House GOP Health Bill Still Cuts Tax Credits, Raises Costs by Thousands of Dollars for Millions of People

Allocating “Reserve Fund” To Higher Tax Credits Would Come Nowhere Close to Solving the Problem

The updated House Republican legislation to repeal the Affordable Care Act (ACA) raises total out-of-pocket health costs (premiums, deductibles, copays, and coinsurance) by an average of $3,600 in 2020 for people who buy health insurance through the ACA marketplaces — just as the previous version of this legislation would have done. Total cost increases would be larger for people who have lower incomes, are older, or live in high-cost states. Specifically, as explained below, tax credits that help people pay premiums would fall sharply (by an average of $2,200); average premiums would rise; and out-of-pocket costs such as deductibles, copays, and coinsurance would increase (by an average of $1,200). Total cost increases would be larger for people who have lower incomes, are older, or live in high-cost states: in 15 states, average increases would exceed $4,000.

House Republicans have argued that, rather than analyze their bill as written, observers should judge it based on how the Senate might change it. Specifically, they note that the updated bill allocates $85 billion to expand the income tax deduction for out-of-pocket medical expenses, and they argue that these resources constitute a reserve fund that the Senate can use “to potentially enhance the tax credit for those aged 50 to 64 who may need additional assistance.”[1]

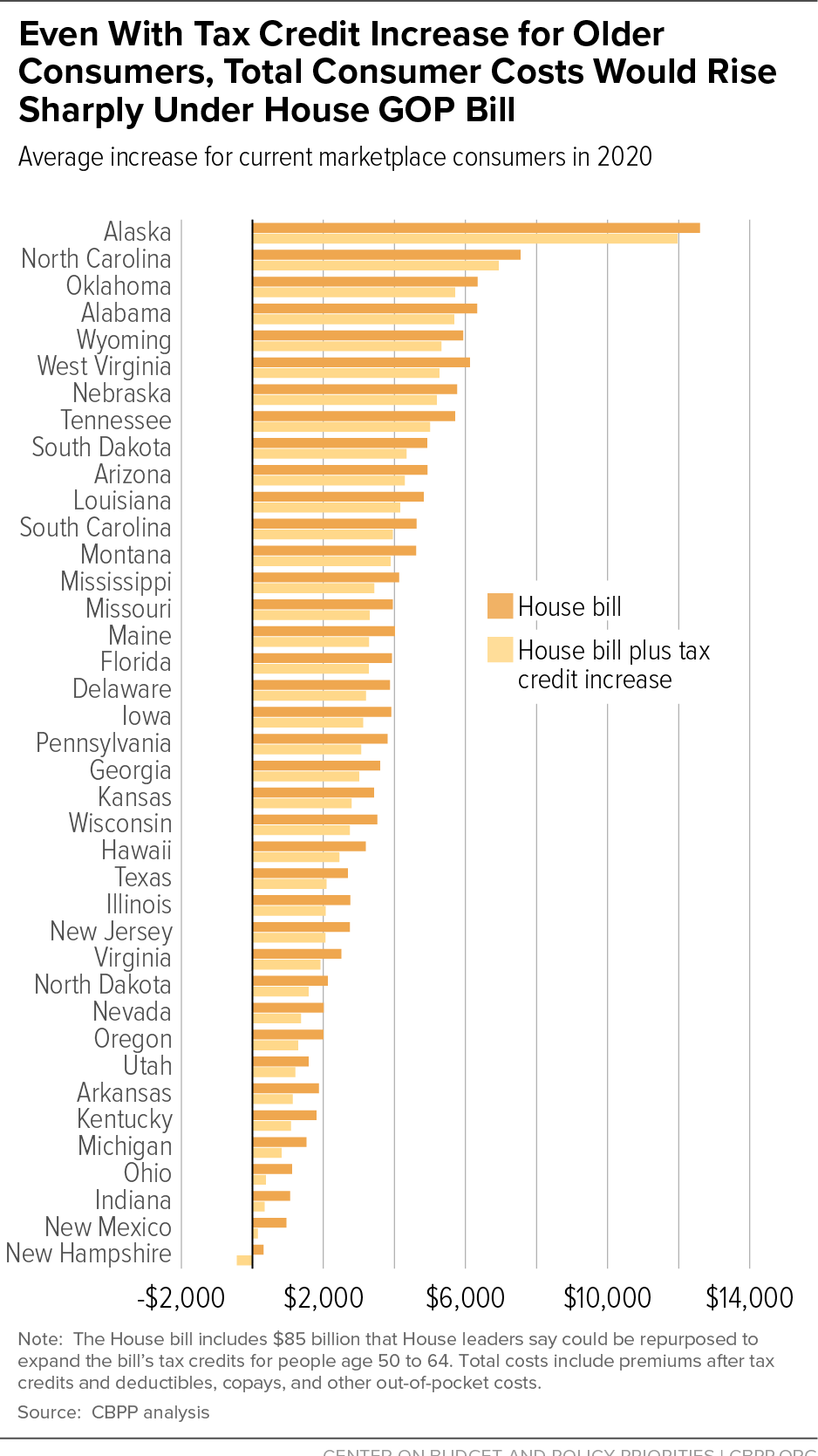

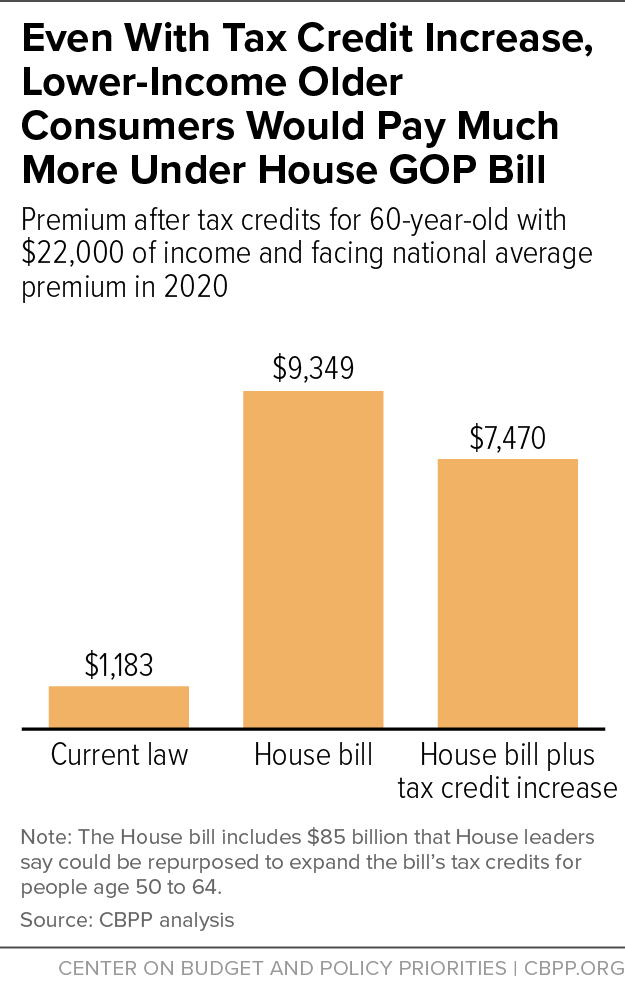

But even if fully $85 billion were reinvested in higher tax credits for older Americans, total cost increases for marketplace consumers would still average $2,900 — more than 80 percent as much as under the current House bill. Total costs would still increase by an average of more than $4,000 in 11 states. (See Figure 1.) And lower-income seniors would still be the hardest hit. For example, premiums, net of tax credits, for a 60-year-old with income of $22,000 would increase six-fold, from $1,200 to $7,500.

