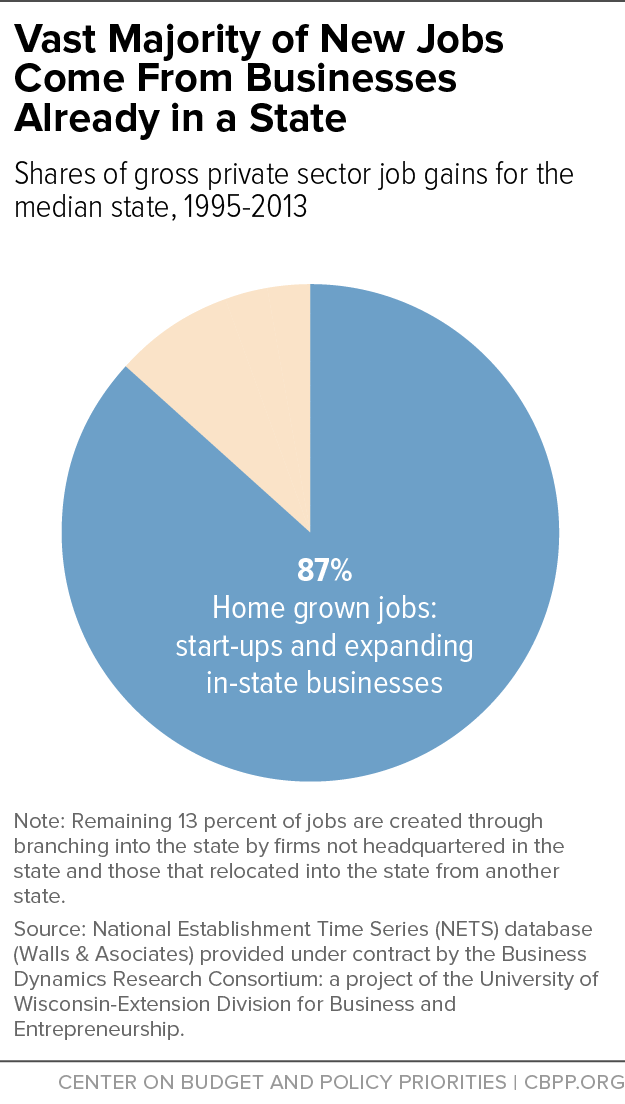

As Figure 1 shows, fully 87 percent of all 1995-2013 gross private-sector job creation was “home grown” — it came from startups, the expansion of employment at existing establishments, and the creation of new in-state locations by businesses already headquartered in the state.[16] Although much discussion by elected officials of economic development is framed as “attracting businesses from other states,” only 11 percent of the new jobs created in the median state were the result of the creation of new in-state business establishments by companies headquartered out-of-state. And an even smaller share of new jobs — a miniscule 3 percent — resulted from the actual relocation of pre-existing positions from one state to another.