Analyzing the Impact of the House Plan

This paper estimates the House bill’s impact on total health care costs, as written and if the bill’s tax credits for people age 50 and older were increased by $85 billion. Our estimates draw on data from the Centers for Medicare & Medicaid Services (CMS), projections from the Congressional Budget Office (CBO) and the CMS Actuary, and CBO’s analysis of the House bill’s impact on premiums and plan generosity. For data availability reasons, we focus on impacts for the roughly 9 million marketplace consumers in the 39 states that use the HealthCare.gov enrollment platform. Compared to our earlier paper on the House plan’s impact on tax credits, this paper updates the analysis for more recent data released by CMS on March 15; as a result, many estimates change slightly.[2] Our estimates for the base House bill (not including the $85 billion increase in tax credits) are similar to cost estimates from the Center for American Progress.[3] (For a complete description of our methodology, see the Appendix.)

We estimate the average impact of the House bill for current marketplace consumers, supposing they all maintained coverage. The House plan, unlike the ACA, also provides tax credits to the minority of individual-market consumers who purchase coverage outside the marketplace (though not to those with the highest incomes). Thus, average tax credits under the House plan, taking into account all individual-market consumers, would be higher than the amounts we calculate. But the impact on current marketplace consumers is the more relevant metric for assessing the House plan’s impact on coverage and affordability, since people purchasing health insurance outside the marketplace, by definition, can afford coverage without financial assistance.

As with any estimates of the impacts of complex health care legislation, our precise estimates are subject to significant uncertainty. Nonetheless, they paint a clear picture of how the House bill would affect various groups of marketplace consumers.

The House Plan’s Impact on Tax Credits

The ACA’s premium tax credit varies based on income and the cost of insurance. Low- and moderate-income families without access to other coverage are guaranteed the option to purchase benchmark health insurance for a set percentage of their income, with the premium tax credit covering the remainder. Once the credit’s value is set under this formula, consumers can use the credit to help pay the premium of any qualified health plan offered in their state’s marketplace.

Because the ACA’s premium tax credit is based on the cost of a benchmark plan — an actual plan in the marketplace for someone of the consumer’s age in the consumer’s geographic rating area — it is flexible enough to meet the needs of people who live in high-cost states, are older, or have lower incomes. The average ACA premium tax credit in HealthCare.gov states is projected to be about $5,000 in 2020. But because of the large variation in the cost of coverage across states, tax credits would average more than $13,000 in Alaska and less than $3,000 in New Hampshire. Credits also vary significantly by age and income.

By contrast, the House bill would provide flat tax credits varying only by age: $2,000 for people under 30, $2,500 for people age 30 to 39, $3,000 for people age 40 to 49, $3,500 for people age 50 to 59, and $4,000 for people age 60 and older. Tax credits would be the same regardless of the local cost of premiums and would generally be the same regardless of income (although they would phase out at higher income levels).[4]

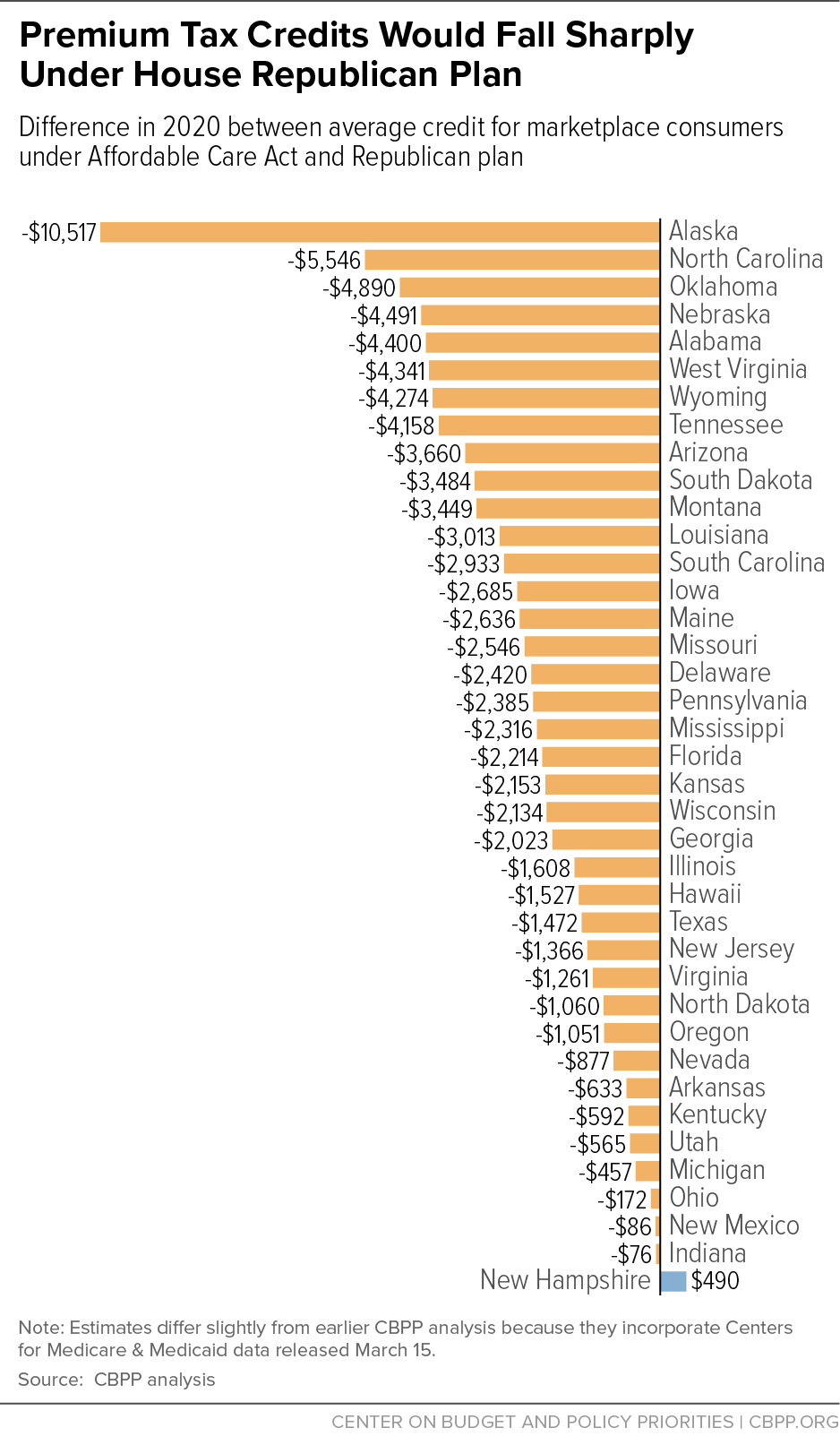

Average tax credits would fall sharply under the House bill, by an average of $2,200 (43 percent) for current marketplace consumers in HealthCare.gov states.[5] Consumers in high-cost states would see especially large losses, exceeding $3,000 in 12 states. In North Carolina, Oklahoma, Alabama, Nebraska, Wyoming, West Virginia, and Tennessee, average tax credit losses would range from $4,200 to $5,500, while Alaska consumers would lose an average of $10,500. (See Figure 2 and Appendix Table 1.)

Losses would also grow over time. Under the ACA, tax credits increase over time as needed to largely shield low- and moderate-income consumers from premium increases. For example, in 2017, pre-credit premiums increased significantly, but net premiums among consumers eligible for tax credits remained flat at $106 per month.[6] Under the House plan, tax credits would grow at the rate of inflation plus 1 percentage point, no matter how quickly premiums rose in a particular year or state. As a result, CBO estimates that average tax credits for subsidized consumers would fall by 40 percent in 2020, but 50 percent by 2026.

The House Bill’s Impact on Net Premiums

The House bill does not offset its reductions in average tax credits with reductions in average premiums. In fact, CBO’s estimates imply that average premiums for current marketplace consumers would increase. As a result, consumers’ net premiums would grow even more than their tax credits would shrink.

Some measures in the House bill would increase premiums, while other measures would reduce them. First, the bill repeals the individual mandate, leading healthier people to drop coverage and raising premiums by 20 percent, all else being equal.[7] Second, the bill includes a Patient and State Stability Fund that provides funding for various measures to reduce premiums.[8] Third, as discussed below, the bill allows insurers to stop offering lower-deductible plans; the resulting drop in plan generosity and increase in deductibles and other out-of-pocket costs lowers premiums.

Using CBO’s estimates of how premiums would change for people of different ages and averaging over the age distribution of marketplace consumers, we find that the House bill would increase average premiums by 4 percent for current marketplace consumers, consistent with a recent Brookings analysis.[9] CBO’s finding that average premiums would decrease by 10 percent reflects its conclusion that older people would be disproportionately likely to drop coverage under the House bill. Since older people have higher costs and premiums, coverage losses for older people mechanically reduce average premiums.

In 2020, a 4 percent increase in average premiums would translate into $270. Taking into account both premium increases and tax credit losses, net premiums for HealthCare.gov marketplace consumers would increase by an average of $2,400. Changes across states would range from a $300 decrease in New Hampshire to an $11,100 increase in Alaska.[10]

Net premium changes also would vary substantially by age and income. Some higher-income and younger marketplace consumers would pay lower net premiums under the House bill, but many lower-income and older consumers would see larger-than-average increases. For example, a 60-year-old with income of $22,000 would see net premiums increase by more than $4,000 in every state, by $8,200 if she faces the national average premium, and by over $10,000 in 12 states (Alaska, North Carolina, Oklahoma, Arizona, Wyoming, Nebraska, West Virginia, Tennessee, Alabama, Montana, South Dakota, and Delaware).[11] (See Appendix Table 2.)

The House Plan’s Impact on Out-of-Pocket and Total Costs

The House bill makes two changes that would increase consumers’ out-of-pocket costs.

First, it repeals (without any substitute) the ACA’s cost-sharing subsidies, which reduce out-of-pocket costs for people with incomes below 250 percent of the poverty line (about $30,000 for a single person, or about $60,000 for a family of four). Under current law, almost 60 percent of marketplace consumers qualify for these subsidies, which entitle them to purchase coverage with lower deductibles and other out-of-pocket costs. Without these subsidies, average marketplace deductibles would increase by about $2,800 for single people with incomes below $18,000, by about $2,300 for single people with incomes between $18,000 and $24,000, and by about $600 for single people with incomes between $24,000 and $30,000.[12] The result is that many lower-income people would have difficulty paying the deductibles and other cost-sharing necessary to use their coverage.

The House bill would also increase deductibles and other out-of-pocket costs for people with incomes above 250 percent of the poverty line, who don’t get cost-sharing subsidies under the ACA. The bill effectively eliminates the ACA’s requirement that insurers offer consumers the choice of a lower-deductible plan, which CBO projects would lead many insurers to offer only high-deductible options. As a result, CBO concludes, “individuals’ cost-sharing payments, including deductibles, in the nongroup market would tend to be higher than those anticipated under current law.”[13] Specifically, CBO estimates that under the House bill, the average actuarial value of marketplace plans — the share of costs covered by the plan, versus by the consumer through deductibles and other cost sharing — would fall to 65 percent, from about 70 percent today. That change would increase average costs by several hundred dollars per marketplace consumer.

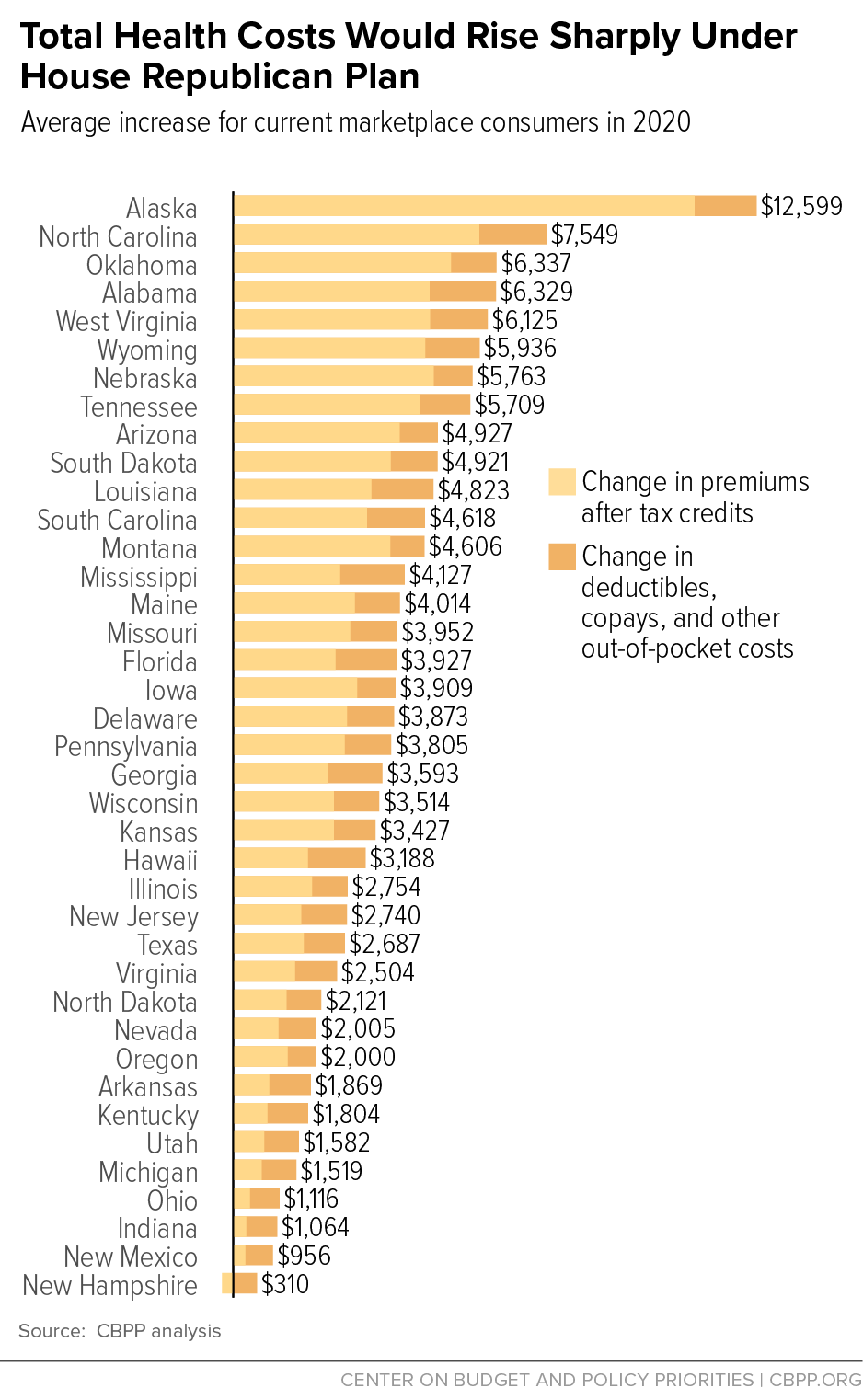

Overall, the House bill increases out-of-pocket costs by an average of $1,200 for current HealthCare.gov state marketplace consumers. These increases are concentrated among people with incomes below 250 percent of the poverty line, who make up the majority of marketplace consumers.