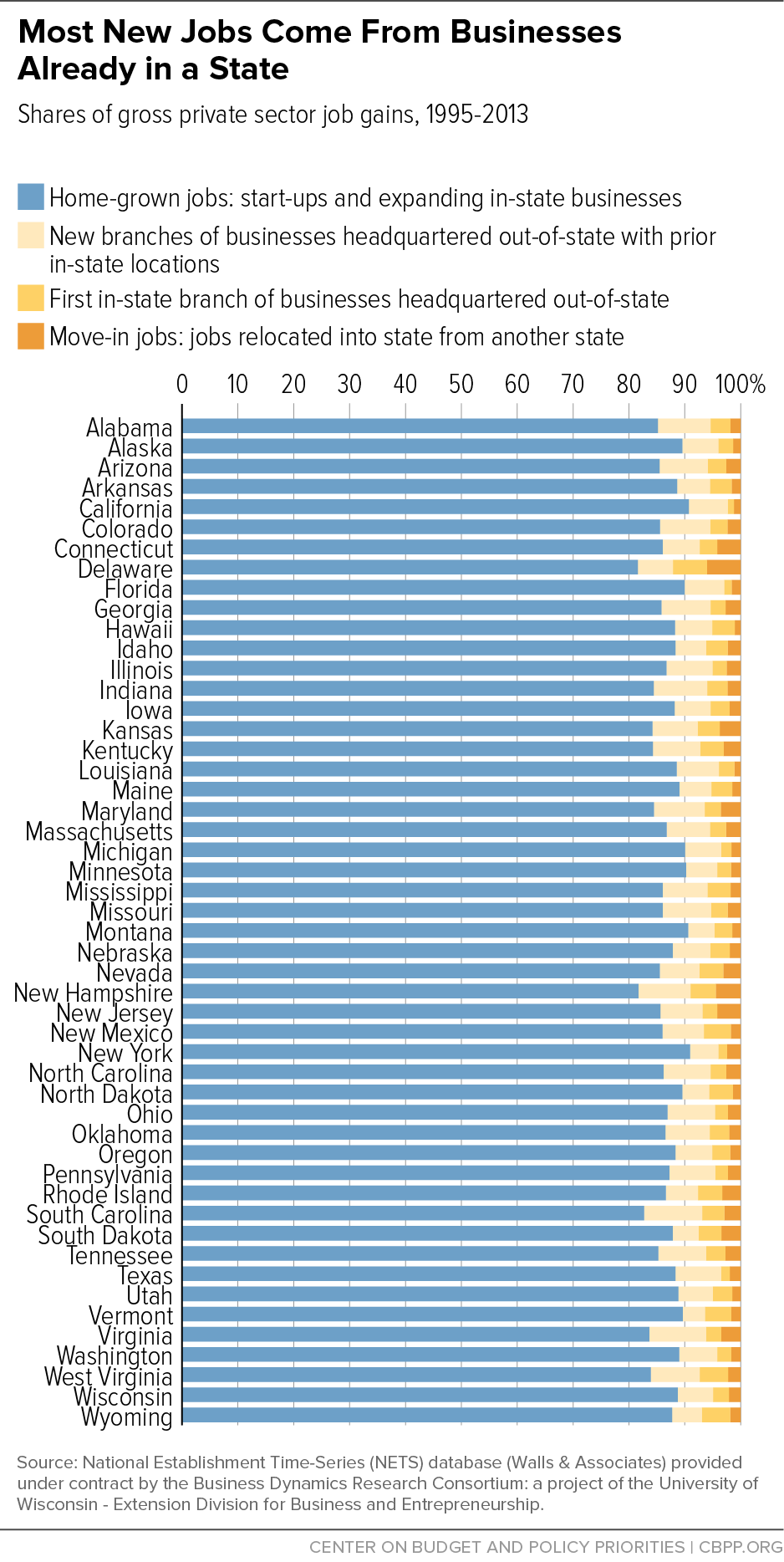

The relative shares of these three types of job creation vary relatively little among the states. (See Figure 2.) For example, startups and expansions of in-state businesses accounted for between 82 percent (Delaware) and 91 percent (New York) of total job creation. Relocations generally accounted for between 1 percent and 4 percent of job creation, with only five states falling outside that range.[17] Job creation from the opening of new branches in a state by businesses headquartered out of state varies somewhat more, ranging from 7 percent (New York) to 14 percent (South Carolina).

Moreover, as Figure 2 illustrates, the majority of jobs created by interstate branching came from businesses that were headquartered out-of-state but already had facilities in the state. In every state except one (Vermont) at least half of the jobs created by the branching of out-of-state firms into the state were created by businesses that were already present in the state, and in some 30 states at least two-thirds of “new branch” jobs were created by already present firms. Firms tend to branch into states where they already are familiar with the market for their products, know that the labor force generally has the skills their industry needs, and can realize managerial, transportation, and other logistical efficiencies and cost savings by remaining close to their existing facilities.