Figure 3 and Appendix Table 1 show the combined impact of the House bill’s increases in net premiums and out-of-pocket costs.[14] Marketplace consumers in every state would see higher costs, on average, with large differences across states. Where two states would see increases in total costs averaging less than $1,000, 24 states would see increases of more than $3,000, 15 states would see increases of more than $4,000, and eight states (Alaska, North Carolina, Oklahoma, Alabama, Wyoming, West Virginia, Nebraska, and Tennessee) would see increases of more than $5,000. In Alaska, total costs for marketplace consumers would go up by $12,600, on average. While higher-income and younger consumers would see lower-than-average increases, or cost decreases, many lower-income and older consumers would see even larger increases than their state averages.

Modified House Bill’s “Reserve Fund” Does Not Solve These Problems

The modified House bill introduced March 20 has essentially the same effects on premiums and out-of-pocket costs as the original legislation. However, House Republicans added a provision, reportedly costing $85 billion, that expands the income tax deduction for out-of-pocket medical expenses. In itself, that provision is worth little or nothing to most of those who are harmed the most by the House bill.[15] But even if the $85 billion were repurposed to pay for higher tax credits for people age 50 and older, marketplace consumers would still see large cost increases. That’s because the House tax credits would remain both underfunded and poorly targeted compared to the ACA’s financial assistance, which adjusts based on both income and the actual cost of health insurance and which helps with both premiums and out-of-pocket costs.

If the $85 billion the House bill dedicates to expanding the income tax deduction for out-of-pocket medical costs were repurposed to increase tax credits for older consumers, we estimate that 2020 credit amounts would increase from $3,500 to $5,100 for people age 50 to 59 and from $4,000 to $5,900 for people 60 and older. Even so:

- Tax credits would still fall sharply. Across HealthCare.gov states, current marketplace consumers would lose an average of $1,500 in tax credits in 2020, compared to $2,200 under the original House bill. And the changes would do even less to mitigate losses in high-cost states: tax credits would fall by more than $3,000 on average in Alaska, North Carolina, Oklahoma, Alabama, Wyoming, West Virginia, Nebraska, Tennessee, and Arizona.

- Out-of-pocket costs would still increase by an average of about $1,200. Increasing tax credits would do nothing to address the House bill’s increases in deductibles, copays, coinsurance, and other out-of-pocket costs. So these costs would still rise, especially for those with incomes below 250 percent of the poverty line.

- Total costs would increase by an average of $2,900 — more than 80 percent as much as under the House bill. As Appendix Table 3 shows, changes in total costs would range from a decrease of $400 in New Hampshire (the least affected state) to an increase of $1,600 in North Dakota (the tenth least affected), $4,300 in Arizona (the tenth most affected), and $12,000 in Alaska (most affected). Cost increases would still be higher in many rural states, as would be the case under almost any approach that does not adjust tax credits based on actual local premiums. (See box.)

- Lower-income older consumers would still be hit the hardest. Net premiums would increase by $1,500 for a 45-year-old with income of $22,000 (roughly the median age and income of marketplace consumers), supposing she faced the national average premium. For a 60-year-old with the same income, net premiums would increase by $6,300, a six-fold increase that would leave this consumer paying more than one-third of income in premiums. (See Figure 4.) As Appendix Table 4 shows, net premium increases for this consumer would range from $2,600 to $26,900 across states. In Alaska, North Carolina, Oklahoma, Arizona, Wyoming, and Nebraska net premiums would increase by more than $10,000. Older, lower-income consumers would also see their deductibles and other out-of-pocket costs increase sharply due to the bill’s elimination of cost-sharing subsidies.

CBO’s analysis of the original House bill concluded that about 10 million people would lose private coverage[16] and uninsured rates would rise for young, middle-aged, and older people both below and above 200 percent of the federal poverty line. Since the modified House bill has almost the same effects as the original bill on coverage affordability, it would likely result in very similar private coverage losses. Even among those who could maintain their coverage, many would face burdensome premium increases and large increases in cost sharing that could keep them from accessing needed health care.

House Bill Raises Costs More for Rural Consumers

States with high rural populations would see disproportionately large cuts in tax credits and increases in costs under the modified House bill. In 12 of the 15 states that would see the steepest increases in total costs, rural residents make up at least one-quarter of marketplace enrollees today, above the HealthCare.gov average of 18 percent. For example, in Wyoming, which has the highest rural share of marketplace enrollees (78 percent), a consumer’s total costs would rise by $5,900, on average.

Even within a given state, rural consumers would often fare worse than urban ones, county-level data from the Kaiser Family Foundation show.a In urban Memphis (Shelby County), Tennessee, a 40-year-old earning $30,000 would get a $3,000 tax credit under the House plan, or $450 less than under current law. But in the rural counties to the north, like Gibson or Madison County, that $3,000 credit would be $3,500 less than what the ACA would provide.

That gap between urban and rural consumers is almost unbridgeable without restoring the ACA’s approach of basing financial assistance on actual local costs. The ACA’s tax credits are tied to the cost of an available marketplace plan where an individual lives. In contrast, the House tax credit wouldn’t adjust for geographic differences in premiums. That particularly hurts consumers in rural states and rural areas, where premiums tend to be higher because low population density often raises medical costs and contributes to a limited array of providers and little competition among insurers.b

Non-metropolitan areas saw a dramatic 25 percent reduction in their uninsured rate between 2013 and 2015 under the ACA, but those gains — like the overall gains in uninsured rates nationwide — would likely be erased under the House plan.c

a Kaiser Family Foundation, “Premiums and Tax Credits Under the Affordable Care Act vs. the American Health Care Act: Interactive Maps,” March 21, 2017, http://kff.org/interactive/tax-credits-under-the-affordable-care-act-vs-replacement-proposal-interactive-map/.

b Abigail Barker, et al., “Health Insurance Marketplaces: Premium Trends in Rural Areas,” Center for Rural Policy Analysis, May 2016, http://cph.uiowa.edu/rupri/publications/policybriefs/2016/HIMs%20rural%20premium%20trends.pdf.

c See Census Bureau estimates for 2015, https://www.census.gov/content/dam/Census/library/publications/2016/demo/p60-257.pdf.

Appendix: Methodology

Our projections for premiums, tax credits, and out-of-pocket costs under the ACA and the House bill draw on data on actual premiums, tax credits, cost-sharing reduction payments, and consumer demographics by state in 2016 and 2017 from the Department of Health and Human Services (HHS) and projections for future years and the House bill from CBO and the CMS Office of the Actuary.

Premiums. We obtain data on 2017 average and benchmark marketplace premiums by state from the Department of Health and Human Services.[17] To project premiums for 2020, we inflate 2017 premiums to 2020 using National Health Expenditure (NHE) projections from the CMS Office of the Actuary.[18] To project premiums under the House bill for different age groups, we follow the approach described in a recent Brookings analysis to convert CBO’s estimated changes in premiums for people age 21, 40, and 64 into a complete forecast of premium changes by age under the House bill.[19] We compute the change in the average premium for current marketplace consumers by computing average current-law and House-bill premiums using the current marketplace age distribution. We assume that the percentage increases in premiums under the House bill are the same across states.

Tax credits. We obtain data on 2017 average premium tax credits by state from CMS.[20] We inflate these tax credits to 2020 based on CBO’s projected growth in average premium tax credits.[21] We then compute tax credits under the House plan in 2020 based on the age distribution of each state’s 2017 marketplace plan selections.[22] To calculate tax credits for hypothetical consumers, we follow the approach used in a recent Kaiser Family Foundation analysis.[23] Specifically, we inflate the ACA’s required premium contributions using the ratio of growth in employer-sponsored insurance spending per enrollee and GDP per capita from the NHE and inflate federal poverty guidelines using consumer price index projections from CBO. For hypothetical consumer examples, we assume consumers face premiums equal to the average benchmark (second-lowest-cost silver plan) premium in their state.

Out-of-pocket cost increases. We obtain data on 2016 average cost-sharing reductions by state from HHS and on the share of consumers eligible for cost-sharing reductions in 2017 from CMS.[24] We inflate cost-sharing reductions to 2020 based on CBO’s projected growth in average cost-sharing reduction amounts. To calculate the additional increase in cost sharing due to the reduction in plan actuarial value, we compare CBO’s estimate of the average actuarial value under the House bill (65 percent) to average actuarial values across states in 2015 (the latest data available); the average actuarial value in most states was close to 70 percent.[25] We calculate the expected out-of-pocket cost increase from reducing actuarial value from (for example) 70 to 65 percent as 5%*state average premium*80% (where the 80% factor approximates the share of the plan premium that pays for administrative versus claims costs).

Accounting for the House bill “reserve fund.” The modified House bill includes a provision that would expand the existing income tax deduction for out-of-pocket medical expenses. According to news accounts, this provision costs $85 billion over ten years; House Republicans have suggested that funding could be repurposed to provide higher tax credits for people 50 and older. For our analysis of this reserve fund, we assume the $85 billion would be used to increase the House bill tax credit amounts for people age 50 to 59 and 60 and older. $85 billion represents a 24 percent increase in funding for the House bill tax credits, and, based on the age distribution of current marketplace consumers, about half of the cost of these tax cuts goes to people age 50 and older. Thus, the reserve fund would allow for a nearly 50 percent increase in tax credit amounts for these consumers. In 2020, tax credit amounts would increase from $3,500 to $5,144 for people age 50 to 59 and from $4,000 to $5,879 for people age 60 and older.

| APPENDIX TABLE 1 | |||||

|---|---|---|---|---|---|

| Changes in Total Costs For Marketplace Consumers Under House Republican Proposal Projections for 2020 for HealthCare.gov States; Average Across Current Marketplace Consumers, Compared to Current Law (ACA) | |||||

| Changes in Premiums | Cost Sharing Increase | Change in Total Costs | |||

| AHCA Premium Increase* | Change in Tax Credits | Change in Enrollee Premium | |||

| Alaska | 589 | -10,517 | 11,106 | 1,493 | 12,599 |

| North Carolina | 375 | -5,546 | 5,921 | 1,628 | 7,549 |

| Oklahoma | 351 | -4,890 | 5,241 | 1,096 | 6,337 |

| Alabama | 325 | -4,400 | 4,725 | 1,604 | 6,329 |

| West Virginia | 397 | -4,341 | 4,738 | 1,387 | 6,125 |

| Wyoming | 348 | -4,274 | 4,622 | 1,314 | 5,936 |

| Nebraska | 337 | -4,491 | 4,828 | 935 | 5,763 |

| Tennessee | 332 | -4,158 | 4,491 | 1,218 | 5,709 |

| Arizona | 346 | -3,660 | 4,006 | 921 | 4,927 |

| South Dakota | 306 | -3,484 | 3,790 | 1,130 | 4,921 |

| Louisiana | 313 | -3,013 | 3,325 | 1,498 | 4,823 |

| South Carolina | 290 | -2,933 | 3,223 | 1,395 | 4,618 |

| Montana | 329 | -3,449 | 3,778 | 828 | 4,606 |

| Mississippi | 258 | -2,316 | 2,573 | 1,554 | 4,127 |

| Maine | 293 | -2,636 | 2,929 | 1,086 | 4,014 |

| Missouri | 273 | -2,546 | 2,819 | 1,133 | 3,952 |

| Florida | 250 | -2,214 | 2,465 | 1,462 | 3,927 |

| Iowa | 298 | -2,685 | 2,983 | 926 | 3,909 |

| Delaware | 322 | -2,420 | 2,742 | 1,131 | 3,873 |

| Pennsylvania | 302 | -2,385 | 2,687 | 1,118 | 3,805 |

| Georgia | 244 | -2,023 | 2,266 | 1,327 | 3,593 |

| Wisconsin | 291 | -2,134 | 2,425 | 1,089 | 3,514 |

| Kansas | 269 | -2,153 | 2,422 | 1,005 | 3,427 |

| Hawaii | 270 | -1,527 | 1,797 | 1,391 | 3,188 |

| Illinois | 293 | -1,608 | 1,901 | 853 | 2,754 |

| New Jersey | 271 | -1,366 | 1,637 | 1,103 | 2,740 |

| Texas | 228 | -1,472 | 1,700 | 987 | 2,687 |

| Virginia | 229 | -1,261 | 1,491 | 1,014 | 2,504 |

| North Dakota | 226 | -1,060 | 1,286 | 835 | 2,121 |

| Nevada | 214 | -877 | 1,091 | 913 | 2,005 |

| Oregon | 262 | -1,051 | 1,313 | 687 | 2,000 |

| Arkansas | 238 | -633 | 871 | 998 | 1,869 |

| Kentucky | 230 | -592 | 822 | 982 | 1,804 |

| Utah | 181 | -565 | 745 | 836 | 1,582 |

| Michigan | 228 | -457 | 684 | 834 | 1,519 |

| Ohio | 234 | -172 | 406 | 710 | 1,116 |

| Indiana | 238 | -76 | 314 | 749 | 1,064 |

| New Mexico | 207 | -86 | 293 | 663 | 956 |

| New Hampshire | 226 | 490 | -264 | 575 | 310 |

| HealthCare.gov state average | 269 | -2,169 | 2,439 | 1,170 | 3,609 |

| APPENDIX TABLE 2 | |||||||

|---|---|---|---|---|---|---|---|

| Premiums Accounting for Tax Credits for Marketplace Consumers Under Current Law (ACA) and House Republican Plan | |||||||

| Premiums Accounting for Tax Credits for Consumers with Incomes of $22,000 (2020) Assumes Consumers Face Their State Average Benchmark Premiums |