Many States Pursue Failing Economic Development Strategies

State policymakers too often pursue economic development strategies that are bound to fail because they ignore the fundamental realities about job creation revealed by the new data and research discussed above.

Income Tax Cuts for “Small Businesses”

In recent years, policymakers in a number of states have pursued deep cuts in individual income taxes in the name of encouraging economic growth. The logic behind these tax cuts seems to be that most businesses that become innovative high-growth firms start out small, and most small business owners pay personal income taxes rather than corporate income taxes on the businesses’ profits.[18] On the basis of this theory, some states have cut top income tax rates, and others have completely or partially exempted small business profits from taxation. Both types of tax cuts are ill-advised for a number of reasons.

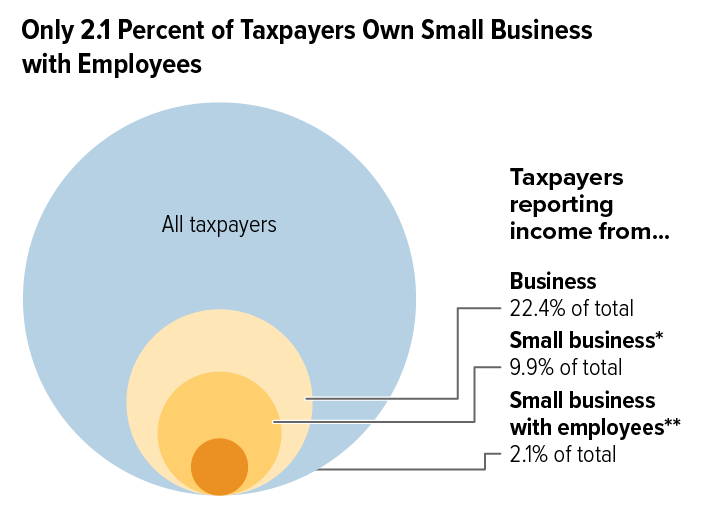

First, they are poorly targeted to young, fast-growing firms. Only one of every seven U.S. taxpayers has any ownership stake in an active small business, so an across-the-board cut in income tax rates is an extremely costly and wasteful way to help such businesses.[19] (See Figure 3.) Tax cuts limited to small business profits are just as poorly targeted to firms likely to create jobs, because four-fifths of small businesses employ no one except the owner.[20] The vast majority of such businesses have little potential to hire even a single employee — let alone numerous employees.[21]

Even if tax cuts were limited to small businesses with employees — and none of those proposed or enacted in recent memory have been — they would be almost as wasteful and ineffective in creating jobs as cuts in the top income tax rate. As economist Ian Hathaway has explained: “Young companies, not necessarily small companies, are responsible for the substantial majority of net job creation in the U.S. In fact, outside of startups, small business net job creation has been negative during the last two decades.” outside of startups, small business net job creation has been negative during the last two decades. From 1990 to 2009, the only small businesses that created jobs were start-ups — those less than a year old. Young small businesses (those between one and five years old) were net job losers due to high failure rates, and older small businesses were net job eliminators as well. [22] Again, as Haltiwanger’s path-breaking research has demonstrated, only “a small fraction of high-growth firms contribute disproportionately to job creation in the United States. These findings pose challenges to policymakers seeking to promote job creation by encouraging entrepreneurship, because most young and small businesses are not in fact primary creators of jobs.”[23]

The second reason state personal income tax cuts are unlikely to help many of the rapidly growing start-up firms most likely to create a large number of jobs is that many of these firms spend so heavily on new equipment, product development, and marketing that they have relatively little taxable profit in their early years.[24] In response to a costly decision in Kansas to exempt the profits of all small businesses in the state from personal income taxation, entrepreneurship experts Dane Stangler and Jason Wiens recently observed, “[I]ncome taxes are often less of an issue [for young companies] than employment and property taxes [because the latter two taxes are due even if the business isn’t profitable while income taxes are not].”[25] It therefore is not surprising that in the Endeavor Insight study “Only 5% of entrepreneurs cited low tax rates as a factor in deciding where to launch their company.”[26]