|||||||

| 45-Year-Old | 60-Year-Old | ||||||

| Net Premium | Net Premium | ||||||

| ACA | House | Change in Premiums | ACA | House | Change in Premiums | ||

| Alabama | 1,183 | 4,237 | 3,054 | 1,183 | 12,974 | 11,791 | |

| Alaska | 784 | 11,323 | 10,540 | 784 | 29,593 | 28,810 | |

| Arizona | 1,183 | 4,953 | 3,771 | 1,183 | 14,653 | 13,470 | |

| Arkansas | 1,183 | 1,674 | 491 | 1,183 | 6,962 | 5,779 | |

| Delaware | 1,183 | 3,540 | 2,357 | 1,183 | 11,338 | 10,155 | |

| Florida | 1,183 | 2,089 | 906 | 1,183 | 7,935 | 6,752 | |

| Georgia | 1,183 | 2,145 | 962 | 1,183 | 8,067 | 6,884 | |

| Hawaii | 940 | 2,428 | 1,487 | 940 | 8,730 | 7,790 | |

| Illinois | 1,183 | 2,616 | 1,434 | 1,183 | 9,172 | 7,989 | |

| Indiana | 1,183 | 1,316 | 133 | 1,183 | 6,122 | 4,939 | |

| Iowa | 1,183 | 2,805 | 1,622 | 1,183 | 9,614 | 8,431 | |

| Kansas | 1,183 | 2,805 | 1,622 | 1,183 | 9,614 | 8,431 | |

| Kentucky | 1,183 | 1,881 | 699 | 1,183 | 7,448 | 6,266 | |

| Louisiana | 1,183 | 3,408 | 2,225 | 1,183 | 11,029 | 9,846 | |

| Maine | 1,183 | 2,974 | 1,792 | 1,183 | 10,012 | 8,829 | |

| Michigan | 1,183 | 1,297 | 114 | 1,183 | 6,078 | 4,895 | |

| Mississippi | 1,183 | 2,145 | 962 | 1,183 | 8,067 | 6,884 | |

| Missouri | 1,183 | 2,748 | 1,565 | 1,183 | 9,482 | 8,299 | |

| Montana | 1,183 | 4,181 | 2,998 | 1,183 | 12,841 | 11,658 | |

| Nebraska | 1,183 | 4,746 | 3,563 | 1,183 | 14,167 | 12,984 | |

| Nevada | 1,183 | 1,693 | 510 | 1,183 | 7,006 | 5,823 | |

| New Hampshire | 1,183 | 1,127 | -55 | 1,183 | 5,680 | 4,497 | |

| New Jersey | 1,183 | 2,390 | 1,207 | 1,183 | 8,642 | 7,459 | |

| New Mexico | 1,183 | 1,222 | 39 | 1,183 | 5,901 | 4,718 | |

| North Carolina | 1,183 | 5,406 | 4,223 | 1,183 | 15,714 | 14,531 | |

| North Dakota | 1,183 | 2,428 | 1,245 | 1,183 | 8,730 | 7,547 | |

| Ohio | 1,183 | 1,259 | 77 | 1,183 | 5,990 | 4,807 | |

| Oklahoma | 1,183 | 4,991 | 3,808 | 1,183 | 14,742 | 13,559 | |

| Oregon | 1,183 | 2,409 | 1,226 | 1,183 | 8,686 | 7,503 | |

| Pennsylvania | 1,183 | 3,163 | 1,980 | 1,183 | 10,454 | 9,271 | |

| South Carolina | 1,183 | 3,012 | 1,829 | 1,183 | 10,100 | 8,918 | |

| South Dakota | 1,183 | 4,049 | 2,866 | 1,183 | 12,531 | 11,349 | |

| Tennessee | 1,183 | 4,256 | 3,073 | 1,183 | 13,018 | 11,835 | |

| Texas | 1,183 | 1,919 | 736 | 1,183 | 7,537 | 6,354 | |

| Utah | 1,183 | 2,541 | 1,358 | 1,183 | 8,995 | 7,813 | |

| Virginia | 1,183 | 1,976 | 793 | 1,183 | 7,669 | 6,487 | |

| West Virginia | 1,183 | 4,275 | 3,092 | 1,183 | 13,062 | 11,879 | |

| Wisconsin | 1,183 | 2,729 | 1,547 | 1,183 | 9,437 | 8,255 | |

| Wyoming | 1,183 | 4,784 | 3,601 | 1,183 | 14,255 | 13,073 | |

| HealthCare.gov states* | 1,183 | 2,692 | 1,509 | 1,183 | 9,349 | 8,166 | |

| APPENDIX TABLE 3 | ||||||

|---|---|---|---|---|---|---|

| Changes in Total Costs For Marketplace Consumers Under House Republican Proposal, Assuming Larger Tax Credits for Older People, Compared to Current Law (ACA) | ||||||

| Projections for 2020 for HealthCare.gov States; Average Across Current Marketplace Consumers Assumes $85 Billion Additional Funding for Tax Credits for People Age 50 and Older |

||||||

| AHCA Premium Increase* | Change in Tax Credits | Change in Enrollee Premium | Cost Sharing Increase | Change in Total Costs | Total Cost Increase Compared to Original House Plan | |