—Endeavor Insight study

Perhaps the most serious consequence of making deep cuts in personal income taxes to stimulate entrepreneurship is that the revenue loss is likely to harm the state’s education system and other public investments that entrepreneurs need. In the Endeavor Insight study, “31% of founders cited access to talent as a factor in their decision on where to launch their company. . . . A number of founders also highlighted the link between the ability to attract talented employees and a city’s quality of life.” This suggests that states that cut taxes and then address the revenue loss by letting their schools, parks, roads, and public safety deteriorate will become less attractive to the kinds of people who start high-growth companies and the people they need to hire.

Tax and Non-Tax Incentives to Lure Out-of-State Companies

Many policymakers also continue to focus on trying to lure companies from other states with tax breaks, grants, and various forms of direct aid. Experts have pointed to the disconnect between the growing body of data showing that the vast majority of jobs are home-grown and the continued focus on what used to be called “smokestack chasing”:

[T]he common zero-sum attempts to incentivize firm relocation are oblivious to the important pattern of gross job creation revealed by the B[usiness] D[ynamics] S[tatistics]. States and cities with job creation policies aimed at luring larger, older employers can’t help but fail, not just because they are zero-sum, but because they are not based in realistic models of employment growth. Job growth is driven, essentially entirely, by start-up firms that develop organically. . .[27]

The new data on the dynamics of job creation demonstrate that elected officials’ all-too-common tendency to equate economic development with the state’s ability to attract jobs from other states and prevent business flight is at odds with how state job creation actually occurs. As discussed above, jobs gained due to firm relocation are such trivial factors in a state’s overall job creation record that they should not be a consideration in formulating state tax policy or economic development policy more broadly. Likewise, the data cited above on the very small share of jobs resulting from interstate branching implies that focusing on attracting new branch facilities of businesses embedded in industries with little prior presence in the state is likely to provide little job creation bang for the revenue buck given away.

Policy Directions

There is a growing consensus among the economists who have studied the new data on the dynamics of job creation about its implications for public policy: policy needs to focus on encouraging entrepreneurship generally, helping new businesses to survive, and enabling businesses with the potential to become high-growth firms to fulfill that potential.

So, for example, economist Ian Hathaway has argued that affirmative state policy needs to boost entrepreneurs’ ability to obtain “critical early-stage capital.” [28] And entrepreneurship expert Scott Shane suggests that policymakers can focus as well on how to help businesses survive past the start-up phase: “[s]mall-business development centers could spend less time teaching would-be entrepreneurs how to write business plans and more time teaching existing business owners to manage their cash flow.”[29]

While state and local economic development experts are developing a consensus about what types of firms to help, they do not necessarily agree about how to do so. States and cities throughout the country are engaged in an array of experiments aimed at figuring out what entrepreneurs need from public policy and how to most cost-effectively allocate limited resources. There are pilot programs in entrepreneurship education, in converting public university research into commercially useful products, in organizing networks of startup “angel investors,” in crowd-funding new firms, in linking entrepreneurs with mentors, in organizing informal networking events for entrepreneurs, and many more. Many of these pilot programs are being studied — and in some cases partially financed — by the Kauffman Foundation, a leading national think-tank on entrepreneurship and entrepreneurship policy. The foundation has published “Guidelines for Local and State Governments to Promote Entrepreneurship,”[30] and in February 2016 will issue “America’s New Entrepreneurial Growth Agenda,” an expanded set of entrepreneurship policy recommendations for federal, state, and local governments to consider.

It may take five to ten years of this type of experimentation to arrive at a consensus about the most cost-effective ways for states and localities to foster entrepreneurship and high-growth firms. In the meantime, policymakers should avoid frittering away precious tax revenue on scattershot tax cuts for small businesses and yet more incentive programs aimed at poaching today’s hot out-of-state industry. Such actions will only harm their state’s ability to provide the high-quality public education, transportation, and recreation that build the skilled workforce and quality of life that today’s high-growth entrepreneurs seek.