| Alaska | 589 | -9,886 | 10,476 | 1,493 | 11,968 | 95% |

| North Carolina | 375 | -4,936 | 5,311 | 1,628 | 6,938 | 92% |

| Oklahoma | 351 | -4,263 | 4,614 | 1,096 | 5,710 | 90% |

| Alabama | 325 | -3,754 | 4,080 | 1,604 | 5,683 | 90% |

| Wyoming | 348 | -3,656 | 4,004 | 1,314 | 5,318 | 90% |

| West Virginia | 397 | -3,484 | 3,881 | 1,387 | 5,268 | 86% |

| Nebraska | 337 | -3,917 | 4,254 | 935 | 5,189 | 90% |

| Tennessee | 332 | -3,449 | 3,781 | 1,218 | 4,999 | 88% |

| South Dakota | 306 | -2,901 | 3,207 | 1,130 | 4,338 | 88% |

| Arizona | 346 | -3,025 | 3,370 | 921 | 4,292 | 87% |

| Louisiana | 313 | -2,352 | 2,665 | 1,498 | 4,163 | 86% |

| South Carolina | 290 | -2,267 | 2,557 | 1,395 | 3,952 | 86% |

| Montana | 329 | -2,733 | 3,062 | 828 | 3,890 | 84% |

| Mississippi | 258 | -1,621 | 1,879 | 1,554 | 3,432 | 83% |

| Missouri | 273 | -1,893 | 2,166 | 1,133 | 3,299 | 83% |

| Maine | 293 | -1,905 | 2,198 | 1,086 | 3,283 | 82% |

| Florida | 250 | -1,565 | 1,816 | 1,462 | 3,278 | 83% |

| Delaware | 322 | -1,742 | 2,064 | 1,131 | 3,195 | 82% |

| Iowa | 298 | -1,892 | 2,190 | 926 | 3,116 | 80% |

| Pennsylvania | 302 | -1,641 | 1,943 | 1,118 | 3,061 | 80% |

| Georgia | 244 | -1,434 | 1,677 | 1,327 | 3,004 | 84% |

| Kansas | 269 | -1,520 | 1,789 | 1,005 | 2,795 | 82% |

| Wisconsin | 291 | -1,363 | 1,654 | 1,089 | 2,743 | 78% |

| Hawaii | 270 | -787 | 1,057 | 1,391 | 2,448 | 77% |

| Texas | 228 | -874 | 1,102 | 987 | 2,089 | 78% |

| Illinois | 293 | -913 | 1,206 | 853 | 2,059 | 75% |

| New Jersey | 271 | -680 | 950 | 1,103 | 2,054 | 75% |

| Virginia | 229 | -670 | 900 | 1,014 | 1,913 | 76% |

| North Dakota | 226 | -521 | 747 | 835 | 1,583 | 75% |

| Nevada | 214 | -240 | 454 | 913 | 1,367 | 68% |

| Oregon | 262 | -339 | 600 | 687 | 1,288 | 64% |

| Utah | 181 | -193 | 374 | 836 | 1,210 | 77% |

| Arkansas | 238 | 98 | 139 | 998 | 1,137 | 61% |

| Kentucky | 230 | 126 | 104 | 982 | 1,086 | 60% |

| Michigan | 228 | 239 | -11 | 834 | 823 | 54% |

| Ohio | 234 | 567 | -333 | 710 | 377 | 34% |

| Indiana | 238 | 643 | -405 | 749 | 344 | 32% |

| New Mexico | 207 | 720 | -513 | 663 | 150 | 16% |

| New Hampshire | 226 | 1,236 | -1,010 | 575 | -435 | NA |

| HealthCare.gov state average | 269 | -1,478 | 1,748 | 1,170 | 2,918 | 81% |

| APPENDIX TABLE 4 | |||||||

|---|---|---|---|---|---|---|---|

| Appendix Table 4: Premiums Accounting for Tax Credits for Marketplace Consumers Under Current Law (ACA) and House Republican Plan, Assuming Larger Tax Credits for Older People | |||||||

| Premiums Accounting for Tax Credits for Consumers with Incomes of $22,000 (2020) Assume Consumers Face Their State Average Benchmark Premiums Assumes $85 Billion Additional Funding for Tax Credits for People Age 50 and Older |

|||||||

| 45-Year-Old | 60-Year-Old | ||||||

| Net Premium | Change in Premiums | Net Premium | Change in Premiums | ||||

| ACA | House | ACA | House | ||||

| Alabama | 1,183 | 4,237 | 3,054 | 1,183 | 11,094 | 9,912 | |

| Alaska | 784 | 11,323 | 10,540 | 784 | 27,714 | 26,930 | |

| Arizona | 1,183 | 4,953 | 3,771 | 1,183 | 12,774 | 11,591 | |

| Arkansas | 1,183 | 1,674 | 491 | 1,183 | 5,083 | 3,900 | |

| Delaware | 1,183 | 3,540 | 2,357 | 1,183 | 9,459 | 8,276 | |

| Florida | 1,183 | 2,089 | 906 | 1,183 | 6,055 | 4,873 | |

| Georgia | 1,183 | 2,145 | 962 | 1,183 | 6,188 | 5,005 | |

| Hawaii | 940 | 2,428 | 1,487 | 940 | 6,851 | 5,910 | |

| Illinois | 1,183 | 2,616 | 1,434 | 1,183 | 7,293 | 6,110 | |

| Indiana | 1,183 | 1,316 | 133 | 1,183 | 4,243 | 3,060 | |

| Iowa | 1,183 | 2,805 | 1,622 | 1,183 | 7,735 | 6,552 | |

| Kansas | 1,183 | 2,805 | 1,622 | 1,183 | 7,735 | 6,552 | |

| Kentucky | 1,183 | 1,881 | 699 | 1,183 | 5,569 | 4,386 | |

| Louisiana | 1,183 | 3,408 | 2,225 | 1,183 | 9,149 | 7,967 | |

| Maine | 1,183 | 2,974 | 1,792 | 1,183 | 8,133 | 6,950 | |

| Michigan | 1,183 | 1,297 | 114 | 1,183 | 4,199 | 3,016 | |

| Mississippi | 1,183 | 2,145 | 962 | 1,183 | 6,188 | 5,005 | |

| Missouri | 1,183 | 2,748 | 1,565 | 1,183 | 7,602 | 6,420 | |

| Montana | 1,183 | 4,181 | 2,998 | 1,183 | 10,962 | 9,779 | |

| Nebraska | 1,183 | 4,746 | 3,563 | 1,183 | 12,288 | 11,105 | |

| Nevada | 1,183 | 1,693 | 510 | 1,183 | 5,127 | 3,944 | |

| New Hampshire | 1,183 | 1,127 | -55 | 1,183 | 3,801 | 2,618 | |

| New Jersey | 1,183 | 2,390 | 1,207 | 1,183 | 6,763 | 5,580 | |

| New Mexico | 1,183 | 1,222 | 39 | 1,183 | 4,022 | 2,839 | |

| North Carolina | 1,183 | 5,406 | 4,223 | 1,183 | 13,835 | 12,652 | |

| North Dakota | 1,183 | 2,428 | 1,245 | 1,183 | 6,851 | 5,668 | |

| Ohio | 1,183 | 1,259 | 77 | 1,183 | 4,110 | 2,928 | |

| Oklahoma | 1,183 | 4,991 | 3,808 | 1,183 | 12,862 | 11,680 | |

| Oregon | 1,183 | 2,409 | 1,226 | 1,183 | 6,807 | 5,624 | |

| Pennsylvania | 1,183 | 3,163 | 1,980 | 1,183 | 8,575 | 7,392 | |

| South Carolina | 1,183 | 3,012 | 1,829 | 1,183 | 8,221 | 7,038 | |

| South Dakota | 1,183 | 4,049 | 2,866 | 1,183 | 10,652 | 9,469 | |

| Tennessee | 1,183 | 4,256 | 3,073 | 1,183 | 11,138 | 9,956 | |

| Texas | 1,183 | 1,919 | 736 | 1,183 | 5,657 | 4,475 | |

| Utah | 1,183 | 2,541 | 1,358 | 1,183 | 7,116 | 5,933 | |

| Virginia | 1,183 | 1,976 | 793 | 1,183 | 5,790 | 4,607 | |

| West Virginia | 1,183 | 4,275 | 3,092 | 1,183 | 11,183 | 10,000 | |

| Wisconsin | 1,183 | 2,729 | 1,547 | 1,183 | 7,558 | 6,375 | |

| Wyoming | 1,183 | 4,784 | 3,601 | 1,183 | 12,376 | 11,193 | |

| HealthCare.gov state average | 1,183 | 2,692 | 1,509 | 1,183 | 7,470 | 6,287 | |

End Notes

[1] Press accounts vary as to whether the House bill “reserve fund” is $75 billion or $85 billion and whether that amount refers just to the enhanced income tax deduction for medical expenses or also includes the cost of other provisions added to the bill as part of the manager’s amendment. This paper uses the highest estimate reported – $85 billion – thereby portraying the House bill in the most favorable possible light. See Mike DeBonis, “House Republicans Unveil Changes to Their Health-Care Bill,” Washington Post, March 20, 2017, https://www.washingtonpost.com/powerpost/trump-to-visit-capitol-tuesday-urge-house-republicans-to-vote-for-health-bill/2017/03/20/4d93f9ac-0d8c-11e7-9b0d-d27c98455440_story.html?utm_term=.3a2bec418859. See also the joint Energy and Commerce Committee and Ways and Means Committee press release: “House Republicans Announce Updates to Strengthen American Health Care Act,” March 20, 2017, https://energycommerce.house.gov/news-center/press-releases/house-republicans-announce-updates-strengthen-american-health-care-act.