End Notes

[1] Ian Hathaway, “Small Business and Job Creation: The Unconventional Wisdom,” Bloomberg Government Briefing, October 31, 2011, p. 8.

[2] Hathaway, p. 8.

[3] Ryan Decker, John Haltiwanger, Ron Jarmin, and Javier Miranda, “The Role of Entrepreneurship in US Job Creation and Economic Dynamism,” Journal of Economic Perspectives, Summer 2014, p. 8, https://www.aeaweb.org/atypon.php?return_to=/doi/pdfplus/10.1257/jep.28.3.3.

[4] Economists Eric Hurst and Benjamin Pugsley have found that the vast majority of new small businesses stay small because they are in industries characterized by numerous, independent small-scale firms (restaurants, for example) and because their founders have no desire to manage large, multi-establishment enterprises. See: “What Do Small Businesses Do?” Brookings Papers on Economic Activity, Fall 2011.

[5] For a discussion of the various ways that researchers have defined gazelle firms, see: Magnus Henrekson and Dan Johansson, “Gazelles as Job Creators: A Survey and Interpretation of the Evidence,” Small Business Economics, 2010.

[6] Decker, Haltiwanger, Jarmin, and Miranda, 2014, p. 6.

[7] Only a fraction of these surviving firms would achieve the 20 to 25 percent annual growth rate that is often used to define “gazelles,” which is why their average growth rate is about 60 percent rather than 100 percent or more.

[8] Total annual private sector job creation during this period was significantly less than 2.4 million because businesses more than five years old are net job eliminators.

[9] Decker, Haltiwanger, Jarmin, and Miranda, 2014, pp. 8-10.

[10] Decker, Haltiwanger, Jarmin, and Miranda, 2014, p. 9.

[11] Ryan A. Decker, John Haltiwanger, Ron S. Jarmin, and Javier Miranda, “Where Has All the Skewness Gone? The Decline of High-Growth (Young) Firms in the U.S.,” December 2015, http://www.nber.org/papers/w21776. This paper examines gazelle job growth through 2011.

[12] Decker, Haltiwanger, Jarmin, and Miranda, 2014, pp. 13-21. See also: Ian Hathaway and Robert Litan, “Declining Business Dynamism in the United States: A Look at States and Metros,” Brookings Institution, May 2014.

[13] Decker, Haltiwanger, Jarmin, and Miranda, 2015, p. 26. The study notes that “For any continuing establishment that changes ownership. . . [our] method[ology] attributes any [subsequent] net employment growth to the acquiring firm” (emphasis added), p. 8.

[14] Endeavor Insight, “What Do the Best Entrepreneurs Want In a City? Lessons from the Founders of America’s Fastest Growing Companies,” February 2014, p. 6, http://issuu.com/endeavorglobal1/docs/what_do_the_best_entrepreneurs_want.

[15] For a summary of this research, see: Michael Mazerov, “Cutting State Personal Income Taxes Won’t Help Small Businesses Create Jobs and May Harm State Economies,” Center on Budget and Policy Priorities, February 19, 2013, pp. 12-14, https://www.cbpp.org/sites/default/files/atoms/files/2-19-13sfp.pdf.

[16] 1995-2013 is the entire period for which complete data from the National Establishment Time Series (NETS) database are most readily available to researchers. NETS is the only longitudinal business database that is capable of identifying jobs moved from one state to another, which is why it was used for the analysis in this portion of this paper.

[17] A 2010 paper used the same data source, the National Establishment Time Series (NETS) database, to calculate the share of job creation and elimination attributable to business relocations for a limited number of states. See: Jed Kolko, “Business Relocation and Homegrown Jobs, 1992-2006,” Public Policy Institute of California, September 2010, http://www.ppic.org/content/pubs/report/R_910JKR.pdf.

[18] Most small businesses are legally organized as sole proprietorships, Subchapter S corporations, partnerships, or limited liability companies. As a group these types of businesses are known as “passthrough entities,” because any profit (or loss) of the business is exempt from federal and state corporate income taxes and instead is passed through for tax purposes to the personal income tax return of the owner(s).

[19] Mazerov, p. 3.

[20] In 2012, 22.7 million U.S. businesses had no employees other than the owner(s) — what the federal government and economists refer to as “nonemployer” businesses. (See: https://factfinder.census.gov/faces/tableservices/jsf/pages/productview.xhtml?pid=NES_2012_00A2&prodType=table.) An additional 5.7 million businesses had at least one paid employee in addition to the owner(s). (See: Anthony Caruso, “Statistics of U.S. Businesses Employment and Payroll Summary, 2012,” U.S. Census Bureau, February 2015, http://www.census.gov/content/dam/Census/library/publications/2015/econ/g12-susb.pdf.) These facts taken together mean that four-fifths of U.S. businesses are non-employer firms. In fact, it is likely that significantly more than four-fifths of all businesses are non-employer firms. The Census Bureau considers a business legally organized as a corporation to be an “employer business” even if the only person(s) drawing a salary from the business are its owner(s). There are many such corporations, most of which elect “S corporation” passthrough tax treatment under the federal Internal Revenue Code.

[21] A 2009 study looked at non-employer businesses in 40 industries in which they are most commonly found and found that between 1994 and 1997 only 3 percent of them transitioned to employer businesses by hiring at least one worker. See: Steven J. Davis, et al., “Measuring the Dynamics of Young and Small Businesses: Integrating the Employer and Nonemployer Universes,” in Timothy Dunne, J. Bradford Jensen, and Mark J. Roberts, editors, Producer Dynamics: New Evidence from Micro Data, University of Chicago Press, 2009.

[22] Hathaway, p. 11.

[23] Decker, Haltiwanger, Jarmin, and Miranda, 2014, p. 21.

[24] A recent study found that start-up firms receiving venture capital investments are likely to grow much more rapidly and ultimately create a much larger number of jobs than similar firms not obtaining venture capital. The study found that fully 47 percent of firms receiving such investments had no revenue in their first year of operation, let alone any profit. Moreover, for the firms that were profitable, the profitability dropped sharply after the venture capital investment as the firms used the money to hire more higher-salary employees and to grow rapidly. It took an average of nine years for the rate of profit of venture-capital-financed startups to equal the rate of profit of start-ups that did not obtain venture capital investments. Manju Puri and Rebecca Zarutskie, “On the Lifecycle Dynamics of Venture-Capital- and Non-Venture-Capital-Financed Firms,” National Bureau of Economic Research Working Paper 14250, August 2008.

A second study found that “while investing in the development of intellectual property (specifically, patents) in young ventures allows them to grow their sales, this growth is not profitable (at least in the short run).” Maija Renko, “Innovations and the Performance of New Ventures: Evidence from the Kauffman Firm Survey,” unpublished, 2011. Emphasis added.

[25] Dane Stangler and Jason Wiens (Kauffman Foundation), “Young Companies Are the Job Creators,” Wichita Eagle, June 1, 2014.

[26] Endeavor Insight, p. 12.

[27] Tim Kane, “The Importance of Startups in Job Creation and Job Destruction,” Kauffman Foundation Research Series on Firm Formation and Economic Growth, July 2010, p. 6, http://www.kauffman.org/~/media/kauffman_org/research%20reports%20and%20covers/2010/07/firm_formation_importance_of_startups.pdf.

[28] Hathaway p. 16.

[29] Scott Shane, “Why We Should Invest More in Existing Businesses,” Entrepreneur, March 22, 2012; http://www.entrepreneur.com/article/223204.

[30] March 2015, available at http://www.kauffman.org/~/media/kauffman_org/research%20reports%20and%20covers/2015/03/government_guideline_report.pdf.

More from the Authors

Areas of Expertise