[2] On March 15, the Centers for Medicare & Medicaid Services released data on premiums, tax credits, and consumer demographics covering the full 2017 open enrollment period. Previously, we relied on estimates covering the first eight weeks of open enrollment. For our earlier analysis, see Aviva Aron-Dine and Tara Straw, “House Tax Credits Would Make Health Insurance Far Less Affordable in High-Cost States,” Center on Budget and Policy Priorities, revised March 16, 2017, https://www.cbpp.org/research/health/house-tax-credits-would-make-health-insurance-far-less-affordable-in-high-cost.

[3] David Cutler, Topher Spiro, and Emily Gee, “The Impact of the House ACA Repeal Bill on Enrollees’ Costs,” Center for American Progress, March 16, 2017, https://www.americanprogress.org/issues/healthcare/reports/2017/03/16/428418/impact-house-aca-repeal-bill-enrollees-costs/.

[4] The House tax credits phase out starting at an income of $75,000 ($150,000 for a married couple filing jointly). By ignoring these phaseouts, the calculations in this paper very slightly understate reductions in average tax credits for current marketplace consumers under the House bill.

[5] A Kaiser Family Foundation analysis estimates that tax credits nationwide would fall by an average of $1,700 for current marketplace consumers, compared with our estimate of $2,200 for consumers in HealthCare.gov states. On average, HealthCare.gov states have higher premiums and more lower-income consumers, resulting in higher tax credits under the ACA. Cynthia Cox, Gary Claxton, and Larry Levitt, “How Affordable Care Act Repeal and Replace Plans Might Shift Health Insurance Tax Credits,” Kaiser Family Foundation, March 10, 2017, http://kff.org/health-reform/issue-brief/how-affordable-care-act-repeal-and-replace-plans-might-shift-health-insurance-tax-credits/.

[6] Centers for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period,” March 15, 2017, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-03-15.html.

[7] Congressional Budget Office, “Repeal the Individual Mandate,” December 8, 2016, https://www.cbo.gov/budget-options/2016/52232.

[8] See Sarah Lueck, “House Republican Plan Needs $100 Billion Fund to Maintain Individual Insurance Market,” Center on Budget and Policy Priorities, March 15, 2017, https://www.cbpp.org/blog/house-republican-plan-needs-100-billion-fund-to-maintain-individual-insurance-market.

[9] Matthew Fiedler and Loren Adler, “How Will House GOP Plan Affect Individual Market Premiums?” Brookings Institution, March 16, 2017, https://www.brookings.edu/blog/up-front/2017/03/16/how-will-the-house-gop-health-care-bill-affect-individual-market-premiums/.

[10] These estimates assume that average premiums would increase by 4 percent in all states under the House bill. In reality, high-cost states would likely see larger premium increases, on average, while some low-cost states would likely see premium decreases. That’s because the large cuts to tax credits in high-cost states would themselves tend to drive premiums up. As CBO explained in analyzing an earlier Republican ACA repeal bill, if subsidies are insufficient to make coverage affordable, “not only would enrollment decline, but the people who would be most likely to remain enrolled would tend to be less healthy (and therefore more willing to pay higher premiums). Thus, average health care costs among the people retaining coverage would be higher, and insurers would have to raise premiums in the nongroup market to cover these high costs.” Should that happen, the differences in the House plan’s impact across states would be even greater than these figures show. Congressional Budget Office, “How Repealing Portions of the Affordable Care Act Would Affect Health Insurance Coverage and Premiums,” January 17, 2017, https://www.cbo.gov/sites/default/files/115th-congress-2017-2018/reports/52371-coverageandpremiums.pdf.

[11] These and other examples assume consumers face the average benchmark (second-lowest-cost silver) premium in their state.

[12] Commonwealth Fund, “The ACA’s Cost-Sharing Reduction Plans: A Key to Affordable Health Coverage for Millions of U.S. Workers,” October 13, 2016, http://www.commonwealthfund.org/publications/issue-briefs/2016/oct/aca-cost-sharing-reduction-plans.

[13] Congressional Budget Office, “Cost Estimate for the American Health Care Act,” March 13, 2017, https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/americanhealthcareact.pdf.

[14] The increase in total costs can also be thought of as the additional amount consumers would have to pay in premiums in order to maintain coverage as generous as their current plan.

[15] Robert Greenstein, “Commentary: The House Republican Health Bill — A Test for Members,” Center on Budget and Policy Priorities, March 22, 2017, https://www.cbpp.org/health/commentary-the-house-republican-health-bill-a-test-for-members.

[16] In 2020, CBO estimates a net coverage loss of 9 million in the non-group market. By 2026, CBO estimates a net coverage loss of only 2 million in the non-group market, but that likely reflects the combined impact of about 9 million people losing non-group coverage and about 7 million people moving from employer-sponsored to individual-market coverage.

[17] Data on benchmark premiums are from “Health Plan Choice and Premiums in the 2017 Health Insurance Marketplace,” Department of Health and Human Services Office of the Assistant Secretary for Planning and Evaluation, October 24, 2016, https://aspe.hhs.gov/system/files/pdf/212721/2017MarketplaceLandscapeBrief.pdf. Data on average premiums are from Centers for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period,” March 15, 2017, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2017-Fact-Sheet-items/2017-03-15.html.

[18] Premium growth-rate projections are from Office of the Actuary in the Centers for Medicare & Medicaid Services, National Health Expenditure Projections, 2016-2025, https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsProjected.html.

[19] Matthew Fiedler and Loren Adler, “How Will House GOP Plan Affect Individual Market Premiums?”

[20] Center for Medicare & Medicaid Services, “Health Insurance Marketplaces 2017 Open Enrollment Period.”

[21] Congressional Budget Office, “Federal Subsidies Under the Affordable Care Act for Health Insurance Coverage Related to the Expansion of Medicaid and Nongroup Health Insurance: Tables from CBO’s January 2017 Baseline,” https://www.cbo.gov/sites/default/files/recurringdata/51298-2017-01-healthinsurance.pdf.

[22] CMS provides data on the number of consumers under age 25, 25-34, 35-44, 45-54, 55-64, and 65 and older. To approximate the number of consumers in each of the House tax credit’s age categories, we assume a uniform age distribution within the CMS age groups.

[23] Cynthia Cox, Gary Claxton, and Larry Levitt, “How Affordable Care Act Repeal and Replace Plans Might Shift Health Insurance Tax Credits,” Kaiser Family Foundation, March 10, 2017, http://kff.org/health-reform/issue-brief/how-affordable-care-act-repeal-and-replace-plans-might-shift-health-insurance-tax-credits/.

[24] Department of Health and Human Services Assistant Secretary for Planning and Evaluation, “Health Insurance Marketplace Cost Sharing Reduction Subsidies by Zip Code and County for 2016,” https://aspe.hhs.gov/health-insurance-marketplace-cost-sharing-reduction-subsidies-zip-code-and-county-2016 and Centers for Medicare & Medicaid Services, “March 31 2016 Effectuated Enrollment Report,” June 30, 2016, https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-06-30.html.

[25] Centers for Medicare & Medicaid Services, “Summary Report on Transitional Reinsurance Payments and Permanent Risk Adjustment Transfers for the 2015 Benefit Year: Appendix A,” June 30, 2016, https://www.cms.gov/CCIIO/Programs-and-Initiatives/Premium-Stabilization-Programs/.

More from the Authors

Areas of Expertise